Modelling the long-run economic impacts of a stylised US tariff increase: technical paper

This paper uses the Scottish Government Computable General Equilibrium (CGE) model to assess the long-run economic impacts of a stylised 10% tariff increase by the United States on UK goods exports.

Results

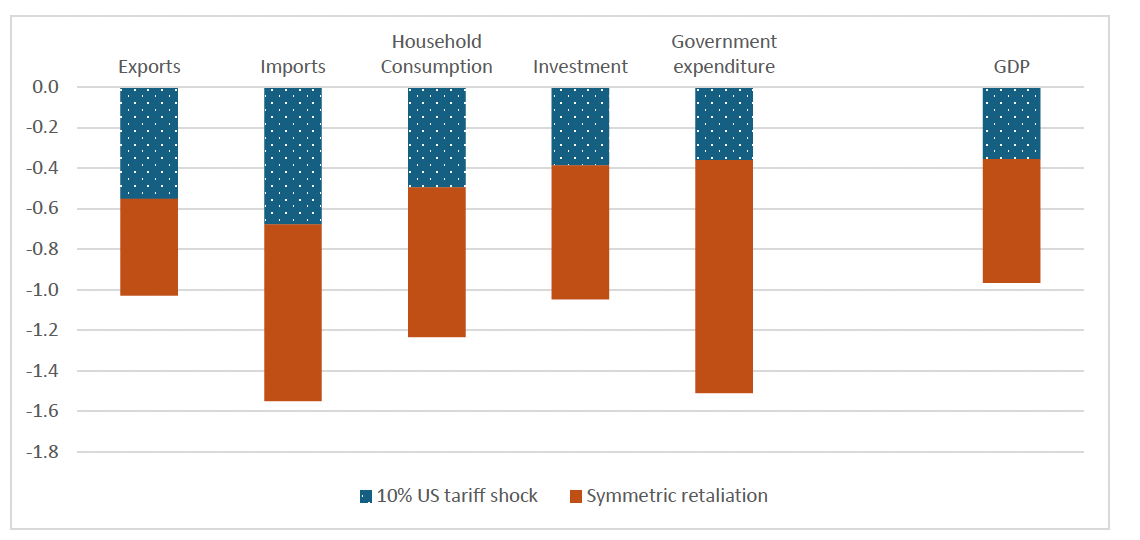

The 10% US-UK tariff increase simulation results in a long-run reduction in Scotland’s GDP of approximately 0.4%. The shock to the rUK economy accounts for around a third of the impact on Scotland’s GDP, highlighting the importance of interregional linkages.

A tariff shock on non-EU exports reduces Scotland’s competitiveness, leading to a fall in export demand and total output. This contraction lowers firms’ demand for labour, resulting in higher unemployment and reduced household incomes. As consumption declines, firm revenues fall, discouraging investment. The government also experiences a drop in tax revenues, which under a balanced budget assumption reduces government spending, amplifying the overall economic downturn.

If the UK retaliates by imposing a 10% tariff increase on imports from the US, the economic impact deepens. This retaliation introduces demand and supply side shocks alongside the initial demand-side contraction. On the demand side, higher import prices reduce household and business incomes, reducing household consumption and business investment. On the supply side, increased input costs, especially in sectors reliant on imported goods, raise production costs and suppress output.

Source: OCEA modelling

These retaliation findings are consistent with those of Figus et al. (2017)[8], who demonstrate that comparable import price shocks lead to more severe GDP and employment losses than export price shocks in a UK CGE model under WTO-style tariff assumptions. Their results identify the harmful effects of tariff retaliation, particularly when imported inputs are essential to domestic production.

The 10% US tariff shock has a compounding effect on Scotland’s economy over time. Initially modest, the impact increases as falling demand reduces firm profitability, leading to lower wages, household income and consumption. This weakens overall demand further, putting more downward pressure on employment, investment, and wages until a new equilibrium is reached.

While the shock to rUK exports is bigger than Scotland’s, the net impact on GDP is very similar.

|

Variable |

Short-run |

5 years |

10 years |

Long-run |

rUK long run |

|---|---|---|---|---|---|

|

GDP |

-0.06 |

-0.23 |

-0.33 |

-0.36 |

-0.34 |

|

Exports |

-0.40 |

-0.45 |

-0.53 |

-0.55 |

-0.70 |

|

Imports |

-0.52 |

-0.64 |

-0.67 |

-0.68 |

-1.06 |

|

Employment |

-0.02 |

-0.17 |

-0.24 |

-0.26 |

-0.25 |

|

Real wage |

-0.03 |

-0.29 |

-0.41 |

-0.44 |

-0.44 |

|

Household consumption |

-0.33 |

-0.41 |

-0.48 |

-0.50 |

-0.48 |

|

Investment |

-0.25 |

-0.56 |

-0.44 |

-0.39 |

-0.37 |

|

Government expenditure |

0.36 |

-0.09 |

-0.30 |

-0.36 |

-0.57 |

Source: OCEA modelling

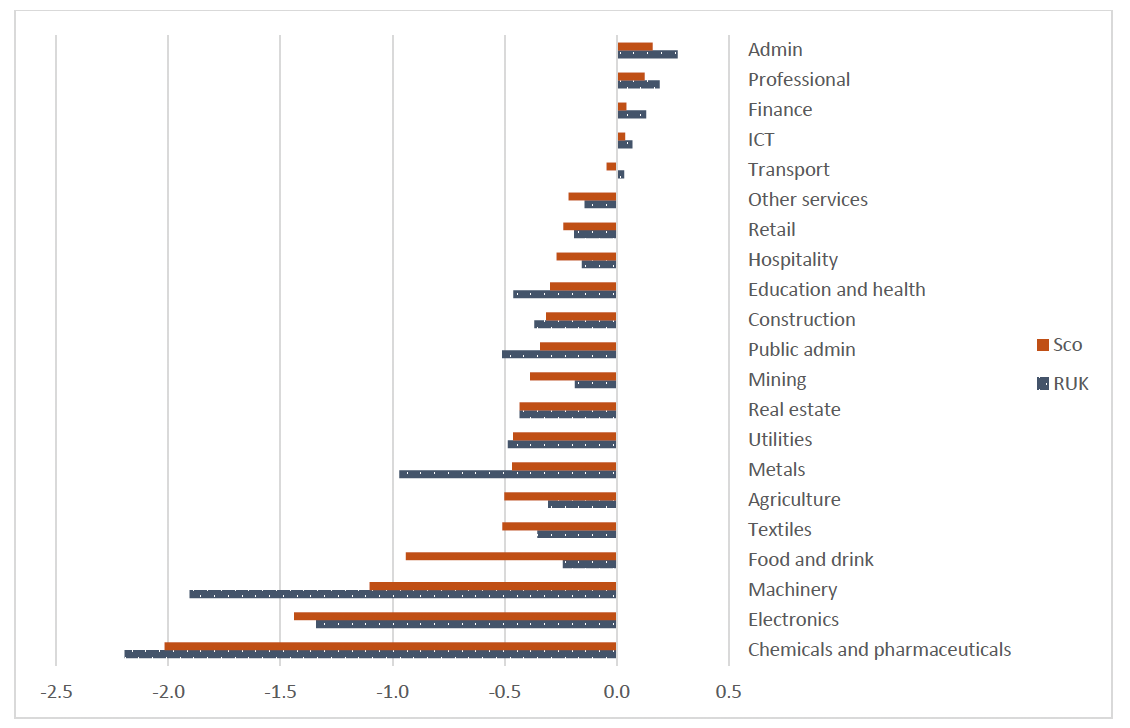

Sectors for which US exports account for a greater share of economic activity experience the greatest shortfalls in output (see Annex E). The overall impact is similar for Scotland and the rest of the UK. However, Scotland’s food and drink sector is more impacted, driven by whiskey exports, and rUK’s machinery industry is more impacted, driven by road vehicle exports. Lower demand overall has wider impacts across the economy while some sectors benefit slightly from labour and capital reallocation.

Source: OCEA Modelling

Contact

Email: economic.statistics@gov.scot