International best practice in tax communications: Ernst and Young Research

Research conducted by Ernst and Young, commissioned by the Scottish Government, on approaches to tax communications internationally.

2. Findings from literature and select country analysis

This chapter sets out the approach and findings of the literature review and selected country best practice analysis. The analysis looks at both the general literature on government communication, as well as the specific literature on tax communications, and the findings have been set out in this chapter based on the broad themes that emerged from the analysis, specifically:

- Considering the purpose of the communication

- Understanding the existing environment into which the communication will be launched

- Developing a clear and simple message

- Identifying and targeting vulnerable or hard-to-reach groups

- Choosing the right communication channels

- Considering behavioural insights in the choice of channel, message and focus

- Measurement of effectiveness and use of feedback to improve communication

2.1 Approach

Communication plays a crucial role in raising awareness of taxpayers (the focus of this paper) and is involved in various stages from the creation and implementation of tax decisions to the dissemination of information on its operation and function. The literature on government communications and engagement can be categorised into several general areas.

- Broad government communication and engagement with citizens, often focusing on specific sectors or industries

- Tax specific communications

Valuable lessons can be drawn from the wider body of literature on government communication on regulation and therefore has been covered first. As noted in section 2.1, the tax specific literature addresses four aspects of taxpayer communications, being taxpayer awareness, engagement, assistance and education. This paper focuses on the literature through the lens of taxpayer the first of these areas, taxpayer awareness.

2.1.1 Approach to literature review

A selective literature review was undertaken on international best practices for communicating and engaging with taxpayers. The objective of the review was to identify, analyse, and synthesise existing research, policy documents, and international tax communication approaches to understand the strategies and techniques utilised by tax authorities globally. The methodology encompassed a search strategy based on the selective identification of best practice literature and in relevant and high-quality sources[9].

The analysis of the literature was conducted through a multi-faceted approach. Thematic analysis was used to identify common themes, patterns, and gaps in the literature. Additionally, a critical evaluation was conducted to assess the quality, reliability, and validity of the studies, considering the methodologies used and the robustness of the findings. This literature review covers only publicly available information.

2.1.2 Approach to the select country review

The review of country case studies aims to supplement the literature review with examples of best practices in taxpayer communication and engagement, drawing insights from jurisdictions or regions renowned for their innovative approaches or common features. Not all observed practice will be easily transferred to Scotland, as the practices may be dependent on the specific environment, but they should provide opportunities for adaption or help inform future plans.

The methodology for selecting countries for the benchmarking report on tax communication and engagement involved a review of approaches taken by different nations in engaging with the public around taxation. The selection criteria focused on countries that are small independent nations, have federal and devolved government structures, and are recognized for their best practices in digital tax administration techniques and approaches. This approach was taken to provide a diverse representation of governance models and innovative practices in tax communication[10]. The countries chosen for the report were:

- Australia and the Australian Tax Office (ATO)

- California

- Canada and the Canada Revenue Authority (CRA)

- Estonia and the Estonian Tax and Customs Board (ETCB)

- Germany

- New Zealand, and the Inland Revenue Department (IRD)

- Norway and the Norwegian Tax Administration (NTA)

2.2 Considering the purpose of the communication

The literature on the role and process of communication in building government legitimacy is helpful in providing a broader theoretical framework for analysing tax communication. Literature related to communication in areas such as regulation is particularly useful due to the parallels in building consensus on tax, where public compliance is required for the common good.

The literature highlights that the level of communication will vary based on the aim and role of the stakeholder in the regulatory decision-making processes. Some communication will allow the public to influence decision-makers through the exchange of arguments and information. This has been reflected in the diagram in Figure 1 which sets out the level of communication that is appropriate based on the outcome[11] and is used in public policy discussions in New Zealand.

Having considered the intent of the communication, the various mechanisms for engagement can be considered. These include:

- Public hearings (including consultations)

- Public opinion surveys and citizen panels

- Opinion polls

- Focus groups and citizen advisory committees

- Citizen juries

- Referenda

Whilst the “inform” category is most pertinent to the raising of general citizen tax awareness and will be considered in greatest detail by this report, the others also provide a useful checklist of options for policymakers to consider.

2.3 Understanding the existing environment into which the communication will be launched

2.3.1 General literature

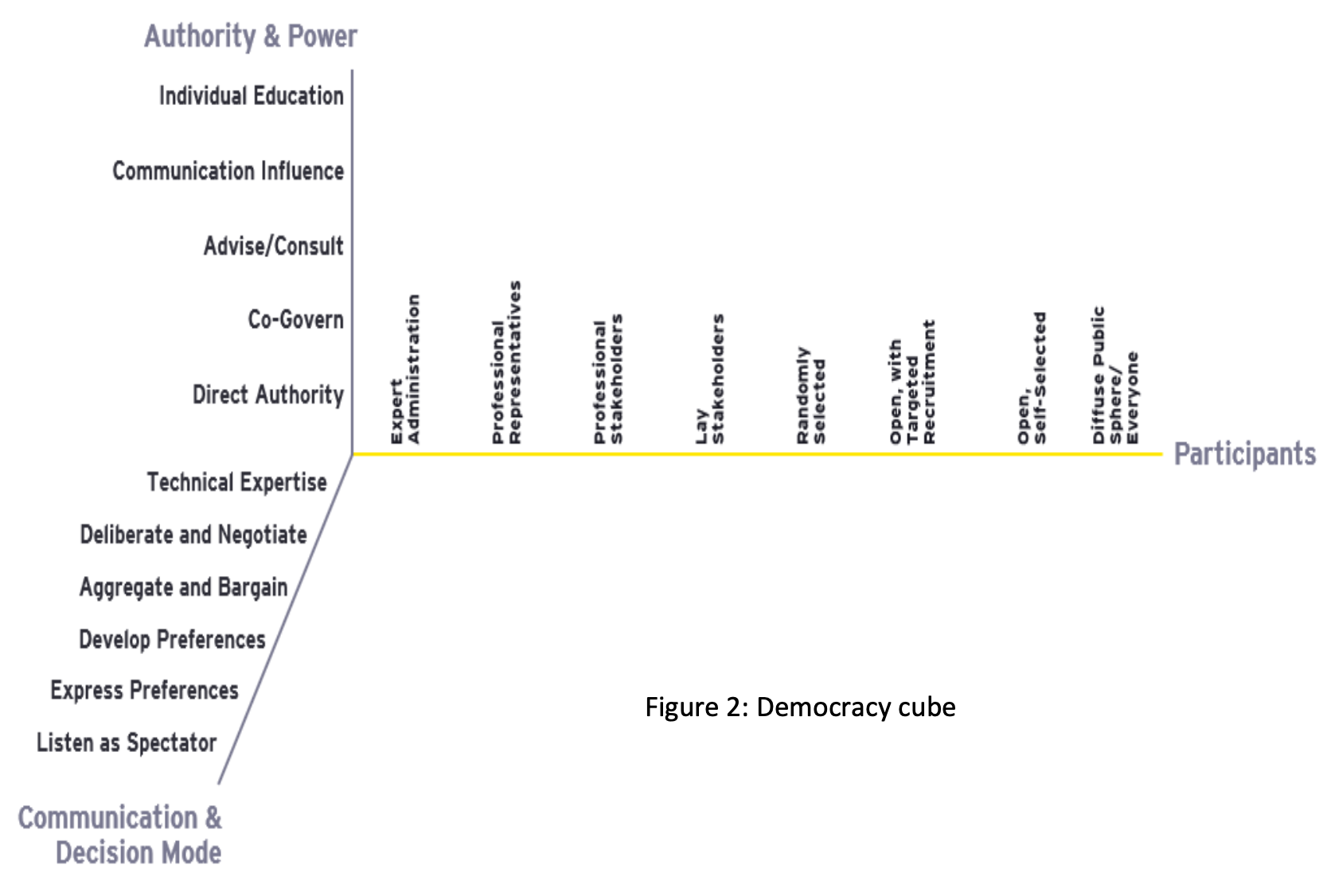

A further developed typology for considering what form of government communication might be suitable in a given situation was set out by Archon Fung. Fung considered how participation selection methods, modes of communication and decision, and the extent to which authority and power interact.[12] This is presented as the “democracy cube”, and the various means of communication can be plotted on the cube. Through considering the interplay of the three axes, a suitable means of communication can be determined for each topic.

The axes of the cube cover:

- Participant inclusivity: This axis examines how inclusive or exclusive the engagement or communication process is. At the exclusive end, participation is limited to expert administrators and elected representatives. Moving towards the middle, there is a more expansive selection of participants, for example through random selection. At the inclusive end, the process is open to all citizens, allowing for the broadest possible participation. This spectrum highlights the trade-offs between inclusivity and the ability to manage and process the input from a large number of participants.

- Communication intensity or decision mode: This axis measures the intensity of engagement in the participatory process starting from the least intense end, where participants are merely listening (analogous to the “inform” category in Figure 1 above). This study focuses on the upper end of the scale, such as is communication to raise individual awareness or for information only, rather than higher intensity engagement. For example, where participants engage in developing preferences and bargaining, or where participants contribute to the decision-making process or negotiations (which would fall within the “empower” category above).

- Extent of authority: This axis charts the level of decision-making power granted to participants. At the least authority end, participants gain an understanding of the benefits of participation but do not impact the decision. Moving up the spectrum, participants can have a level of influence on decisions through expressing their preferences while other participants may be specifically advised or consulted. Towards the end of this spectrum, co-governance would involve joint development of action plans between citizens and the government. At the highest level, direct authority is where citizens make actual decisions. These different levels of stakeholder authority would need to be considered carefully in the context of tax decisions, for example. While direct citizen level decision making is rare in taxation (for example, the requirement in Switzerland to hold a referendum), more engagement and consultation on the design and administration of decisions might be appropriate.

2.3.2 Specific benchmarked country examples

New Zealand has created (and amended over time) a formal tax policy process called the General Tax Policy Process (GTPP), whose main objectives include providing an opportunity for substantial external input into the policy formulation process. The GTTP has been recognised as a best practice in policy formulation[13] and part of this is linked to the embedding of tax engagement within the process.

The New Zealand Tax Working Group notes that the public engagement triggered by the GTPP “improves policy and regulatory outcomes, and informs stakeholders in advance of regulatory changes”. It notes that:

“Through initial discussions with stakeholders, officials have identified that the following principles should be applied to public engagement on tax policy initiatives:

- Earlier and more frequent engagement

- The use of a greater variety of engagement methods

- Wider engagement

- Greater transparency and accountability”

It describes the policy development process as largely occurring in the operational and legislative phases of the GTPP, and is made up of five stages:

- Concept: Identifying issues and opportunities, clarifying the scope of the issue, and getting approval to begin project planning.

- Plan: Forecasting the time and resources required for the project.

- Research: Undertaking research and analysis, identifying the options, costs and impacts. Getting approval to consult externally.

- Develop: This stage covers consultation, finalising policy options, costs and impacts, getting Ministerial and Cabinet approval for the policy changes, developing draft legislation.

- Legislate: This stage covers the parliamentary process and communication about any resulting legislation.

The New Zealand Tax Working Group[14] notes that

“generally, consultation usually occurs only once the project has reached the “Develop” stage. This is when some research and analysis has already been undertaken on the issue, and options to address the issue have been identified. Some consultation also occurs in the “Legislate” stage through the Select Committee process.”

The GTPP is intended to impose structure on the policy making process and can be seen as a tool for delivering a clear approach to consultation. Alongside the GTPP, the Government publishes a Tax Policy Work Programme (TPWP) that seeks to provide a status report of various policy issues and a short description of the problem definition for each issue. Interested parties can then contact tax policy officials if they have any issues with how the problem has been defined, or simply to express interest in being included in any preliminary consultation. The TPWP also provides the basis for call for evidence.

As noted above, this has been highlighted as best practice in policy making since it was first introduced in 1998. Whilst it has been lauded and improved since its formation, it brings with it a considerable cost and expectation. Recently, there have been concerns about the erosion of public consultation in New Zealand’s tax policy development and suggestion that the consultation process could involve a broader scope.[15]

2.4 Developing a clear and simple message

2.4.1 General literature

Much of the literature considers the need for a message to be “simple” without defining what this means in practice. For the purpose of this report, messages or policies are considered to be simple if they are “no more complex than necessary to achieve their aims”.[16]

Reducing jargon

Whilst the topics of tax can be complex, it is broadly accepted that complex issues can be simplified. Literature advocates for avoiding jargon and using plain language, with targeted guides that can be tailored to specific users. In particular, given the developments in technology, messages can be delivered in multiple forms, each of which may resonate with a different section of the intended audience. When considering the adjacent field of taxpayer education, the OECD notes that the publishing of informational videos and posts can explain new developments or rules in simple language.[17] The World Bank has commented that earlier research indicates that simplification of messages received by taxpayers can help taxpayers to comply with a process that can otherwise seem overwhelming, and that easy-to-understand images may also be beneficial alongside written messages.[18]

The European Union (EU) has published guidelines on using communication to build trust between taxpayers and the tax administration, noting that how information is disseminated to taxpayers can affect trust.[19] The guidance agrees with the need to have clear and understandable communication, noting that communication should be concise and to the point, whilst bridging the gap between the taxpayer and the tax administration. The EU also notes that the tone of communication could show empathy and understanding to help make taxpayers feel respected, even if the message is not favourable to them.

Building a team

It is generally accepted that all teams aim to produce simple messaging, but that in practice this is not given sufficient time or priority. In order to mitigate this, the UK Institute for Government (IfG) has suggested that government communicators should have more input in initial policy discussions. It argues that a government should seek to employ well-trained communications specialists and establish ethical safeguards for such communicators.[20] Sharp (2013) comments that investing in a team specifically dedicated to educating and communicating with taxpayers are valuable contributions to successful tax reforms.[21]

Using digital innovations

Digital tools can be more effective in reaching a younger generation of taxpayers, with digital tools such as educational videos, web games and apps being utilised by some jurisdictions for taxpayer education.[22] Digital tools may need to be reviewed on a regular basis to ensure that they remain relevant as online trends and digital technology change quickly. Sharp (2013) notes that modern methods (at the time of writing) of communicating such as through SMS and email were more effective methods of communicating than using letters.[23]

The IfG noted that media platforms which offer one universal user experience for all of their audiences are losing popularity, whilst those that have personalised offerings are growing. These personalised offerings allow the government to reach particular groups of people but make it more difficult and expensive to reach everyone at once. The IfG also states that misinformation and disinformation are challenges present in attempts to communicate with taxpayers.[24]

2.4.2 Specific benchmarked country examples

A key element in the development of a simple message is understanding the context of the recipient of the message. Whilst this is informed by behavioural analysis, a simpler approach is to identify “taxpayer journeys”, such that the taxpayer can self-identify and access information that is tailored for their broad circumstances. The CRA created user journeys to adapt to the various needs of their taxpayers[25]. The user journeys are intended to map the optimal interaction between a taxpayer and the tax administration, and the usability of the service is tested by a representative from each target audience that the CRA is trying to reach. This allows the CRA to ensure that certain subsets of taxpayers are receiving relevant information that they require and to simplify content of the CRA website and publications for selected taxpayer groups.

Taxpayers can also be subdivided by their nature. The ATO splits taxpayers into groups such as individuals and families, businesses and organisations and tax and super professionals. Pages for each topic are written with the specific audience in mind and contain short informational videos as well as text. Similar disaggregation is seen in Estonia (which splits between private taxpayers and business taxpayers) and New Zealand which publishes tax information under the headings of individuals and families, business and organisations and intermediaries and others.[26]

Beyond taxpayer journeys, many jurisdictions have adopted “no jargon” policies, with clear writing instructions. For example, in New Zealand, policymakers are advised that they:

“can expect to get quality feedback on a draft document if:

- it is easy to read, jargon-free, and not too long

- it is attractively presented

- the topic is highly relevant to the survey population

- the issues are of interest and concern to those surveyed.”

The advice is tailored depending on the communication channel, such as presentations, receiving written submissions, drafting questionnaires, and other participatory measures.[27]

2.5 Identifying and targeting vulnerable or hard-to-reach groups

2.5.1 General literature

Campaigns are most effective when they are targeted to cultural contexts and specific groups.[28] Mass communication may not be sufficient to reach the most vulnerable, hard-to-reach or remote groups of taxpayers, and some messages may be needed to be tailored to certain groups of taxpayers to ensure the message is understood and accepted. To target vulnerable or hard-to-reach groups, they first have to be identified.

Communication plans have been developed by some jurisdictions with the help of academics and scholars to understand their target audience better and reach taxpayers that cannot be reached through usual channels.[29] The IfG (2023) notes that representativeness should not come at the expense of targeting specific groups, and that good engagement with the public requires tailoring engagement to specific needs and interests.[30] Sharp (2013) similarly finds that direct communications initiatives can benefit from being tailored to different taxpayer groups.[31] New entrepreneurs and foreign workers are commonly identified subgroups which may require further tailoring in communications.[32]

As indicated above, clear, jargon-free language is essential in delivering the message effectively and proactive communication involving communication specialists may be beneficial. Messaging can be better received by vulnerable groups when the communication is tailored to them, and ethnographic research can be used to help achieve this. Behavioural insights can be used to instil a positive attitude from taxpayers towards paying taxes and the tax administration (see below).

In order to access taxpayers that may not naturally engage with the tax administration and therefore reach a bigger audience, tax administrations partner with other organisations and entities; for example, the tax authority in Slovenia partnered with Slovenia’s Government Communication Office for the campaign regarding checking invoices.[33] Sharp (2013) finds that partnerships with trusted organisations can be effective. This was found to be true particularly when working with schools, civil society groups and business or religious organisations.[34]

2.5.2 Specific benchmarked country examples

The definition of hard-to-reach groups can vary substantially between jurisdictions and can relate to challenges in messaging through to challenges to get attention. The approach to reach such groups depends on the nature of the challenge and a key stage is the development of a taxonomy of such hard-to-reach groups.

Race and culture

Hard-to-reach groups can relate to race or culture, with Canada collecting sociodemographic and income filing tax data on Indigenous Peoples, Black Canadians and other racial groups as these groups tended to have more difficulty in accessing disability services and support than others. It stated that the linking of sociodemographic and income filing tax data would help to identify populations that face difficulty in using the digital application process for registering as disabled and result in a greater understanding of the needs of the disabled community in Canada and the barriers they face, as well as increasing the uptake for the online application for the disability services. The CRA noted that for the Indigenous population, it partners with external organisations such as national Indigenous organizations and Indigenous Services Canada.

Language

One difficulty in reaching taxpayers can be language. The ATO has invested in tailored tax assistance and education programs, including an indigenous helpline and the translation of tax information into 13 Aboriginal languages. Additionally, an Indigenous artist was commissioned to create artwork for branding to display cultural diversity and inclusion. Targeted radio advertising in English and Yolngu Matha languages was also conducted to encourage corporations registered under the Corporations (Aboriginal and Torres Strait Islander) Act 2006 (CATSI Act) to apply for a digital ID. The ATO also ran a “Tax and Super Basics” campaign to support taxpayers from culturally and linguistically diverse (CALD) backgrounds to be more aware of their obligations and to provide better access to information and services. This campaign was carried out in 12 languages across a variety of channels. Eight in-language videos were developed for this taxpayer group on topics including education on filing a tax return and starting a business.[35]

IRD posts short informational YouTube videos in three different languages: Te Reo Maori, Tongan and Samoan.[36] Similarly, the CRA produces factsheets and infographics to assist newcomers and Indigenous Peoples in eight third languages (in addition to English and French) and 16 Indigenous languages. In Europe, Estonia has identified and tailored information for vulnerable groups of taxpayers, including a specific page for advice for war refugees from Ukraine on how they can register for employment and taxation of wages in Estonia.[37] Similarly, Norway has a page for tax information for asylum seekers from the Ukraine which is published on the NTA’s website, available in Ukrainian, English and Russian.[38]

Additionally, the NTA hires two language managers to ensure that enquiries to the Tax Administration can always be answered in English.[39] The NTA also educates foreign, personal and corporate income taxpayers through information dissemination and the provision of professional guidance in English to encourage compliance.[40]

Time

As noted, some groups are hard-to-reach due to lack of time or propensity to engage. This can be addressed by using established communication channels of other organisations. The ATO partners with trade media in Australia to share resources and information across their channels and networks. The ATO reaches out to industry groups and bodies, small businesses, professional associations, chambers of commerce, government agencies and others on a monthly basis to ensure the regular reproduction of the ATO’s content via stakeholder channels.[41] The ATO works with tax practitioners and associations through bespoke groups for consultations, with six special working groups. The ATO also has a newsroom for tax professionals, as well as webinars and open forums.[42] Additionally, the Australian Board of Taxation functions as a communication channel between Australia’s Treasury, the ATO and the private sector. It has been recognised that this had improved the quality of contact with taxpayers.[43]

Similarly, New Zealand’s IRD has strong links with large accounting and legal firms, and industry bodies such as Chartered Accountants Australia and New Zealand and the New Zealand Law Society. However, the IRD recognised in 2019 that it needed to form stronger links with non-profit and community organisations; youth, Māori and Iwi representatives, specific industry and sector representatives, accounting software providers, small and medium businesses and members of the general public. Each of these groups could be targeted separately, but in a holistic manner.

High risk businesses[44]

A further hard-to-reach category may be high-risk businesses, which may not wish to have any exposure to the tax authorities. This may be addressed through targeted communications that are focused on areas where such taxpayers may be present. New Zealand’s IRD has targeted communication for the construction industry, where 40,000 individual businesses were contacted or advertised to with a “last warning to pay taxes”. Taxpayers were directed to an online “Tax Toolbox for Tradies”, with officers from the IRD visiting a number of hardware stores to provide in-person advice and education. The IRD did this by developing a communication and public education plan, running online campaigns and going on mainstream and ethnic radio channels, as well as advertising at family and recreation centres in New Zealand. 2,500 tax workshops were also hosted for businesses and sole-traders.[45]

2.6 Choosing the right communication channels

2.6.1 General literature

Once the means of communication has been considered within the democracy cube, the next stage is to consider the precise channels that will be used – these will be dependent on the intended purpose, objective and desired outcome of the communication. There are four steps to the process:

1. Consider all aspects of the democracy cube to identify the type of consultation or engagement that is wanted.

2. Building on the communication mode axis, consider whether the communication is about awareness, explanation, or gathering feedback.

3. Identify all the potential channels that could be used that would address the right area of the democracy cube.

4. Deploy a coherent approach, considering the use of multiple channels.

In addressing the third step above, the OECD[46] has emphasised that communication channels focused on delivering information can be sub-divided into awareness generating and explanatory channels. It notes that:

- Awareness generating channels are those that engage the taxpayers’ attention and interest, and direct or encourage taxpayers to use additional channels to obtain further information. Examples may include letters and emails, but, where these are sent too frequently there is a risk that these will be ignored over time. Social media is another form of awareness generating channels with the added bonus of the multiplier effect as people share or comment on the posts.

- Explanatory channels provide more detailed information to taxpayers and, where necessary, will link to other important information. Examples typically include the tax administration’s website and digital channels such as podcasts, videos and presentations.

There is considerable literature discussing the benefits of using multiple channels, with a further OECD report[47] noting that the challenge of delivering a message to a large part of the population may be overcome by mixing multiple methods of communication. This finding was also reported by the World Bank, which found that tax authorities should use multiple different methods to communicate depending on cultural context.[48] Similarly, Sharp (2013) finds that governments commonly use multiple channels to relay tax information, which can vary from direct communication to education initiatives. Sharp (2013) further notes that the optimal communication strategy depends on contextual factors including the potential to generate revenue, state legitimacy, current levels of tax compliance and availability and quality of taxpayer records.[49]

In addition to considering individual communications, benefits can develop from building a regular and ongoing positive presence in the lives of taxpayers, as then taxpayers will know where to turn when they have questions or want to be part of a debate about tax.[50] However, this can risk being overwhelming, and hence failing to provide value for money and fragmenting the message that the government is trying to deliver. In an analysis of the UK Government’s messaging, the IfG found that the government should be quicker to shut down campaigns that are performing poorly and should place further emphasis on increasing public awareness of the positive aspects of what the government is achieving.[51]

Specific channels

In relation to how to use the specific channels, care needs to be taken to consider their best use. For example, in practice, taxation communication often makes use of formal public consultation processes and public opinion surveys. These mechanisms allow the public to express their views on regulatory matters, providing a significant amount of written and oral material encapsulating public opinion and specific stakeholder views before a decision is made. These processes often operate on a reactive basis, with the assumption that all interested parties will participate, which may not always be the case. In commenting on the use of these methods,[52] the following recommendations have been noted:

- Give sufficient notice of the proposed change, so that all parties have time to consider.

- Allow for written and oral comments, to maximise the opportunity for feedback.

- After the policy decision has been made, publish a general statement explaining the decision in light of the evidence and comments received. This aims to mitigate the risk that decisions which do not align with the respondent’s views give rise to reticence for further engagement.

In practice[53], tax administrations commonly use specific locations such as fairs to get in touch with taxpayers, as well as mass media including the internet, TV and radio to reach a broad range of taxpayers. In some countries, national TV and radio channels are used to broadcast information that generally applies to most taxpayers, whilst local stations are used for announcements specific to taxpayers in certain regions.

According to the OECD,[54] friendly approaches are more efficient in garnering a positive attitude from taxpayers. An example of a friendly approach may be to host events with a theme of tax citizenship. Tax days, tax weeks and fairs are common, often comprising presentations by government officials and awarding of prizes, as well as activities for children and exchanges with taxpayers in a friendly atmosphere. These events may be advertised and in some cases celebrities and influencers may be invited to the events to encourage fans and followers to attend the event. Whilst these events can be resource intensive and time consuming, participation in other pre-existing events can help to reduce the costs associated with events.

2.6.2 Specific benchmarked country examples

The benchmarked jurisdictions provide lots of evidence of the use of a wide range of channels. Remaining with New Zealand, the Tax Working Group notes that “a greater focus will be placed on ensuring that the method of engagement used is fit for purpose. While a consultation document may be appropriate in most circumstances, officials will have regard to: “the intended audience and how best to communicate with them; who is likely to be affected by the proposal; the scope and scale of the proposal; and the purpose of the consultation”.

In addition to the use of public consultation documents, the New Zealand Tax Working Group planned to use:

- Focus groups with customers

- Workshops with representative industry bodies and community organisations, market participants, and service providers

- Online forums

- Use of multimedia content across different languages

- Culturally tailored methods of engagement – e.g. which follow tikanga principles when engaging with Māori

- Face to face discussions with affected customers.

It is clear that there remains a role for formal consultation. California holds public interested party meetings and public regulation hearings, where all interested persons can attend the meeting to present written or verbal comments on proposed regulatory actions. Notice of the meetings is published 30 days in advance of the meetings, alongside information on how the public can participate in the meetings. Related documents are published for the current and previous year’s meetings.[55]

The communications of the tax administration may be considered in conjunction with other governmental communications. In Germany, there is an integrated whole of government cross-media and multi-perspective approach to communication. This is intended to reach the widest possible range of general public and disseminators of information such as journalists. The three pillars are:[56]

1. Integrated communication. Departments are coordinated by the Federal Press Office (BPA) and encouraged to place key projects at the centre of their own communications. The BPA develops visual and textual narratives, as well as developing key storyline messages designed to be communicated by each department. Objectives of campaigns and their budgets are to be linked with the activities of other departments.

2. A cross-media approach. The cross-media approach is utilised to communicate with a wider range of socio-demographic groups in both urban and rural locations. Various textual, visual and audio-visual formats were used and distributed through both the channels of various ministries and sub-national authorities. Campaigns were also used and combined with live events such as panel events and digital citizens’ dialogues to allow for exchange with taxpayers. Websites were also used to provide a central hub for all sources of information, showing the range of social media and print resources, as well as third party communication including media. Channels such as Twitter were used for statements by the Federal Finance Minister as well as explaining issues often perceived by the public to be complex in nature.

3. A multi-perspective approach. This involves departments linking national aspects of modernisation plans back to the resilience plan in their communications.

A similar cooperative approach was seen in Norway with multiagency coordination to reduce the demand for unofficial labour in the construction industry. This involved a collaboration between several government agencies, social partners, municipalities and county authorities.[57]

Using digital innovations

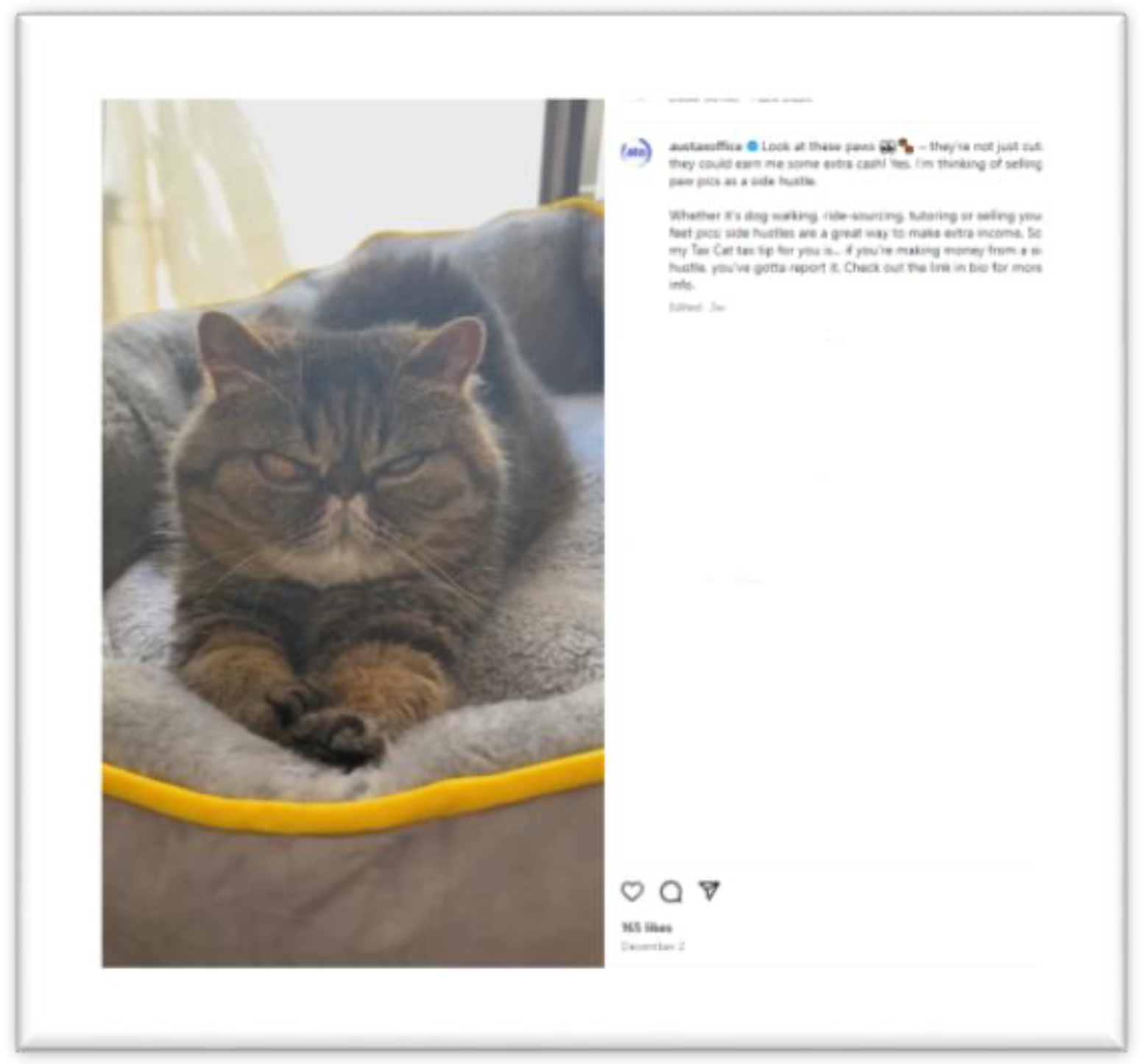

There are also many examples of the use of digital innovation to enhance messaging. For example, Australia has sought to target and catch the attention of younger taxpayers through a “tax cat”. The ATO frequently posts videos and photos of a cat on the ATO’s Instagram page, which effectively acts as the ATO’s mascot accompanied by tax information and messaging[58]. For example, the following was posted in relation to the taxation of “side hustles”:

“Look at these paws 👀🐾 – they’re not just cute, they could earn me some extra cash! Yes, I’m thinking of selling paw pics as a side hustle. Whether it's dog walking, ride-sourcing, tutoring or selling your feet pics; side hustles are a great way to make extra income. So, my Tax Cat tax tip for you is... if you're making money from a side hustle, you've gotta report it. Check out the link in bio for more info.”

Another alternative approach was in Norway where the NTA developed a computer game with second-screen technology aimed at secondary school pupils to teach them the benefits of paying taxes both for themselves and the larger community. The game focuses on the shadow economy and the negative effects of undeclared work on employers and employees.

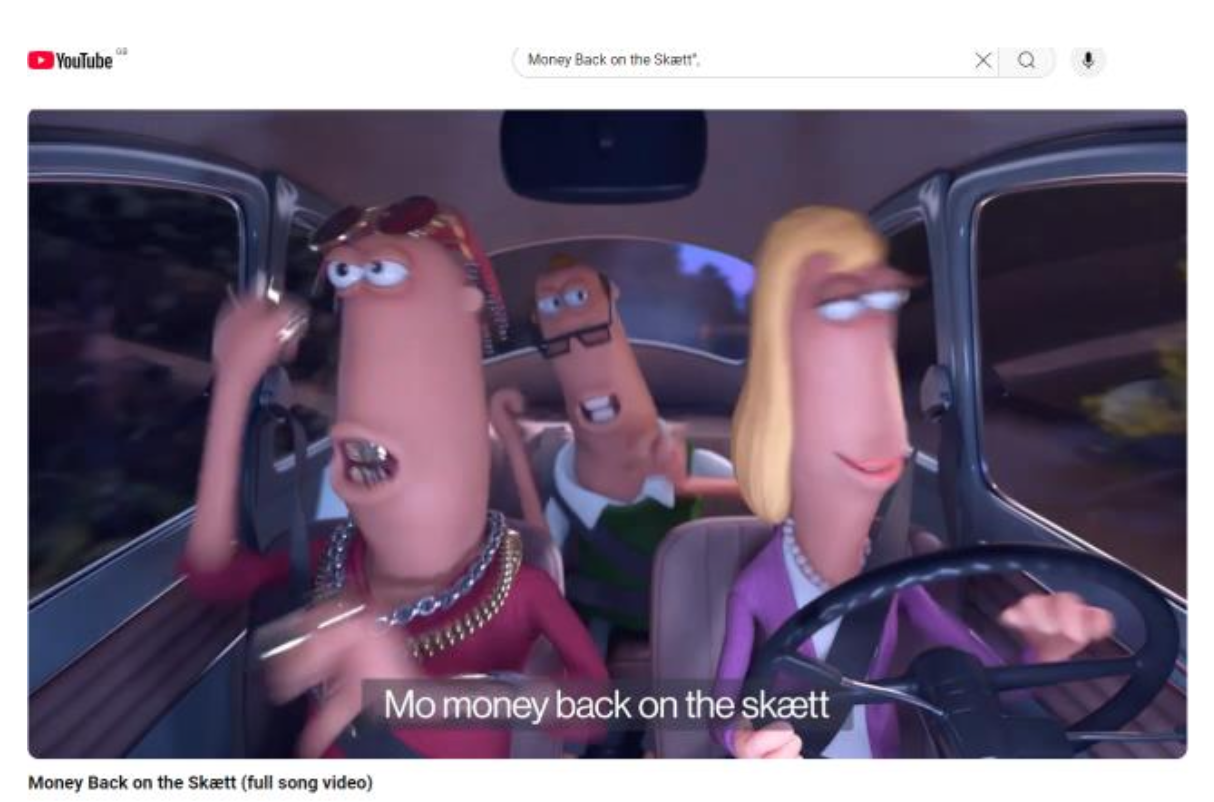

NTA also released YouTube videos (in Norwegian and English) titled “Money Back on the Skætt”, in which fictional characters rap about tax[59]. This was part of a marketing campaign targeted at young taxpayers to encourage them to check and revise their tax returns online, increase their understanding of their tax situation and duty to submit correct information to the NTA.

Beyond these examples, use of digital technologies to deliver existing messages in a multi-media manner is common. Germany has published on the Federal Ministry of Finance website a collection of short videos called “Finanzisch” (which translates to “financial slang”) which briefly and concisely explains common financial policy terms.[60] Similarly the State of Baden-Württemberg has created a video series to promote tax compliance and answer the frequently asked questions of the citizens concerning taxes.[61]

Canada launched an ‘every dollar counts’ webpage with videos, which discuss benefits, credits and programs available as well as information on where to attend a free tax clinic. This was supplemented by a podcast in February 2024 called ‘Taxology’, providing further information on benefits and credits available to taxpayers.

The situation in Estonia is further developed, as the government has adopted a primarily digital approach to communication with citizens. Most taxpayers are registered for an online e-MTA portal and information including administrative acts and documents are sent through the portal. Additional notifications to check the notification on the portal are sent via the taxpayer’s email address or by SMS. This consistent interaction with citizens makes it easier to engage and identify areas where communication on taxation is relevant.

2.7 Considering behavioural insights in the choice of channel, message and focus

2.7.1 General literature

The use of behavioural insights to create messages that increase compliance, through the addition of social norms and minority norms,[62] has received a lot of attention. Hallsworth et al (2017) found that the most effective messages were those that included social norm messages with a minority norm frame (e.g. “the majority of people pay on time, you are in a small minority who do not”).[63] Findings by Sharp (2013) were similar, noting that tax compliance is influenced not only by enforcement incentives, but also by social norms and expectations of receiving something back for paying taxes. Sharp further comments that deterrence messaging appears less effective in higher-income contexts.[64]

Furthermore, the World Bank (2021) notes that appealing to a taxpayer’s sense of duty and good citizenship can be effective as people prefer to think of themselves as honest and moral people, therefore describing their non-compliant behaviours as intentional and unethical can increase compliance. The World Bank further comments that highlighting the compliant behaviour of others can encourage further compliance. However, the World Bank did also consider the effects of deterrence messaging, stating that signalling an increase in enforcement mechanisms can make it feel like a higher risk to the taxpayer if they do not comply and therefore encourage compliance.[65]

From the wider perspective of taxpayer awareness and engagement, many of the design decisions as to choice of channel, message and focus can be informed by behavioural insights. Rather than considering this as a separate activity, this consideration should be embedded in the decisions discussed previously and then the full design reviewed holistically.

2.7.2 Specific benchmarked country examples

The CRA used ethnography to support its taxpayer communications, allowing it to tailor communication for small business and vulnerable groups. The CRA used methods such as immersion, observation of participants and semi-structured interviews to collect data which shows insights into taxpayers’ experiences and behaviours. The information has been used to improve outreach to certain taxpayer groups and tailor communications to their needs. Three ethnographic research projects were carried out with a focus on small businesses, homeless people and housing-insecure persons and vulnerable newcomers.[66]

2.8 Measurement of effectiveness and use of feedback to improve communication

2.8.1 General literature

As noted in the democracy cube (Figure 2), communications are deployed into a complex environment. It is therefore very important for the communications to be evaluated, allowing successes to be built upon and shortfalls to be addressed. There are a number of examples of good evaluations.

2.8.2 Specific benchmarked country examples

The CRA has subjected its communications strategies to a formal Public Opinion Research (POR) study, with the findings from the POR sessions to be used to revise communications strategies.[67] In a comparable area, Estonia monitors the visibility in the media of its Recovery and Resilience Facility (RRF) communication plan, through preparation of a quarterly overview of the RRF-related coverage in news programmes on Estonian TV and radio, print and online media. Targets were set for coverage per quarter.[68]

Beyond evaluation of coverage, the ETCB has also looked to evaluate the effectiveness by creating an index of willingness to pay taxes, which measures tax behaviour by four determinants: knowledge, attitudes, social norms, and perception of behaviour. The index is used to evaluate the impact of the ETCB’s activities and external factors on taxpayer behaviours.[69]

Germany has adopted particular measurement and feedback metrics for communications, particularly around its RRF. The monitoring of communication activities performance is conducted by the Federal Press Office and the relevant ministries, with ongoing analysis carried out to adjust communication according to success. The strategy notes the importance of using qualitative measure of success to identify the impact of key messages on the public, to be reviewed after a certain time period, and the use of a future deeper demographic review to be used to develop further measures. The European Commission undertakes statistical analysis of the formats used on a monthly basis. Representatives were also to be sent to events organised by third parties to allow dialogue with interested members of the public. A uniform look and feel to social media communication was applied to help to generate public recognition and trust in the communications, as well as increase visibility and outreach.[70]

Monitoring and evaluation of the communication strategy under the German Recovery and Resilience Facility communication plan are as follows for each communication type:[71]

Communication channel

Social networks and Search Engine Optimisation (SEO)

- Metric or Indicator

- Number of users affected by advertising

- Organic user intervention

- Click through rate – number of clicks per restoration plan website

- Number of debates organised

- Note

- Data analytics are obtained through analytical tools integrated in the social media platform and are available to advertisers.

Webpage

- Metric or Indicator

- Number of unique visitors per month or quarter or year

- Analysis of the monthly trend of visits

- Demographic analysis of visitors

- Note

- To allow the content of the website to be adapted on the basis of data and analysis at a later stage.

Newsletters

- Metric or Indicator

- Number of users logged in (public)

- Number of users logged in (media)

- Number of unsubscribed users (public)

- Number of users logged (media)

- Open rate (% of users opening a newsletter)

- Note

- At a later stage, the content of the newsletter should be personalised and adapted on the basis of the personal preferences of each registered user.

Audiovisual and print media

- Metric or Indicator

- Number of “per activity” viewers affected

- Number of “per activity” audiences affected

- Number of “per activity” readers affected

- Note

- Based on the analysis, the communication team can evaluate the content quality of the activities and adapt the content for each target group.

Public debates and seminars

- Metric or Indicator

- Number of active participants

- Number of questions or interactions from participants

- Note

- N/A