Government Expenditure and Revenue Scotland (GERS): detailed methodology 2024-25

Details of the methodology used to obtain estimates of public sector revenues and expenditure for the Government Expenditure and Revenue Scotland (GERS) 2024-25 publication.

Part of

Approach to estimating revenue in GERS

This section outlines the various methodologies used to obtain estimates of public sector revenues in Scotland.

There is no generic best approach to estimating public sector revenue; instead each revenue is estimated using a separate methodology. This section discusses the methodology used to apportion a share of each revenue stream to Scotland and highlights any significant changes which have been introduced in this edition of GERS. It should be noted that, as the underlying datasets used in GERS have been subject to revisions and updates, estimates may differ from previous editions of GERS even if the methodology remains unchanged.

Methodology Overview

As highlighted in Chapter 1 of the main report, the majority of public sector receipts raised in Scotland are collected at the UK level by HM Revenue and Customs.

In some cases, revenue figures can be obtained for Scotland directly. Examples include local government revenues, devolved taxes, and elements of public corporation revenues. For other taxes separate identification of Scottish revenue is not possible. GERS therefore uses a number of different methodologies to apportion revenues to Scotland. In doing so, there are often theoretical and practical challenges in determining an appropriate share to allocate to Scotland. In certain cases, a variety of alternative methodologies could be applied each leading to different estimates.

Obtaining an estimate of public sector revenues in Scotland is a two-stage process.

In the first stage, the UK outturn figure for each stream of revenue is obtained from the ONS Public Sector Finances statistics. In the second stage, Scotland’s share of the UK figure is estimated according to a specific apportionment methodology. The methodology used differs for each element of revenue. However, in general, the information comes from survey data for the UK, or a sample of UK administrative data.

UK Revenue Figures

The basis for estimating public sector revenue for Scotland is National Statistics outturn figures for UK fiscal revenue taken from ONS Public Sector Finances. The detailed components, revenue by revenue, are taken from an ONS database (PSAT2) which is produced on a quarterly basis. The fiscal balance calculations in GERS are constrained to the UK Public Sector Finances for June 2024, published in July 2024. An accounting adjustment is applied to both the expenditure and revenue totals so that both sides of the fiscal balance calculations are presented on a consistent basis. The revenue accounting adjustment is small and has been included in the ‘other taxes’ line.

These data are presented on an accruals basis and separately identify revenue attributed to central government, local government and public corporations. The international standards for National Accounts and Government Finance Statistics use the accruals basis rather than a cash approach. This is because accruals accounting reflects a more accurate picture of when revenue is due and spending occurs than the more volatile alternative of cash, which, for example, records when bills are settled rather than when the expenditure occurs.

The assumptions underpinning the apportionment of each revenue source are outlined below.

Summary of methodology approaches

Table 1 provides a summary of the apportionment methodologies used for each element of revenue and highlights whether or not the methodology has changed since the previous edition of GERS. In some instances ONS’s Public Sector Finance estimates of UK revenue for some taxes have also been revised since the last edition of GERS, and these changes will affect the estimates of Scottish tax revenue. In addition, there have been revisions to some of the data sources used to apportion tax revenues to Scotland.

Table 1: Apportionment Methodologies and Sources for Public Sector Revenue in Scotland (Excluding North Sea Revenue)

|

Revenue |

Apportionment Methodology |

Source |

Changed |

|

Income tax |

Scottish share of UK income tax liabilities applied to income tax gross of tax credits. Negative expenditure on tax credits estimated using Scot/UK share of overall spend on tax credits (negative tax plus benefits) |

Scottish outturn statistics: HMRC Data on overall spend on tax credits: HMRC |

No |

|

National insurance contributions |

Estimates of employer and employee NICs revenue in UK and Scotland |

Supplied directly by HMRC |

No |

|

VAT |

Since 2011, HMRC VAT Assignment statistics for Scotland. Earlier years, Living Costs and Food Survey, ONS |

HMRC Living Costs and Food Survey: ONS ONS Regional Accounts |

No |

|

Corporation tax (excl. North Sea) |

Scotland’s share of UK onshore corporation tax |

HMRC |

No |

|

Fuel duties |

Scotland’s share of road traffic fuel consumption |

Fuel consumption statistics: Department for Energy Security and Net Zero |

No |

|

Non-domestic rates |

Outturn data for Scotland |

Scottish Local Government Finance Statistics |

No |

|

Council tax |

Outturn data for Scotland |

Scottish Local Government Finance Statistics |

No |

|

VAT refunds |

LG refunds: Scotland’s share of UK LG current expenditure on goods and services CG Refunds – MoD: Scotland/UK populations – NHS: Scotland/UK TES for Health – Other Gov depts: Scotland/UK total TES (Excluding NHS/MoD) |

Country and Regional Analysis, HM Treasury |

No |

|

Capital gains tax |

Outturn data for Scotland |

HMRC |

No |

|

Inheritance tax |

Outturn data for Scotland |

HMRC |

No |

|

Scottish Landfill tax |

Outturn data for Scotland |

Revenue Scotland |

No |

|

Reserved stamp duties |

Land and property stamp duty: Outturn data for Scotland Stocks and shares: - Scotland/UK ratio of adults owning shares |

Land and property stamp duty: HMRC. Stocks and shares: ONS Country and Regional Public Sector Finances |

No |

|

Land & buildings transaction tax (LBTT) |

Outturn data for Scotland |

Revenue Scotland |

No |

|

Air passenger duty |

Estimates of air passenger duty raised in Scotland |

Scottish Fiscal Commission |

No |

|

Tobacco duties |

Spend on tobacco in Scotland/UK |

Living Costs and Food Survey: ONS |

No |

|

Alcohol duties |

Consumption of alcohol in Scotland/UK |

Family Food Survey, DEFRA |

No |

|

Insurance premium tax |

Spend on insurance Scotland/UK |

Living Costs and Food Survey: ONS |

No |

|

Vehicle excise duty |

Scotland’s share UK vehicle licences issued |

DVLA |

No |

|

Environmental levies |

Renewables obligation: Scottish data from ONS Carbon Reduction Commitment: Scotland’s share of UK electricity consumption by industrial users |

ONS Department for Energy Security and Net Zero |

No |

|

Other taxes |

Various (see below) |

Various (see below) |

No |

|

North Sea revenue |

Scotland’s estimated share of UK Continental Shelf tax revenue |

ONS Country and Regional Public Sector Finances |

No |

|

Interest and dividends |

CG: Population share of non-student loan interest and dividends LG: Population share PC: Scotland’s share of public sector GVA PC pensions: Scotland’s share of public sector GVA |

Regional Accounts: ONS |

No |

|

Gross operating surplus |

CG: Scottish/UK share of central government NMCC LG: Scottish/UK share of local government NMCC Public corporations – consistent with the ONS Country and Regional Public Sector Finances |

CG: ONS Regional Accounts LG: ONS Regional Accounts PC: ONS Country and Regional Public Sector Finances |

No |

|

Other receipts |

Various (see below) |

Various (see below) |

No |

Income tax

Background

Income tax is the single largest source of public sector revenue in both Scotland and the UK. A taxpayer's income is assessed for income tax according to a prescribed order:

- non-savings and non-dividend (NSND) income

- savings income

- dividend income

NSND income tax covers around 90% of income tax, with a small amount (around 1%) of income tax being paid on savings, and the remainder of income tax paid on dividend income.

Since 2017-18, a different tax regime applies to non-savings income, income tax in Scotland. This is referred to as Scottish Income Tax. Although the personal allowance continues to be set for the whole of the UK, the subsequent rates and bands for NSND income tax are now set by the Scottish Government. Savings and dividend income continues to be taxed at the same rates across the UK. Information on the UK personal allowance and the rates and bands for reserved income tax is available at https://www.gov.uk/personal-tax/income-tax

The table below show the income tax rates and bands for NSND income tax in Scotland for 2024-25. Further information on Scottish income tax is available at https://www.gov.scot/policies/taxes/income-tax/

Income tax rates for Scotland in 2024-25

|

Band |

Band name |

Rate |

|

Over £12,571 to £14,732 |

Starter |

19% |

|

Over £14,877 to £26,561 |

Basic |

20% |

|

Over £26,562 to £43,662 |

Intermediate |

21% |

|

Over £43,663 to £75,000 |

Higher |

42% |

|

£75,001 to £125,140 |

Advanced |

45% |

|

Over £125,140 |

Top |

48% |

Consistent with the presentation of income tax used by the OBR and ONS, the income tax line in GERS also includes a number of smaller taxes. These are:

- Company income tax;

- Household charitable donations via gift aid;

- Non-profit institutions serving households tax credits.

Methodology

The approach for estimating Scottish revenue for each line is summarized in the table below. UK figures for income tax and associated revenue are taken from ONS’ database underlying the Public Sector Finances.

The main apportionment for income tax is HMRC’s Scottish Income Tax statistics. This is administrative outturn data on NSND income tax for all Scottish income tax payers.

|

Revenue |

Description |

Methodology |

|

Income tax |

The main tax on personal incomes in the UK. This is split into income tax collected through pay as your earn (PAYE) and income tax collected through self-assessment. |

Prior to 2016-17: Apportioned to Scotland on the basis of income tax liabilities from Survey of Personal Incomes (SPI) data

2016-17 onwards: Apportioned to Scotland on the basis of income tax liabilities from Scottish Income Tax. |

|

Company income tax |

Where properties in the UK are owned by non‑residents, the non-resident is treated as a company, but rather than paying corporation tax pays income tax on income earned income from these properties, such as rental income. |

Apportioned to Scotland on the basis of Scotland’s proportion of the UK GVA. |

|

Household charitable donations via gift aid |

When UK income tax payers donate to charity, the charity can claim an extra 25p for every £1 donated. |

As income tax |

|

Non-profit institutions serving households tax credits |

Tax credits paid to non-profit institutions serving households, typically charities.

|

As income tax |

Data are taken from the latest outturn statistics for Scottish Income Tax, published by HMRC. The publication provides a breakdown of Scottish Income Tax by self-assessment and by pay as you earn (PAYE) for the years 2016-17 to 2023-24. It also provides indicative information on PAYE income tax for 2024-25 through the real time information system.

Scottish Income Tax Outturn Statistics: 2023 to 2024 - GOV.UK

Income tax is split into income tax from PAYE and self-assessment. This reflects the different way these taxes are recorded in the Public Sector Finances. For PAYE, the Public Sector Finances shows income tax against the year that the income was earned. For example, PAYE income tax for 2024-25 shows tax paid on income earned in 2024-25. For self-assessment, the Public Sector Finances show the income tax at the time it was paid. For example, self-assessment income tax for 2024-25 shows the tax which was paid in 2024-25, which primarily relates to income earned during the 2023-24 tax year.

GERS therefore apportions PAYE income tax and self-assessment income tax separately. For PAYE, the Scottish share is taken as the share of NSND PAYE Scottish Income Tax liabilities for that year. For 2024-25, the growth rate in indicative income tax from the real time information system is used to determine the Scottish share.

For self-assessment, the Scottish share is taken as the share of NSND self-assessment Scottish Income Tax for the previous year. That is, the share of self-assessment liabilities in 2023-24 is applied to UK self-assessment income tax receipts for 2024-25. This methodology assumes that self-assessed income tax received in 2024-25 relates to income tax liabilities from 2023-24. This is a simplification, as many self-assessed income tax payers will make pre-payments of their income tax, known as payments on accounts. This methodology will continue to be reviewed in conjunction with users.

This methodology is applied from 2016-17 onwards, which is the period that information is available collected using new Scottish taxpayer identifiers on income tax returns. For previous years, the Scottish share of income tax liabilities from the Survey of Personal Incomes (SPI) continues to be used. GERS uses the SPI data excluding taxpayers with no postcode information for this calculation.

Differences from Previous Year’s Methodology

There are no differences from the previous year’s methodology.

National insurance contributions

Background

National insurance contributions (NICs) are a tax on earnings. Their payment is designed to allow the payee to build an entitlement to certain social security benefits, including the state pension. There are a number of different rates, thresholds and classes for national insurance. The main rate, known as the class 1 rate, was unchanged between 2011-12 and most of 2023-24 at 12% for employees and 13.8% on employers. In January 2024 the main rate for employees was cut to 10%, and in April 2024 it was cut further to 8%. There have also been changes to thresholds during this period.

For details of current thresholds and rates please see https://www.gov.uk/national-insurance-rates-letters/contribution-rates

Methodology

The UK figure for total NICs from ONS’ database underlying the Public Sector Finances is apportioned using Scotland’s share of UK class 1 NICs separately for employees and employers, using data from HMRC’s Real Time Information system provided by HMRC.

Differences from Previous Year’s Methodology

There are no differences from the previous year’s methodology.

Value added tax (VAT)

Background

Value added tax (VAT) is charged on the sale of most goods and services in the UK. Depending upon the product, VAT is charged at three different rates; during the period of the report these were: standard rate, reduced rate (5%) and zero rate. Certain services are also ‘exempt’ from VAT.

The standard rate of VAT was temporarily reduced from 17.5% to 15% on 1 December 2008, and it returned to 17.5% on 1 January 2010. The standard rate of VAT increased from 17.5% to 20% on 4 January 2011. For further details please see VAT rates - GOV.UK (www.gov.uk)

Methodology

The UK figure for total VAT revenues is taken from ONS’ database underlying the Public Sector Finances. VAT revenue is then disaggregated into VAT paid by households, businesses, government, and the housing sector.

Scotland’s share of UK VAT revenues is taken from HMRC’s Scottish VAT assignment statistics. This shows the results of the VAT assignment model jointly developed by the Scottish and UK Governments. The approach used in the VAT assignment model is very similar to that previously used in GERS. VAT is split between a number of sectors, such as households, business and government, and Scotland’s share of these sectors is estimated individually to derive an estimate of overall VAT. The VAT assignment methodology extends the approach previously used in GERS to explicitly consider VAT from tourism, and incorporates adjustments for elements such as the Retail Export Scheme and traders below the VAT schedule. Information on the results are available at Scottish VAT Assignment – Experimental Statistics - GOV.UK (www.gov.uk)

The latest estimates from the VAT assignment model are for 2022. This shows the Scottish share continuing to recover from a low figure in 2020 due to a fall in domestic tourism during the pandemic.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Corporation tax (excluding the North Sea)

Background

Corporation tax is a tax on a company’s taxable income or profits. Different rates apply depending upon the amount of profit raised. There are a number of special accounting rules for particular expenditures, such as capital investment and research and development, which qualify for tax allowances and reliefs. Details of the current tax allowances and tax rates are available at Business tax: Corporation Tax - detailed information - GOV.UK (www.gov.uk)

In the November 2022 Autumn Statement, the UK Government announced an additional Electricity Generator Levy, which came into effect on 1 January 2023 and is included within corporation tax revenue in GERS. The levy is intended as a temporary 45% charge on exceptional receipts generated from the production of wholesale electricity. Exceptional receipts will be defined as amounts from wholesale electricity sold at an average price in excess of a benchmark price of £75/MWh over an accounting period. This benchmark price will be adjusted in line with the Consumer Price Index from April 2024.

There are different rates and rules governing corporation tax of North Sea output. These are discussed in more detail later in this note.

Methodology

In general, GERS apportions a share of UK revenues from corporation taxes based on the economic activity undertaken in Scotland and not the location of companies’ headquarters. Public corporations’ and North Sea corporation tax revenues are excluded from the analysis and are apportioned to Scotland separately.

Calculating Scottish corporation tax revenues is a two stage process. Firstly the UK figure for total corporation tax is taken from ONS’ database underlying the Public Sector Finances. An adjustment is then made to remove corporation tax payments from the North Sea sector.

The Scottish share of UK corporation tax (excluding North Sea) is taken from the ONS Country and Regional Public Sector Finances publication Country and regional public sector finances - Office for National Statistics (ons.gov.uk)

Differences from Previous Year’s Methodology

The figure for financial year 2024 was provided directly to the Scottish Government by ONS, as there has been no ONS Country and Regional Public Sector Finances publication in 2025.

Fuel duties

Background

Fuel duty, formally known as hydrocarbon oil duty, is an excise duty levied on the sale of oils (including road fuels). The rate of duty levied varies between fuel types. Information on current duty rates is available from Business tax: Fuel Duty - detailed information - GOV.UK (www.gov.uk)

Methodology

The UK figure for total fuel duties is taken from ONS’ database underlying the Public Sector Finances. This is split into duty paid on petrol and duty paid on diesel using data from HMRC’s Hydrocarbon Oils Duties bulletin. Hydrocarbon Oils Bulletin - GOV.UK

As with other excise duties, the estimation of revenues raised from fuel duty in Scotland is based on the premise that the burden of duty is borne by the final consumer.

Fuel duty revenues are apportioned to Scotland by estimating Scotland’s share of UK fuel consumption. UK road traffic fuel consumption and a regional breakdown, based on weighted traffic flows on a sample of roads across the UK, are published by the Department for Business, Energy, and Industrial Strategy (BEIS). Using this information Scotland’s share of UK petrol and diesel consumption is derived. These estimates are then applied to the figure for UK revenue from each source to estimate Scotland’s share of total fuel duty.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Non-domestic rates

Background

In general, non-domestic rates, or business rates, are levied on occupiers of non-residential properties such as shops, offices, warehouses and factories. In Scotland, rates are calculated by multiplying a property’s rateable value, set by the local assessor, by the poundage rate, set by the Scottish Government. The basic poundage rate in Scotland in 2024-25 was 49.8 pence; i.e., a property with a rateable value of £10,000 would pay non-domestic rates of £4,980.

In addition, businesses with a rateable value of more than £51,000 and less than £100,000 in 2024-25 pay an intermediate supplement of 1.3 pence, and those with a rateable value of more than £100,000 pay a higher supplement of 2.6 pence. Between 2012-13 and 2014-15 large retail properties which are licenced to sell alcohol for consumption off premises and with a rateable value of more than £300,000 pay a Public Health Supplement of 13 pence.

Methodology

For earlier years the figure for Scotland is taken directly from Scottish Local Government Financial Statistics. Non-domestic rates income statistics - gov.scot

The latest year’s figure uses the published mid-year estimate. Non-domestic rates income statistics - gov.scot

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Council tax

Background

Full council tax is levied on occupiers of a house which is their sole or main residence. There are a range of exemptions and reliefs from council tax, including a 25% reduction for single occupancy households, and between 10% and 50% reduction for dwellings which are not the main residence (i.e. second homes). For further details about exemptions and reliefs from council tax please see: https://www.gov.uk/council-tax

Methodology

Council tax receipts for Scotland are taken directly from the Scottish Government. Council Tax Collection Statistics, 2024-25 - gov.scot

Since the collection year for the latest rate is provisional and is typically an underestimate due to late payments, the accrued estimate for the latest year has been taken as the net amount billed multiplied by the historic collection rate across all years.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

VAT refunds

Background

Some public sector bodies receive refunds of VAT that they have paid in respect of contracted out services for non-business purposes, including the free-to-enter public museums. As this VAT is recovered, it is netted out in departmental budgets. In the National Accounts, as these VAT payments by general government bodies form part of the prices paid as a final consumer, they are added back into government expenditure to show gross expenditure. A symmetric adjustment is made to revenues to show VAT receipts gross of these refunds.

Methodology

VAT refunds from local government and central government are apportioned differently. Local government VAT refunds are apportioned on the basis of Scotland’s share of UK local government final consumption expenditure.

Central government VAT refunds:

- to the Ministry of Defence are assigned on the basis of Scotland’s share of the UK population;

- to NHS are assigned on the basis of Scotland’s share of UK Total Expenditure on Services on health;

- to other government departments – on basis of Scotland’s share of total UK Total Expenditure on Services (less Ministry of Defence and NHS).

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Capital gains tax

Background

Capital gains tax (CGT) is a tax on capital gains from the buying and selling of assets. The capital gain is broadly the difference between the disposal proceeds and the cost of acquiring an asset. Individuals have an annual amount on which CGT is not liable and as with other forms of personal taxation various reliefs and exemptions are available.

Prior to June 2010 capital gains tax was charged at a flat rate of 10%. In June 2010, it has been charged at a basic rate of 18% and a top rate of 28% for higher-rate taxpayers. This was then changed again in 2016-17, and the tax rate now depends on whether the asset is a residential property or not.

- For higher rate tax payers:

- 24% on residential property;

- other assets. - 18% April to October 2024, 24% October 2024 onwards.

- For basic rate tax payers:

- residential property - 18%

- other assets - 10% April to October 2024, 18% October 2024 onwards.

Details of the current tax allowances and tax rates are available at Capital Gains Tax: what you pay it on, rates and allowances: Overview - GOV.UK (www.gov.uk)

Methodology

The UK figure for total CGT is taken from ONS’ database underlying the Public Sector Finances.

ONS produces estimates of the amount of revenue raised from capital gains tax in Scotland for each financial year. These annual figures are converted to quarterly estimates, and the proportion of the UK revenue raised in Scotland based on these figures is applied to the UK total. The latest estimates of Scottish revenues are for 2022-23.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Inheritance tax

Background

Inheritance tax is a tax on assets, exceeding a minimum threshold, transferred on or shortly before death. An individual’s estate on death for inheritance tax purposes is made up of a range of assets including those held directly in their name, their share of jointly owned assets and various other forms of asset. For further information regarding exemptions is available from Personal tax: Inheritance Tax - detailed information - GOV.UK (www.gov.uk)

Methodology

The UK figure for total inheritance tax is taken from ONS’ database underlying the Public Sector Finances.

HMRC produces estimates on the amount of revenue raised from inheritance tax in Scotland. The proportion of the UK revenue raised in Scotland based on these figures is applied to the total UK figure obtained from the ONS’ database. The latest HMRC data are for 2021-22.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Reserved stamp duties

Background

Stamp duty is levied on conveyances and transfers of land and property and on share transactions. Since 1 April 2015, stamp duties on transfers of land and property in Scotland have ben devolved to the Scottish Parliament, and only stamp duty on share transactions remains reserved.

For details on the rates of UK duty, please see Completing a stock transfer form - GOV.UK (www.gov.uk)

Stamp duties in GERS also include the Annual Tax on Enveloped Dwellings, which was introduced in April 2013. This is a tax payable by companies that own residential property valued at over £2 million. Further information is available at Annual Tax on Enveloped Dwellings - GOV.UK (www.gov.uk)

Methodology

The UK figure for revenue from reserved taxes is taken from ONS’ database underlying the Public Sector Finances.

Separate methods are used for estimating Scotland’s share of UK revenue raised from (1) stocks and shares stamp duties, and (2) the annual tax on enveloped dwellings.

- Stocks and Shares Stamp Duty: The Scotland/UK ratio stamp duty on stocks and shares is taken from the ONS publication Country and Regional Public Sector finances.

- Annual tax on enveloped dwellings: HMRC publishes estimates of receipts from this tax in Scotland, based upon the share of transactions of residential property valued above £1 million. This is used in place of administrative data in order to meet disclosure rules.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Land and buildings transaction tax

Background

Land and Buildings Transaction Tax replaced the UK Stamp Duty from 1 April 2015. It is a tax on purchases of commercial and residential land and buildings. The structure of the tax is designed so that the charge is proportionate to price of the property. From 1 April 2016, an additional supplement is applied to purchases of additional residential properties in Scotland, such as buy-to-let properties and second homes.

For further details and rates see Land and Buildings Transaction Tax | Revenue Scotland

Methodology

Figures reflect outturn data from Revenue Scotland. For years prior to 2024-25, figures are consistent with Revenue Scotland’s latest Annual Report - Devolved Taxes Accounts. For 2024-25, figures are based on the in-year reported amounts. There may be small differences due to timing adjustments.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Scottish landfill tax

Background

Environmental levies consist of Carbon Reduction Commitment and Renewables Obligation payments.

The Carbon Reduction Commitment is a mandatory scheme which aims to improve energy efficiency and cut emissions in large public and private sector energy users across the UK. Participants must monitor their energy supplies and purchase allowances to cover the associated CO2 emissions.

The Renewables Obligation places an obligation on UK electricity suppliers to source an increasing proportion of the electricity they supply from renewable sources. Operators require certificates for the energy they generate. Certificates can be traded between operators to ensure they have sufficient to meet their scheme targets. As the scheme is mandatory, payments associated with it are regarded as a tax, even when they are not made directly to the government. As such, revenue and expenditure associated with the scheme by energy operators are included as both an imputed tax and subsidy in the public sector finances. This does not affect the fiscal balances.

Methodology

Scotland is allocated a share of Carbon Reduction Commitment revenue in line with its share of UK electricity consumption by industry. This is taken from the BEIS Sub-national electricity consumption data. https://www.gov.uk/government/collections/sub-national-electricity-consumption-data

Figures for the Renewables Obligation are based on data on payments made by operators in Scotland, based on data provided directly by ONS.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Other taxes

Background

Other taxes and royalties comprise a number of relatively small public sector revenue sources. Each of which is apportioned to Scotland separately.

Methodology

UK revenue from other taxes is apportioned to Scotland as follows

|

Revenue |

Background |

Methodology |

|

Betting and gaming duties |

A tax on various forms of gambling. There are six different betting and gaming duties each of various rates. For example, there is a 15% tax on bookmakers’ gross profits and for non-UK established online betting and gaming operators. |

Scottish share of expenditure on gambling products is estimated using the Living Costs and Food Survey (LCF), |

|

Horserace betting levy board |

A levy on bookmakers and the Tote to fund the horserace betting levy board. |

Scottish share of expenditure on gambling products is estimated using the Living Costs and Food Survey (LCF), |

|

Climate change levy |

A levy chargeable on the industrial and commercial supply of lighting, heating and other sources of power used by industry, commerce, agriculture, public administration and other services. The levy does not apply to domestic consumers or to charities. Different rates apply for different sources of power. |

Based on Scottish consumption of electricity and gas, from BEIS. |

|

Aggregates levy |

A tax on the commercial exploitation of rock, sand and gravel. It is charged at a flat rate per tonne |

Based on Scottish Fiscal Commission estimates. |

|

Non-Fossil Purchasing Agency levy income |

OFGEM’s Non-Fossil Purchasing Agency sells renewable electricity produced under Non-Fossil Fuel Obligation orders, and may charge a levy to cover any losses it makes

|

As for renewable energy obligations |

|

Apprenticeship levy |

A tax on employers which can be used to fund apprenticeship training. |

Taken from the ONS publication Country and Regional Public Sector finances. |

|

Soft drink levy |

A tax on drinks above a specified level of sugar content. |

Scottish share is estimated using the Living Costs and Food Survey (LCF), |

|

Fossil Fuel Levy |

For years up to 2002/03, this was a levy paid by suppliers of electricity from non-renewable energy sources in the UK. The costs were passed to the consumers in the cost of the electricity supplied. The fossil fuel levy was imposed to fund the Non-Fossil Fuel Obligation. |

Based on GVA share |

|

Immigration and Health charge |

A fee paid by migrants resident in the UK for more than six months. |

As for the immigration skills charge |

|

Immigration skills charge |

A charge on employers who employ foreign workers |

As for the apprenticeship levy. |

|

Consumer Credit Act fees |

The Consumer Credit Act requires businesses that offer credit or lend money to consumers to be licensed by the OFT. This includes where credit is arranged to finance the purchase of goods or services. |

Apportioned to Scotland on the basis of Scotland’s proportion of the UK population. |

|

Northern Ireland domestic rates |

|

Not applicable to Scotland |

|

To levy funded bodies |

Statutory bodies which impose a compulsory change on industry members and exist only in the agricultural sector. |

Scotland share of agriculture GVA. |

|

Regulatory fees |

Fees and levies intended to be raised for regulatory bodies such as the FSA, the Financial Services Ombudsman and Financial Services Compensation Scheme. |

Apportioned to Scotland on the basis of Scotland’s proportion of the UK population. |

|

Boat licences |

|

Apportioned to Scotland on the basis of Scotland’s proportion of the UK population.

|

|

Milk super levy |

UK-administered quota system on milk production introduced by the EU in 1984 to curb excess production. If a producer exceeds the quota an annual super levy is charged and used to pay for disposal. |

Apportioned to Scotland on the basis of Scotland’s proportion of UK agricultural GVA. |

|

National lottery |

This is the contribution that Camelot makes to the National Lottery Distribution Fund (not part of betting and gaming duty). |

Method as for betting and gaming duty – using Scotland’s proportion of estimated UK spend on betting etc as estimated by the Living Costs and Food Survey. |

|

Rail franchise premia |

Train operators pay the government a set fee for the right to run services on the rail network. The franchises usually run for 10 years. |

On the advice of ONS, Scotland is allocated 6.7% of this revenue. |

|

Fishing licences |

These relate to Environment Agency rod licences in England and Wales. No fishing/rod licence is required for fishing in Scotland (although as per England and Wales a fishing permit is often requested by a local water authority or land owner). |

None for Scotland |

|

Passport fees |

|

Apportioned to Scotland on the basis of Scotland’s proportion of the UK population. |

|

TV licences |

|

Apportioned to Scotland on the basis of Scotland’s proportion of the UK’s estimated number of private households. |

|

Accounting adjustment |

Adjustment to constrain total UK revenue to be consistent with the latest public sector finances |

Apportioned to Scotland on the basis of Scotland’s proportion of the UK population. |

Differences from Previous Year’s Methodology

There have been no change in methodology since the previous edition of GERS.

Interest and dividends

Background

This revenue element includes all interest and dividend payments received by the public sector from the private sector and the rest of the world. Interest payments received by public sector bodies from other UK public sector bodies are not included.

Methodology

UK figures for interest and dividend revenue received by (a) public corporations, (b) local government and (c) central government and (d) public sector pensions, are obtained from ONS’ database underlying the Public Sector Finances. Following advice from the OBR, central government interest income is split into interest received from student loans and other interest income. Following the reclassification of housing associations into the public sector, public corporation interest income is split into housing association and non-housing association income.

UK central government student loans income is estimated for Scotland using actual Scottish receipts in the ONS PSAT2 database. Local government and other central government revenues from interest and dividends are apportioned to Scotland using Scotland’s share of UK population. Interest income relating to public sector pensions is apportioned using public sector GVA.

Income for Scottish housing associations is taken directly from the Scottish series for the UK Public Sector Finances. Interest income for other public corporations is apportioned using public sector GVA.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Gross operating surplus

Background

Gross operating surplus (GOS) refers to the operating (or trading) surpluses (or losses) of central government, local government and public corporation trading activity.

By definition, general government GOS is equal to general government non-market capital consumption. This is a measure of the amount of fixed capital resources used up in the production process (i.e. depreciation). Since this is a public sector receipt, that does not raise actual funds, it is balanced by an offsetting item within public expenditure. By definition, the adjustment item (NMCC) is added to public expenditure rather than subtracted on the revenue side.

For public corporations, the GOS figure includes the gross trading surplus, rental income, stock appreciation (or holding gains), and FISIM (Financial Intermediation Services Indirectly Measured).

Methodology

In calculating GOS for Scotland, separate figures are estimated for:

- Central government

- Local government

- Public corporations

1. The UK revenue for central government GOS is taken from ONS’ database underlying the Public Sector Finances.

It is apportioned to Scotland according to Scotland’s share of UK NMCC for central government obtained from ONS Regional Accounts.

2. The UK revenue for local government GOS is taken from ONS’ database underlying the Public Sector Finances.

It is apportioned to Scotland according to Scotland’s share of UK NMCC for local government obtained from ONS Regional Accounts.

3. Scotland’s share of GOS for public corporations is taken from the ONS Country and Regional Public Sector Finances.

The approach taken to estimate the GOS for public corporations in Scotland is different. The GOS of public corporations comprises the following elements –

- Gross trading surplus (from operating activities);

- Gross trading surplus (from artistic originals);

- Housing Revenue Account (HRA)

- Rental Income (excluding HRA)

- FISIM

- Holding Gains

For elements 1 and 4, revenue from every public corporation was obtained. Public corporations were classified as ‘Scotland’, ‘Not Scotland’, or ‘UK’, depending on their area of coverage. For those classified as ‘Scotland’, all of the revenue (Gross Trading Surpluses, Rental and FISIM) was assigned to Scotland. Public corporations classified as ‘Not Scotland’ were excluded. For ‘UK’ public corporations, revenue was apportioned to Scotland on the basis of the relevant industry GVA share.

Gross trading surpluses relating to artistic originals in general arise from the BBC and Channel 4. Scotland is apportioned a population share of this revenue.

For the Housing Revenue Account, figures were obtained directly for local authority rents in Scotland from ONS.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Other receipts

Background

This revenue covers other non-tax revenue received by central government, local government and public corporation trading activity. The largest component is local government rental income.

The UK figure for rents and other current transfers is taken from ONS’ database underlying the Public Sector Finances.

Rents and other current transfers for central government, local governments and public corporations are estimated separately.

Central government rents and other current transfers comprise the following elements:

- Revenues for spectrum use in relation to licences for 3G mobile telephones

- Rents on land

- Water abstraction

- Other spectrum revenues

- Court fines

- Other, e.g. speed camera fines, charitable contributions to NHS trusts

Local government other receipts comprise income of insurance and pension funds allocated to local authorities as beneficial owners.

Public corporation other receipts relate to the activities of the Export Credits Guarantee Department.

A number of revenue items are netted off in this line, as part of consolidating revenue across the public sector:

- Business rates paid by local authorities in England

- Corporation tax paid by public corporation

Methodology

The methodology for apportioning these revenues to Scotland is shown below.

|

Other receipts |

Apportionment Methodology |

|

Rents on land |

Public sector GVA |

|

Water abstraction |

Public sector GVA |

|

Other spectrum revenues |

Public sector GVA |

|

Court fines |

Separate identification of ‘Scotland’ and ‘Non-Scotland’ revenues |

|

Other, e.g. speed camera fines, charitable contributions to NHS trusts |

Public sector GVA |

|

3G and 4G spectrum receipts |

GVA |

|

Local Government and public corporation receipts |

Public sector GVA |

|

Business rates paid by local authorities |

Public sector GVA |

|

Corporation tax paid by public corporations |

As corporation tax |

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

North Sea revenue

Background

North Sea revenue in GERS comes from three sources: petroleum revenue tax, corporation tax, and licence fees. The taxation or charging regime for each of these elements is as follows:

- Petroleum revenue tax (PRT): The PRT regime has changed significantly in recent years. Historically, PRT was charged at a rate of 50% on field-based profits from oil and gas extraction on fields given development approval prior to March 1993 at which time it was abolished for all new fields. There were deductions for all exploration, appraisal, and development costs on a 100% first year basis with an uplift of 35% for field investment costs prior to field payback. There were also volume and safeguard allowances.

- In the March 2015 Budget, the rate of PRT was reduced from 50% to 35%, with effect from 1 January 2016. This change was then superseded by a reduction in the rate to 0% in the March 2016, which applied retrospectively from 1 January 2016. As companies are still able to claim refunds on PRT paid in previous years against current trading losses and decommissioning spending, PRT receipts will only be negative in the future under the current tax regime.

- Corporation tax: Ring-fenced corporation tax was charged at a rate of 30% on profits net of any PRT payments. A Supplementary Charge is levied on top of corporation tax. The Supplementary Charge has subsequently been decreased to:

- 30% from December 2014;

- 20% from January 2015;

- 10% from January 2016;

- Energy Profits Levy: On 26 May 2022, the UK Government introduced a new Energy Profits Levy. This is an tax on UK oil and gas profits on top of the existing taxes. It was initially set at 25%, before being increased to 35% in the Autumn Statement on 17 November 2022.

- Taken together, corporation tax, the supplementary charge, and the Energy Profits Levy result in an overall tax rate on ring-fenced oil and gas profits of to 75%.

- Licence Fees: The UK Government grants licences for operators to "search and bore for and get" petroleum in specified areas for a set period of time (Petroleum Act 1998 - Petroleum Act 1998 (legislation.gov.uk). Operators pay an annual fee for holding these licences. Licence fees are charged at an escalating rate on each square kilometre that the licence covers.

Methodology

Two estimates of Scotland’s share of North Sea revenue are adopted in the GERS report:

- A population share

- An illustrative geographical share

Under the population share approach, Scotland is allocated a share of the revenues associated with the North Sea based on its share of the UK population.

The illustrative geographical share is consistent with that used by the ONS in their Country and Regional Public Sector Finances publication. Country and regional public sector finances - Office for National Statistics

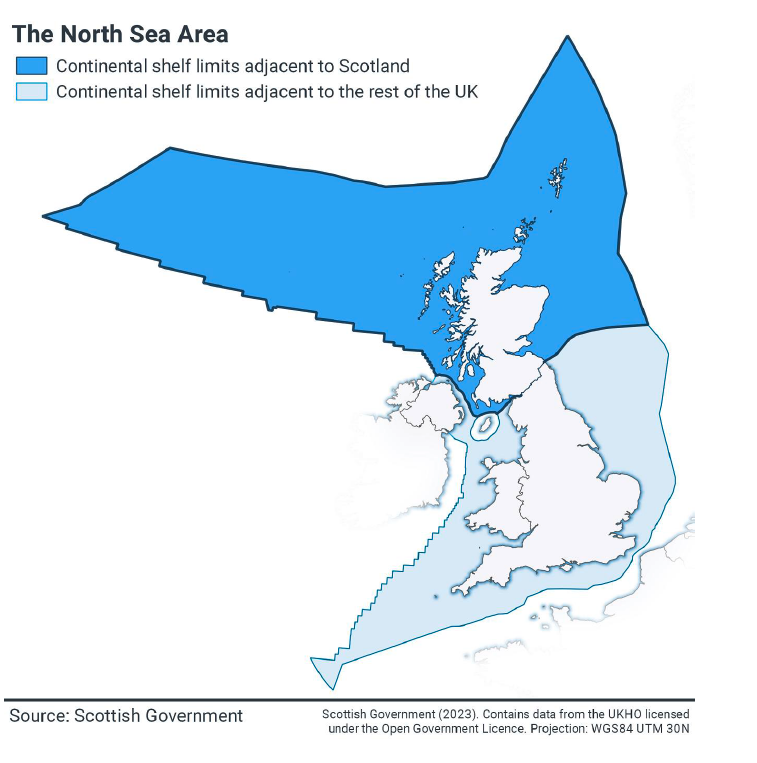

This bases the Scottish boundary of the UKCS on the median line principle as employed in 1999 to determine the boundary between Scotland and the rest of the UK for fishery demarcation purposes. Other alternatives are possible. Scotland’s estimated geographical share of the North Sea sector, used in this report, is highlighted in Figure 1 below. Demarcation by the median line is highlighted by the dark shaded area. UKCS production, costs and revenue is allocated on a field by field basis to either the rest of the UK or Scotland using this boundary.

Figure 1: UK Continental Shelf and Scottish Boundary

Using this methodology, all fields in the Moray Firth, Northern North Sea, West of Shetland regions of the UKCS are allocated to Scotland. Fields in the Southern North Sea and Irish Sea are assigned to the rest of the UK. The Scottish boundary, based on the median line principle, intersects the Central North Sea (CNS) region. Fields in the CNS region to the north of the median line are assigned to Scotland and fields lying to the south assigned to the rest of the UK. No fields are intersected by the median line.

Differences from Previous Year’s Methodology

There has been no change in methodology since the previous edition of GERS.

Contact

Email: economic.statistics@gov.scot