Framework for Tax 2021

Scotland's Framework for Tax sets out the principles and strategic objectives that underpin the Scottish Approach to Taxation, as well as our approach to decision making, engagement and how we manage and sequence tax policy and delivery.

4 Sequencing: The policy cycle and engagement

This chapter explores the timing and structure for tax policy development in the context of the policy and budget cycles respectively, identifying sequencing throughout the financial year.

Context

During every fiscal and budget cycle Scottish Ministers and the Scottish Parliament consider tax policy. This necessitates engagement, policy development, appraisal, decision making and delivery, although this can be to differing extents depending on the particular tax, timing and nature of any proposed changes. The operation of the Fiscal Framework, the timing of the UK Budget and UK tax, fiscal and macro-economic policies can all present challenges for the Scottish Government, particularly when legislation is required at short notice to protect revenues or prevent market distortions. For significant policy changes, policy development comprises the key stages of the policy cycle set out below.

The work of the Devolved Taxes Legislation Working Group seeks to develop a more structured approach to the planning, management and implementation of legislative changes to the arrangements for the fully devolved taxes. We intend to reconvene the working group in 2022, to ensure that it can continue to inform our approach. This will

build on the group's interim report, published in 2020, and separately the Scottish Government's consultation on the policy framework for the devolved taxes in 2019.

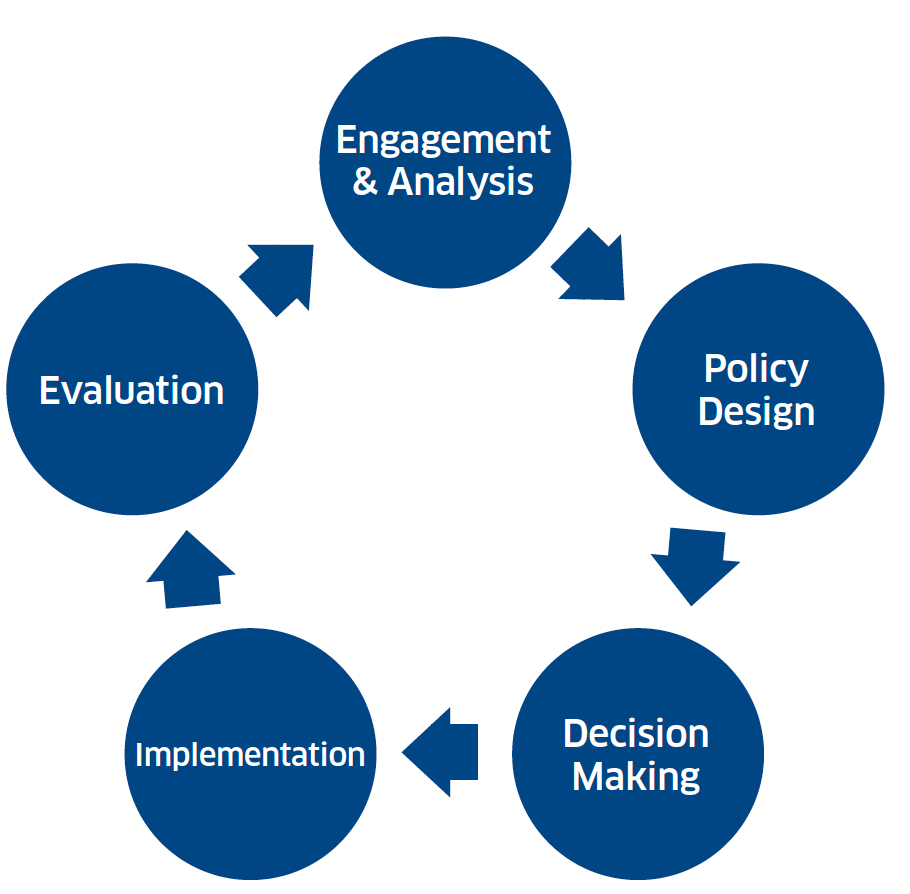

The tax policy cycle

The development of tax policy comprises five stages:

1. Engagement & Analysis: Initial analysis of calls for policy changes, including proposed objectives and rationale. Building an evidence base and assessing potential delivery issues, including engagement with the relevant tax authority. Proposals may come from ongoing evaluation, feedback from stakeholders or specific consultation, in line with our commitment to an open approach to taxation.

2. Policy design: Data and evidence analysed, proposals developed, appraisal in line with the approach set out above and any specific or wider commitments considered. For significant changes, this part of the cycle will usually be more extensive.

3. Decision making: Identification of lead options, ongoing engagement with the relevant tax authority, and in some cases ongoing dialogue with stakeholders, leading to the provision of advice to Ministers and timely decisions being taken.

4. Implementation: Delivering the necessary legislative changes and working closely with the relevant tax authority to ensure changes are implemented, clearly understood, and with efficient administration and collection (including taxpayers).

5. Evaluation: monitoring and assessing existing policy and any recent changes against intended aims and performance expectations.

Graphic text below:

- Engagement & Analysis

- Policy Design

- Decision Making

- Implementation

- Evaluation

The Scottish Budget Cycle

There are key times throughout the budget cycle where Ministers are required to consider tax changes, subject to the timing of the annual UK Budget (e.g. Autumn or Spring). As far as possible, timing will align with the policy cycle.

Autumn UK Budget: UK tax changes announced as part of an Autumn UK Budget gives the Scottish Government notice of UK tax, fiscal and macro-economic decisions in advance of the Scottish Budget. The specific timing can present challenges for the Scottish Government if significant changes are announced with little time before the Scottish Budget is published. This can impact the decisions Scottish Ministers will take and may require rapid policy development.

Scottish Budget: Decisions are typically made around rates and bands (Type A, see Table 2, below) and how these can support spending and outcomes. However the budget is also an opportunity to announce consultations on other changes, such as changes to existing reliefs or new taxes (Types B to D).

Budget Negotiations: With the Bute House Agreement, there is majority support in this Parliamentary term (2021-26) for the Scottish Budget. However, due to the design and composition of the Scottish Parliament's electoral system, it is rare that the Scottish Government will command a majority in the chamber. As such, it is often necessary to negotiate to garner Parliamentary support for the Budget Bill, which may include tax changes (this could include all decision types).

Spring UK Budget: A Spring UK Budget means that Scottish Ministers' decisions on devolved tax policy will have been made without prior knowledge of UK tax, fiscal and macro-economic decisions. This creates a risk for our tax policy decisions and could lead to unintended impacts. It may also mean that subsequent changes to devolved tax policy are required as a result of UK policies.

Types of tax policy change

The following table outlines the main categories of tax policy change:

Table 2: Decisions for tax policy changes

Policy change:

A. Changes to tax rates and bands or reliefs: usually via secondary legislation

Approach:

Typically announced in the Scottish Budget

Typical purpose:

Changes to account for inflation

Raise revenue, provide stimulus, or distribution.

Incentivise/discourage particular economic or other behaviours e.g. forestalling

Address impacts arising from UK Government announcements on tax.

Policy change:

B. Care and Maintenance: usually via secondary legislation, but some changes may require primary legislation

Approach:

May require an urgent change or be addressed as part of a Budget or consolidation package

Typical purpose:

Clarify devolved tax policy and legislation.

Address unforeseen consequences.

Protect revenue and/or strengthen delivery.

Tackle avoidance.

Ensure, where appropriate, a consistent approach across the UK.

Policy change:

C. Significant policy changes, including structural changes to a tax: likely to require primary legislation

Approach:

Policy development, underpinned by the Framework for Tax and Programme of work

Typical purpose:

Policy outcomes in relation to revenue, distribution and/or behaviours.

Address impacts, including those arising from UK Government announcements on tax.

Prevent any market distortion in Scotland or ensure a common UK approach, where appropriate.

Policy change:

D. Introducing a new tax: likely to require UK secondary and Scottish primary and secondary legislation

Approach:

Policy development, underpinned by the Framework for Tax and Programme of work

Typical purpose:

Create new sources of revenue, stimulus or distribution.

Promote behavioural change.

Address particular challenges, e.g. shifting or eroding tax base, or to support emerging SG objectives.

Implement devolution, for example a new devolved tax.

Sequencing

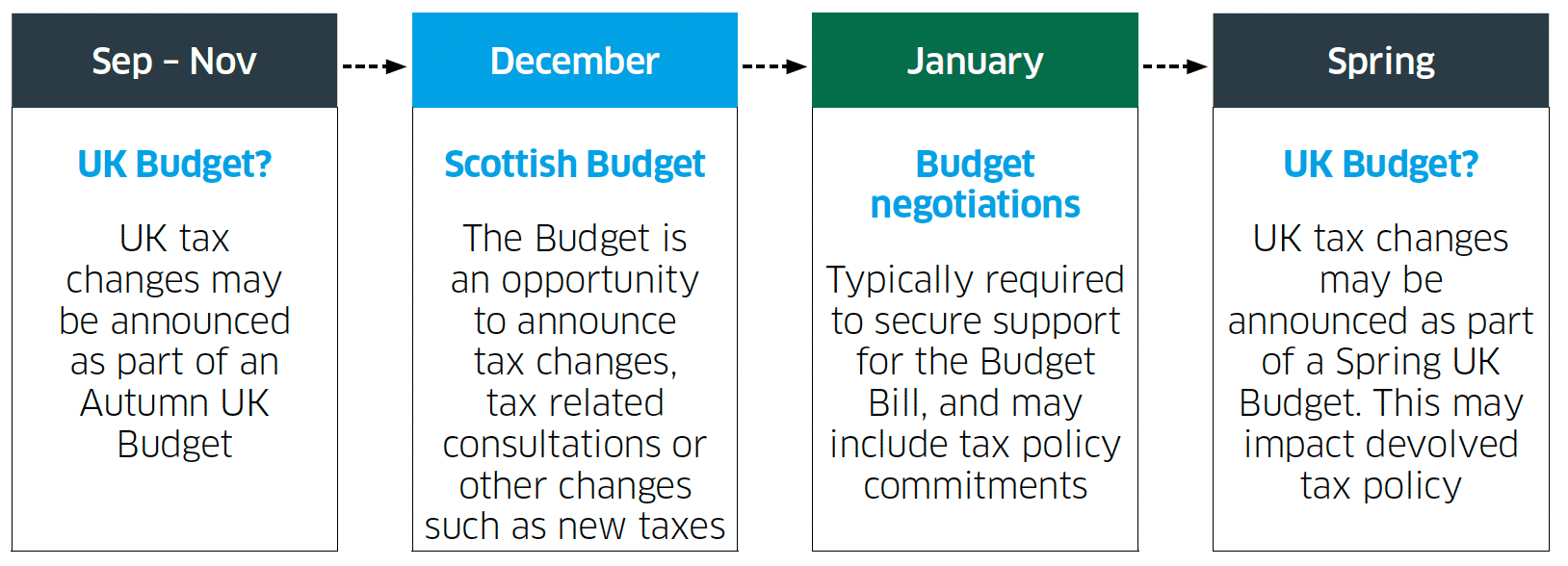

We will normally approach our annual planning cycle as follows, although timing and policy development can be affected by the specific timing of the UK Budget and fiscal events, as set out above.

Sep – Nov

UK Budget?

UK tax changes may be announced as part of an Autumn UK Budget

December

Scottish Budget

The Budget is an opportunity to announce tax changes, tax related consultations or other changes such as new taxes

January

Budget negotiations

Typically required to secure support for the Budget Bill, and may include tax policy commitments

Spring

UK Budget?

UK tax changes may be announced as part of a Spring UK Budget. This may impact devolved tax policy

Graphic text below:

Sep – Nov

UK Budget?

UK tax changes may be announced as part of an Autumn UK Budget

December

Scottish Budget

The Budget is an opportunity to announce tax changes, tax related consultations or other changes such as new taxes

January

Budget negotiations

Typically required to secure support for the Budget Bill, and may include tax policy commitments

Spring

UK Budget?

UK tax changes may be announced as part of a Spring UK Budget. This may impact devolved tax policy

Changes to devolved taxation will follow different cycles, depending on the nature of the change. Type A and B decisions for change, i.e. changes to existing rates and bands or operational maintenance of existing devolved taxes, are likely to take place either on an ad hoc basis, or most likely as part of the annual Scottish Budget.

Type C and D changes, i.e. major structural reforms to existing devolved taxes, or the introduction of new local or national devolved taxes, are likely to be announced at the Scottish Budget and may span several budget cycles, given the requirement for evidence gathering, consultation, design and primary legislation that underpins good tax policy making. For new national taxes, this is in addition to negotiation and securing agreement

of the UK and Scottish parliaments to devolve the requisite powers, which introduces further uncertainty over precise timelines.