Framework for Tax 2021

Scotland's Framework for Tax sets out the principles and strategic objectives that underpin the Scottish Approach to Taxation, as well as our approach to decision making, engagement and how we manage and sequence tax policy and delivery.

3 Strategic objectives and decision-making

This chapter sets out the Scottish Government's strategic objectives for tax policy and the factors we seek to weigh and balance when making decisions.

Context

We will seek to align tax policies with the Scottish Government's operating environment

and have regard to key strategies, which include:

- The Scottish Government's economic strategy

- The operation of the Fiscal Framework

- The Medium Term Financial Strategy

- Scotland's spending, capital and infrastructure plans

- Scotland's National Performance Framework

- The Climate Change Plan

- The Programme for Government

- The Shared Policy Programme with the Scottish Green Party

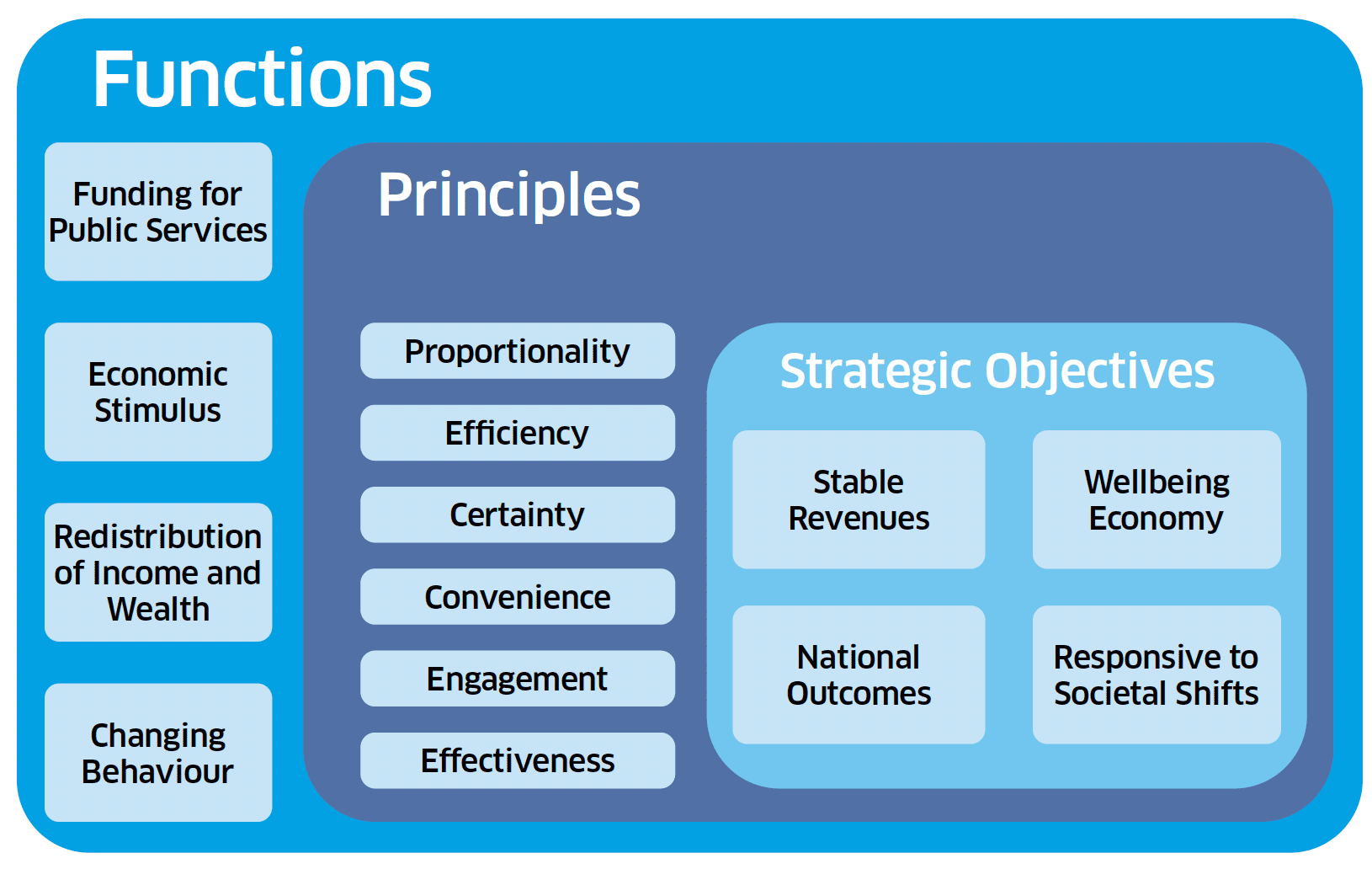

Visualisation of this Framework

Taken together, the functions of tax policy, our principles and our strategic objectives form a solid foundation for a coherent approach to tax policy in Scotland.

Graphic text below:

Functions

- Funding for Public Services

- Economic Stimulus

- Redistribution of Income and Wealth

- Changing Behaviour

Principles

- Proportionality

- Efficiency

- Certainty

- Convenience

- Engagement

- Effectiveness

Strategic Objectives

- Stable Revenues

- Wellbeing Economy

- National Outcomes

- Responsive to Societal Shifts

Strategic Objectives

In light of COVID-19, our public finances face unprecedented circumstances. Our ambition is to support Scotland's recovery and renewal towards a greener, fairer and more inclusive society. In the longer term, tax policy will also play a crucial role in ensuring fiscal sustainability, tackling climate change and reducing inequality.

To this end, the Scottish Government is pursuing four strategic objectives for tax:

- Generating stable revenues to fund public services and support social renewal, ensuring Scotland's public finances are fiscally sustainable.

- Supporting a wellbeing economy by helping to deliver a sustainable and inclusive economic recovery and support new, good green jobs, businesses and industries for the future.

- Delivering national outcomes by reducing inequality and funding the public services that promote and protect the wellbeing and rights of our citizens.

- Delivering a tax system with the ability to respond to societal and economic shifts by ensuring that tax policies and processes are robust and flexible.

Appraisal and Decision Making

Policy appraisal ensures existing tax policies and new proposals are balanced, coherent and deliver against objectives. Our goal is therefore to ensure decisions are based on the best evidence available and taken in the round, and we are being transparent about how we seek to do that.

The table below comprises the key factors that guide our decisions on tax policy. It is not intended to operate as a mandatory checklist for every change to tax policy and, similar to our guiding principles, it is not a list of absolutes. It supports a methodical and consistent approach to appraisal, identifying any tensions and conflicts to assess the relative merits of potential tax policy changes.

Table 1: Matrix for tax decision making

Fiscal Impacts

Proposals must be accompanied by a policy costing, including an estimate of the impact on our funding position and, where appropriate, an analysis of the distributional impacts. This should include the potential for long-term economic impacts, as well as any impacts on future budgets and the tax base.

Principles and Objectives

Policy options should be considered against the Principles of Good Tax Policy Making, with a clear rationale for any deviation, as well as our strategic objectives and the core policy objectives of the proposed change, identifying any conflicts or trade-offs.

Policy Alignment

Proposals should be considered in the round alongside: other devolved and local tax policies; our economic strategy; spending plans; social security commitments; wider devolved and local government policies; and UK tax and fiscal policies. Analysis should seek to identify any conflicts or trade-offs.

Affordability and Value for Money

Policy costings should be assessed for affordability and value for money, particularly if tax reliefs or exemptions are being considered.

Impact Assessment

The policy development process should surface and consider potential impacts, including unintended consequences, and include applicable impact assessments. For example, in relation to equalities, business and regulation, the environment, human rights and the Fairer Scotland Duty.

Deliverability and Administration

Issues pertaining to delivery, administration and collection should be identified and considered at the earliest opportunity, in consultation with the relevant tax authorities, including consideration of the administrative burden on taxpayers and other delivery partners. Assessment should also be given to any legal, operational or political concerns and impact on the Fiscal Framework or in relation to devolution. Timing of a proposed intervention should be considered in relation to fiscal and economic cycles.