Framework for Tax 2021

Scotland's Framework for Tax sets out the principles and strategic objectives that underpin the Scottish Approach to Taxation, as well as our approach to decision making, engagement and how we manage and sequence tax policy and delivery.

2 Principles of good tax policy making

Every tax performs one or more of the following functions:

- raising money to fund public services;

- providing economic and social stimulus;

- promoting a more equal society through redistribution;

- encouraging taxpayers (businesses and/or individuals) to change their behaviour.

Any tax system must generate sufficient revenues to support government spending, ensuring revenues grow in line with demographic and economic conditions and reflecting broader changes in technology and society. There are also times when tax policy can be used as a lever for economic and social stimulus. Taxes play a role in the redistribution of income and wealth, especially through progressive taxation. Finally, tax can be used as a lever to increase the cost of harmful behaviours, or reduce the costs of desired behaviours, in order to incentivise change.

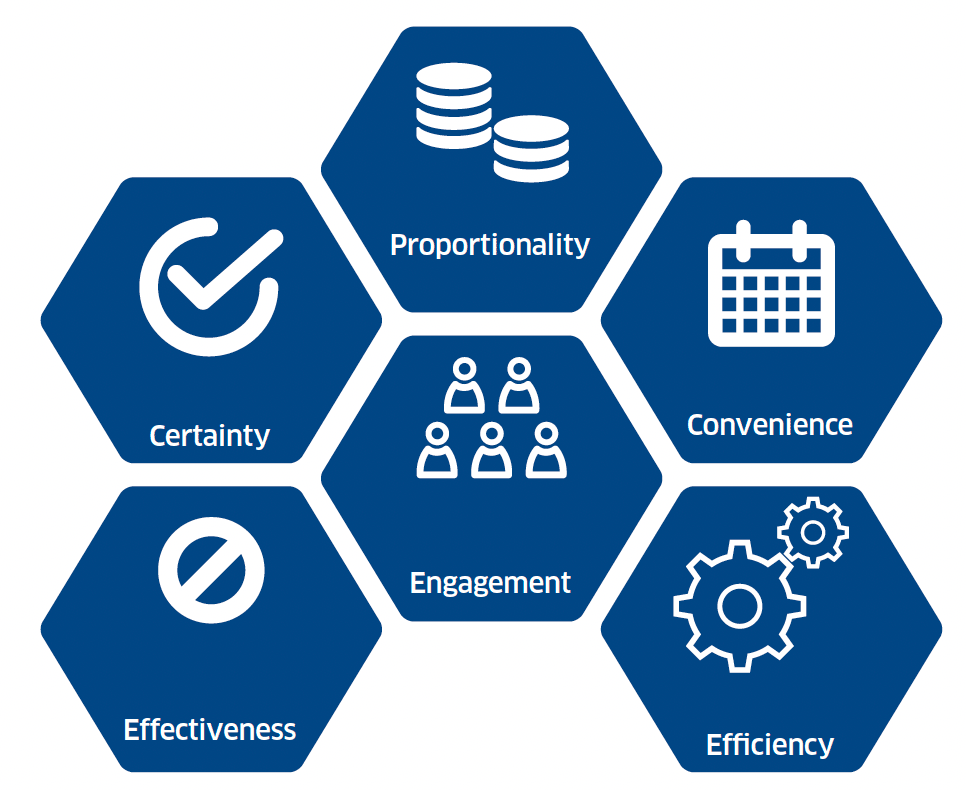

The Scottish Government's approach to tax policy has developed over time, particularly following the devolution of further tax powers in 2016. Our approach is underpinned by a set of principles, including the four principles of taxation proposed by the Scottish economist Adam Smith (namely: Certainty, Proportionality to the ability to pay, Convenience and Efficiency). We have added Engagement and Effectiveness to embed a set of six guiding principles that will underpin tax policy in Scotland. We have set out below how each of those principles is interpreted and applied by the Scottish Government today.

This is not an exhaustive list. It reflects prominent attributes of good tax policy design; a set of values that can be identified in international good practice and tax policy literature, as well as the fabric of our approach to date. Nor is it a list of absolutes. There may be tension or conflict between certain principles in specific cases. Hence, these serve as a basis against which to assess tax policy and promote system-wide coherence.

Graphic text below:

- Proportionality

- Certainty

- Convenience

- Engagement

- Effectiveness

- Efficiency

Proportionality: Taxes should be levied in proportion to taxpayers' ability to pay. The Scottish Government also believes that a fair tax system should be progressive, i.e. that the proportion of tax paid should reflect the relative income or wealth of the taxpayer. Equally, comparable circumstances should attract comparable tax treatment, in the absence of strong justification to the contrary.

Efficiency: The tax system must balance the prospects for revenue against the potential for unintended behavioural responses. If such responses reduce economic activity – where, for example, a tax change prompts employees to cut back on working hours – they can create economic inefficiencies.

Certainty: Taxpayers must know if they are liable to pay tax, the amount to be paid and when it is to be paid. This allows businesses and individuals to plan and invest with confidence. Changes to the tax system should be justified and, where possible, follow a predictable fiscal cycle or published roadmap.

Convenience: Taxes should be collected at a time and in a manner that maximises convenience for taxpayers. Tax policy should be as simple, clear and straightforward as possible and opportunities to streamline the tax system should be taken where they arise.

Engagement: People and businesses should be able to understand the tax system and governments and tax authorities play a critical role in relation to that. Governments must therefore be open and transparent about tax policies and their decision-making, consulting as widely as possible. This is crucial for accountability and trust.

Effectiveness: Design of the tax system should focus on ensuring taxes raise the expected revenues and achieve their intended aims. This includes designing taxes that minimise opportunities for tax avoidance. The vast majority of taxpayers want to pay the correct amount of tax, and do, but where taxpayers do engage in avoidance practices governments and tax authorities should respond quickly and proactively to tackle them.