Fiscal framework outturn report: 2023

The Fiscal Framework Outturn Report 2023 publishes outturn and reconciliation information for Scottish Income Tax, Scottish Landfill Tax, Land and Buildings Transaction Tax and devolved Social Security benefits, as well as updates on borrowing and the Scotland Reserve.

3. Income Tax

28. Since April 2017, the Scottish Parliament has had the power to set rates and bands for non-savings, non-dividend Income Tax. This includes earnings from employment, self-employment, pensions and property. The responsibility for defining the Income Tax base, which includes the setting or changing of Income Tax reliefs and exemptions, and the tax-free Personal Allowance, remains reserved to the UK. For any income people get from savings or dividends, the rates and bands are also set by the UK Government. Scottish Income Tax is therefore a partially devolved tax.

29. For Scottish Income Tax, outturn data is normally available around 16 months after the end of the financial year and a single reconciliation is applied to the following Budget, three years after the original Budget was set. For example, the reconciliation relating to Income Tax in the 2018-19 financial year was applied to the 2021-22 Budget.

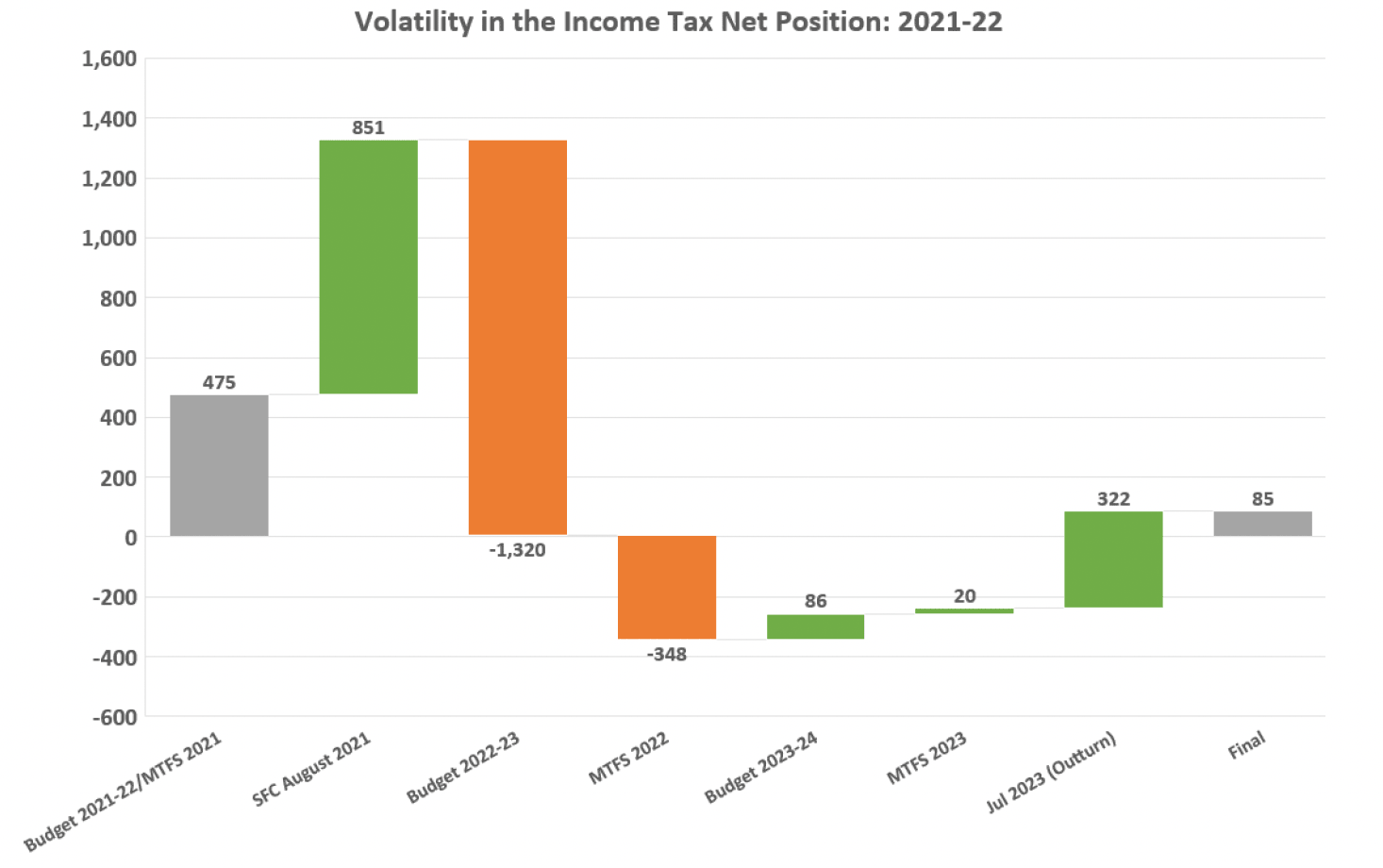

30. Final outturn data for 2021-22 Income Tax was published by HMRC on 6 July 2023. This data has been used to calculate the provisional reconciliations to the Scottish Government’s Block Grant, which will be applied to the 2024-25 Budget. Table 3 shows the data, together with the net effect on the Budget.

| 2021-22 Income Tax | Revenues | BGA* | Net effect on Budget |

|---|---|---|---|

| Forecast as of Budget Act 2021 | 12,263.3 | -11,788.1 | 475.2 |

| Outturn | 13,724.4 | -13,639.0 | 85.4 |

| Outturn against forecast | 1,461.1 | -1,851.0 | -389.9 |

31. This translates into a £389.9 million negative reconciliation requirement that will be applied to the 2024-25 Budget (see section 8 for a full breakdown of reconciliations for the 2024-25 Budget).

32. The forecast for 2021-22 Income Tax revenue compared to the corresponding BGA was forecast to have a positive net effect on Scotland’s finances at the time of setting the 2021-22 Budget, with revenues forecast to exceed the BGA by £475.2 million. The outturn data details that revenues did exceed the BGA, but by £85.4 million. This translates into a £389.9 million negative reconciliation, in order to correct for the forecast error within the 2021-22 Budget. This is a normal part of the Fiscal Framework and the application of reconciliations to correct for forecast error should not be interpreted as a reflection of the underlying performance of the Scottish or equivalent UK tax base.

33. This is also the biggest Income Tax reconciliation payment for forecast error faced to date, however, this was not unexpected as the original Budget forecasts were produced during the height of the Covid-19 pandemic. This was a time of unprecedented economic uncertainty, and forecasts were therefore subject to a much greater degree of error due to differences in data, judgement and timing of the SFC’s and OBR’s forecasts. At the time, the SFC cautioned that a negative reconciliation was likely, suggesting a value of -£300 million[4].

34. Fiscal devolution means that the Scottish Budget is now more closely linked to Scotland's relative economic and tax performance, which is in turn driven by regional and sectoral patterns, demographics, and the composition of the tax base as well as differences in government economic and tax policy.

35. The SFC estimate that Income Tax policies implemented since 2017-18 have raised up to £750 million in 2021-22, when compared with matching Income Tax policy in the rest of the UK. However, relatively weaker economic performance alongside differences in the income distribution have partly offset this. Therefore, the overall benefit of Income Tax devolution to the Scottish Budget in 2021-22 has been £85 million.[5]

36. The outturn data for Income Tax 2022-23 and 2023-24 should be available in summer 2024 and 2025 respectively, with reconciliations then being applied to the 2025-26 Budget and 2026-27 Budgets.

37. Estimates of future reconciliations for the financial years 2022-23 and 2023-24 are directly derived from latest SFC and OBR forecasts. They have a direct bearing on the Scottish Government’s multi-year funding envelope as they inform decisions on future resource borrowing and spending.

38. As highlighted in Box 3 of the 2023 MTFS, there is significant volatility in the forecasts produced in between the budget setting forecasts and final outturn. This will in part reflect that the net position is the difference between the forecasts of two large numbers (income tax and the BGA), and so small changes in either forecast can result in large changes in the net position, as illustrated in Table 4.

39. The SFC’s Forecast Evaluation Report also noted that there is no clear evidence that estimates of future reconciliations get better, or worse, over time.[6] The Commission is therefore exploring alternative approaches to producing and reporting on indicative reconciliation estimates.

40. New forecasts for reconciliations which reflect the latest outturn data will be published at the next fiscal event and will inform the 2024-25 Scottish Budget.

Contact

Email: rory.mack@gov.scot