Five Family Payments: evaluation

This report details findings from an evaluation of the Five Family Payments.

Findings

In this chapter of the report, the data sources outlined in the methodology chapter are used to evaluate progress towards the Five Family Payments’ immediate, short-term and medium-term policy outcomes. Based on this, likely progress towards the Scottish Government’s long-term outcomes are assessed.

Achievement against immediate Five Family Payment policy outcomes

This section evaluates the Five Family Payments against the following policy outcomes, which are relevant to one or more of the benefits:

- The benefits are well promoted (All benefits)

- The benefits and their eligibility criteria are well understood (All benefits)

- The benefits are taken up (All benefits)

- Making an application is clear and easy (All benefits)

- Applications and payments are processed in a timely manner (All benefits)

- Awareness is raised about other forms of support (All benefits)

- Clients feel they have been treated with dignity, fairness and respect (All benefits)

- Card reduces stigma and is easy to use (Best Start Foods)

- Card provides access to a range of retailers (Best Start Foods)

- Card provides access to a range of healthy foods (Best Start Foods)

It uses data from a range of sources, primarily Official Statistics, estimated take-up rates of Scottish benefits, the Social Security Scotland Client Survey, and bespoke commissioned research. Where appropriate, findings from the previous evaluations of the Five Family Payments are also cited. The section ends with a recap of achievement against immediate Five Family Payments policy outcomes, based on a summary of key findings.

Please note that, throughout this section, notable differences in how subgroups of Client Survey respondents answered questions have been presented. As explained in the Methodology chapter, these are reported in cases where the difference between the subgroups was more than 5 percentage points.

The benefits are well promoted

This outcome is relevant to all of the Five Family Payments benefits. There are a number of indirect ways to evaluate whether the Five Family Payments are well promoted. One indirect method is to look at overall take-up of the benefits, which could be impacted by promotional activity.[22] Take-up refers to the extent to which people receive the benefits they are eligible for. This can be estimated by measuring the ‘take-up’ rate, which is the number of benefit recipients divided by the number of people eligible to receive the benefit.

Take-up estimates are provided for the Five Family Payments in the annual Take-up rates of Scottish benefits publication. The most recent estimates show:

- Take-up for Scottish Child Payment was 89% in 2023-24

- Take-up for Best Start Grant Pregnancy and Baby Payment was 87% in 2022-23

- Take-up for Best Start Grant Early Learning Payment was 87% in 2021-22

- Take-up for Best Start Grant School Age Payment was 97% in 2023-24

- Take-up for Best Start Foods was 84% in 2023-24.[23]

These figures show that most people who were eligible for the Five Family Payments received the benefits. While it is not possible to isolate the impact of promotional activity on take-up, promotions are likely to have contributed to these figures to some extent, as indicated by the findings in Table 3 below. However, further steps are still needed to maximise take-up of the Five Family Payments.

Another way to evaluate the promotion of the Five Family Payments is to consider how people found out about them. The Client Survey asks respondents how they first found out about the benefit(s) they applied for. The findings in Table 3 show respondents found out about the Five Family Payments in a range of ways.[24] For all application types, the most common responses were word of mouth (25%), online or social media (13%), and the health service (11%).

Notably, those who made an application which included Best Start Grant and Best Start Foods were most likely to say they found out about the benefits via the health service. For example, 25% of those who made a joint application for Best Start Grant and Best Start Foods found out about them via the health service, compared to 5% who applied for Scottish Child Payment only. This reflects findings from the previous evaluation of Best Start Foods, which showed recipients commonly heard about it from healthcare professionals they were in regular contact with, such as family nurses and health visitors. It also reflects the differing nature of the policies and their eligibility criteria – i.e. Best Start Foods and Best Start Grant can be claimed during pregnancy, and are for younger children only, whereas Scottish Child Payment can only be claimed once children are born, and is available to older children (up to 15 years old).

| Response option | Joint application for Best Start Grant, Best Start Foods, and Scottish Child Payment | Joint application for Best Start Grant and Best Start Foods only | Application for Scottish Child Payment only | All applications |

|---|---|---|---|---|

| Social Security Scotland contacted me (for example, phone call or letter) | 9% | 6% | 6% | 7% |

| Advert (for example, TV, radio, newspaper) | 3% | - | 6% | 4% |

| Online or social media (for example, Twitter, Facebook) | 11% | 14% | 14% | 13% |

| News article or programme (including radio) | 1% | # | 2% | 1% |

| Word-of-mouth | 21% | 20% | 28% | 25% |

| Citizens Advice | 7% | 5% | 8% | 7% |

| Department for Work and Pensions (DWP), including Jobcentre Plus | 9% | 6% | 10% | 9% |

| Health service (for example, NHS worker, GP, Health Practitioner, Psychologist) | 18% | 25% | 5% | 11% |

| Community or social care service | 4% | 3% | 5% | 4% |

| Leaflet, pamphlet or poster | 3% | # | 1% | 2% |

| Other | 14% | 19% | 18% | 17% |

| Total number of respondents | 1,489 | 293 | 2,129 | 3,911 |

There were notable differences in how respondents found out about the Five Family Payments benefit(s). With regards to the priority families at risk of poverty:

- Families from white ethnic backgrounds were more likely than families from minority ethnic backgrounds to have found out about the benefits via word of mouth (28% compared with 18%)

- Families with a mother aged under 25 were more likely than families without a mother aged under 25 to have found out about the benefits via the health service (30% compared with 11%)

- Families with children aged under 1 were more likely than families without a child aged under 1 to have found out about the benefits via the health service (25% compared with 7%).

Additionally, respondents with an unsuccessful application outcome were more likely than respondents with a successful outcome to have found out about the benefits via the health service (16% compared with 10%).

The commissioned research also provides an insight into the promotion of the benefits. In qualitative interviews, participants were asked how they became aware of the Five Family Payments. Their answers broadly reflect the findings in Table 3 above. They specifically said they found out about the benefits:

- Through word of mouth, such as from friends, family and colleagues

- From conducting their own research online

- From their midwife, family nurse or health visitor

- From other professionals they were in contact with

- From social media platforms and national news

- From their children’s schools

- From their local council and through communication from Social Security Scotland.

Participants were also asked about possible barriers to claiming Five Family Payments, based on their own experience of claiming them. They commonly cited a lack of knowledge and awareness about the benefits, perceiving there to be a lack of promotion within local communities. The qualitative evidence also demonstrated that awareness of the Five Family Payments can be mixed, with some parents saying they missed the chance to receive payments at an earlier date, or receiving certain payments altogether. Examples included claiming Best Start Grant but not being aware of Scottish Child Payment at the time, and only finding out about Best Start Grant and Best Start Foods after their child was born.

I just found out about [Scottish Child Payment] about a year and a half ago. It’s not a payment everyone knows about and it’s helped me with day to day living so I’ve lost so many years as it’s not an advertised payment.

(Survey respondent)

She [family nurse] asked me if I was receiving [Best Start Foods] and I was like, 'No, I didn't even know about it.' Then she was like, 'Oh, you could've been getting it this whole time,' and I was like, 'Oh great.' At least I found out later than never. Better late than never.

(Parent and carer interview)

Also in qualitative interviews, stakeholders acknowledged that take-up of the Five Family Payments was high in general. However, they felt that awareness was low amongst specific groups, such as families with older children, women who were pregnant with their first child, survivors of domestic abuse, those with English as a second language, and lone parent fathers.

Stakeholders also perceived there to be a lack of media coverage of devolved benefits, which they felt made them less well-known than reserved benefits. They also felt the complexity of the benefits system (i.e. having devolved and reserved benefits administered by different agencies) was a barrier to the Five Family Payments. For example, they said Child Benefit and Scottish Child Payment were commonly confused, with families receiving Universal Credit and Child Benefit assuming they were already receiving all of their benefit entitlements. Having two benefit systems was cited as a particular issue for migrant families with the Right to Reside or Habitual Residency, who it was said were often preoccupied with Universal Credit claims and therefore unaware of devolved benefits. There was also a perception amongst stakeholders that the DWP do not explicitly advertise Social Security Scotland benefits to Scottish clients, and vice versa.

I would say they’re [parents who have migrated] definitely the biggest percentage of parents that haven’t claimed benefits and have absolutely no idea and because usually once they get the Right to Reside and Habitual Residency and they’re claiming Universal Credit they’re so focused on claiming Universal Credit because that’s the benefit that is going to keep them going. They don’t realise there’s other things, and the problem is when it comes to advertising or information, the DWP won’t tell you about Social Security Scotland and Social Security Scotland won’t tell you about the DWP benefits.

(Stakeholder interview)

The benefits and their eligibility criteria are well understood

It is intended that the Five Family Payments and their eligibility criteria should be understood by potential applicants. This outcome is relevant to all of the Five Family Payments benefits. Previous evaluations of Scottish Child Payment and Best Start Foods found that, overall, people understood that the purpose of the benefits was to help with the costs of raising a family and to buy healthy foods, respectively. In the commissioned research undertaken for the current evaluation, findings on how people used the Five Family Payments also demonstrate that recipients understand the purpose of the benefits. (For more detail on how people used the benefits, see the ‘Achievement against short-term policy outcomes’ section below.)

However, previous evaluations of Scottish Child Payment and Best Start Foods also showed that there was some confusion over the eligibility criteria for the benefits amongst applicants. One way to assess whether the Five Family Payments eligibility criteria are understood is by looking at the proportion of applications that have been denied. This is because benefit applications are denied in cases where applicants are ineligible, which, in some cases, could be due to a misunderstanding of the eligibility criteria.[25] Official Statistics provides the following information about denied applications in the 2024/25 financial year:

- 28% of Scottish Child Payment applications were denied

- 34% of Best Start Grant and Best Start Foods applications were denied

These statistics show that around 1 in 3 Five Family Payments applications were denied in the 2024/25 financial year, which indicates that there is still some confusion around the eligibility criteria amongst applicants. Notably, however, evidence from the commissioned research indicates that people who have applications denied are not always ineligible for the Five Family Payments. In the qualitative interviews, parents and carers who went on to claim payments spoke about having their initial applications denied, despite being eligible at the time. This was often a result of not providing enough supporting evidence. One recipient said that when this happened to them they did not know why their application was denied until they contacted Social Security Scotland.

[…] it was a lot of unnecessary anxiety that it caused, because twice they were like, 'We can't offer you it', instead of looking at it and being like, 'Oh, we could offer you it, if you give us this evidence.' But both times, it was a solid no and I'm sitting there thinking, 'But I meet all the criteria. How are you saying no to me?'

(Parent and carer interview)

The Client Survey also provides evidence on the clarity of eligibility rules. It asks respondents who looked up the Social Security Scotland website if it made their eligibility clear or not. Amongst Five Family Payments applicants, 80% strongly agreed or agreed the information made it clear if they were eligible or not, whilst 11% neither agreed nor disagreed, and 9% strongly disagreed or disagreed (n=2,246). With regards to the priority families at risk of poverty, the following subgroups were more likely than others to agree the website made their eligibility clear:

- Families from minority ethnic backgrounds (88%) compared to families from white ethnic backgrounds (78%)

- Families with three or more children (87%) compared to families with one or two children (79%)

- Families with no child aged under 1 (82%) compared to Families with children aged under 1 (75%).

Respondents with a successful application outcome (88%) were also more likely to agree the website made their eligibility clear compared to respondents with an unsuccessful outcome (60%).

The benefits are taken up

Take-up rates and potential barriers to take-up

Take-up refers to the extent to which people receive the benefits they are eligible for. This outcome is relevant to all of the Five Family Payments benefits. A direct way to assess progress on this outcome is to estimate the ‘take-up’ rate, which is the number of benefit recipients divided by the number of people eligible to receive the benefits. As mentioned above, take-up rates are provided in the annual Take-up rates of Scottish benefits publication. The most recent take-up estimates for the Five Family Payments were as following:[26]

- 89% for Scottish Child Payment in 2023-24

- 87% for the Best Start Grant Pregnancy and Baby Payment in 2022-23

- 87% for the Best Start Grant Early Learning Payment in 2021-22

- 97% for Best Start Grant School Age Payment in 2023-24

- 84% for Best Start Foods in 2023-24.

Notably, for Scottish Child Payment, the take-up rate in 2023-24 was 97% for children aged under 6 and 85% for children aged 6 to under 16. Additionally, analysis of quarterly Scottish Child Payment take-up rates throughout 2023-24, for June, September, December and March, show estimated take-up rates for children aged 6 to under 16 steadily increasing over that time. Furthermore, take-up rate estimates for Scottish Child Payment are also now published by local authority. In 2023/24 they ranged from the lowest estimates of 84% for Aberdeenshire, East Dunbartonshire and East Renfrewshire, to the highest estimate of 94% for Falkirk.

These figures show that take-up was generally high for the Five Family Payments, and was especially high for Scottish Child Payment (for families with children aged under 6) and the Best Start Grant School Age Payment. Notably, automated payments were introduced for the latter in November 2022 for families who already received Scottish Child Payment. [27] However, despite these positive findings, further steps are still needed to maximise take-up of the benefits.

The commissioned research provides some evidence on potential barriers to take-up. In the qualitative interviews, Five Family Payments recipients and stakeholders were asked, based on their own experience, what factors could prevent take-up of the benefits. As mentioned above, a lack of awareness was commonly raised, with some recipients saying they personally missed the chance to receive payments at an earlier date because they did not know about them at the time – e.g. only finding out about Best Start Foods after their child was born. A perceived lack of promotion and issues around the complexity of the benefits system were offered as reasons for low awareness.

Stakeholders also said some claimants needed benefit advisors with in-depth knowledge of reserved and devolved benefits to ensure they get all of the benefits they are entitled to, and felt there was a lack of trained advisors in Scotland who were able to do this, citing a perceived prevalence of non-specialist support workers relying on benefits calculators. Parents and carers also described instances of receiving incorrect information and advice regarding their eligibility to apply for the Five Family Payments.

I think nowadays if you were to go into loads and loads of advice agencies and ask somebody to sit down with a pen and a bit of paper and do a benefit check with the rates, I don’t think they would be able to do it. I think people now are relying on benefit calculators and if you’re relying on a benefit calculator you don’t understand the system so you’ll maybe no’ necessarily understand what could make a difference in this person’s circumstances…I think in Scotland there is a real lack of people that can do an in-depth benefit check in that respect.

(Stakeholder interview)

[A third sector staff member] told me that I wasn't entitled to it when I was entitled to it, and that's as well how people would maybe not be able to get these payments, because they maybe go to the wrong person for advice and get the wrong advice, and that's put a stop to it.

(Parent and carer interview)

Stakeholders frequently cited issues faced by minority ethnic families with limited English, which was described as a ‘massive barrier’, as they could be unable to read application forms or find it challenging to contact organisations for support. They also flagged that, in some cases, people are illiterate in their own language, or speak rare dialects of their native language, meaning they also struggle to read translated information. Furthermore, stakeholders said that it could be difficult for some ethnic minority families to make claims due to a lack of documentation e.g. photo ID and children’s birth certificates.

Other issues flagged by stakeholders that could be affecting take-up of the Five Family Payments were:

- Having initial applications denied (e.g. due to a lack of supporting evidence, or applying before becoming eligible), which can put people off applying again

- Digital poverty, with claimants not having access to a computer and/or limited data on their phones

- Digital illiteracy and general issues with literacy, with cases of parents and carers being unable to read their address, NI number, or passport information, and struggling to navigate the Scottish Government website

- The mental burden of poverty giving some people limited capacity to think about benefit applications, because they are often in crisis mode

- The stigma that can be associated with receiving benefits, especially if it is the person’s first time needing help

- For survivors of domestic abuse, concerns around sharing personal details and potentially putting themselves at risk of harm.

Notably, a secondary analysis of open-text responses to the Client Survey highlighted a small number of cases where survivors of domestic abuse faced barriers when applying for the Five Family Payments. More detail than is available in the open-text responses would be required to fully interpret these cases. However, respondents mentioned difficulties providing paperwork that would be accepted as supporting information by Social Security Scotland.

There is information on your website regarding extra support for second child [for Best Start Grant Pregnancy and Baby Payment] if you have experienced domestic abuse. Unfortunately after disclosing information…I am unsure what relevant documents would be needed to support this. I was unfortunately declined the ‘double payment’ and my case was closed at the re decision stage. […] Unfortunately I was previously told by an advisor that I was 100% eligible for the double payment.

(Client Survey open-text response)

The application itself was relatively simple. However, it did not allow for my circumstances of abuse to be considered thoroughly and therefore left me in an unfortunate position. Had it been taken into consideration, I feel my initial outcomes would have been different. […] there wasn’t/isn’t really much room for this as part of the process.

(Client Survey open-text response)

In the commissioned research interviews, stakeholders and recipients suggested measures they felt could increase take-up of the Five Family Payments, relating to the barriers mentioned in the bullet points above. For example, tackling stigma in promotions by avoiding the word ‘benefit’ or focusing on how the payments can help children. Suggested measures can be read in full in Chapter 8 of the commissioned research report (see Annex A).

Lastly, although not directly related to estimated take-up, stakeholders felt that having Universal Credit as a qualifying benefit could be a barrier to the Five Family Payments for some families. This is because the Universal Credit application form was perceived by these stakeholders to be challenging and onerous, with the result that in their experience, some clients some did not complete it, whereas others were rejected initially due to errors in their application. However, the DWP does not provide an estimated take-up rate for Universal Credit.[28] This means it is not clear how many people in Scotland are affected by this issue, including those that would also meet the other eligibility criteria for the Five Family Payments.

The profile of Five Family Payments applicants

Beyond take-up estimates, Official Statistics and Social Security Scotland client diversity and equalities analysis provide information on applications and applicants by each of the equalities groups. This provides an insight on the profile of Five Family Payments applicants.

- · Table 4 presents a secondary analysis of Official Statistics on approved applications by the age-group of applicants in the financial year 2024/25.

- · Tables 5-12 present a secondary analysis of client diversity and equalities data on applicants who applied for a benefit in the financial year 2024/25 and filled out an equalities monitoring form. [29] They present the proportion of applicants approved within the category, as a proportion of all applicants that were approved. [30] The data used in these tables represents applicant outcomes at 27 May 2024.

As mentioned in the methodology chapter, data is presented to zero decimal places. ‘0%’ should therefore be interpreted to mean less than 0.5%. If no responses were given then this is denoted by ‘-’.

| Age-group | Scottish Child Payment (%) | Best Start Grant and Best Start Foods (%) |

|---|---|---|

| Under 18 | 1% | 1% |

| 18-24 | 14% | 22% |

| 25-34 | 40% | 53% |

| 35-44 | 33% | 22% |

| 45-54 | 10% | 2% |

| 55+ | 2% | 0% |

| Gender | Scottish Child Payment (%) | Best Start Grant and Best Start Foods (%) |

|---|---|---|

| Woman | 80% | 86% |

| Man | 12% | 6% |

| In another way | 0% | 0% |

| Preferred not to say | 8% | 8% |

| Physical or mental health condition or illness | Scottish Child Payment (%) | Best Start Grant and Best Start Foods (%) |

|---|---|---|

| Yes | 20% | 19% |

| No | 67% | 68% |

| Preferred not to say | 13% | 13% |

| Ethnicity | Scottish Child Payment (%) | Best Start Grant and Best Start Foods (%) |

|---|---|---|

| White | 81% | 83% |

| Asian | 4% | 4% |

| African | 2% | 2% |

| Mixed or Multiple ethnic groups | 1% | 1% |

| Other ethnic group | 2% | 1% |

| Caribbean or black | 0% | 0% |

| Preferred not to say | 9% | 9% |

| Sexual orientation | Scottish Child Payment (%) | Best Start Grant and Best Start Foods (%) |

|---|---|---|

| Heterosexual | 85% | 86% |

| Gay & lesbian | 0% | 0% |

| Bisexual | 2% | 2% |

| In another way | 0% | 0% |

| Prefer not to say | 13% | 12% |

| Transgender | Scottish Child Payment (%) | Best Start Grant and Best Start Foods (%) |

|---|---|---|

| Yes | 0% | 0% |

| No | 91% | 91% |

| Prefer not to say | 9% | 9% |

| 6-fold Urban Rural Classification[31] | Scottish Child Payment (%) | Best Start Grant and Best Start Foods (%) |

|---|---|---|

| Large urban area | 39% | 40% |

| Other urban area | 35% | 36% |

| Accessible small town | 8% | 7% |

| Remote small town | 3% | 3% |

| Accessible rural area | 11% | 10% |

| Remote rural area | 4% | 3% |

| SIMD quintile[32] | Scottish Child Payment (%) | Best Start Grant and Best Start Foods (%) |

|---|---|---|

| 1 (most deprived) | 37% | 43% |

| 2 | 25% | 26% |

| 3 | 17% | 15% |

| 4 | 13% | 11% |

| 5 (least deprived) | 7% | 5% |

| Residence on mainland or island communities | Scottish Child Payment (%) | Best Start Grant and Best Start Foods (%) |

|---|---|---|

| Scottish Mainland | 98% | 99% |

| Scottish Island | 1% | 1% |

As outlined in the introduction to this report, the Five Family Payments are a strategic commitment in the Scottish Government’s plan to address child poverty. The tackling child poverty delivery plan identified six priority families who are especially vulnerable to poverty. Data is not routinely collected and/or published on these groups in Official Statistics. However, estimates on the proportion of Five Family Payments applicants in each priority family will be provided in the forthcoming Social Security Scotland Client Survey, to be published in November 2025.[33] The estimates will be based on an analysis of data collected from Client Survey respondents.

Making an application is clear and easy

This outcome is relevant to all of the Five Family Payments. As outlined in the Introduction chapter, there are three types of application forms for the Five Family Payments: (i) a standalone Scottish Child Payment application form, (ii) a joint Best Start Grant and Best Start Foods application form, and (iii) a joint Scottish Child Payment, Best Start Grant and Best Start Foods application form.[34]

Official Statistics provides information about how people make applications for the Five Family Payments. It shows:

- Of the 414,700 applications received for Scottish Child Payment to 31 March 2025, 91% were made online, 7% were made on the telephone, 2% were paper-based, and <0.5% were made through other channels.

- Of the 537,215 applications received for Best Start Grant and Best Start Foods to 31 March 2025, 90% were made online, 8% were made on the telephone, 2% were paper-based, and <0.5% were made through other channels.

The Client Survey provides evidence on people’s experience completing Five Family Payments application forms. It asks respondents how they found different aspects of the process. As shown in Figure 2:

- 90% strongly agreed or agreed that the application process was clear, whilst 5% strongly disagreed or disagreed

- 89% strongly agreed or agreed that the application process did not take too long, whilst 5% strongly disagreed or disagreed

- 89% strongly agreed or agreed that it was easy to provide supporting information, whilst 4% strongly disagreed or disagreed.

The only notable subgroup differences related to application outcome. Respondents who had a successful application outcome were more likely than those with an unsuccessful application outcome to strongly agree or agree:

- The application process was clear (94% compared with 79%)

- The application did not take too long (92% compared with 83%)

- It was easy to provide supporting information (91% compared to 83%).

The commissioned research also provides evidence on the experience of completing applications. It reflects the Client Survey findings in that, overall, parents and carers had a positive experience applying for the Five Family Payments. In the qualitative interviews and open-text survey responses, participants said they appreciated being able to apply online, the form was easy to complete, and the language used was easy to understand. They often compared their experience with other benefits like Universal Credit, saying they would usually seek out support to complete other forms, but did not need support when applying for the Five Family Payments.

Usually, I have to get people to help us fill out forms, especially if it's on paper because sometimes I don't understand the questions and stuff, but I never struggled. I think maybe it helps because it's on your phone. It's a lot easier to fill things out on your phone than it is to write them down on a bit of paper. I never had any problem. I found the process for all of the applications really easy.

(Parent and carer interview)

The participants that did receive support from Social Security Scotland when applying had a positive experience of doing so, describing staff as helpful and friendly. They also spoke positively about being able to make joint claims for the benefits on a single application form, and said it was easy to add a new child to their Scottish Child Payment account, because it did not involve completing a new application form for them. However, despite the generally positive feedback, some participants said the application form was too long, experienced some challenges completing the form. Some also reported challenges communicating with Social Security Scotland, such as not having enough time to phone and wait to speak to staff and issues reaching staff through the live chat.

Applications and payments are processed in a timely manner

Application processing times

Application processing times are relevant to all of the Five Family Payments benefits. Official Statistics provides information on application processing times, which are calculated from the point of initial benefit application until a decision on the application is made, and includes time spent waiting to receive copies of documents or evidence requested from applicants. On that basis, a yearly breakdown of application processing times is shown in Tables 13 and 14. [35] [36]

The data in Tables 13 and 14 show that both Scottish Child Payment application processing times, and that Best Start Grant and Best Start Foods application processing times, have improved in recent years. For example, in 2024/25:

- Scottish Child Payment applications were processed in 11 working days on average, which was quicker than in all previous years

- Best Start Grant and Best Start Foods applications were processed in 10 working days on average, which was quicker than in all previous years except 2018/19 and 2019/20.

| Financial year | Number of processed applications (excluding redeterminations) | Percentage of applications processed within 10 working days | Percentage of applications processed in 41 or more working days | Average (median) processing time in working days |

|---|---|---|---|---|

| 2020-2021 | 80,795 | 6% | 42% | 37 |

| 2021-2022 | 65,505 | 22% | 21% | 25 |

| 2022-2023 | 153,530 | 17% | 31% | 29 |

| 2023-2024 | 61,520 | 44% | 19% | 13 |

| 2024-2025 | 42,745 | 49% | 7% | 11 |

| Financial year | Number of processed applications (excluding redeterminations) | Percentage of applications processed within 10 working days | Percentage of applications processed in 41 or more working days | Average (median) processing time in working days |

|---|---|---|---|---|

| 2018-2019 | 17,930 | 55% | 3% | 9 |

| 2019-2020 | 120,665 | 56% | 3% | 9 |

| 2020-2021 | 111,700 | 23% | 15% | 19 |

| 2021-2022 | 82,460 | 29% | 19% | 20 |

| 2022-2023 | 88,335 | 6% | 43% | 39 |

| 2023-2024 | 61,705 | 46% | 16% | 12 |

| 2024-2025 | 47,025 | 52% | 6% | 10 |

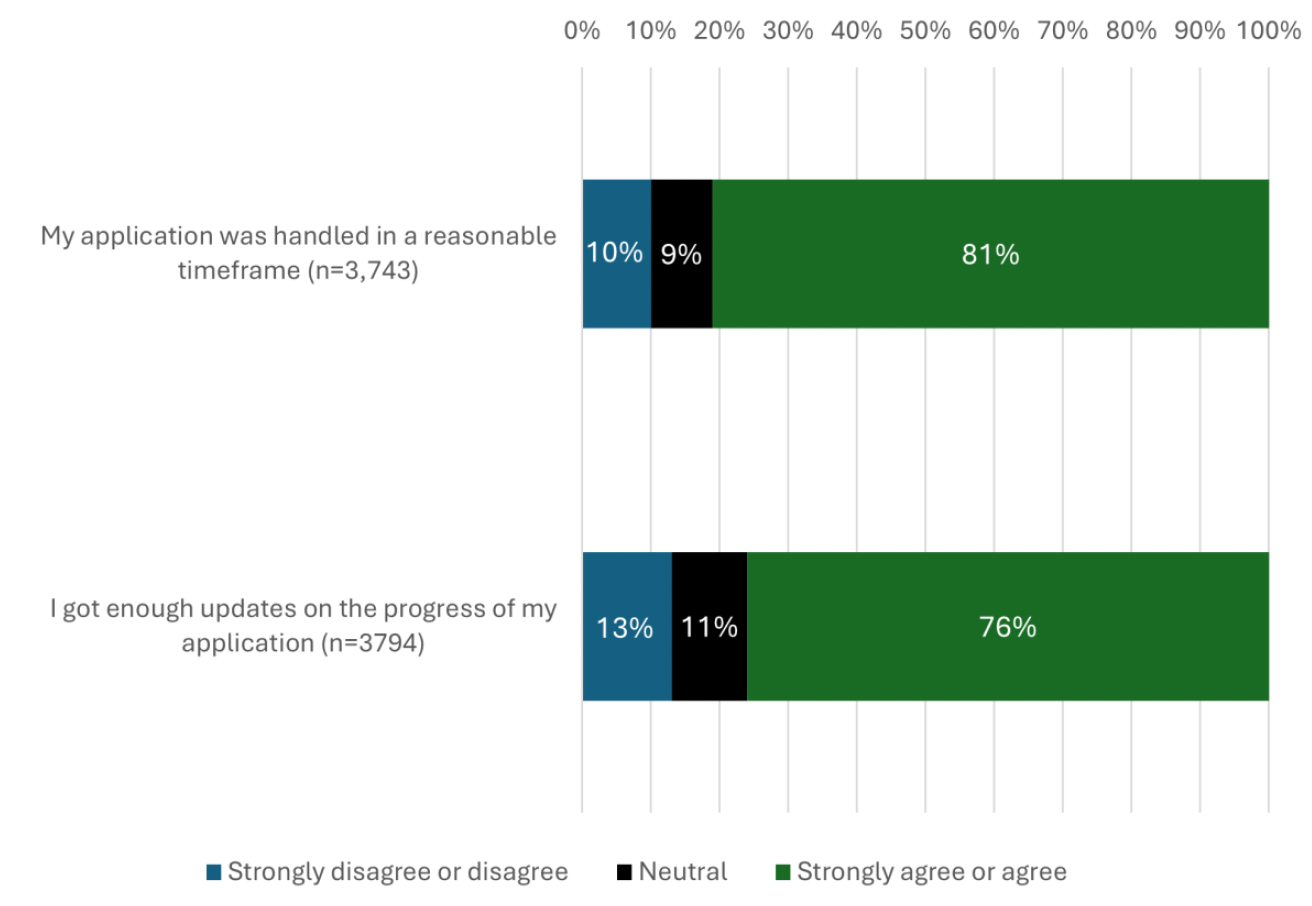

The Client Survey asks applicants about their experiences after submitting an application form. Specifically, if they felt (a) their application was handled within a reasonable time frame, and (b) they got enough updates on the progress of their application. The findings in Figure 3 show that:

- 81% strongly agreed or agreed that their application was handled in a reasonable timeframe, whilst 10% strongly disagreed or disagreed

- 76% strongly agreed or agreed they got enough updates on the progress of their application, whilst 13% strongly disagreed or disagreed

There were notable subgroup differences relating to priority families at risk of poverty. Specifically:

- Families from minority ethnic backgrounds were more likely than families from white ethnic backgrounds to agree their application was handled in a reasonable timeframe (86% compared to 80%) and they got enough updates on their application (83% compared to 74%).

- Households without a disabled family member were more likely than those with a disabled family member to agree they got enough updates on their application (79% compared to 73%)

- Families without a mother aged under 25 were more likely than families with a mother aged under 25 to agree they got enough updates on their application (77% compared to 71%)

Regarding other subgroup differences, respondents who had a successful application outcome were more likely than those with an unsuccessful application outcome to agree their application was handled in a reasonable timeframe (86% compared to 72%), and they got enough updates on the progress of their application (83% compared to 63%).

The commissioned research also provided evidence about people’s experiences after submitting a Five Family Payments application form. While qualitative interview participants were generally positive about their experience of the application process, some said they experienced a long wait for an application decision. This reflects the Official Statistics presented in Tables 13 and 14, showing a small proportion of applications were processed in 41 days or more. It also reflects the Client Survey findings in Figure 3 that 10% of respondents strongly disagreed or disagreed their application was handled in a reasonable timeframe.

Payment processing

The processing of payments is also relevant to all of the Five Family Payments. Official Statistics provides a range of information on payments made to Five Family Payments recipients. For Scottish Child Payment, 209,200 individual clients were paid in the financial year 2024/25. Also, as of 31 March 2025, the number of children benefitting from Scottish Child Payment was 326,225. For Best Start Grant and Best Start Foods, 69,285 individual clients were paid in the financial year 2024/25. Official Statistics also show the following about payments since the benefits were introduced:

- 7,456,725 payments were administered to Scottish Child Payment recipients between February 2021 and March 2025, with a total payment value of £1,133,678,377.

- 104,120 Best Start Grant Pregnancy and Baby Payments were administered between December 2018 and March 2025, with a total payment value of £46,483,056

- 135,900 Best Start Grant Early Learning Payments were administered between May 2019 and March 2025, with a total payment value of £37,362,030

- 123,760 Best Start Grant School Age Payments were administered between July 2019 and March 2025, with a total payment value of £34,282,276

- 2,210,895 Best Start Foods payments were administered between September 2019 and March 2025, with a total payment value of £69,303,084.

As mentioned in the Introduction chapter, auto-awarded payments for Best Start Grant Early Learning Payment and School Age Payment were introduced in November 2022 for parents and carers who already receive Scottish Child Payment. Official Statistics show that up to 31 March 2025, a total of 43,305 auto-awards have been made for Early Learning Payment, and 43,705 for School Age Payment, with payment values of £12,977,794 and £13,358,821, respectively.

The Client Survey asks respondents about their experience of receiving payments. Amongst Five Family Payments recipients:

- 90% received their payment when Social Security Scotland said they would, whilst 2% did not, and 8% could not remember/did not know (n=3,293)

- 90% received the right amount first time, whilst 3% did not, and 7% could not remember/did not know (n=3,299)

- 92% received the right amount every time, whilst 3% did not, and 6% could not remember/did not know (n=3,236).

Social Security Scotland conducted a survey of Five Family Payments recipients (n=569) who had received auto-awarded payments of Best Start Grant Early Learning Payment and School Age Payment.[37] It found:

- 95% said their overall experience of receiving an auto-awarded payment was good or very good, whilst only 1% said their experience was poor or very poor

- Over half of respondents had previously applied for a payment they were auto-awarded (e.g. for another child), and 95% of these respondents agreed they preferred receiving the payment automatically.

In written responses, whilst some respondents said it would have been more useful receiving the payment at a different time, most said the payment came at a useful time. Additionally, respondents often commented they preferred the automatic payments because they were easier, saved time, were less hassle and prevented worry about applying at the right time.

I love the system. I didn't know about the payment. It was a very pleasant and welcome surprise and even better that I didn't need to fill out more forms. Getting a text was great as piles of letters in the post isn't just bad for the environment, they give me anxiety. Can't fault it.

(Auto-award survey respondent)

Stakeholders who took part in the commissioned research spoke about the auto-awarded Best Start Grant payments in qualitative interviews. They felt that these were a positive development, helping to simplify the claims process and ensuring more families were receiving their entitlements.

Awareness is raised about other forms of support

Clients who interact with Social Security Scotland when making a benefits application can be informed about other forms of support. This outcome is relevant to all of the Five Family Payments.

The Client Survey asks respondents who have been in touch with a member of Social Security Scotland staff if they were told about (a) other benefits they might be entitled to, and (b) other sources of additional help (e.g. Citizens Advice). The findings for Five Family Payments applicants are presented in Table 15. They show:

- 37% said they were told about other benefits, whilst 38% who were not told about other benefits (but would have liked to have been told) [38]

- 31% said they were told about other sources of additional help, compared to 29% who were not told about other forms of additional help (but would have liked to have been told).

| Survey question | Number of respondents | Yes | No, but I would have liked them to | Not applicable/relevant |

|---|---|---|---|---|

| Did staff tell you about other benefits you might be entitled to? | 1,775 | 37% | 38% | 26% |

| Did staff tell you about other sources of additional help | 1,534 | 31% | 34% | 35% |

There were notable subgroup differences relating to priority families at risk of poverty:

- Families with a mother aged under 25 were more likely than families with no mother aged under 25 to say they were told about other benefits they might be entitled to (53% compared to 36%) and other sources of additional help (53% compared to 30%).

- Families with a child aged under 1 were more likely than families with no child aged under 1 to say they were told about other benefits they might be entitled to (47% compared to 32%)

- Families from minority ethnic backgrounds were more likely than families from white ethnic backgrounds to say they were told about other benefits they might be entitled to (43% compared to 34%)

Respondents with a successful application outcome were also more likely than those with an unsuccessful outcome to say they were told about other benefits they might be entitled to (39% compared to 29%) and other sources of additional help (34% compared to 23%).

Clients are treated with dignity, fairness and respect

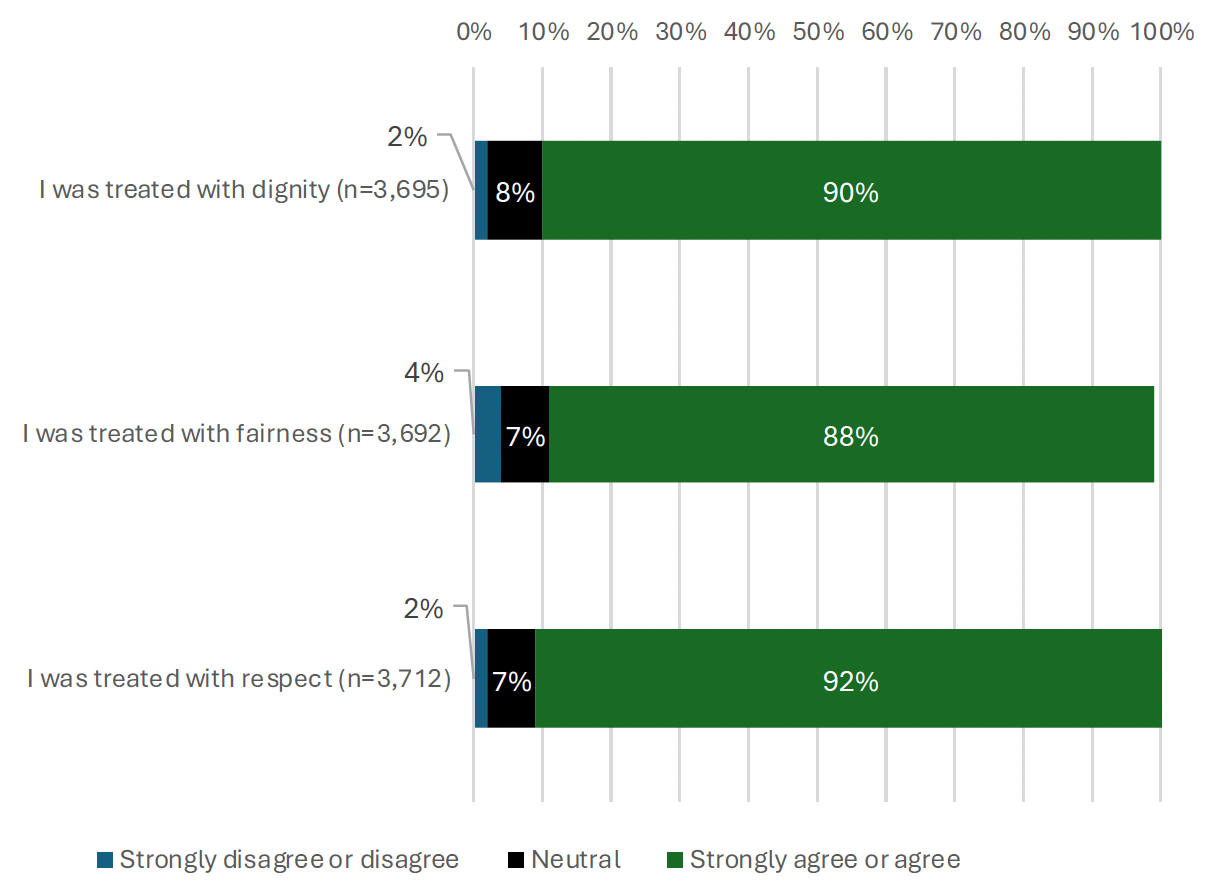

Social Security Scotland aims to treat all clients with dignity, fairness and respect.[39] This outcome is therefore relevant to all of the Five Family Payments. The Client Survey asks respondents about their experiences with Social Security Scotland, including how they felt they had been treated by the organisation. As shown in Figure 4, amongst those who applied for at least one of the Five Family Payments:

- 90% strongly agreed or agreed they were treated with dignity, whilst 2% strongly disagreed or disagreed

- 88% strongly agreed or agreed they were treated with fairness, whilst 4% strongly disagreed or disagreed

- 90% strongly agreed or agreed they were treated with respect, whilst 2% strongly disagreed or disagreed.

The only notable subgroup differences related to application outcome. Respondents with a successful application outcome were more likely than those with an unsuccessful application outcome to agree that they were treated with dignity (94% compared with 80%), fairness (94% compared with 73%), and respect (96% compared to 82%) by Social Security Scotland.

The commissioned research evidence from qualitative interviews and open-text survey responses reflects the Client Survey findings presented above. Those who got support with their applications from Social Security Scotland were largely positive about these interactions. They described being given helpful advice and guidance, and being treated well by staff.

It has been a great experience and the staff I’ve spoken to on the phone when setting up were all fantastic, especially when it came to adding my new baby to the claim. It has definitely helped us to be less stressed about money.

(Survey respondent)

It was very easy to apply for my application was dealt with easily and quickly. I have been treated with respect and kindness from staff.

(Survey respondent)

Card is easy to use and reduces stigma

This outcome relates specifically to Best Start Foods. As mentioned in the Introduction chapter, Best Start Foods payments are made every four weeks via payment card, which can be used like a normal bank card with contactless or Chip & Pin features. The Client Survey asks respondents about their experiences using the Best Start Foods card. The findings show that:

- 92% strongly agreed or agreed it was clear how to use the card, whilst 5% neither agreed nor disagreed, and 3% strongly disagreed or disagreed (n=702)

- 88% strongly agreed or agreed they were able to use the card without any difficulties, whilst 7% neither agreed nor disagreed, and 6% strongly disagreed or disagreed (n=682).

The only notable subgroup difference related to the priority families at risk of poverty. Specifically, families from minority ethnic backgrounds were more likely than families from white ethnic backgrounds to say they could use the Best Start Foods card without any difficulties (92% compared to 86%).

In the commissioned research, survey respondents were asked why they did not spend the money on their Best Start Foods card, and they could select more than one option. As shown in Table 16, most respondents (64%) said this was not applicable to them, as they always spent most or all of the money on their card. Others selected options which are not indicative of issues with the card itself - i.e. sometimes forgetting the card (12%), having no reason for not spending the money (7%), saving the money on the card (6%), and not needing help to buy healthy foods (1%)

However, some respondents selected options that are indicative of issues with the card. These included that it did not always work (8%), it was hard to use (3%), and that it was not accepted where they shop (1%). Additionally, those who selected ‘another reason’ (6%) could explain their response, and the most frequent comment related to difficulties splitting payments between foods they were buying with the card and other shopping. Lastly, 7% of respondents said they did not spend all of the money on the card because they felt embarrassed using it, indicating that some Best Start Foods recipients feel there is a stigma associated with the card.

Table 16 Reasons why Best Start Foods recipients did not spend all of the money on the card, where applicable

Response option

Not applicable – I always spend all or most of the money on my card

Proportion of respondents

64%

Response option

I sometimes forget my card

Proportion of respondents

12%

Response option

My card does not always work

Proportion of respondents

8%

Response option

No reason – I just don’t spend it all

Proportion of respondents

7%

Response option

I feel embarrassed using the card

Proportion of respondents

7%

Response option

I am saving the money on my card

Proportion of respondents

6%

Response option

I find the card hard to use

Proportion of respondents

3%

Response option

The card is not accepted where I shop

Proportion of respondents

1%

Response option

I do not need help to buy healthy foods

Proportion of respondents

1%

Response option

Another reason

Proportion of respondents

6%

Total number of respondents

522

Also in the commissioned research, the qualitative interviews and open-text survey responses provided more detail on experiences with the Best Start Foods card. There were parents and carers who did not have issues with the card, and some who said having a separate card for food shopping helped with budgeting. However, some participants reported the following difficulties:

- Receiving payments irregularly

- Cards expiring or being blocked, and delays receiving the card

- Card errors like not being able to use cards in certain shops and online, contactless payments not working, or the card not working in general

- Certain supermarkets or shops in the local area not accepting the card

- A lack of clarity where the card can be used and how it can be spent.

Specifically regarding stigma, the initial evaluation of Best Start Foods found that, generally, the card reduced stigma when compared with the DWP Healthy Start Vouchers system it replaced in Scotland. However, as shown by the survey findings above, 7% of recipients said they felt embarrassed using the card. In qualitative interviews and open-text survey responses, parents and carers reported embarrassment when having the card declined or rejected, and at having to separate shopping items in order to use the card. There were therefore suggestions to receive the payment into their own bank account.

I do sometimes think that me and other people, I think they find it embarrassing with the card, because everyone knows what that card is, because they all look the same. […] I think it's an internal thing where you think, 'Oh, I should be able to get this without needing help.' But then I suppose if it was put in people's banks, they might not spend it on the right thing, so there is ups and downs to it.

(Parent and carer interview)

Other issues raised by survey and interview respondents included damaging or losing their card, forgetting their pin, difficulties with checking their balance and views that what you can buy with the card were too restricted.

Card provides access to a range of retailers

This outcome also relates specifically to Best Start Foods. As mentioned in the Introduction chapter, the payment card works in all supermarkets or local shops that sell food and accept bank card payments, and can also be used online.

The Client Survey asks respondents if it was clear where the Best Start Foods payment card could be used. The findings show 88% strongly agreed or agreed it was clear where they could use the card, whilst 6% neither agreed nor disagreed, and 6% strongly disagreed or disagreed (n=693). With regards to the priority families at risk of poverty, the following subgroups were notably more likely to say it was clear where to use the Best Start Foods card:

- Families from minority ethnic backgrounds (95%) compared to families from white ethnic backgrounds (85%)

- Households without a disabled family member (91%) compared to households with a disabled family member (82%).

In the commissioned research, participants in qualitative interviews described using their Best Start Foods card in a variety of supermarkets and local shops. This reflects findings from the initial evaluation of Best Start Foods, which also found the card was being used in a wide range of shops, including large and small supermarket chains, smaller franchises and local independent shops. However, as shown in Table 16 above, a small proportion of survey respondents (1%) said the card was not accepted where they shop. This issue was also highlighted by recipients in qualitative interviews and open-text survey responses.

Card provides access to a range of healthy foods

This outcome also relates specifically to Best Start Foods. While actual spend is not monitored, the following items are prescribed to purchase via Best Start Foods:

- Fresh eggs

- Milk – plain cow’s milk and first infant formula

- Fruit/vegetables – fresh, frozen or tinned (those with added salt and sugar are excluded)

- Pulses (e.g. peas, lentils and beans) – dried, fresh, frozen or tinned.

In the commissioned research, participants in qualitative interviews said they used their Best Start Foods payment card to buy a range of foods and essential non-food items for their children. Participants also mentioned using Best Start Foods to pay for healthy foods in bulk, and generally to buy more fruit and vegetables than they did previously. However, some felt that the prescribed range of healthy food items is too restrictive. This reflects findings in the initial Best Start Foods evaluation. It found that, while some recipients felt the range of prescribed foods was appropriate and reasonable, others felt that expanding the range would be beneficial – for example, to include other sources of protein such as meat and poultry.

Recap of achievement against immediate outcomes

The evidence presented throughout this section shows that:

- People find out about the Five Family Payments in a range of ways, particularly word of mouth, online and social media, and via health professionals

- Take-up of the Five Family Payments benefits is generally high, and is especially high for families with children aged under 6 receiving Scottish Child Payment and Best Start Grant School Age Payment

- Five Family Payments application forms are generally considered to be easy and quick to complete

- Five Family Payments application processing times have improved in recent years, and most recipients are satisfied with the experience of receiving payments

- Five Family Payments applicants feel they were treated with dignity, fairness and respect by Social Security Scotland

- The Best Start Foods payment card is generally found to be easy to use, and provides access to a range of retailers and healthy foods.

The evidence also highlights some issues relating to immediate outcomes, notably that around 1 in 3 Five Family Payments applications were denied in 2024/25, which indicates there is some confusion over eligibility criteria amongst applicants. A minority of people also face issues such as take-up barriers, not being told about additional benefits or forms of support by Social Security Scotland, and problems with the Best Start Foods payment card.

However, overall, the findings demonstrate that immediate Five Family Payments outcomes are being achieved. According to the Five Family Payments theory of change, this makes it possible for short-term policy outcomes to be achieved. Actual achievement against short-term policy outcomes is explored in the section below.

Achievement against short term Five Family Payment policy outcomes

This section evaluates the Five Family Payments against the following policy outcomes, which are relevant to one or more of the benefits:

- Increased child-related spend (All benefits)

- Reduced pressure on household finances (All benefits)

- Reduced money-related stress (All benefits)

- Children able to participate in social and educational opportunities (Scottish Child Payment and Best Start Grant)

- Improved position of main carers within households (Scottish Child Payment)

- Grant reaches people at key transition points in child’s life (Best Start Grant)

- Families financially supported at key transition points (Best Start Grant)

- Healthy foods are more affordable (Best Start Foods)

- Mothers and children eat more healthy foods (Best Start Foods)

- Supports healthier shopping habits and meal planning (Best Start Foods)

It uses data from the bespoke commissioned research. As outlined in the methodology chapter in this report, the commissioned research involved (i) a survey of Five Family Payment recipients and (ii) qualitative interviews with Five Family Payments recipients and stakeholders who support low income families. The section ends with a recap of achievement against short-term Five Family Payments policy outcomes.

It should also be noted that, throughout this section, notable differences in how commissioned survey respondents answered questions in the survey have been presented. As explained in the Methodology chapter, subgroup differences are reported in cases where the difference between the subgroups is statistically significant. The subgroup differences are discussed in more detail in the ‘discussion of progress towards Five Family Payments outcomes’ section.

Increased child-related spend

It is intended that the Five Family Payments increase child-related spend. This outcome is therefore relevant to all of the Five Family Payments benefits. The commissioned research addressed this topic in the survey and qualitative interviews. The findings are presented below for each of the individual benefits.

Scottish Child Payment and child-related spend

The commissioned research asked Scottish Child Payment recipients questions about child-related spend. In the survey, recipients were asked what they spent their payments on. They were presented with a range of options, and could select more than one option. With regards to child-related spend, the findings show:

- 78% used Scottish Child Payment to buy things for their child (such as toys, clothes, or bedding)

- 53% used Scottish Child Payment to pay for activities for the child or the whole family (such as day trips, or visits to family or friends)

- 18% used Scottish Child Payment to buy things for their pregnancy or baby (such as breast pads, nappies, or formula milk)

- 9% used Scottish Child Payment as savings for their child or the family.

Respondents also said they used Scottish Child Payment for day-to-day household costs and essentials such as food and bills (66%), and larger household costs such as furniture and car expenses (5%).

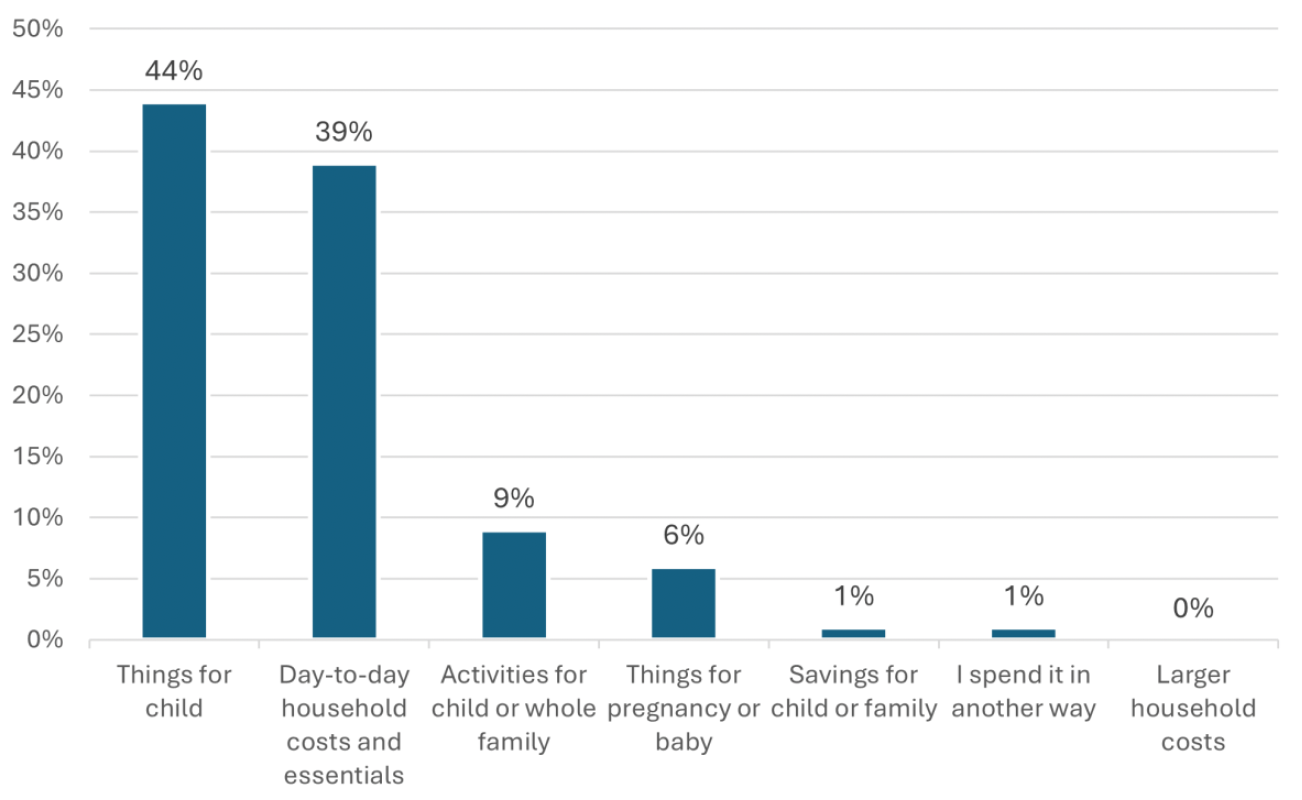

The survey also asked respondents what they spent Scottish Child Payment on the most, and they could choose only one option. As shown in Figure 5, 44% said they spent Scottish Child Payment mostly on things for their child, which was the most common response. A smaller proportion of respondents selected activities for their child or whole family (9%) or things for pregnancy or baby (6%). The second most common response was using Scottish Child Payment for day-to-day household costs and essentials (39%).

With regards to mostly spending Scottish Child Payment on things for their child (such as toys, clothes, or bedding), the only statistically significant difference related to the priority families most at risk of poverty. Specifically, households without a disabled family member were more likely than those with a disabled family member to say they mostly spent the money on things for their child (46% compared with 42%).

The qualitative interviews and open-text survey responses largely reflect the survey findings presented above. There were parents and carers who said, where possible, they used Scottish Child Payment specifically to buy things for their child. In some of these cases, participants said that they treated income from wages or other benefits as being for household costs, whilst Scottish Child Payment was for child-related spend. However, other participants said they pooled their income and spent it on whatever their child or family needed at the time.

…I like opened a children’s account for both of my kids because like to try and be organised with funds and make sure that I’m allocating it towards them now when those specific funds come through.

(Parent and carer interview)

I very much concentrated on the money needs to go towards what we need, which is food for the house, nappies for the baby, her toiletries, things like that. It was very much decided through what is essential to spend this money on.

(Parent and carer interview)

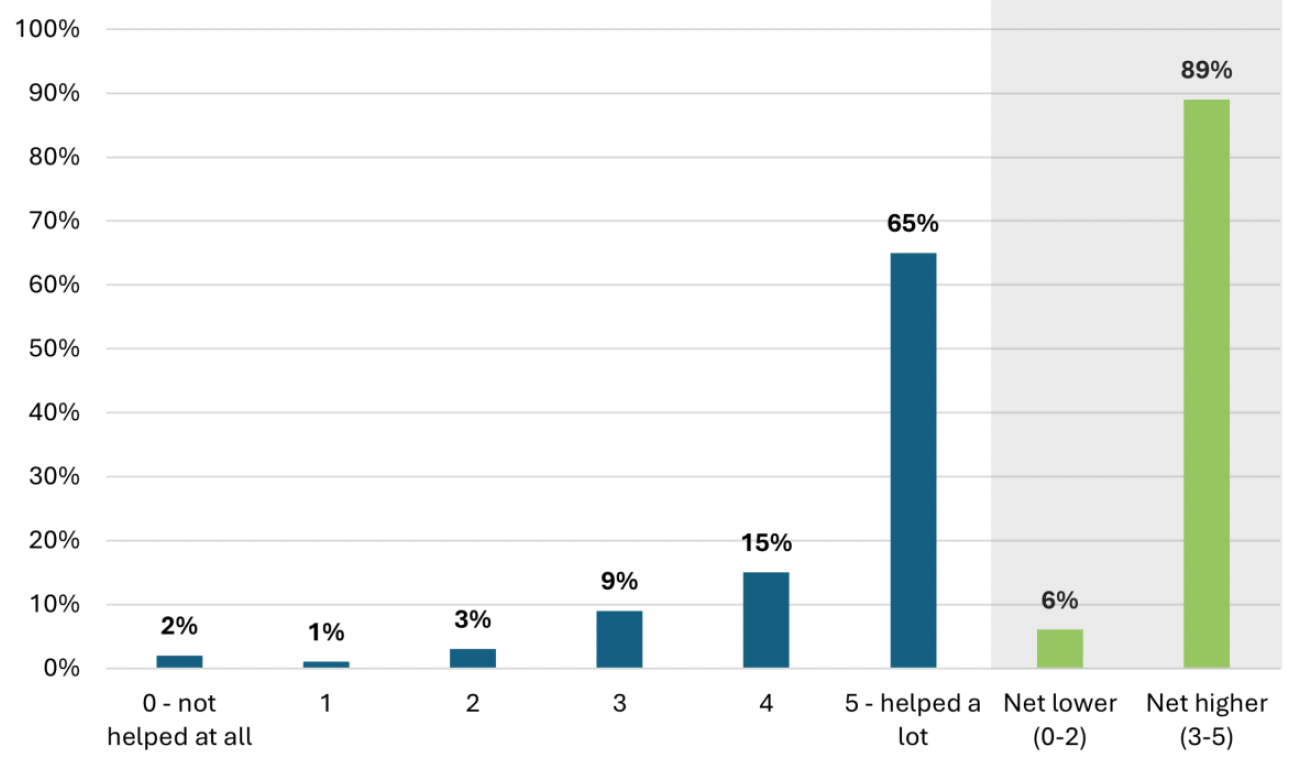

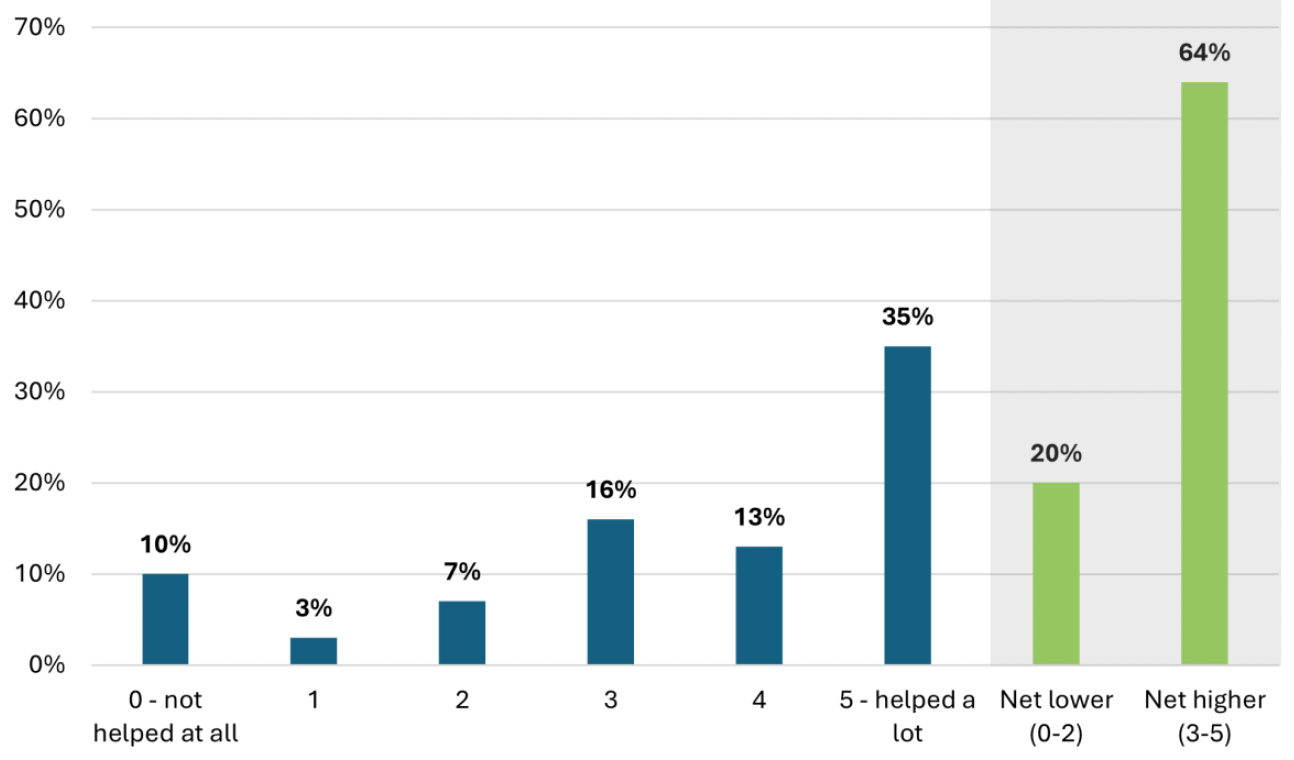

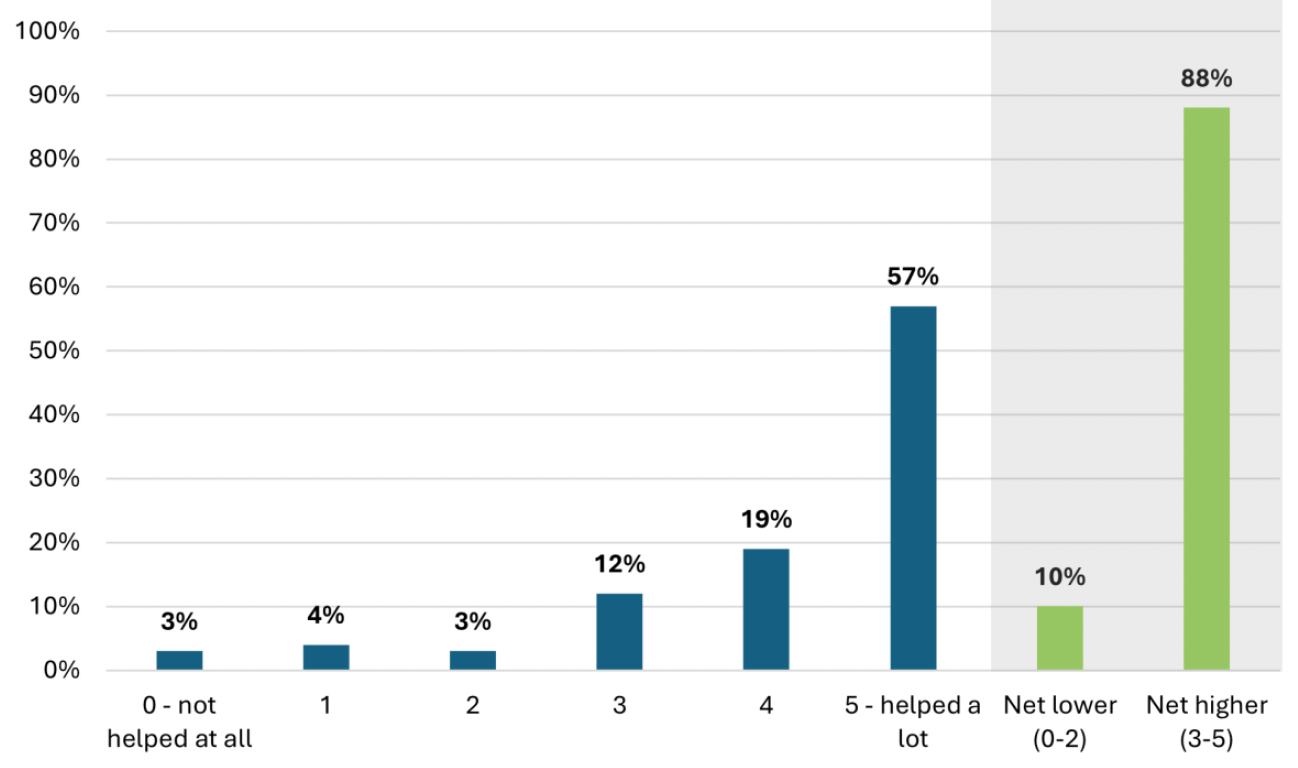

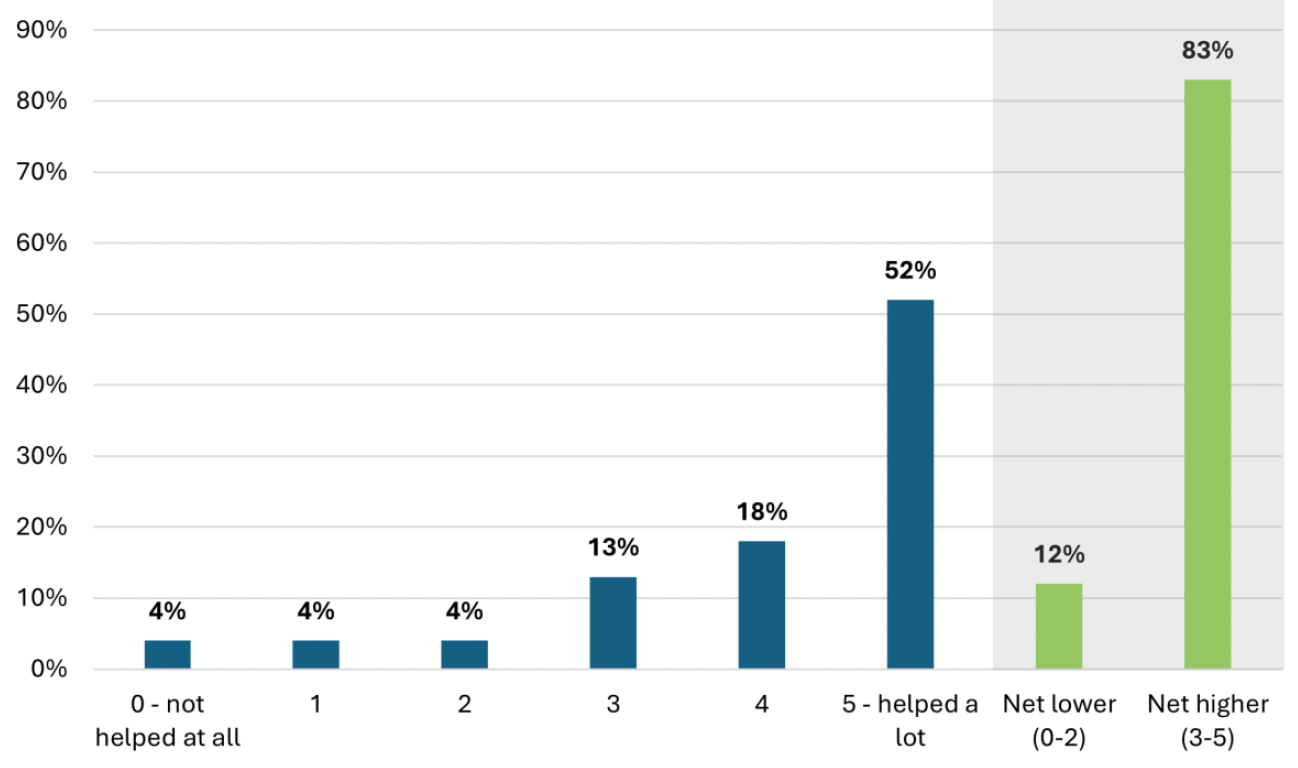

In the survey, Scottish Child Payment recipients were also asked, on a scale of zero (‘not at all’) to five (‘a lot’), how much the payments helped them with different types of child-related spend. As shown in Table 17:

- 75% rated Scottish Child Payment five (helped a lot) for helping to buy their child essential items such as clothes, food, and medicine. Overall, 94% gave a higher rating of three to five, and 4% gave a lower rating of zero to two.

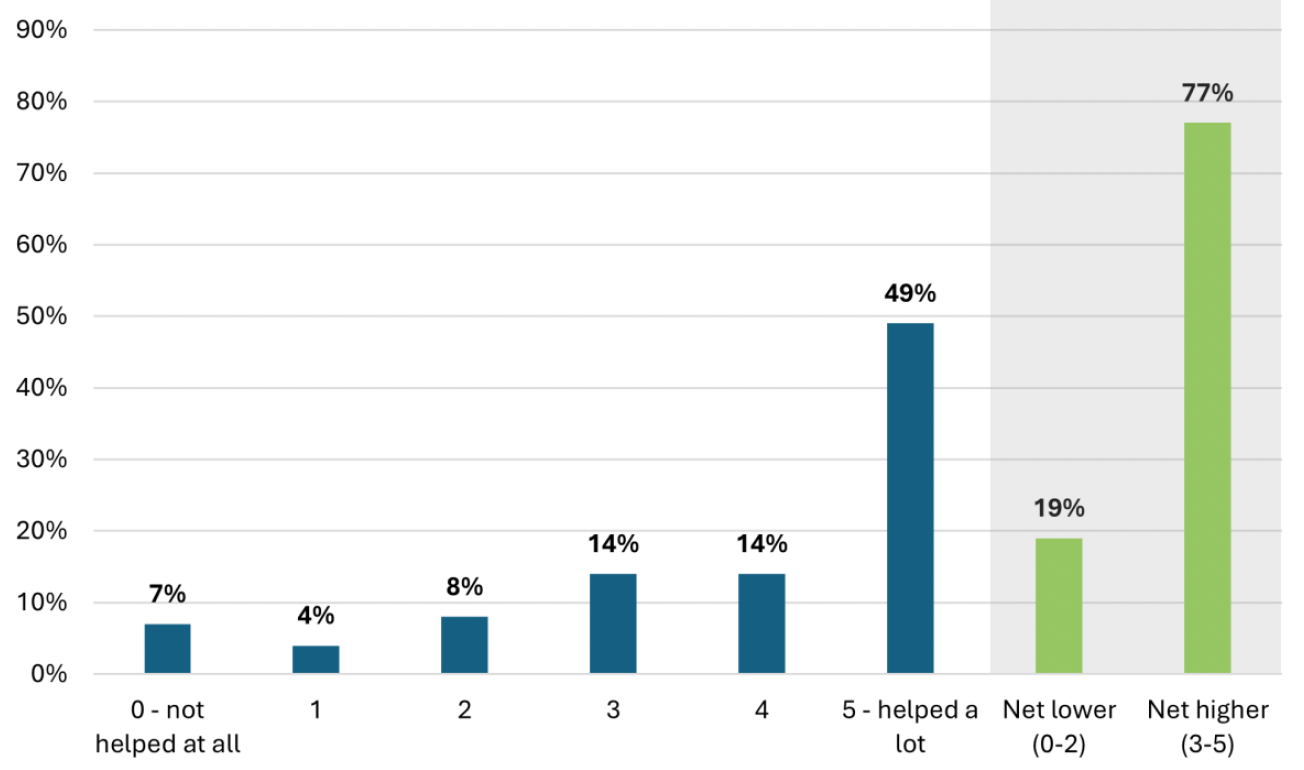

- 57% rated Scottish Child Payment five (helped a lot) for helping to buy their child school items such as pencils, a bag, and a uniform. Overall, 84% gave a higher rating of three to five, and 9% gave a lower rating of zero to two.

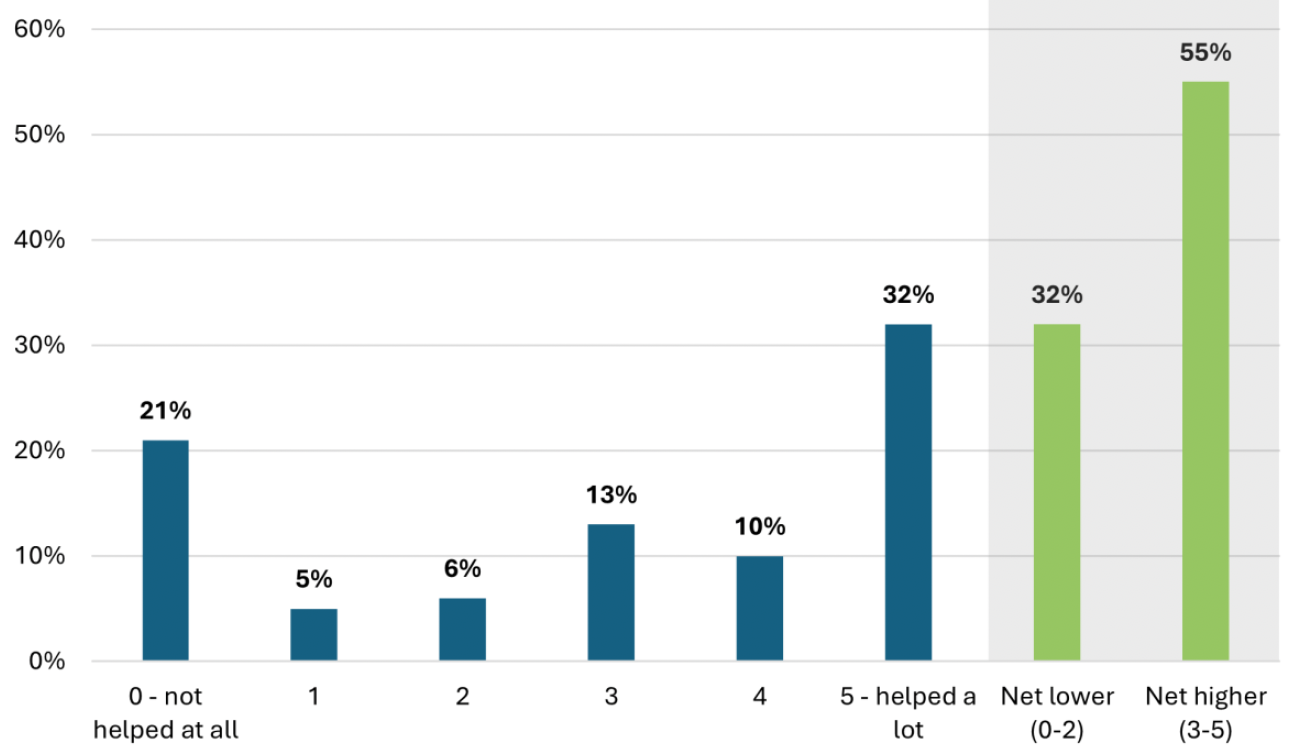

- 50% rated Scottish Child Payment five (helped a lot) for helping to buy their child treat items such as toys, ice cream, and magazines. Overall, 79% gave a higher rating of three to five, and 17% gave a lower rating of zero to two.

| Survey measure | Total respondents | 0 – not helped at all | 1 | 2 | 3 | 4 | 5 – helped a lot | Net lower (0-2) | Net higher (3-5) |

|---|---|---|---|---|---|---|---|---|---|

| Helped buy my child essential items | 3,404 | 1% | 1% | 2% | 8% | 11% | 75% | 4% | 94% |

| Helped buy my child things they needed for school | 3,402 | 3% | 2% | 4% | 13% | 14% | 57% | 9% | 84% |

| Helped buy my child treat items | 3,402 | 4% | 4% | 9% | 17% | 12% | 50% | 17% | 79% |

There were statistically significant differences relating to the priority families most at risk of poverty. Specifically:

- Families with three or more children were more likely than families with one or two children to say it helped ‘a lot’ buying their child essential items (79% compared with 74%) and school items (63% compared with 56%)

- Families from white ethnic backgrounds were more likely than those from minority ethnic backgrounds to say it helped ‘a lot’ with buying their child essential items (76% compared with 68%) and school items (58% compared with 51%)

- Households with a disabled family member were more likely than those without disabled family member to say it helped ‘a lot’ with buying their child essential items (77% compared with 72%).

Regarding other subgroups with statistically significant differences:

- Families who had been receiving Scottish Child Payment for over 12 months were more likely than those who had been receiving it for up to 12 months to say it helped ‘a lot’ with buying their child school items (60% compared with 53%) and treat items (53% compared with 44%)

- Families from the 20% most deprived areas were more likely than those from the 20% least deprived areas to say it helped ‘a lot’ with buying their child treat items (54% compared with 45%).

In the qualitative interviews and open-text survey responses, parents and carers indicated that food and clothing were key areas of essential child-related spend. For some, these were the main, or only, items they spent Scottish Child Payment on. This reflects the survey findings above, which show that the majority of respondents gave Scottish Child Payment a high rating for helping to buy their child essential items such as clothes, food and medicine. With regards to clothing, some participants said they had to frequently replace clothes because their child was growing so fast.

…my grandson of 11 he got his school shoes in August and he got his feet measured and everything and they’re too tight for him now. So after school today I’ve got to go down the town and get him new shoes because he was complaining that they were tight this morning. […] And the oldest one who’s 15 he’s a size 10½ in a shoe so he’s men’s prices for his shoes and things like that.

(Parent and carer interview)

Essential spend also varied by the circumstances of the child and family. For example, parents of newborns reported using payments for essentials like formula milk and nappies. Others said Scottish Child Payment helped them meet the needs of their disabled child, which could be expensive. This also reflects the survey findings above, which show that households with a disabled family member were particularly likely to give Scottish Child Payment a high rating for helping them to buy their child essential items.

My son had a lot of hospital visits as he grew until recently and it helped us get to them and buy him specific foods that fit his dietary needs.

(Survey respondent)

It was also common for respondents to say they used Scottish Child Payment for school clothes, including clothing for school clubs, which also had to be replaced regularly due to the child growing quickly, or because they got mucky or torn at school. Other school-related costs included lunches, bags, supplies, fees, trips and events.

[Scottish Child Payment] Helps me to provide essential items my child needs for day to day, uniform, clothing, school trips to prevent exclusion from friends, would be a huge struggle to manage without it.

(Survey respondent)

Some parents and carers shared that Scottish Child Payment helped them to buy treats for their children. Examples they gave included toys, money to go out with friends, and birthday and Christmas presents. Some also said that Scottish Child Payment enabled them to pay for treats despite the cost of living increases.

Very grateful for the additional money. With the recent impact of inflation, that has increased the cost of daily living and taking more of our family income, this extra money helps the kids still get the extras that they need and softens the impact of the price increases.

(Survey respondent)

However, some participants said they used Scottish Child Payment for basic needs and were unable to use it for treats at all, or could do so very rarely. This also reflects the survey findings, which show that fewer respondents rated Scottish Child Payment five (helped a lot) for buying their child treat items (50%) compared with buying their child essential items (75%).

Best Start Foods and child-related spend

The commissioned research asked Best Start Foods recipients about child-related spend. The findings demonstrate that Best Start Foods has led to increased child-related spend on healthy food items. However, as most of these findings are partially related to child-related spend, they are covered later in the Findings chapter, specifically in relation to the outcomes ‘Healthy foods are more affordable’, ‘Mothers and children eat more healthy foods’, and ‘Supports healthier shopping habits and meal planning’.

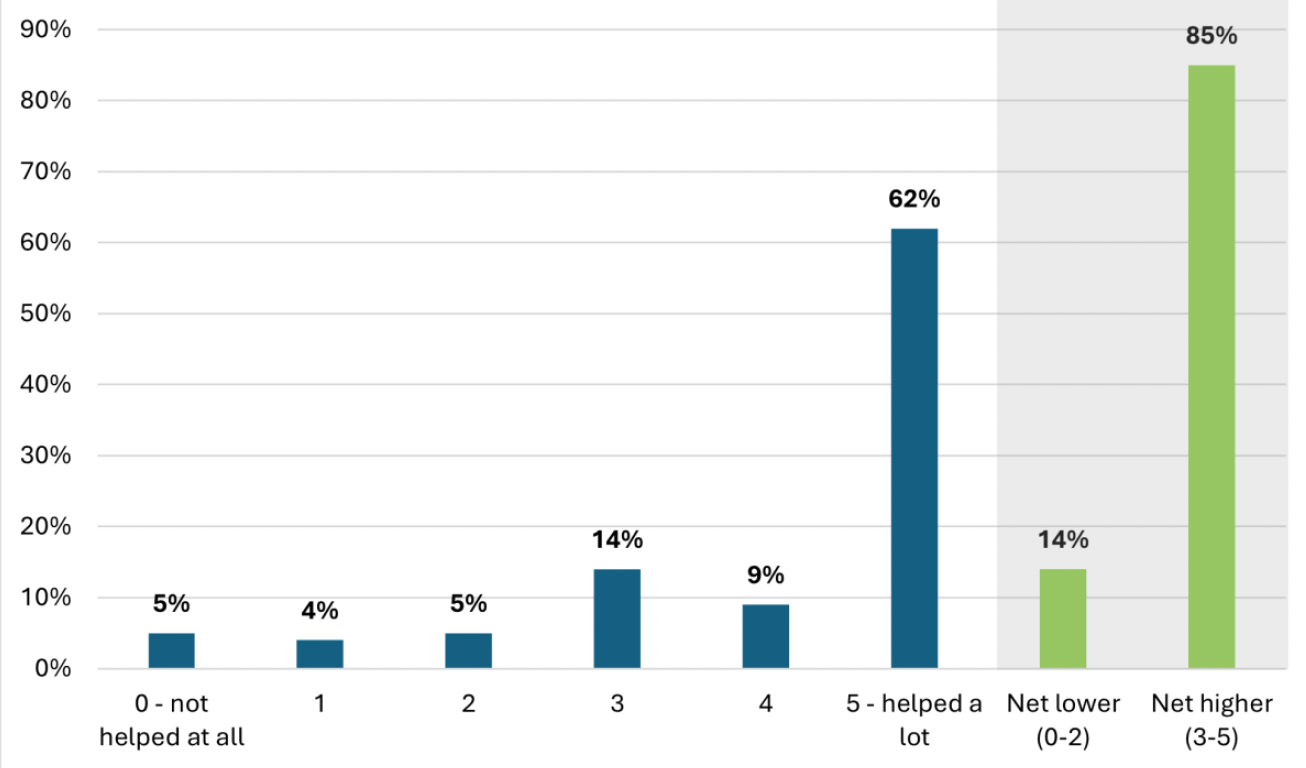

However, the survey did ask about child-related spend directly regarding first infant formula milk. Best Start Foods recipients were asked if they used the payments to buy first infant formula milk for any children aged under one in their household. Those who did were asked on a scale of zero (‘not at all’) to five (‘a lot’) how much the payments helped them to buy first infant formula milk. The findings in Figure 6 show that 62% rated Best Start Foods five (helped a lot) for helping to buy first infant formula milk. Overall, 85% gave a higher rating of three to five, and 14% gave a lower rating of zero to two. There were no statistically significant differences between subgroups of respondents.

In the qualitative interviews and open-text survey responses, participants emphasized how much Best Start Foods helped them pay for first infant formula milk, which was described as being expensive. Some also felt they would have to borrow money or skip bills to afford formula if they did not have Best Start Foods.

It’s [Best Start Foods] taken the pressure off of paying certain bills because again I would skip a bill to buy her formula. […] it is handy for essentials and it probably makes a bigger impact to people who are more disadvantaged than me you know. It does help.

(Parent and carer interview)

[If didn’t receive Best Start Foods] I would have borrowed off my parents. My dad can’t really afford it but he would give me the money for formula for her because she needs it and again he would sacrifice a meal so she could eat because he did that when I was a kid.

(Parent and carer interview)

Best Start Grant and child-related spend

The commissioned research asked Best Start Grant recipients about child-related spend. In the survey, those who had received at least one Best Start Grant payment were asked what they had spent the payments on. They were presented with a range of options, and could select more than one option. With regards to child-related spend, the findings show that:

- 71% used Best Start Grant to buy things for their child (such as toys, clothes, or bedding)

- 59% used Best Start Grant to buy things for their pregnancy or baby (such as breast pads, nappies, or formula milk)

- 23% used Scottish Child Payment to pay for activities for child or the whole family (such as day trips, or visits to family or friends)

- 4% used Best Start Grant as savings for their child or the family.

Respondents also said they used Best Start Grant for day-to-day household costs and essentials such as food and bills (29%), and larger household costs such as furniture and car expenses (5%).

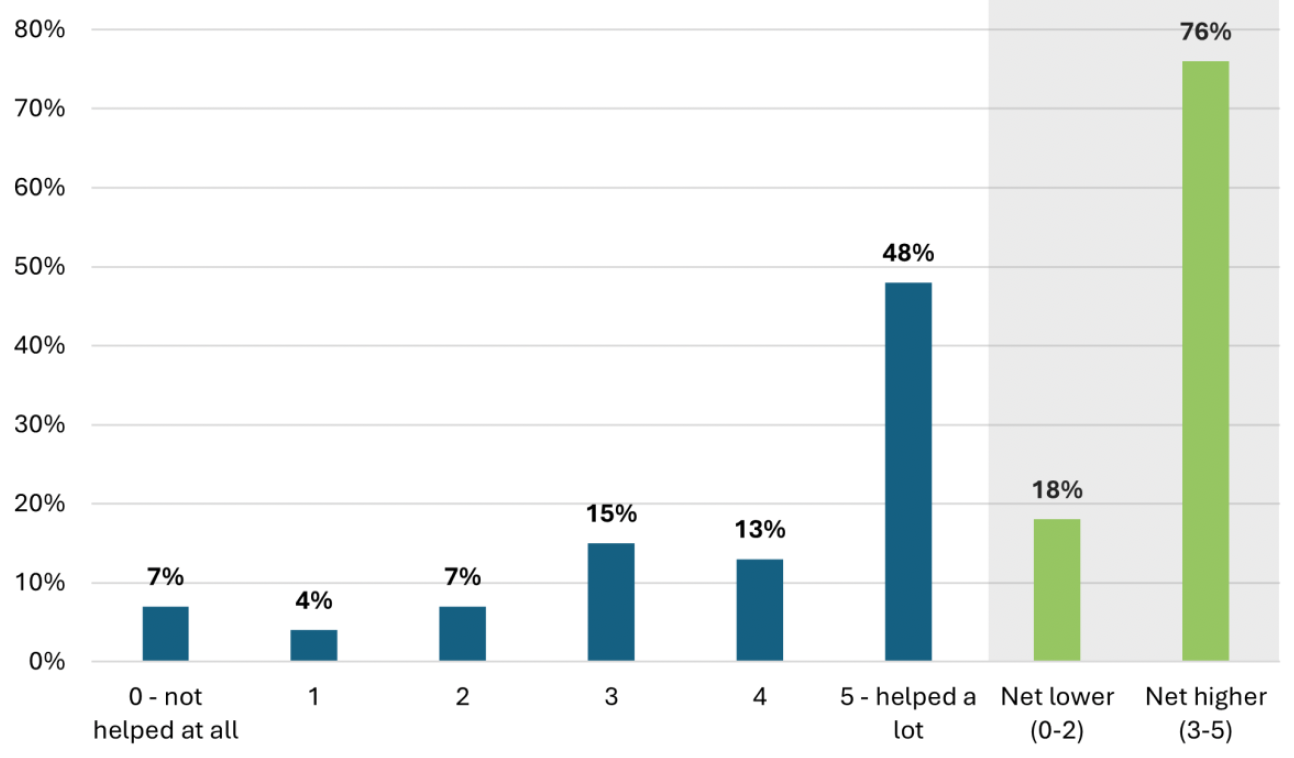

Best Start Grant recipients were also asked on a scale of zero (‘not at all’) to five (‘a lot’) how much the payments helped them to buy the things their child needed, such as when they were born, or started nursery or school. As shown in Figure 7, 65% rated Best Start Grant five (helped a lot) for helping them to buy the things their child needed. Overall, 89% gave a higher rating of three to five, and 6% gave a lower rating of zero to three.

There were statistically significant differences relating to priority families most at risk of poverty. Specifically, the following subgroups were more likely than others to rate Best Start Grant five (helped a lot) for helping them to buy the things their child needed, such as when they were born, or started nursery or school:

- Respondents from two or more parent/carer households (69%) compared with those from one parent/carer households (64%)

- Households with a disabled family member (68%) compared with those without a disabled family member (62%).

- Families from white ethnic backgrounds (68%) compared with those from minority ethnic backgrounds (50%).

In the qualitative interviews and open-text survey responses, Best Start Grant recipients explained how the payments helped them with child-related spend. Pregnancy and Baby Payment recipients said the large one-off payment enabled them to buy expensive essential items such as a pram, cot, car seat or bedroom furniture. Some parents and carers also used the payment for items they needed as a new mum, such as maternity clothing, breast pumps and breast pads. While the pregnancy and baby payment did not always cover all the new child costs, overall it helped families to buy what they wanted, when they needed it.

It went quick because the cot was £200, the pram was near enough £300, then obviously the movers and my breast pumps and the bottles, so I don’t think it actually covered all of that but it covered the majority of it. So it allowed me to get the things I needed so it was…it’s a good whack of money that really does help.

(Parent and carer interview)

Early Learning Payment recipients described using the payment to buy nursery clothes, such as a uniform or clothes suitable for nursery activities, like wellies, waterproofs, hats and gloves to be bought and left at nursery. Parents and carers also said the value of the payment helped them to buy better quality items such as shoes that would last longer, or clothing as and when their child needed it, citing their child growing quickly or their clothes being worn out from play and activity.

I went out and bought her some Clarks trainers because they're obviously really good trainers. They don't get scuffed up as quick as what cheaper trainers do. And I went and bought her loads of spare clothes that she could just wear for nursery because obviously, you can imagine their clothes get ruined at nursery. A hat and gloves, a bag, lunchbox, stuff like that. So that really helped out too.

(Parent and carer interview)

School Age Payment recipients mostly described using the payment for school uniforms and other school-related costs. As with the other Best Start Grant payments, while some parents and carers used the payment for the eligible child only, others used it for multiple children where necessary. For example, those with large families highlighted the expense of clothing multiple children. There were also examples of the School Age Payment helping parents and carers meet the needs of a child with sensory needs linked Autism. This reflects the survey findings above, which show that households with a disabled family member were more likely than those without a disabled family member to say Best Start Grant helped ‘a lot’ to buy the things their child needed.

He just started school in August, yeah August, so yeah we received that [School Age Payment] which was amazing and we obviously used that for things like his school uniform, for his first school haircut […] he has sensory difficulties, so we had to make sure that the uniform we bought was okay with his skin and kind of checked the labels and things like that. […] you’d have to maybe get the bus because I don’t drive and go to different supermarkets and try out different clothes and see how he reacted with the textures when he had them on.

(Parent and carer interview)

Reduced pressure on household finances

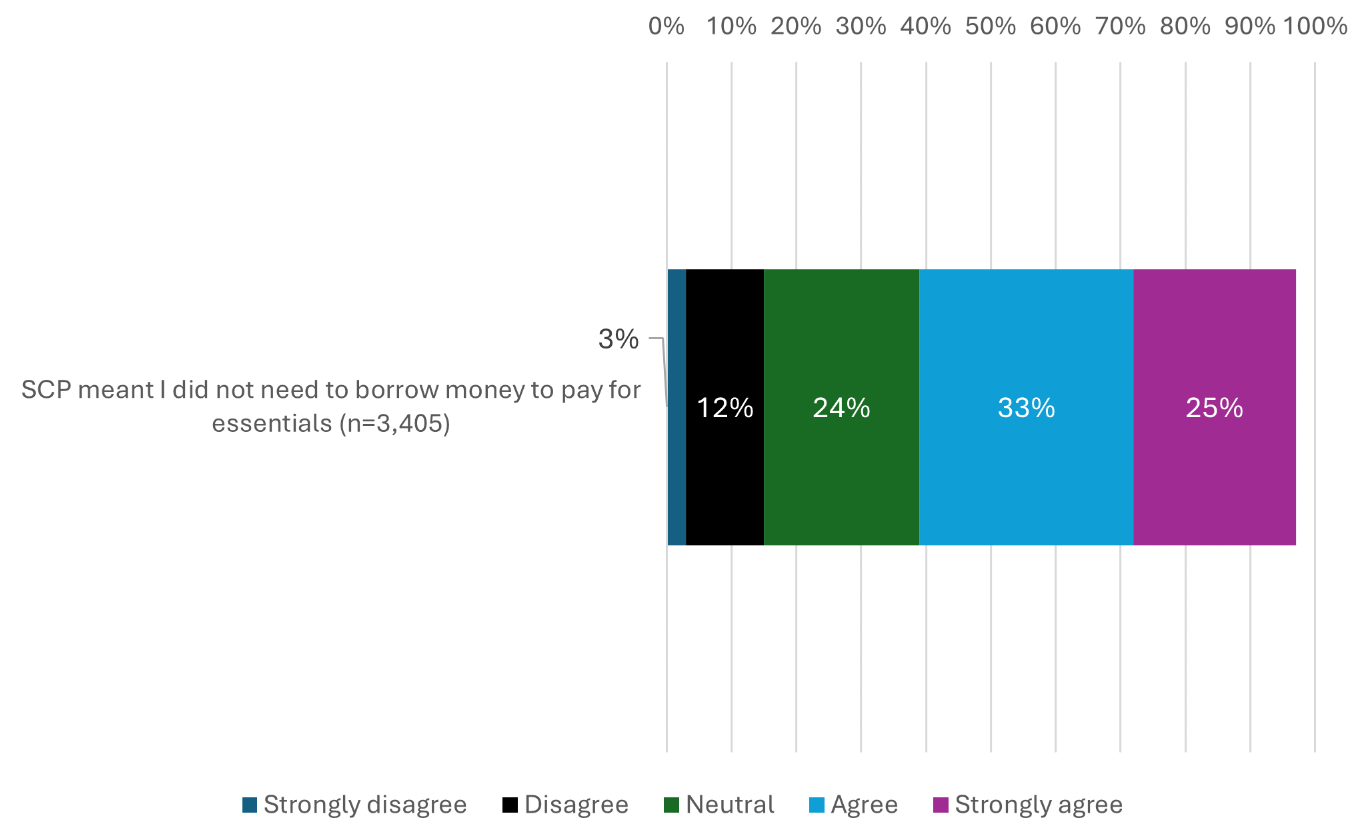

It is intended that the Five Family Payments lead to reduced pressure on household finances. This outcome is therefore relevant to all of the Five Family Payments benefits. The commissioned research addressed this topic in the survey and qualitative interviews. This section focuses specifically on how the payments helped with the cost of household essentials. The findings are presented below for each of the individual benefits. However, other relevant findings are covered later in the Findings chapter, specifically in relation to the outcomes ‘Reduced money-related stress’ and ‘Reduced incidence of debt’.

Scottish Child Payment and pressure on household finances

The commissioned research explored the impact of Scottish Child Payment on paying for household essentials. As shown earlier in this report, 66% of survey respondents who received Scottish Child Payment said they used the payments for day-to-day household costs and essentials, whilst 39% said this is what they used Scottish Child Payment for the most. There were statistically significant differences relating to the priority families most at risk of poverty. Specifically, the following subgroups were more likely to say they mostly used Scottish Child Payment for day-to-day household costs and essentials:

- Households with a disabled family member (43%) compared to those without a disabled family member (33%).

- White ethnic families (42%) compared to minority ethnic families (24%)

- Families with no child under 1 year old (41%) compared to those with a child under 1 year old (21%).

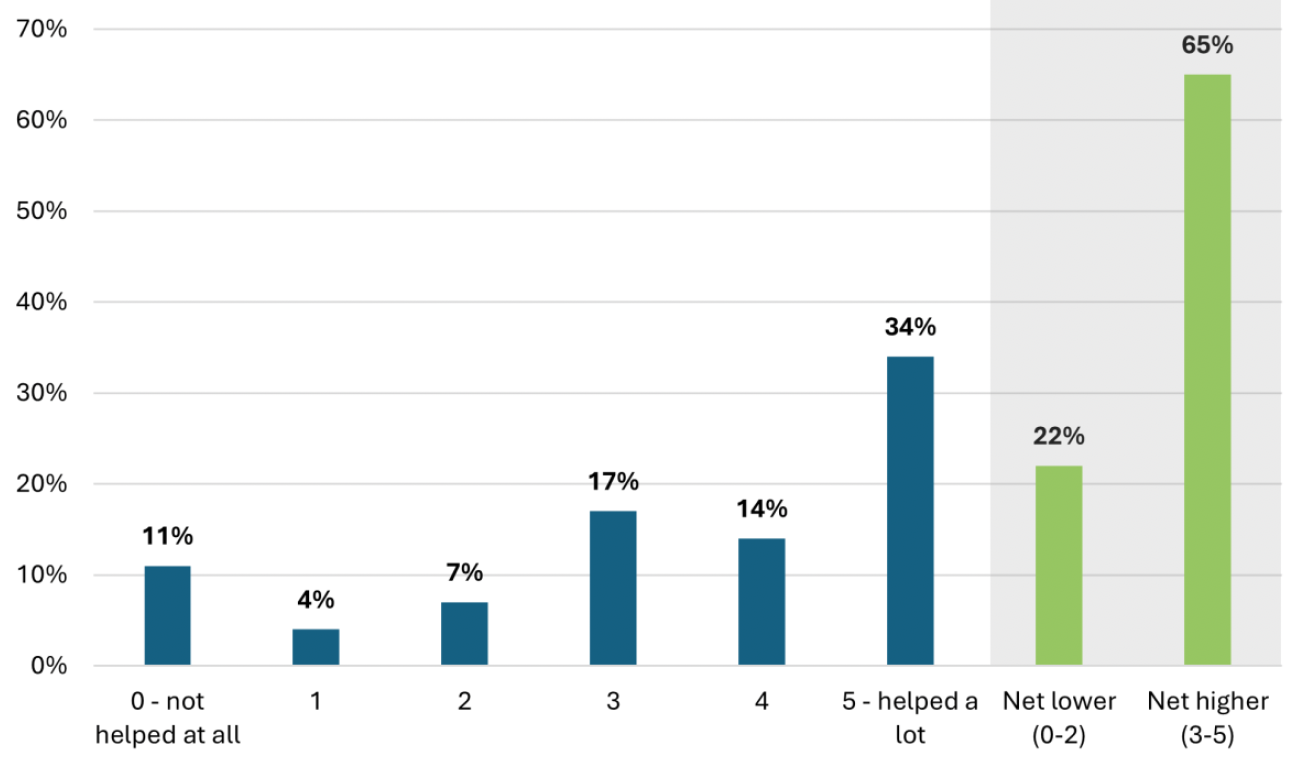

Respondents were also asked, on a scale of zero (‘not at all’) to five (‘a lot’), how much the payments helped them to pay for household essentials like food, rent, gas and electricity. As shown in Figure 8, 49% rated Scottish Child Payment five (helped a lot) for helping to pay for household essentials. Overall, 77% gave a higher rating of three to five, and 19% gave a lower rating of zero to two.

With regards to the priority families at risk of poverty, the following subgroups were more likely than others to rate Scottish Child Payment five (helped a lot) for helping them to pay for household essentials:

- Families with three or more children (54%) compared to those with one or two children (47%)

- Households with a disabled family member (51%) compared to those without a disabled family member (45%)

- Families from white ethnic backgrounds (51%) compared to those from minority ethnic backgrounds (38%).

- Families with no children under 1 year old (49%) compared to those with a child aged under 1 (41%).

Notably, as shown above, three of these subgroups (households with a disabled family member, families from white ethnic backgrounds, and families with no children under 1 year old) were also more likely to say they spent Scottish Child Payment on household essentials. These findings appear to be linked, suggesting those who spent the payments mostly on household essentials were therefore more likely to find them helpful when it came to buying household essentials.

Regarding other subgroups with statistically significant differences:

- Those who had been receiving Scottish Child Payment for over 12 months were more likely than those receiving it for less than 12 months to say it helped ‘a lot’ to pay for household essentials (51% compared with 44%).

The commissioned research also provides qualitative evidence about Scottish Child Payment being used for household essentials. In open-text survey responses, hundreds of respondents said they used Scottish Child Payment to help with household essentials, particularly food, housing and utility bills. Some said they relied on the payments to pay for these essentials, especially due to the cost of living increases, which Scottish Child Payment helped to mitigate.

This payment has been a life saver, especially since the cost of living crisis. I used to be able to get a decent amount of shopping and essentials every week without worrying too much, but the cost of shopping is unbelievable. Without this payment we would be eating much worse, less fresh and nutritious foods and be relying on cheap frozen food instead.

(Survey respondent)

I rely heavily on the payment to help with weekly household costs which are constantly increasing.

(Survey respondent)

Parents also said they relied on Scottish Child Payment for essentials because their personal circumstances (such as being a lone parent, having a large family, caring for a disabled family member, or being out of work) made their finances challenging. This reflects the survey findings above, which show that those with three or more children or a disabled family member were more likely to say Scottish Child Payment helped them ‘a lot’ to pay for household essentials.

I have 6 kids. The Scottish payments very helpful because without Scottish payments I can’t manage living crisis. I like to say many thanks.

(Survey respondent)

Stakeholders felt that Scottish Child Payment was important for large families for whom they said payments could make the difference between being in poverty or not, with one stakeholder citing the impact of the two-child limit for Child Tax Credits and Universal Credit.

[Scottish Child Payment] definitely makes an impact financially, especially where you have families who have more than 2 children right because of the 2-child rule. So, if you’ve got 4 kids right and you’re not getting the child element payment for 2 of them […] that £53 a week can go towards food bills, can go towards ongoing clothes that they need...

(Stakeholder interview)

However, some recipients said they struggled with the cost of living despite the assistance of Scottish Child Payment. In some of these cases, parents mentioned that increasing the payment amount would help them meet essential costs and reduce financial pressure.