Decarbonising heating - economic impact: report

This report considers the potential economic impacts arising from a shift towards low carbon heating technologies in Scotland, over the period to 2030.

Appendix B Deployment of heating technologies in Scotland to 2030

B.1 Framing the analysis

We applied a technology diffusion model, FTT:Heat, to assess how different heating technologies could be deployed in the period to 2030 to meet Scotland's heat demand under different policy scenarios. More detail is provided on the modelling framework in Appendix A.

We constructed a baseline projection, setting out how, absent any further policy intervention, heating demand in the period to 2030 is expected to be met. This reflects the existing deployment of heating technologies (since the majority of technologies currently in use would be expected to continue to be in use in 2030).

Three policy scenarios were then modelled. In the first, 'Subsidy', additional policies focused on market-based instruments, and in particular providing subsidies to reduce the up-front cost by 75% of low carbon heating technologies from 2022 onwards. Electric heating, heat pump ground, heat pump air/water, heat pump air/air, and solar thermal are considered low carbon heating technologies. Biobased heating technologies have been excluded from this subsidy package.

In the second, 'Regulation', policies are focused on regulation, for example specifically phasing out gas boilers. From 2025 onwards new capacity of these technologies cannot be installed and they phase out at a rate that is approximately inverse to their lifetimes. Such a policy will likely have to be imposed by the UK government.

Finally, the 'Extended' scenario introduces both market-based and regulatory policies to meet the stringent targets set for Scottish heat decarbonisation by 2030. In addition to the subsidies and regulations, it includes a government procurement program, through which the Scottish Government can encourage the take-up of low-carbon heating technologies via bulk procurement for installation into buildings. Lastly, in this scenario biomethane blending rates increase to 7.5% on a volume basis, a conservative projection compared to what is proposed in scenarios for the Energy Networks Association (Navigant 2019).

It should be noted that the first two scenarios do not meet current Scottish Government targets – they are instead exploratory scenarios to evaluate the potential impact of policy measures. The key focus of the analysis, therefore, is on the Combined scenario and its potential impacts.

Note(s): Direct emissions only.

| Scenario \ Policy | Regulations | Subsidies | Procurement program | Biomethane blending[6] |

|---|---|---|---|---|

| Reference scenario | Limited additional communal heating and gas grid extension | No subsidies | No procurement program | At a constant 1.5% of the gas supply |

| Subsidy scenario | As reference | 75% subsidies on the upfront costs of renewable heating | No procurement program | At a constant 1.5% of the gas supply |

| Regulation scenarios | As reference + Complete phase-out of fossil fuelled boiler sales | No subsidies | No procurement program | At a constant 1.5% of the gas supply |

| Extended scenario | As reference + Complete phase-out of fossil fuelled boiler sales | 75% subsidies on the upfront costs of renewable heating | Flats: procurement program to increase electric heating[7] and air-to-air heat pumps. Houses & non-domestic buildings: procurement program to increase heat pumps. | Grows to 7.5% of the gas supply in 2030 |

B.2 Modelled technology pathways

To model the technology pathways under different conditions, we evaluated historical uptake of heating technologies, as this is the point of departure for the scenarios. In our analysis, we constructed historical data on useful heat generation (final energy use for heat purposes minus efficiency losses) for the period between 2005 and 2018 for domestic flats, domestic houses, and non-domestic buildings. Over this period, Scottish homes were predominantly heated by burning natural gas, while about half of the non-domestic buildings utilise electric heating (see Figure 2.1).

Heat projections for domestic buildings

We developed projections of useful heat demand. A sizeable proportion of flats and houses are rated EPC band C or lower (57.3% of all dwellings, Scottish Housing Condition Survey (2019)). The Scottish Government is aiming to bring all homes up to EPC band C by 2033. However, at the time this analysis was carried out, the expected target was for all homes to be EPC band C by 2035, and it is this slower rollout of energy efficiency that is included in this analysis. Therefore, three factors determine the demand for domestic heat:

- Increasing building efficiencies

- Changes in the number of households per local authority

- A split between flats and houses between local authority

Heat demand for non-domestic buildings

To project future heat demand, gross value added (GVA) projections by local authority were used as an estimate for the number of non-domestic buildings (GVA projections were modelled by Cambridge Econometrics and includes estimated COVID-19 impacts[8]). About 86% of the non-domestic buildings were rated EPC band D or worse (The Scottish Government 2018), leaving plenty of room for improvement. From the historical non-domestic energy demand and estimates on heating technology efficiencies, estimates for historical useful heat demand were obtained. By connecting the historical useful heat demand with the historical GVA, useful heat demand intensities (as a function of GVA) were obtained. Therefore, non-domestic heat demand projections depend on:

- GVA projections

- Energy efficiency improvements (i.e. energy intensity reductions), based on the 2010 to 2018 compound annual growth rate in non-domestic energy intensity (GWh/m£2016 GVA)

Simulation of future heat technology uptake

By applying the Future Technology Transformations for heat (FTT:Heat) methodology (see Appendix D), it is possible to look at the effects of different policy packages on the supply-side of heating. Technology substitution is cost-based, context-driven, region-dependent, and realistically constrained in this framework (Knobloch, Mercure and Pollitt, et al. 2017).

If no additional policies are introduced (Reference scenario), it is very likely that gas-based heating remains dominant for both domestic building types, while gas-based heating grows a bit at the expense of low-quality electric heating. This is mainly due to non-domestic GVA being projected to grow faster in gas-dominant regions, which therefore leads to more rapid heating demand growth in these areas and the continued domination of gas heating.

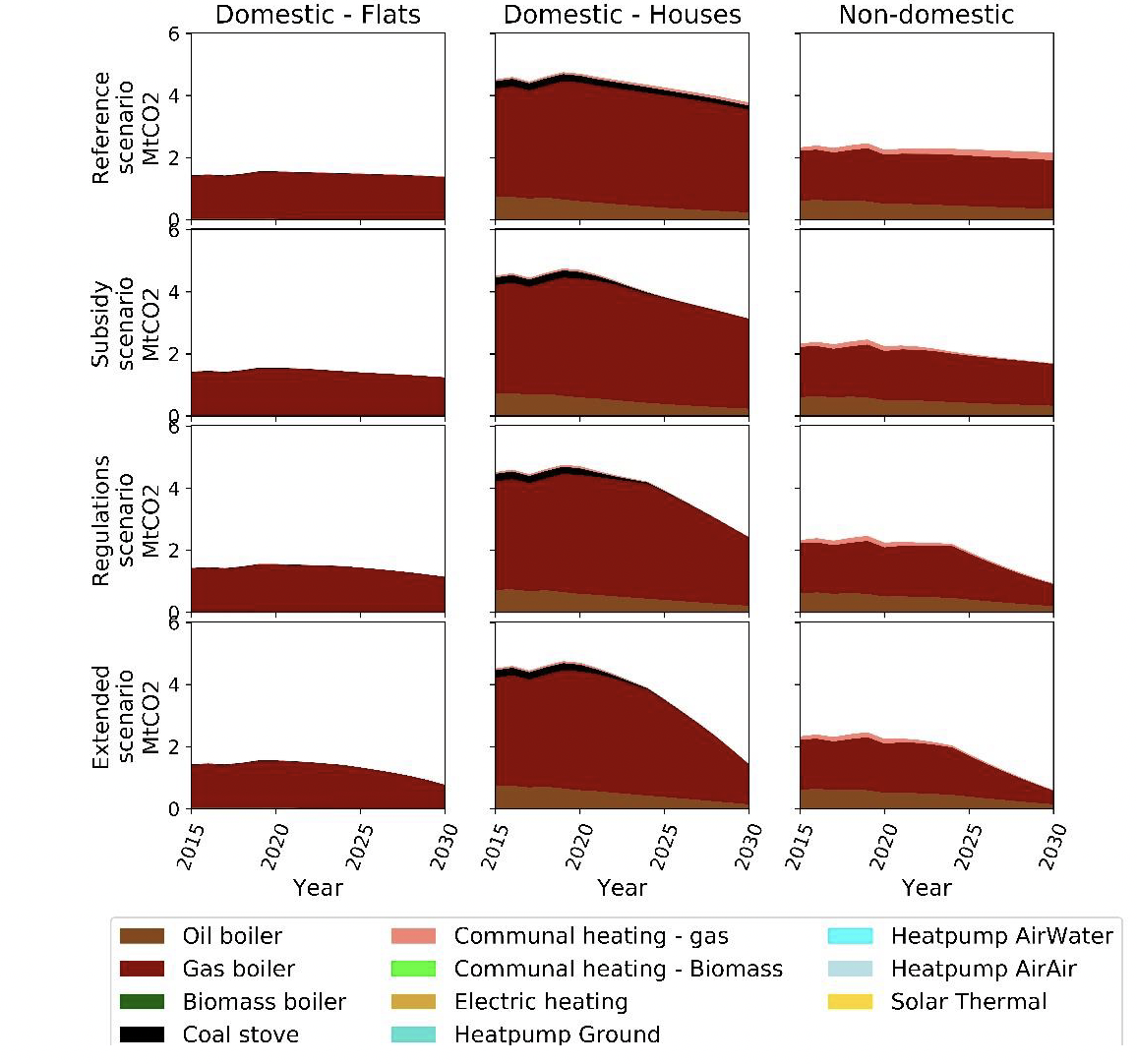

Emissions by heating technology

The technological composition of heating demand affects the emission profile of each building type (see Figure B.1). In the Reference case, a stagnant profile is found for flats. The increase in the number of flats is offset by an increase in building efficiency, but gas boilers remain dominant as little technology substitution takes place. In houses, a steady decrease in emissions is seen. This is due to increased efficiency and marginal substitution from gas boilers to renewable heating technologies. For non-domestic buildings a slight increase in emissions occurs, which is mainly driven by increasing GVA in some local authorities where fossil-fuelled heating is a slightly greater proportion of the technology mix, leading to a deployment of new fossil fuel-based heating at a greater rate than realised energy efficiency measures can fully counterbalance.

Decision-making in terms of investment in specific technologies responds to the policies enacted, and this is reflected in the emissions profiles. Houses and non-domestic buildings show some emission decreases in the subsidy and regulations scenario. Flats show a stagnant profile in both scenarios. We found major emission decreases under the Extended scenario for houses and non-domestic buildings due to replacement of gas boilers by heat pumps. Emissions from flats also decrease in this scenario, albeit at slower pace.

The emissions outcome is summarised in Table B.2 for each of the scenarios and building types.

| 1990 | 2018 | 2030 | 2030 | 2030 | 2030 | |

|---|---|---|---|---|---|---|

| Unit: MtCO2 | Base year | Last historical datapoint | Reference scenario | Subsidy scenario | Regulation scenario | Extended scenario |

| Flats | n.a. | 4.42 | 3.77 | 3.14 | 2.43 | 1.43 |

| Houses | n.a. | 1.68 | 1.39 | 1.25 | 1.15 | 0.78 |

| Domestic | 8.0 | 6.1 | 5.16 | 4.5 | 4.74 | 2.21 |

| Non-domestic | 2.9 | 2.4 | 2.16 | 1.70 | 0.93 | 0.60 |

| Total | 10.9 | 8.5 | 7.32 | 6.2 | 5.67 | 2.81 |

| Change compared to 1990 base year | 0% | -22.2% | -32.9% | -44.3% | -58.7% | -74.3% |

Expenditure on heating technologies

Beyond affecting the emission profile, the technological composition also affects expenditure on heating technologies. End of life replacement and premature scrapping can affect the expenditure profile (see Appendix D). Expenditure on heating technologies is based on installed heating capacity. For certain technologies more capacity is needed to provide Scottish buildings with enough space and water heat throughout the day and through the year. Due to the specific technologies within heat pumps, although they are more efficient than other heating technologies, the cost of the technology itself is higher than the cost of a gas boiler to meet an equivalent typical Scottish heat demand. As a result, the rate of heat pump uptake has a large effect on expenditure outcomes in the scenarios.

Contact

Email: heatinbuildings@gov.scot