Decarbonising heating - economic impact: report

This report considers the potential economic impacts arising from a shift towards low carbon heating technologies in Scotland, over the period to 2030.

3 The economic impacts of decarbonising heat

Building on the heating technology pathways set out in the previous chapter, we used the Scottish Supply, Use and Input-Output tables to evaluate the economic impacts associated with the different scenarios. More detail on the methodology is presented in Appendix A.

We carried this analysis out in two stages. Initially, we used the Scotland Input-Output tables to evaluate macroeconomic impacts of the different aspects of the decarbonisation of heating at the national level. Subsequently, we explored the distribution of these impacts, both spatially and in terms of socio-economic classification of households, using a combination of quantitative modelling, analysis of historical trends and qualitative narrative.

3.1 The economic footprint of transforming heating demand

All results presented and discussed below are based upon the assumption that the structure of the Scottish economy will not substantially change over the period from 2017-2030 – a necessary assumption for the application of static input-output modelling as carried out for this analysis. The input-output tables provide information on the domestic and imported content of each sector – so we are able to measure how much changes in demand are met through changes in domestic production versus imports, although this data is only available at the 2-digit SIC code level, not at the more detailed component level (this issue is discussed in more detail later in the chapter).

The analysis considers direct and indirect impacts, which is to say direct changes in expenditure (e.g. lower demand for gas boilers, and higher demand for heat pumps) and follow-on impacts through supply chains (for example lower demand for pilot lights and higher demand for electrical heat exchangers, as components of gas boilers and heat pumps respectively). It does not include the induced effects linked to overall changes in economic activity and employment (e.g. if employment in electrical equipment is higher, this creates additional wages in the economy, which increases demand for food & drink and other consumer goods/services). The analysis also does not seek to balance out changes in expenditure; so we do not consider whether household expenditure on other goods and services would decrease in order to facilitate higher expenditure on heating technologies, for example, or the follow-on economic impacts of these shifts.

The analysis splits the transition in heating technologies into four distinct effects[2];

- Reduced demand for high carbon technologies

The shift away from gas- and other fossil fuel-based technologies will result in reduced output from the manufacture of gas and oil burners - Increased demand for low carbon technologies

The greater demand for heat pumps, electrical heating, biomass boilers and solar thermal technologies will increase output from manufacturers of such items - Lower demand for high carbon fuels

The shift away from fossil fuel-based technologies will reduce demand for, and therefore output from, gas and oil to fuel these types of boilers - Higher demand for low carbon fuels (including electricity)

Increased usage of heat pumps and other low-carbon technologies will increase demand for low carbon fuels (chiefly biomass and electricity), leading to higher output from these industries.

In the analysis that follows, each of these impacts is considered in turn. The reason for this approach is that economic analyses often focus on net impacts, in terms of both employment and output. Even when providing some sectoral breakdown of impacts, the focus is on net changes within a given sector, which ignores that different jobs are being created and lost, both in terms of the sub-sector in which the activity takes place, and the geographical location of the activity. For example, manufacturing jobs are lost in gas boiler manufacture, and created in heat pump manufacture – and while both are manufacturing jobs, they require different skills, and are very likely to be based in different places. Through evaluating the job impacts in separate stages, our analysis provides more detailed insight into the creation and loss of jobs and economic activity.

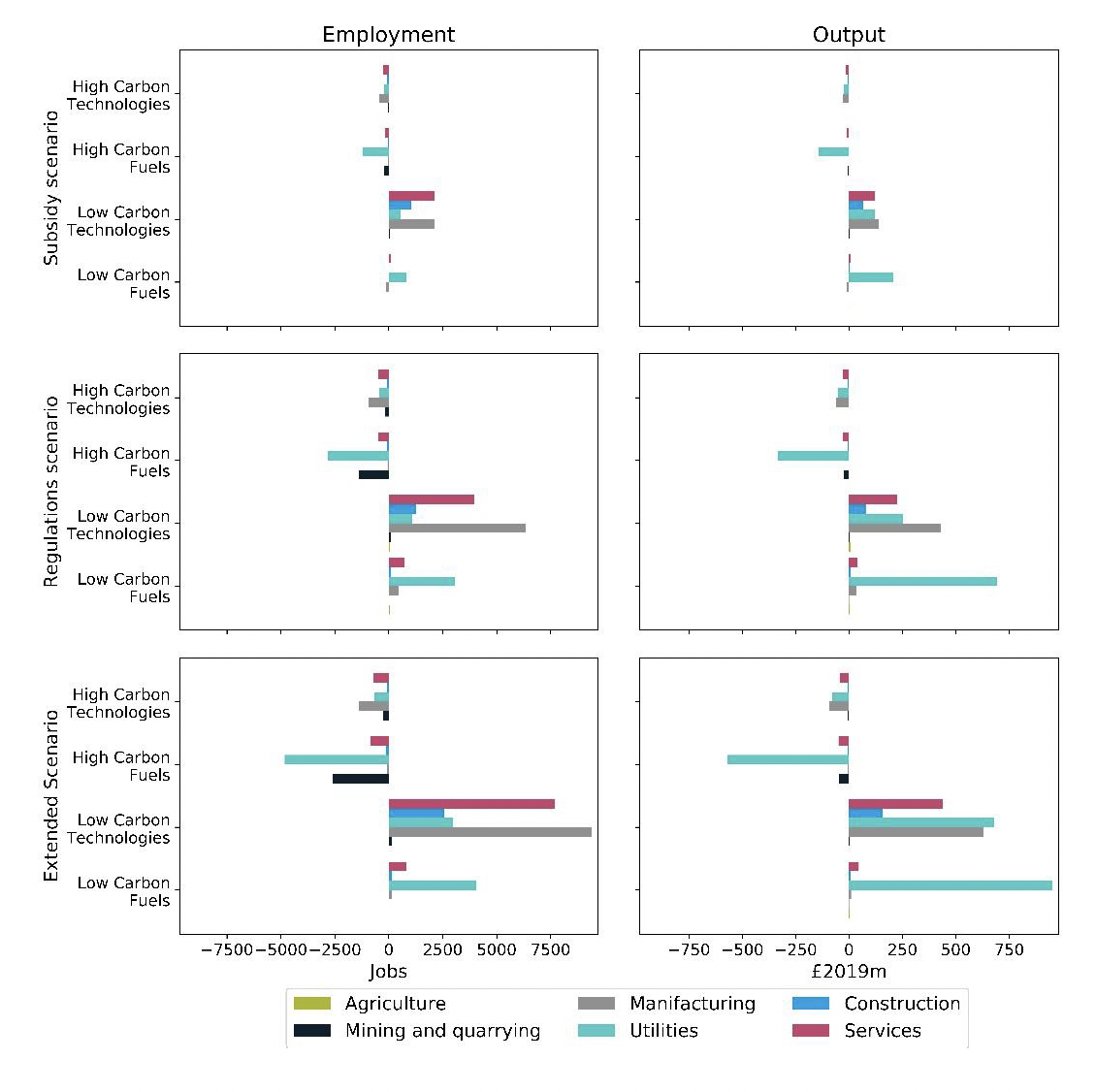

The economic impacts scale with the level of decarbonisation achieved in the scenarios; so the smallest changes in employment and output are seen in the Subsidy scenario, followed by the Regulation scenario, with the largest impacts (both positive and negative) in the Extended scenario. There are similar narratives across all three scenarios, as the underlying dynamics are similar.

The shift away from high carbon technologies results in a small number of jobs losses linked to the supply of the heating technologies themselves, most notably in the manufacture of the equipment. However, our modelling suggests that the potential job gains from a shift to low-carbon technologies will create more jobs than are lost; in manufacturing (linked to the production of the technologies) and services (through supply chain effects). In the Extended scenario, just over 3,100 jobs are lost in 2030 due to the transition away from high-carbon technologies, with 1,400 of those in manufacturing. The switch to cleaner technologies is expected to create 22,800 jobs, however, with over 9,400 in manufacturing and a further 7,700 in services (see Table 3.1).

| Employment difference from baseline, jobs | Switch away from high-carbon technologies | Change in demand for high-carbon fuels | Switch towards low-carbon technologies | Change in demand for low-carbon fuels | Total |

|---|---|---|---|---|---|

| Agriculture | -4 | -8 | +22 | +16 | +26 |

| Mining & quarrying | -264 | -2,613 | +150 | +12 | -2,715 |

| Manufacturing | -1,386 | -102 | +9,413 | +145 | +8,070 |

| Utilities | -671 | -4,825 | +2,957 | +4,071 | +1,532 |

| Construction | -95 | -118 | +2,575 | +140 | +2,502 |

| Services | -710 | -837 | +7,679 | +819 | +6,951 |

| Total | -3,130 | -8,503 | +22,796 | +5,203 | +16,366 |

Conversely, more jobs are lost from reduced demand for high-carbon fuels (primarily gas and oil, with a substantial domestic supply chain) than are gained from increased demand for low-carbon fuels (chiefly electricity). The driver of these outcomes are slightly different; in the case of technologies, the higher up-front costs of low-carbon technologies vis-à-vis their high carbon equivalents means more is spent on them, leading to more jobs being created in the production of low-carbon equipment. In terms of fuels, while the difference in overall expenditure is small (as can be seen in Figure 2.3), the higher labour productivity of the electricity supply sector as compared to gas extraction supply leads to smaller job creation in the electricity sector than the number of jobs lost in the gas industry. These dynamics are demonstrated across the scenarios (see Figure 3.1). However, it should be noted that there is substantial uncertainty around the impacts on the oil & gas sector in particular. This analysis assumes that reduced domestic demand for natural gas for heating would lead to a reduction in supply from offshore rigs; however, it is more likely that this gas would instead be sold into different markets, and it is unlikely that domestic demand would have a major impact on global prices for gas, so in fact there may be minimal (or no) jobs lost in the Scottish extraction industry as a result of this transition.

The impacts on economic output vary from the impacts seen on employment, in terms of relative sectoral weight (i.e. the size of impact in one sector relative to another). This primarily reflects the labour intensity of the different sectors; the utilities sector, for example, has relatively high productivity (based upon data in the input-output tables), and therefore a large impact on output translates into a smaller impact in terms of employment, relative to the impacts in other sectors (notably manufacturing, which typically has a productivity below the economy-wide average). The net impact on gross output in 2030 is an increase of just over £2bn; this is equivalent to a 0.6% increase in the size of the 2017 Scottish Economy, and therefore a slightly smaller percentage increase in the (anticipated) larger Scottish economy of 2030.

In aggregate, the employment impacts are net positive in all scenarios; in the Extended scenario almost 16,400 jobs are created in 2030, once jobs created and jobs lost are balanced against each other. This suggests that overall, the transition can be expected to have a positive impact on the Scottish economy, although continued investment in new low-carbon heating technologies from households and businesses will be required to sustain this effect.

| Gross output difference from baseline, £m (2017 prices) | Switch away from high-carbon technologies | Change in demand for high-carbon fuels | Switch towards low-carbon technologies | Change in demand for low-carbon fuels | Total |

|---|---|---|---|---|---|

| Agriculture | -0.3 | -0.5 | 0.0 | +1.7 | +0.9 |

| Mining & quarrying | -5.2 | -47.3 | +4.0 | +0.4 | -48.1 |

| Manufacturing | -91.3 | -6.3 | +629.8 | +9.6 | +541.8 |

| Utilities | -80.4 | -568.0 | +680.6 | +950.7 | +982.9 |

| Construction | -5.8 | -7.2 | +158.3 | +8.6 | +153.9 |

| Services | -41.8 | -49.2 | +438.9 | +45.6 | +393.5 |

| Total | -224.8 | -678.5 | +1,911.6 | +1,016.6 | +2,024.9 |

It should be noted that this analysis reflects existing Scottish supply chains and assumes that reduced demand from final consumers and industry cannot be replaced by demand from elsewhere (including overseas). This assumption is questionable in respect specifically to the oil & gas extraction industry; as outlined previously, while domestic demand for natural gas will go down as a result of the transition to low-carbon technologies, it is reasonable to think that domestic extraction/production will not go down, but instead that gas that was previously consumed domestically will instead be sold into the international gas markets.

The analysis above is based upon (in the baseline and all scenarios) an assumption that all Scottish homes are upgraded to a minimum of EPC band C by 2035, which was the suggested target at the time this analysis was carried out. The Scottish Government has since committed to deliver this change to the housing stock no later than 2033. This more accelerated rollout of energy efficiency would not change the key messages contained in this economic analysis, although the precise impacts (in terms of specific changes in output and employment) would be expected to change slightly. This is because energy efficiency has the effect of reducing effective heat demand. Under a more rapid deployment of energy efficiency, final heat demand in the period to 2030 would be expected to reduce slightly more rapidly than was modelled. This does not affect the demand for heating technologies, but would reduce overall demand for heating fuels (including electricity), across the baseline and scenarios. This is likely to reduce job losses in the utilities sector, as the change in demand for gas and electricity would be smaller (reflecting the slightly more efficient housing stock needing less in terms of energy inputs), but such impacts would be minor.

3.2 The spatial distribution of activity

Predicting precisely where these jobs will be created within Scotland is a challenging task; it requires knowledge of the existing spatial distribution of existing specific industries and value chains (for example, where are current gas boiler manufacturers and heat pump manufacturers located across Scotland, and where do they source their components from?), but most importantly also requires a prediction of where future activities will take place, and what location decisions will be taken by new/existing firms as demand for these products scales up (for example, will heat pumps continue to be manufactured primarily in existing locations, but at greater scale, or will firms seek to take advantage of the availability of skilled labour in regions where declining demand for gas boilers has led to job losses?). In the analysis that follows, we seek to explore what existing economic data can tell us about the potential geographical impacts of the transition, but further in-depth analysis through survey and case studies should be considered to evaluate these issues in more depth.

In order to consider the differential impacts upon the sub-national economies within Scotland, we evaluated existing industrial structures and assessed which regions currently demonstrate some specialisation in the relevant sectors (in particular, in oil & gas extraction, electrical equipment manufacture, machinery & equipment manufacture, electricity supply and gas supply), in order to understand both where existing jobs (in fossil fuel-related activities) are likely to be lost, and also where there is the greatest likelihood (due to the existence of a suitably skilled workforce, and an existing base of firms) of new jobs being created.

Using data from the Business Register Employment Survey (BRES) for 2017, the local authorities with the greatest shares of Scottish employment in the relevant key sectors have been identified in Table 3.3.

This provides some insight into where the sectoral impacts can be expected to be concentrated. It is unsurprising that over 80% of jobs in Scottish oil & gas extraction are in Aberdeen and the surrounding area (including on offshore rigs), and it is therefore likely that the job losses in this sector (expected to Total 2,700 by 2030 in the Extended scenario) will be focused in this region. However, as noted above, the true impact on the gas extraction industry may well be much lower than set out in this analysis, if the gas is sold into export markets when domestic demand falls.

| Oil & gas extraction 1.2% of Total Scotland employment in 2017 | Electrical equipment 0.6% of Total Scotland employment in 2017 | Machinery & equipment 0.6% of Total Scotland employment in 2017 | Electricity supply 0.5% of Total Scotland employment in 2017 |

Gas supply 0.2% of Total Scotland employment in 2017 |

|||||

|---|---|---|---|---|---|---|---|---|---|

| Aberdeen City | 67% | Fife | 26% | Fife | 17% | Glasgow City | 17% | City of Edinburgh | 29% |

| Aberdeen-shire | 14% | West Dumbarton-shire | 11% | West Lothian | 10% | Perth and Kinross | 16% | South Lanarkshire | 29% |

| Highland | 4% | North Lanark-shire | 9% | Aberdeen-shire | 10% | North Lanark-shire | 12% | Glasgow City | 14% |

| Fife | 2% | Aberdeen City | 8% | North Lanark-shire | 9% | South Lanark-shire | 10% | Aberdeen City | 6% |

| North Lanark-shire | 2% | South Lanark-shire | 8% | Aberdeen City | 8% | Highland | 7% | North Lanarkshire | 6% |

| City of Edinburgh | 2% | Glasgow City | 5% | Renfrew-shire | 8% | City of Edinburgh | 5% | Renfrew-shire | 4% |

Source: BRES

While employment in the other sectors is more spread across Scotland, it's clear that Fife, with a specialisation in electrical equipment and machinery & equipment, faces a major restructuring challenge, with jobs likely to be lost in the manufacture of existing high carbon technologies, but a major opportunity to leverage specialisations to become a focal point for the production of the low carbon alternatives. North and South Lanarkshire will face the same challenge, albeit on a smaller scale. However, it should be noted in all cases that the data only tells us that these regions focus in the broad electrical equipment and machinery & equipment sectors; from this data it is not possible to accurately identify whether there are specific activities relating to boiler or heat pump manufacturing in these locations. Such analysis would require a much more focused data collection exercise, such as a survey, to establish precisely where specific components and products are manufactured. If this were to be carried out, it should focus on mapping out existing producers and supply chains in both the old and new technology value chains; this might best be achieved through a nationwide survey carried out through manufacturing members' organisations.

When looking at fossil fuel supply, Edinburgh, South Lanarkshire and Glasgow are the areas where gas jobs are focused (representing over 70% of Total Scottish employment in this industry) and would expect to bear the brunt of job losses. Conversely, increased demand for electricity could be expected to boost employment in some of the existing key regions for electricity supply, including the offshore wind supply chain clusters in Glasgow and Edinburgh, as well as renewables activities in the Highlands and onshore wind in particular in North and South Lanarkshire. While some regions (notably Glasgow and Edinburgh) are boosted in terms of the size of these industries due to headquartering effects (e.g. SSEN and Scottish Power have major offices in Glasgow), it is reasonable to think that jobs would increase in these locations, alongside generation sites, if Total demand for electricity increased.

While such analysis of, and interpolation from, historical data can provide understanding of where existing jobs might be lost, there is greater uncertainty around where new jobs might be created. Most obviously, given the ongoing decarbonisation of electricity generation, it is not clear that future employment in the electricity sector will be in the same technologies, and therefore in the same locations as existing jobs – although given the advanced state of Scotland's efforts to decarbonise this sector the analysis does at least suggest employment opportunities in regions which already have some degree of specialisation in generation via renewables.

Impacts across the income distribution

The quantitative analysis outlined above does not seek to evaluate the distributional impacts of the transition. However, the technology switching, and information on the cost of technologies and fuels, which is used to calculate the economic impacts outlined above, provides detail into how the nature of consumer expenditure can change in the transition. In the Extended scenario (the focus of our analysis), Total expenditure on heating technologies (i.e. the replacement of existing, primarily gas, boilers with new heat pumps and other low-carbon technologies) increases substantially, although subsidies offered by government bring these costs down broadly into line with the reference case. This shift in expenditure (and in particular the higher unsubsidised upfront 'investment' costs associated with low-carbon heating technologies) is likely to be easier to manage for higher income households, who have the financial liquidity to be able to afford to pay a higher purchase price for the technology (or access to finance to allow it). This demonstrates how important the use of relevant government policy levers (such as subsidies), well targeted at those households that are least able to pay higher up-front costs, are in ensuring the successful deployment of low-carbon technologies.

Conversely, lower income households face two challenges; first, that they are more finance-constrained; meaning that without subsidies they are less likely to be able to afford the greater up-front cost of these technologies, and find it more difficult to borrow money commercially to do so; second, that low-income households are less likely to be owner-occupiers, and more likely to be in rental or state-provided accommodation. The 'split incentives' challenge associated with these types of tenancy agreements is well explored in the academic literature (Aydin, Eichholtz and Holtermans 2019) (Economidou 2014) (Gillingham, Harding and Rapson 2012), and relates to the fact that in non-owner occupied properties, one party (the landlord) pays for the installation and maintenance of heating technologies, and another (the tenant) pays the ongoing energy costs. There is therefore little cost incentive for the owner to pay for the installation of (more costly) low-carbon technologies since they will not reap the benefits of lower running costs. The end result of this is that such households are less likely to switch to the low-carbon technologies.

Ultimately, what this suggests is that, in terms of income distribution, the impacts of the transition could be very unequal without specific government intervention to address this (e.g. through direct procurement). Without policy support to encourage and facilitate take-up amongst low-income households, the majority of the adopters of these new technologies could be expected to be middle- and high-income households. As Chapter 2 shows, Total system costs faced by consumers are similar in the Reference and Extended scenario, but the higher unsubsidised up-front costs for low-carbon heating technologies could present a major potential barrier to take-up from low-income households unless financial support is suitably deployed to support take-up (as assumed in the Extended scenario).

The question of how the jobs impacts of the transition play out across the income distribution is less clear. The Annual Population Survey gives occupational breakdowns for employment in Scotland by broad industry group in 2017; the key information for relevant sectors is summarised in Table 3.4 below.

| B Mining and quarrying | C Manufacturing | D Electricity, gas, air conditioning supply | Scotland economy-wide average | |

|---|---|---|---|---|

| Skill level 1[3] | 4% | 9% | 0% | 11% |

| Skill level 2 | 21% | 28% | 27% | 36% |

| Skill level 3 | 34% | 39% | 39% | 26% |

| Skill level 4 | 40% | 24% | 33% | 27% |

Source: Office for National Statistics, Annual Population Survey

This suggests that the sectors in which the most prominent changes (both positive and negative) are expected have a relatively large proportion of relatively low-skilled (and therefore likely to be low-income) workers in them. For example, around 74% of workers in the mining & quarrying industry were medium-low (level 3) or low (level 4) skilled in 2017, compared to an economy-wide average of 53%. However, because the proportions are broadly similar across the affected industries (73% in manufacturing, and 72% in electricity and gas supply) it is not clear that shifting employment between these industries will have a substantive impact upon the distribution of household income across Scotland. From the evidence presented here, it appears likely that the direct impacts of changing heating technologies will have a more substantive distributional effect. However, it is important to note that the data above is for broad industries only; the value chains associated with the production of both fossil fuel and low-carbon heating technologies have specific labour requirements which do not necessarily directly match up to these industry 'averages'. A more detailed assessment of the specific occupations and skills needed in the respective value chains could provide further insight into the changing demands that this technology shift is likely to place on the Scottish labour force.

Contact

Email: heatinbuildings@gov.scot