Decarbonising heating - economic impact: report

This report considers the potential economic impacts arising from a shift towards low carbon heating technologies in Scotland, over the period to 2030.

2 The heating technology scenarios

In this chapter we outline how heating demand is met by different technologies in the scenarios, and how that alters modelled consumer investment in heating technologies. The four simulated scenarios cover a reference scenario (reflecting the current policy trajectory), a subsidy scenario (providing financial support to the purchase of low-carbon technologies), a regulation scenario (enforcing the phase out of high-carbon technologies), and an extended scenario which combines (more stringent) subsidy and regulation measures. The full detail of the data/assumption inputs used to construct the scenarios are set out in Appendix C. The modelling approach is set out in Appendix D[1].

2.1 Heating demand by technology

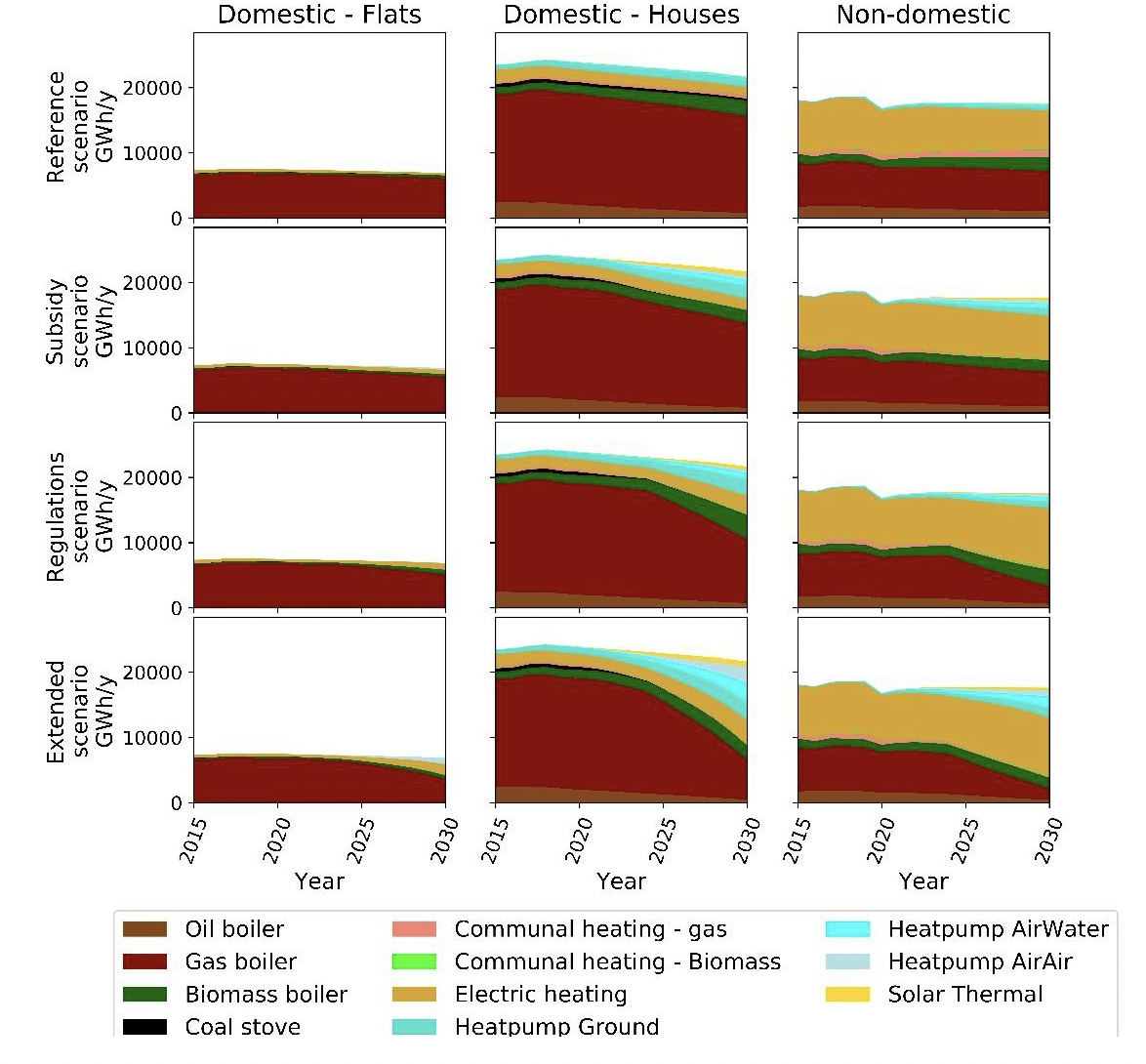

Figure 2.1 illustrates what portion of the useful heat demand is met by the available technologies. Under the influence of the varying policy packages and limitations of specific building types, the way the heating demand is met changes over time. The simulated technology uptake affects final energy use, emissions and expenditure.

Reference scenario

If no additional policies are introduced, our modelling suggests it is very likely that gas-based heating remains dominant in both flats and houses, while non-domestic buildings are heated primarily through electric heating (including electric boilers and electric storage heaters) and gas-based heating. Heat demand projections are a function of new building projections plus assumed efficiency gains. The increase in households, with an assumed constant split between houses and flats over time, leads to an increase in heating demand which is negated by energy efficiency gains in the existing stock. These gains are built on improving the EPC status of all buildings to at least band C by 2035. For non-domestic heating demand, we assume changes in gross value added (GVA) is correlated with changes in the number of non-domestic buildings, whilst a historical decrease in heating demand intensity was continued out to 2030.

Subsidy scenario

Applying subsidies to renewable forms of heating from 2022 onwards incentivises households and firms to move away from fossil-fuelled boilers. Our modelled scenario shows that the heat supply in houses and firms slowly moves away from gas boilers to other technologies, primarily heat pumps. The options for alternative technologies in the heat supply for flats is limited and only minor changes in the take up of technologies in these buildings are simulated by our model. To increase renewable heating in flats, communal forms of heating and heat networks could be deployed. However, these options have not been modelled, since they are regarded to require centralised decision-making while our model captures decisions by individual property owners.

Regulations scenario

In our phase-out regulation scenario, the installation of new fossil-fuelled boilers is banned from 2025 onwards. Consumers are forced to purchase a renewable technology when their boiler reaches the end of its lifetime. The simulated effect of a phase-out regulation differs in each building category. There is a greater uptake of renewable forms of heating in houses and non-domestic buildings. In flats, the effects of a phase-out are limited, primarily due to a lack of suitable alternative technologies.

Extended scenario

Neither subsidies nor regulations alone invoke a large enough change in the heating supply composition to meet the decarbonisation targets (see 0). For that reason, we combined the subsidies and regulations and complemented them with additional policies, such as a procurement scheme, and an increase in biomethane blending. The combined effect of these policies leads to an accelerated uptake of renewable forms of heating. In addition, the biomethane blending reduces the environmental impact of gas boilers.

Emission reductions

Across all domestic and non-domestic buildings, emissions reductions in 2030 of 32.9% (compared to the base year of 1990) are achieved in the Reference scenario, mainly due to improvements in energy efficiency. In the Subsidy and Regulation scenarios, emissions decrease by 44.3% and 58.7% respectively in 2030, compared to 1990 levels. Finally, the Extended scenario achieves a 74.3% decrease in emissions, which is close to the target for 2030. More detail on emission results are provided in Appendix B.

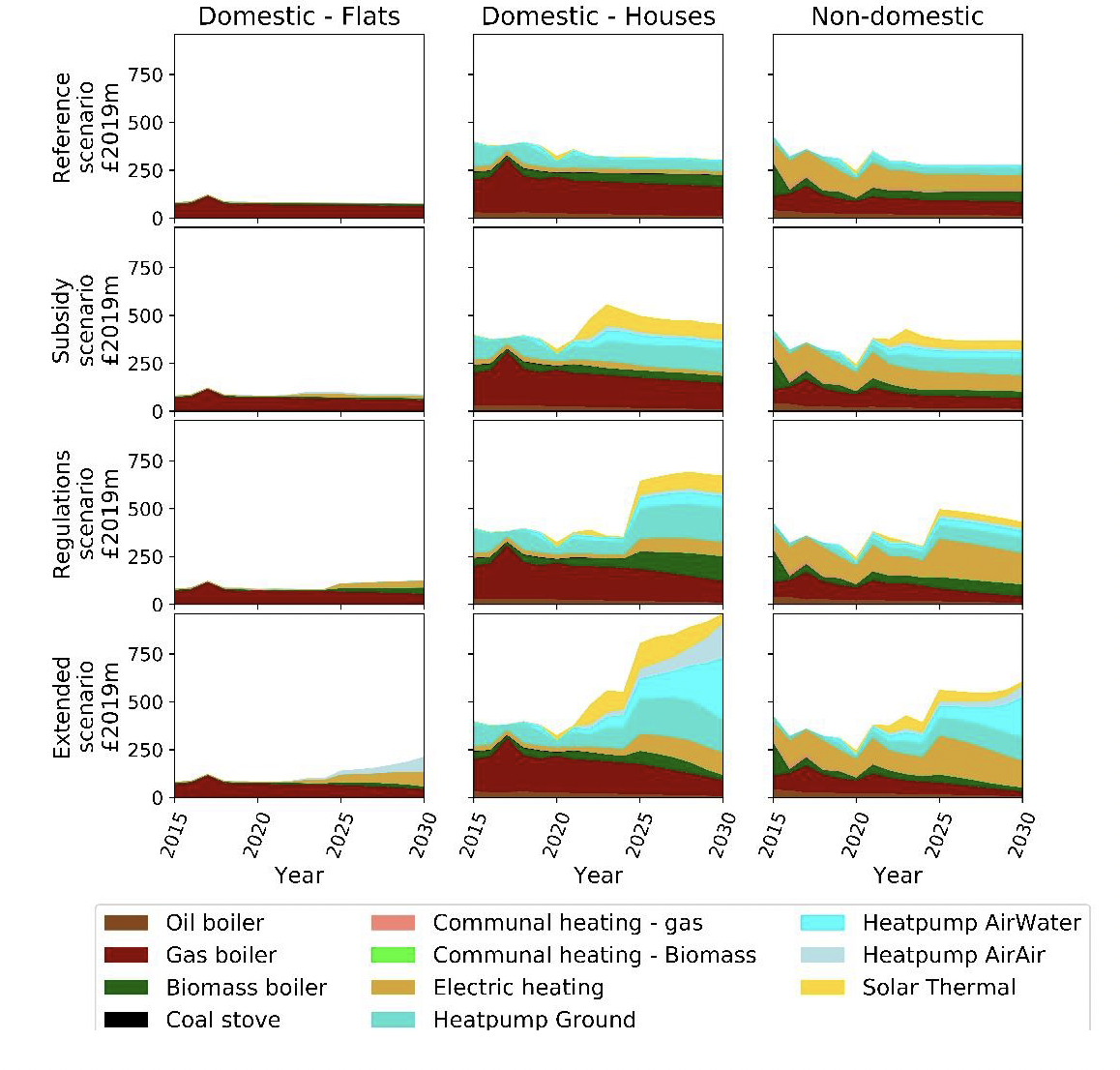

2.2 Investment in new heating technologies

The expenditure profiles for the different building types and scenarios we modelled are set out in Appendix B. Investments occur when households and business need to replace their existing heating unit at the end of its lifetime, or when they replace it prematurely (due to large cost differentials between the operation of existing and new technologies). Modelled scenarios in which more heat pumps are taken up show an increase in upfront costs, because heat pumps are relatively more expensive per unit of heating capacity and more capacity is needed due to climatic conditions to meet peak heat demand. Note that some of these upfront costs are subsidised in the Subsidy and Extended scenarios. Centralised investment in heat networks and/or communal heating could prove to be more cost-effective options in these scenarios but are omitted from the modelling due to the centrally-planned nature of their deployment.

Figure 2.2 shows the investment in heating technology profiles for each of the building types and scenarios. Rapid changes in investment occur in the policy scenarios, because of a shift towards these more expensive (in terms of up-front cost) technologies. In the Regulation scenario expenditure on gas-boilers is displaced to a degree by expenditure in other heating technologies. For flats, no change in expenditure is expected. In the Extended scenario, expenditure is expected to increase 2.5 to 3-fold compared to the Reference scenario due to the high rate of substitution towards heat pumps in houses and non-domestic buildings. Higher expenditure is also seen in flats, due to higher rates of uptake of electric heating.

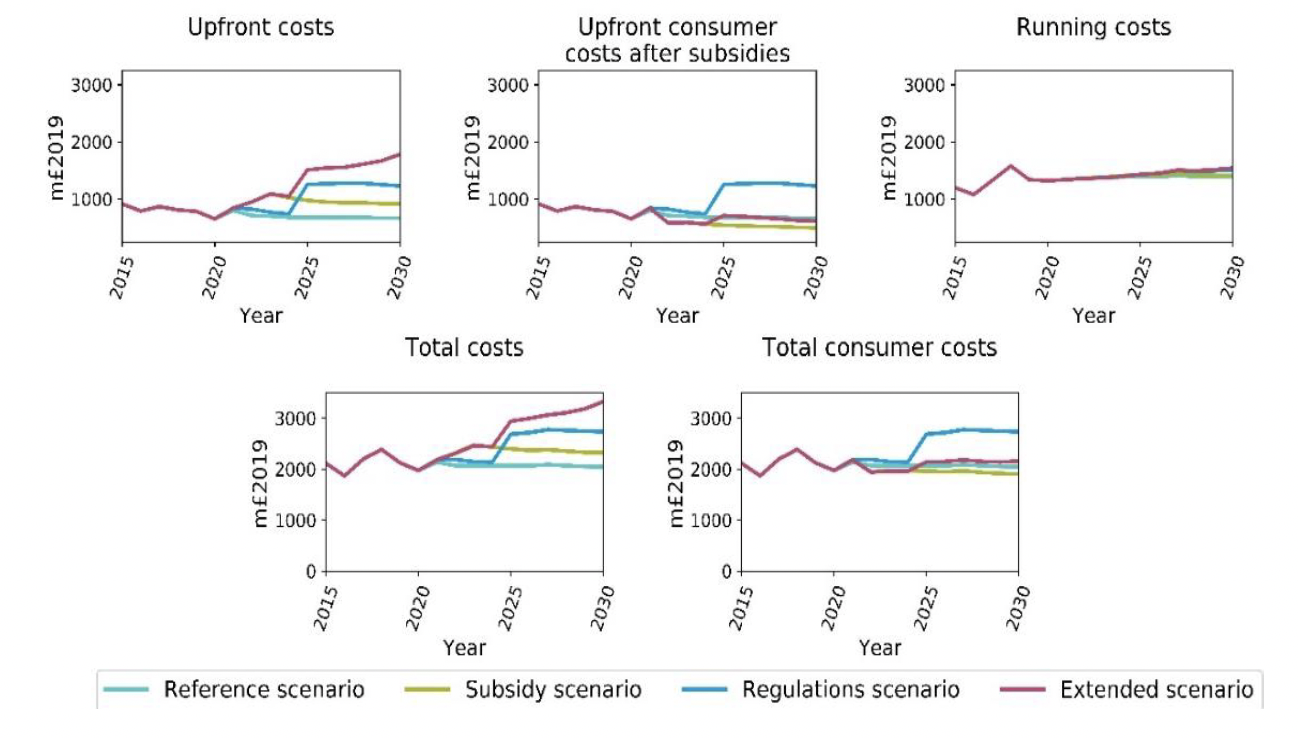

The changing ways in which heating demand is met changes not only upfront costs, but also running costs. Furthermore, maintenance costs differ between boiler types affecting the running costs. Figure 2.3 shows the effects of different scenarios on costs.

When subsidies, regulations, or a combination thereof (plus additional policies) are introduced in the Extended scenario, a much higher take-up of low-carbon technologies is seen, which is associated with higher upfront costs (first panel, top row). However, in the scenarios where subsidies have been implemented (Subsidy and Extended scenarios), some of these costs are not paid by consumers but rather by government (the impacts of which are shown in the second panel, top row). As different heating technologies that use different fuels are adopted, the Total running costs across the system change (third panel, top row). Electrification is largely responsible for increasing running costs, due to the higher prices of electricity relative to gas; this effect outweighs the improved efficiency of heat pumps compared to conventional gas boilers. Combining the upfront costs and the running costs (first panel, bottom row), leads to a £1200m (in 2019 prices) increase in costs.

Lastly, from the second panel in the bottom row, it becomes clear that the subsidies play a key role in ensuring that a low carbon heating does not substantially increase the heating costs faced by consumers. Phase-out regulations force consumers to choose more expensive, but low-carbon options.

Contact

Email: heatinbuildings@gov.scot