Draft Energy Strategy and Just Transition Plan

We are consulting on this draft route map of actions we will take to deliver a flourishing net zero energy system that supplies affordable, resilient and clean energy to Scotland’s workers, households, communities and businesses.

Chapter 3: Energy supply

Scotland will be a renewable powerhouse

By 2030, domestic production of renewable electricity and renewable hydrogen will have increased significantly, helping to address climate change by substantially reducing the emissions of our energy sector. By 2030, the total electricity produced in Scotland over the course of a year will allow us to continue to benefit from exporting electricity and open up the huge opportunities of vast renewable hydrogen production for use in Scotland and for export. This will contribute to economic growth, jobs and investment.

Scotland will be a renewable powerhouse, exporting renewable hydrogen and electricity to support decarbonisation in Europe, as part of an integrated system with the rest of Europe. There will be an additional 20 GW of renewable electricity capacity and 5 GW hydrogen production, as well as substantial growth in marine and solar capacity. Oil and gas in the North Sea is becoming less plentiful and harder to extract. There will be no nuclear power, coal extraction or use of unconventional oil and gas or exploration of onshore conventional oil and gas.

This chapter sets out the scale of the opportunity to transform Scotland's energy supply, with energy increasingly provided from climate-friendly renewable electricity and hydrogen.

To achieve this transformation, we will:

Scale up Renewable Energy

Offshore Wind

We have set out an ambition to have 8-11 GW of installed offshore wind capacity by 2030 and are consulting on setting a further offshore deployment ambition.

We continue to call on the UK Government to devolve the powers necessary to enable us to deliver our ambitions on offshore wind.

We are currently updating our Good Practice Principles for Community Benefit from Offshore Renewable Energy Developments, and will consult on new draft guidance in 2023.

We will revise Scotland's National Marine Plan (NMP) (2015) following the outcome of the earlier (2021) review. This new NMP will update our planning framework and help to facilitate sustainable delivery of offshore renewable energy.

We will use the Sectoral Marine Plan (SMP) Iterative Plan Review to consider and assess new information relating to ScotWind and Innovation and Targeted Oil and Gas Decarbonisation (INTOG), providing an up-to-date evidence base to assist consenting and future planning.

We will deliver up-to-date critical research through the Scottish Marine Energy Research (ScotMER) programme to address key consenting and planning risks with increased funding for projects over the next five years.

Onshore Wind

We will take action to deliver an additional 12 GW of installed onshore wind by 2030, as set out in our Onshore Wind Policy Statement, published in December 2022. This will take us to a total of 20 GW.

We will work with industry to deliver an Onshore Wind Sector Deal in 2023 to ensure we maximise deployment and the economic opportunities that flow from it.

We will ensure that the community energy sector is represented on the forthcoming onshore wind strategic leadership group.

We will convene an expert group, including representatives from industry, agencies and academia. This will provide advice to the Scottish Government on how guidance could be developed to support both our peatland and onshore wind aims.

Wave and Tidal

A draft vision for Marine is set out below, and we are seeking views on this as part of the consultation.

We will support the delivery of the 2021–2025 business plan for Wave Energy Scotland with £18.25 million of investment, and work with stakeholders to explore the longer-term needs of the wave energy sector.

Solar

We are setting out a draft vision for Solar and are seeking views on this, and options for setting a solar deployment ambition, as part of the Strategy and Plan consultation process.

Through the solar vision, we are setting out action to reduce barriers to enable and encourage greater solar deployment.

We are keen to see the number of solar installations offering community benefits increase and continue to encourage the sector to consider what packages of community benefit it can offer communities local to developments, in line with our Good Practice Principles.[44]

Hydro

We will continue to urge the UK Government to provide appropriate market mechanisms for hydro power to ensure the full potential of this sector is realised.

Bioenergy

We are reviewing the potential to scale up domestic biomass supply chains, with the support of a Bioenergy Policy Working Group.

We will develop a strategic framework for the most appropriate use of finite bio-resources, which will be published in a Bioenergy Action Plan.

Hydrogen

We will take forward the actions in our Hydrogen Action Plan, including:

- set out an ambition of 5 GW of renewable and low-carbon hydrogen production by 2030 and 25 GW by 2045.

- £100 million funding towards the development of our hydrogen economy.

We are taking forward a collaborative project with key stakeholders to streamline consenting procedures and reduce consenting timescales.

We will work with key partners to provide targeted support to develop skills programmes and to help people, companies and communities to connect to the opportunities created by the growing hydrogen economy.

Planning and Consenting

We will place climate and nature at the centre of our planning system in line with the Revised National Planning Framework 4, making clear our support for all forms of renewable, low-carbon and zero emission technologies, including transmission and distribution infrastructure.

Economic benefits

In 2023, we will establish a Green Datacentres cluster builder to increase renewable energy adoption by datacentres.

Economic benefits from exporting energy

We are taking forward research into ways of maximising the economic benefits to households, communities and regional economies from Scotland's anticipated low carbon energy surplus.

Reduce our reliance on other energy sources

North Sea Oil and Gas

We are calling on the UK Government to support the fastest possible just transition for the oil and gas sector.

We are calling on the UK Government to take forward a more rigorous package of tests than those recently introduced by the UK Government for the 33rd licensing round to align with global climate goals.

Whilst licensing is reserved to the UK Government, the Scottish Government is consulting on whether, in order to support the fastest possible and most effective just transition, there should be a presumption against new exploration for oil and gas.

To take action to build a skilled, resilient energy workforce of the future, we are supporting reskilling of oil and gas workers through an offshore skills passport as part of our Just Transition Fund.

Our £75m Energy Transition Fund supports five key transition projects in the North East and our £100m Green Jobs Fund provides capital across Scotland to support green industries and the green jobs associated with them.

Our £500m Just Transition Fund will support the North East and Moray to become one of Scotland's centres of excellence for the transition to a net zero economy

We will support Scotland to become a decommissioning centre of excellence. We have announced our intention to invest £9 million in the development of an ultra-deep-water port at Dales Voe, Shetland through the Islands Growth Deal to increase the competitiveness of the decommissioning sector in Scotland.

We urge the UK Government to provide more support directly to the decommissioning sector to ensure as much of this growing area of work as possible is carried out in Scotland, creating and protecting jobs and economic opportunities.

Onshore conventional oil and gas

Ministers confirm a preferred policy position of no support for the exploration or development of onshore conventional oil and gas in Scotland. The relevant statutory and other impact assessments will now be undertaken, and the finalised policy position will be confirmed on conclusion of this process.

Unconventional oil and gas

Ministers have announced their finalised position of no support for unconventional oil and gas.

Coal

Ministers confirm a preferred policy position of no support for coal extraction in Scotland. Impact assessments for this policy will follow a similar approach as outlined above for conventional oil and gas; the finalised policy position will be confirmed on conclusion of this process.

Nuclear

The Scottish Government's position on traditional nuclear energy has not changed. We do not support the building of new nuclear power plants under current technologies.

3.1 – Scaling up renewable energy

Scotland is endowed with vast renewable energy resources including significant offshore wind potential, substantial tidal energy resources and a well-developed onshore wind sector. We will continue to build a diverse renewable energy mix, with significant offshore and onshore wind deployment supported by technologies such as hydro and solar.

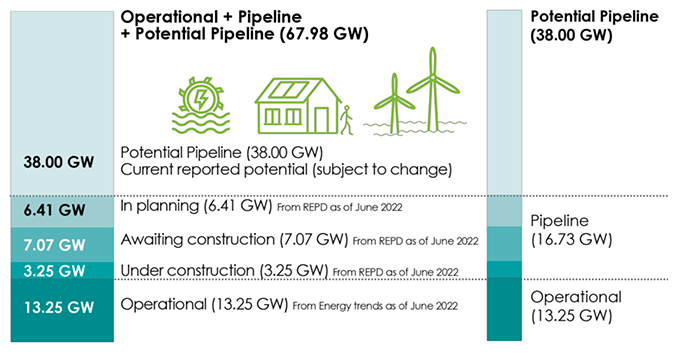

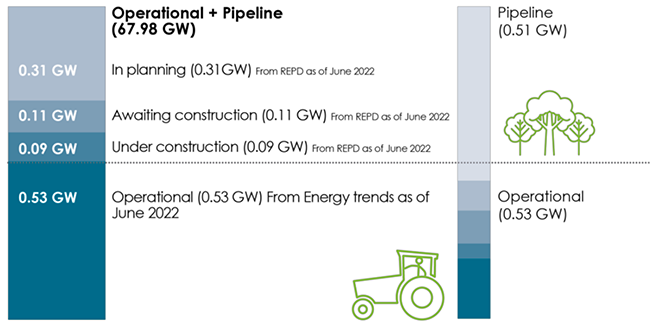

Increasing levels of home-grown renewable supply will make energy more affordable and ensure it is always available when we need it. Alongside investment in electricity networks and flexible responsive technologies, such as storage and smart appliances, our boosted renewables sector will support the continued and rapid decarbonisation of energy use across Scotland's economy, including expansion in electricity demand. Figure 14 shows Scotland's renewable electricity capacity (operational, pipeline and potential).

Source: REPD and Energy Trends (June 2022)

Maximising benefits to communities and regions

The Scottish Government has an ambition of 2 GW of community and locally owned renewable energy by 2030. Community and shared ownership of renewables have a key role to play in helping communities across Scotland gain maximum benefit from the transition, and form an important source of revenue that can be directly invested back into the local community.

As set out in Chapter 2, we are encouraging developers to offer community benefits and shared ownership opportunities as standard on all new renewable energy projects – including repowering and extensions to existing projects.

Maximising benefits to our economy, businesses and workers

Overall, we are a net-exporter of electricity and Scotland's abundant supply of renewable generation exceeds Scottish demand. This presents significant opportunities for businesses and communities in Scotland, in terms of economic growth, expansion of the supply chain and employment in high-quality, green jobs. Scotland has the potential to be a powerhouse for renewable electricity and renewable hydrogen for Europe, exporting clean electricity as part of an integrated system with the rest of Europe, and supporting decarbonisation of industry across the continent. The significant increase in installed capacity of renewable generation over the coming decade could mean Scotland's annual electricity generation is more than double Scotland's demand by 2030, and more than treble by 2045. This will enable Scotland to meet a large proportion of our demand through renewables alone, while still creating an export opportunity for our surplus[45]. We are taking forward research into ways of maximising the economic benefits to households, communities and regional economies from this anticipated surplus. The expansion in renewables offers wider opportunities to the Scottish economy. An example of this is the linking of Scotland's datacentre industry with sources of renewable energy. The Scottish Government's Green Datacentres and Digital Connectivity Vision and Action Plan[46] sets out how we can position Scotland as a leading zero-carbon, cost competitive, green data hosting location. In 2023, we will establish a Green Datacentres cluster builder to increase renewable energy adoption by datacentres.

3.1.1- Offshore wind

Photo credit: Highlands and Islands Enterprise

As set out in the Offshore Wind Policy Statement, published in 2020, the Scottish Government currently has an ambition to achieve up to 8-11 GW of offshore wind in Scottish waters by 2030.

We recognise that this now needs to be reviewed in light of the market ambition expressed in response to the ScotWind leasing round and the associated economic, social, net zero and energy security benefits which could be delivered for Scotland.

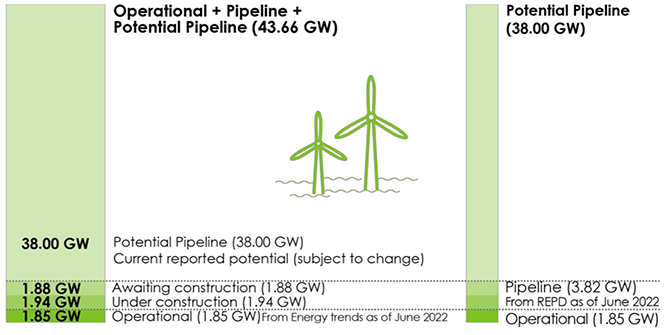

As of June 2022, Scotland has 1.9 GW of operational offshore wind. In the pipeline there is 3.8 GW of projects consented or under construction[47], and 4.2 GW of projects with lease options[48] ahead of the ScotWind leasing round results. Furthermore, the upcoming Innovation and Targeted Oil and Gas Decarbonisation (INTOG) leasing round will enable up to 5.7 GW of new offshore wind projects targeting oil and gas decarbonisation[49], and up to 0.5 GW of innovation projects[50]. Figure 15 shows Scotland's offshore wind capacity (operational, pipeline and potential pipeline).

The results of the ScotWind leasing round, published by Crown Estate Scotland in January last year, reflect market ambitions which exceed our current planning assumptions - with lease options signed by developers for a combined total of 27.6 GW.

Source: REPD and Energy Trends June 2022[51]

The UK Government has also set a target to reach 50 GW of offshore wind by 2030[52], including 5 GW of floating offshore wind. This is part of a further UK Government target to generate 95% of all electricity from low-carbon sources and the Climate Change Committee has projected that significantly more offshore wind will be required to achieve net zero across the UK by 2050[53]. Wind energy is now one of the cheapest forms of energy, and Scotland's offshore wind sector has the opportunity to be at the heart of the UK's energy transition.

However, as part of our just transition to a net zero energy system, the Scottish Government recognises that the major expansion in offshore wind projects required to achieve our net zero and energy security goals will have impacts on marine biodiversity and other users of the sea. The volume of development that can be consented will depend on what is feasible within the bounds of environmental protection regulation, as well as other factors, such as what is technologically achievable within the natural geography of Scotland's seas.

These aspects, together with the need to fully consider the views of stakeholders about impact, mean that at present, whilst that work is underway, it is not possible to know now exactly what scale of development from offshore wind projects will ultimately be permitted or desirable. In addition, other factors which may shape the pace and scale of development include the time required for developments to be connected to the National Grid and the capacity of the supply chain to service a major step change in construction. However, there is no doubt that there is significant potential for the generation of electricity surplus to our domestic needs.

The current seabed leasing allocations are considered sufficient to meet our short-term ambitions, though we remain open to reviewing scope for future leasing opportunities should evidence become available which suggests this is necessary to support the sustainable growth of the Scottish offshore wind sector.

The Iterative Plan Review (IPR) process of the Sectoral Marine Plan for Offshore Wind Energy will take place in 2023. We will have a clearer picture once this review has concluded of the scale of offshore wind development which on current evidence will likely be permitted.

We are pressing the UK Government's Department for Business, Energy and Industrial Strategy (BEIS) and the Department for Environment, Food and Rural Affairs (DEFRA), for reforms to the habitats regulatory regime, through the UK Energy Bill, which will work for Scotland. These reforms are needed to enable a strategic approach to addressing the impact on marine habitats which will deliver gains to biodiversity and help facilitate the expansion of offshore wind in Scottish waters. This is vital to ensure that there is a streamlined and coherent regime in place that can secure sufficient environmental compensation to make projects consentable.

Maximising benefits to our economy, businesses and workers

ScotWind will deliver over £750 million in revenues for these initial awards alone. Once operational, the projects will raise billions more in annual rental revenues, which will be invested back into Scotland, benefitting our communities and our economy.

We welcome the commitments from developers to invest an average of £1.4 billion in the Scottish supply chain across the 20 ScotWind projects. This equates to £28 billion of potential Scottish economic activity, and around £1 billion of investment for every gigawatt of capacity built.

Independent research carried out for the Scottish Trades Union Congress (STUC) shows that Scotwind could add between 2,500-14,400 full time equivalent (FTE) employment[54]. There are also significant opportunities for the Scottish supply chain from our offshore wind potential. Our Sectoral Marine Plan will set the course for this delivery, maximising deployment in Scottish waters whilst protecting marine users and our environment.

In 2021, the Scottish Offshore Wind Energy Council (SOWEC), published its Strategic Infrastructure Assessment (SIA) for Offshore Wind. As the SIA made clear, the sector must now come together and work collaboratively, both to help focus activity and investment in Scottish ports, and to facilitate more meaningful engagement between Scottish suppliers and tier one manufacturers and installers.

SOWEC has developed a Collaborative Framework Charter which encourages developers, the public sector and the supply chain to work together to maximise deployment of offshore wind projects and supply chain opportunities. The Collaborative Framework Charter was launched by the First Minister in May 2022 and has been signed by 24 offshore wind developers. In committing to the Collaborative Framework, developers, while noting the need to make bilateral arrangements with suppliers on a project specific basis, recognise that there is also a role for coordinated, collaborative, strategic investment.

The Scottish Government has been engaging with SOWEC's Collaborative Framework Working Group - alongside all active offshore wind developers in Scotland, enterprise agencies and ORE Catapult - to develop a Strategic Investment Model to facilitate timely, strategic investment through the pooling/sharing and coordination of public and private sector funds.

The Strategic Investment Model is expected to be announced in early 2023.

The DeepWind Cluster, coordinated by Highlands and Islands Enterprise, brings together partners from industry, academia and the public sector, and aims to deliver new offshore wind supply chain opportunities to the north of Scotland. DeepWind will focus on deep water fixed bottom offshore wind technologies and will also act as the lead cluster for floating offshore wind in the UK.

Maximising benefits to communities and regions

Offshore wind is one of the lowest cost forms of electricity, representing good value for money for consumers[55].

We are currently updating our Good Practice Principles for Community Benefit from Offshore Renewable Energy Developments, and will consult on new draft guidance in 2023. We will also use the consultation to build on our evidence base and explore the potential for shared ownership of offshore renewable energy.

Maximising benefits to climate and the environment

We recognise the potential impacts on marine biodiversity arising from the major expansion in offshore wind required to achieve our common net zero goals. We commit to working together in a way that recognises this reality and ensures appropriate protection of our natural environment, as part of our joined up approach to tackling the climate and nature crises.

We will revise Scotland's National Marine Plan (2015) following the outcome of the earlier (2021) review. This new NMP will update our planning framework and help to facilitate sustainable delivery of offshore renewable energy.We will use the SMP (Sectoral Marine Plan) Iterative Plan Review to consider and assess new information relating to ScotWind and Innovation and Targeted Oil and Gas Decarbonisation (INTOG), providing an up-to-date evidence base to assist consenting and future planning.

We will deliver up-to-date critical research through the Scottish Marine Energy Research (ScotMER) programme to address key consenting and planning risks with increased funding for projects over the next five years.

In line with our vision for a Blue Economy approach in Scotland, we are committed to ensuring that we balance our decision making around offshore wind development by considering the sustainability of delivering what is required to achieve our common net zero goals. The second National Marine Plan will be the statutory platform for achieving the desired outcomes.

3.1.2 - Onshore wind

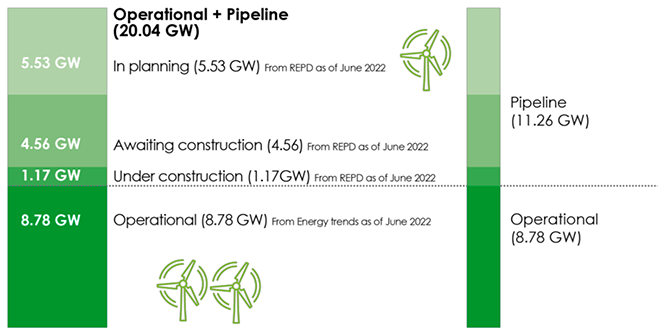

Scotland is leading the way on onshore wind deployment and support at a UK level. We have set an ambition for an additional 12 GW of onshore wind, a total of 20 GW of installed onshore wind by 2030, more than doubling our existing capacity. Figure 16 shows Scotland's current onshore wind capacity (operational and pipeline).

Source: REPD and Energy Trends June 2022

Our recently published Onshore Wind Policy Statement sets out detailed actions to deliver that ambition, including the commitment to a sector deal in 2023 which will seek to maximise supply chain and community benefit opportunities.

Scotland will embrace the opportunity to increase onshore wind capacity through turbine improvements. Taller and more efficient turbines can be deployed at both new developments and when considering the repowering of existing sites, providing significantly increased capacity, often without increasing the footprint of an existing site. There are also substantial opportunities associated with repowering onshore wind farms as they come to the end of their lives.

Maximising benefits to our economy, businesses and workers

We will work with industry to deliver an Onshore Wind Sector Deal in 2023, to ensure we maximise deployment and the economic opportunities that flow from it. We continue to support the Scottish supply chain and recognise the particular opportunities in the onshore market, for example in operation and maintenance and decommissioning of sites.

Maximising benefits to communities and regions

Our Onshore Wind Policy Statement restates our clear position on community engagement, community benefit and shared ownership, including consideration of how communities might benefit from repowering opportunities. We will ensure that the community energy sector is represented on the forthcoming Onshore Wind Strategic Leadership Group.

Maximising benefits to climate and the environment

We are clear on the need to focus on planning and environmental assessment, and to work with developers and consultees to address the nature crisis as we deploy greater volumes of onshore wind.

We recognise, however, that the peatland impacts of onshore wind farms can be significant and we must balance the benefits from onshore wind deployment and the impacts on our carbon rich habitats. This includes being aware that there is potential for development in an area of deep peat to have a net negative carbon impact. We therefore commit to the following actions:

- We will convene an expert group, including representatives from industry, agencies and academia. This will provide advice to the Scottish Government on how guidance could be developed to support both our peatland and onshore wind aims.

- Work is underway to assess the operation of, and if necessary update or replace, the carbon calculator. The Scottish Government will ensure that adequate tools and guidance are available to inform the assessment of net carbon impacts of development proposals on peatlands and other carbon-rich soils.

3.1.3 - Marine energy (wave and tidal)

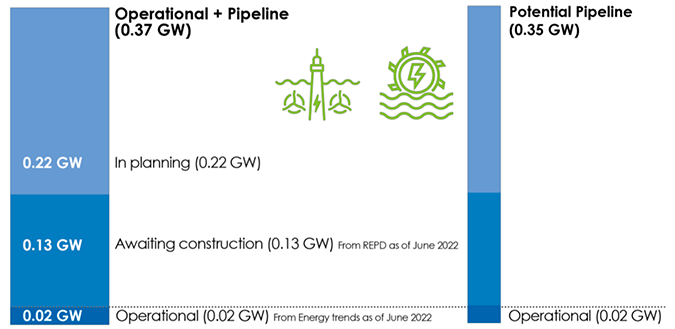

Wave and tidal stream energy are two distinct but related technologies which, as part of a diverse renewable energy mix, can support Scotland's transition to a net zero emissions economy. Figures from BEIS show that there is 22 MW of shoreline wave and tidal electricity generation operational in Scotland. Of this, there are four main live tidal projects with a combined capacity of around 10 MW. New developments have the potential to quadruple this installed capacity to around 40 MW in Scottish waters by 2027. Figure 17 shows Scotland's shoreline wave/tidal capacity (operational and pipeline).

Tidal energy is highly predictable and can complement intermittent sources of energy, smoothing the overall power supply from renewables. The generation profile of wave energy is out of phase with other renewable sources such as offshore wind, giving it the ability to provide a grid balancing function.

A draft vision for marine energy is presented in Annex G, and views are being sought as part of this consultation. The marine energy vision statement will be published as part of the final Energy Strategy and Just Transition Plan in 2023.

Draft vision for marine energy

Wave and tidal energy has the potential to support the delivery of a secure and low carbon energy system while providing a new industrial opportunity and being part of Scotland's response to the global climate emergency. The predictability and availability of the marine energy resource off Scotland's coastline, together with Scotland's early lead in the technology, provides an opportunity to build on Scotland's maritime heritage and to secure a substantial share of the emerging global market for marine energy.

Source: REPD and Energy Trends 2022

Maximising benefits to our economy, businesses and workers

Scotland is a pioneer in both tidal and wave energy, being home to some of the world's first, largest and most advanced tidal stream deployments, as well as our internationally-renowned Wave Energy Scotland programme. Scottish firms have already exported their technology and expertise, with projects in Japan and Canada. A recent independent report by the Scottish Marine Energy Industry Working Group highlights the scale of the opportunity from wave and tidal energy supply chains in Europe and the UK, the latter totalling between £4.9 billion and £8.9 billion GVA by 2050. Scotland's early lead can give it a first-mover advantage, particularly as Scotland has significant transferrable expertise and facilities from industries such as fisheries, offshore wind, oil and gas, shipbuilding and ports and harbours.

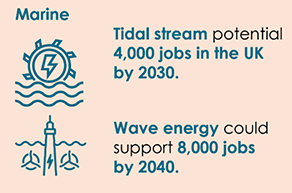

The Offshore Renewable Energy Catapult (ORE Catapult) has estimated that the tidal stream industry has the potential to support almost 4,000 jobs in the UK by 2030, while wave energy could support more than 8,000 jobs in the UK by 2040.

Organisations such as the International Renewable Energy Agency (IRENA) have identified the enormous global potential of marine energy. This includes opportunities for island nations and remote coastal areas due to factors such as land restrictions, the availability of natural resources, the need to transition away from imported oil or diesel for power production, and the requirement for desalination plants. Industry analysis, published in Ocean Energy Europe's 2030 Ocean Energy Vision report, states that 1.3 GW to 2.4 GW of installed capacity from tidal energy could be deployed worldwide by 2030 and potentially more than 100 GW by 2050.

We will continue to support the delivery of the current five year business plan for Wave Energy Scotland and work with stakeholders to explore the longer-term needs of the wave energy sector.

Case study: European Marine Energy Centre (EMEC)

Photo credit: Orkney Sky Cam, courtesy of EMEC

EMEC is an innovation catalyst pioneering the transition to a low carbon future. Celebrating its 20th anniversary in 2023, EMEC is the world's leading centre for demonstrating wave and tidal energy converters in the sea. EMEC has been a catalyst for economic development, creating jobs and a world leading supply chain now exporting skills and knowledge around the globe. EMEC analysis reports this added £306 million GVA to the UK economy between 2003 and 2019.

Maximising benefits to climate and the environment

We recognise the potential impacts on marine biodiversity arising from the major expansion in offshore renewables required to achieve our common net zero goals. We commit to working together in a way that recognises this reality and ensures appropriate protection of our natural environment, as part of our joined up approach to tackling the climate and nature crises.

3.1.4 - Solar energy

Solar has an important role to play in decarbonising our energy system, particularly when combined with other renewables. Our aim is to maximise the contribution solar can make to a just, inclusive, transition to net zero. We will support the sector to minimise barriers to deployment wherever possible and continue to provide support through our renewable support schemes.

Solar is a long established, commercially viable renewable technology that has been at the forefront of decarbonisation efforts. It has seen great success in Scotland and we wish to provide clarity as to the important role it will play in meeting net zero, which is why we are consulting on a draft vision as part of this ESJTP consultation and seeking evidence from a wide range of stakeholders in order to finalise the vision in 2023. We continue to make considerable progress in lowering barriers that are within Scottish Government competence, to facilitate greater deployment of solar. We will continue to work closely with industry to enable solutions for the sector.

Photo credit: Eigg Electric

We see a strong role for solar thermal, as well as domestic and commercial solar PV combined with battery storage systems, which have the potential to help reduce consumer bills.

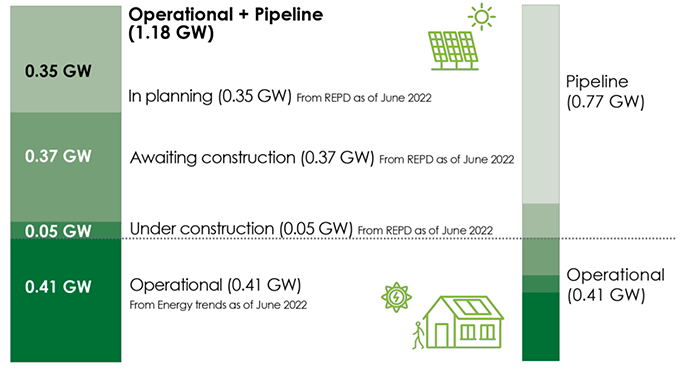

Scotland has 411 MW of operational solar capacity, with a further 767 MW of estimated pipeline capacity[56]. This pipeline of projects, which increases the current capacity by over 150%, shows the significant appetite for greater solar deployment in Scotland. Figure 18 shows Scotland's Solar PV capacity (operational and pipeline).

Independent evidence suggests that costs for solar have reduced by 60% since 2010 [57]with support also provided through UK Government schemes. Scottish Government funding is therefore focused on domestic and non-domestic projects, through a comprehensive range of support schemes for renewable and energy efficiency technologies (See Annex F).

A draft vision for solar energy in Scotland is presented in Annex G. The draft vision sets out the actions we will take to further deployment of solar, and views are being sought as part of this consultation. We are considering the evidence for setting a solar deployment ambition and are consulting on it through this draft vision. We will provide an updated position in our final solar vision in 2023.

Source: REPD and Energy Trends 2022

Maximising benefits to our economy, businesses and workers

On 1 April 2022, we expanded eligibility for the Business Growth Accelerator relief to include solar panels as a qualifying improvement eligible for relief for 12 months after installation.

We provide up to 100% Non-Domestic Rates relief to renewable energy generators, including solar, who provide community benefit. We are keen to see the number of solar installations offering community benefits increase and continue to encourage the sector to consider what packages of community benefit it can offer.

We will introduce a non-domestic rates exemption for plant and machinery used in onsite renewable energy generation and storage, including solar, from 1 April 2023.

We are aware there are pockets of skills gaps across some parts of Scotland for installation and maintenance of solar PV, and we will explore this further with industry. Our Climate Emergency Skills Action Plan provides the framework for creating and supporting the workforce in the transition to net zero and will reflect sector specific skills such as these when it is updated in 2023.

Maximising benefits to climate and the environment

We are engaging with stakeholders on the case that future rural support payments might be eligible on land used for solar installations that is also explicitly being used to deliver our Vision for Scottish Agriculture. In the present Common Agricultural Policy model, support cannot be claimed for this type of dual use. Notwithstanding the outcome of this, we will seek to encourage high biodiversity standards on solar farms.

3.1.5 - Hydro power

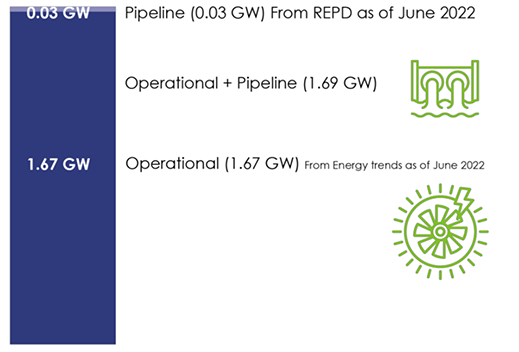

Scotland has a proud history of hydro power and currently has 1.7 GW operational[58], which accounts for 88% of total UK hydro power capacity. There is an additional pipeline totalling 26 MW (excluding pumped hydro storage). Projects vary significantly in size, power output and geography. Figure 19 shows Scotland's hydro capacity (operational and pipeline).

Hydro power has the potential to play a significantly greater role in the energy transition – both at small-scale in co-operation with local communities as part of a diverse resilient energy supply in remote parts of Scotland, and at larger scale, providing flexibility services to the grid and helping to ensure a continued resilient and secure electricity supply.

However, whilst hydro power is a reliable source of renewable electricity, there are a number of challenges in developing new hydro power projects in Scotland. We urge the UK Government to provide appropriate market mechanisms for hydro power to ensure the full potential of this sector is realised. See Chapter 5 for more detail on the crucial role of pumped hydro in system level storage and security.

Source: REPD and Energy Trends 2022

Case study: Community hydro power as part of a diverse energy mix in off- electricity grid areas

Photo Credit: Knoydart Renewables

In 1999 the Knoydart Foundation bought 17,500 acres of the remote off-grid Knoydart Peninsula on behalf of the community. Over the last two decades, the community, supported by the Scottish Government (CARES), HIE, SSE and the Foundation, have refurbished the turbine, repaired the leaking dam, replaced a corroded penstock, generator, transformers, governor, control panels and begun to underground vulnerable overhead power lines. This valuable investment has helped enable the community to transition from a system that regularly needed to use back up diesel generation to a reliable system fit to supply zero-carbon electricity to the Knoydart Community until nearly the end of the century.

3.1.6 - Bioenergy

Our aim is to see bioenergy used only where it can best support Scotland's journey towards net zero. In the short- to medium-term, bioenergy should only be used where it can be most effective in reducing emissions and where there is greatest need for alternatives to fossil fuels. In the longer-term, we want to encourage the use of bioenergy with carbon capture technology where possible. Decisions over use of bioenergy should also align with and support Scotland's goals for protecting and restoring nature. Figure 20 shows Scotland's bioenergy and waste capacity (operational and pipeline).

Source: REPD and Energy Trends 2022

We have put in place an internal Scottish Government Bioenergy Policy Working Group, which is looking at the overall goals and priorities for bioenergy use in the short, medium and long term. The availability of land and competing priorities, such as woodland creation, peatland restoration, biodiversity regeneration, food and fodder production is a key consideration in the future of bioenergy production.

The work of the Bioenergy Policy Working Group will inform the development of a strategic framework for the most appropriate use of finite bio-resources, which will be published in a draft Bioenergy Action Plan for consultation.

3.1.7 - Hydrogen

As set out in our Hydrogen Action Plan,[59] our vision is for Scotland to become a leading Hydrogen Nation with an ambition to produce 5 GW of renewable and low carbon hydrogen by 2030, and 25 GW by 2045. A thriving hydrogen economy in Scotland will support domestic decarbonisation goals, our domestic supply chain capability and secure and create new jobs as part of the just transition. It will also help support the decarbonisation of other nations through the export from Scotland of renewable hydrogen, skills and expertise.

The European Commission's REPowerEU Plan sets a target of 10 million tonnes of domestic renewable hydrogen production and 10 million tonnes of renewable hydrogen imports by 2030. Scotland is well-placed to service future export markets for hydrogen and hydrogen derivatives at scale, by producing hydrogen powered by renewable electricity.

Hydrogen and hydrogen derivatives will help decarbonise sectors which are difficult to electrify and will create further economic opportunities for communities across Scotland. Hydrogen could also play a useful role in delivering large-scale and long-term energy storage in an integrated energy system and has the potential to replace or augment the critical balancing and resilience services that natural gas storage provides to the energy system today. See Chapter 5 for more on energy security.

Our plans to accelerate the hydrogen economy in Scotland will require the Scottish Government and its agencies, working with industry and with the UK Government, to apply both devolved and reserved powers in alignment.

Maximising benefits to our economy, businesses and workers

The growth of the hydrogen economy is dependent on supply and demand developing in concert, as well as the enabling infrastructure required to produce, store and distribute the hydrogen products. Key to this are supportive policies and the establishment of investment and incentives to enable the growth of supply, demand and infrastructure, including the £100 million in capital funding for renewable hydrogen projects from our Emerging Energy Technologies Fund, which will complement UK Government funding and regulatory and market frameworks.

As is outlined in our Hydrogen Action Plan, we will work with key partners to provide targeted support to develop hydrogen production and supply chain capability, and the skills programmes to help individuals, companies and communities to connect to the opportunities created by the growing hydrogen economy.

Economic impact estimates based on scenarios developed for the Scottish Government indicate the development of a hydrogen economy in Scotland could mean between 70,000 and over 300,000 jobs could be protected or created with potential GVA (Gross Value Added) impacts of between £5 billion and £25 billion a year by 2045 depending on the scale of production and the extent of exports.[60]

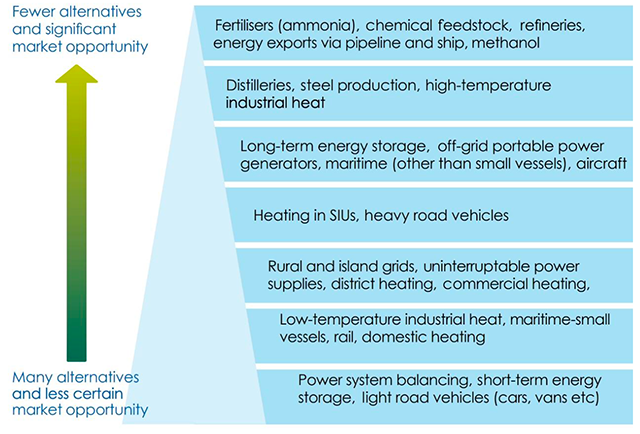

While the nature of hydrogen as an energy vector means that it can theoretically be used across many sectors of the economy, some sectors are more likely than others to adopt hydrogen as an optimal solution. The likeliness of hydrogen being adopted will depend on technical parameters such as efficiency, availability of alternatives. Other regional factors such as resource availability or available infrastructure will be of importance on a case-by-case basis. The potential uses of hydrogen are explored in greater detail in the Hydrogen Action Plan.

A hierarchy of uses is presented below [Figure 21]. This is based on our current understanding of the sector and provides our view of some of the hydrogen uses that are more or less likely to develop, based on current alternatives and available opportunities. This has been produced by considering a range of influencing factors such as economic, technical and logistical issues and will be taken into account as part of our considerations as we design support for the transition to a net zero economy.

Source: Hydrogen Action Plan (2022)

The UK Government must accelerate decisions affecting the growth of the hydrogen economy including: the introduction of hydrogen business models to support production, hydrogen certification and standards, and the regulatory and market support mechanisms required to enable infrastructure development for the offshore transportation of renewable hydrogen from Scotland's ports and harbours. It is important that the supporting market and regulatory frameworks and strategic planning to guide the rollout of hydrogen transport and storage infrastructure is introduced quickly and considers both the onshore and offshore transportation of hydrogen in parallel.

Hydrogen will provide a decarbonisation solution for some parts of the transport sector and for energy-intensive industry, switching to renewable and low-carbon hydrogen is considered one of the few viable options for significant decarbonisation in the next decade. Low-carbon hydrogen production should also achieve the highest technically possible emissions capture rates. See Chapter 4 for more details, and for detail on the role of hydrogen for heat in buildings.

The Hydrogen Action Plan sets out our support for the development of both renewable and low-carbon hydrogen with an ambition of 5 GW of renewable and low-carbon hydrogen production by 2030 and 25 GW by 2045. We expect the majority of our 5 GW ambition by 2030 to come from renewables.

We wish to see as much renewable hydrogen in our energy system as quickly as possible. In addition to renewable and low-carbon hydrogen production and use, we also support the development of biomass gasification with carbon capture and storage for the production of negative emissions hydrogen.

The Scottish Government does not support new hydrogen production where CO2 is unabated. We encourage industry to transition as quickly as possible away from production and use of unabated hydrogen and achieve the lowest possible emissions rates as part of their decarbonisation planning. We will not support via Scottish Government funding the development of new, industrial development where carbon emissions are unabated. Such development will require to demonstrate the implementation of a decarbonisation strategy at point of operation. This could include fuel switching, carbon capture, and energy efficiency and must be in line with our statutory climate change targets.

Maximising benefits to communities and regions

The growth of a strong hydrogen sector offers significant opportunities for regional and local economic benefit, creating new high-quality green jobs in our rural communities, islands and cities, and new opportunities for those currently working in high carbon sectors.

We are actively supporting the creation of Regional Hydrogen Energy Hubs that are host to the entire value chain from production, storage and distribution to end use. The Hubs include multiple end-users with applications covering more than one sector.

Hydrogen will play a key role in decarbonising our industrial clusters, supporting the just transition of the workforce in high carbon sectors in the North East of Scotland, and provide opportunities for our islands and rural communities to maximise the benefit of their vast access to renewable resources. Some Hubs are already producing renewable hydrogen and supporting demand for hydrogen fuels, e.g. Aberdeen and Orkney, while others are in development. The Aberdeen Hydrogen Hub is being taken forward as a joint venture between Aberdeen City Council and BP with £15 million of support from the Scottish Government.

3.2 - Reducing our reliance on other energy sources

We want to ensure the fastest possible just transition from dependence on a fossil fuel energy system to one that maximises the value we obtain from Scotland's rich and varied renewable energy resource. We are clear that unlimited extraction of fossil fuels is not compatible with our climate ambitions and will not resolve the challenges of energy cost or energy security.

We will continue to decarbonise Scotland's power sector. Electricity generation in Scotland is transitioning away from large, centralised fossil fuel power stations to more widely dispersed, smaller renewable generators. However, emissions still remain in combined cycle gas turbine generation, diesel back-up stations in islands locations, North Sea exploration and extraction, and refinement of oil and gas. We will continue to make progress in removing these emissions.

We are opposed to the continued use of unabated fossil fuels to generate electricity. The deployment of CCUS for the Scottish Cluster must demonstrate decarbonisation at pace and cannot be used to justify unsustainable levels of fossil fuel extraction or impede Scotland's just transition to net zero.

In alignment with NPF4, we encourage, promote and facilitate all forms of renewable energy development onshore and offshore. This includes energy generation, storage, new and replacement transmission and distribution infrastructure and emerging low-carbon and zero emissions technologies, including hydrogen and carbon capture utilisation and storage (CCUS).

Some Islands communities rely on carbon intensive diesel generation as a backup in the event of an extended cable fault. These arrangements for securing supplies are not compatible with the transition to net zero, as diesel generation is carbon intensive, costly to operate and sometimes needs to operate for long periods while islands are disconnected from the mainland. In situations such as these, local renewables may need to be turned off to ensure the network operates within safety parameters. There is an opportunity to explore solutions for these situations and we will work to understand more about this ahead of the final Strategy and Plan

3.2.1 - Onshore conventional oil and gas

In line with statutory requirements, the Scottish Government is developing a policy position for onshore conventional oil and gas. On 21 June 2022, we published a call for evidence seeking views on the future of onshore conventional oil and gas in Scotland; the responses to this call for evidence have been independently analysed and considered by Ministers alongside wider policy on energy and climate targets. This has allowed Ministers to confirm a preferred policy position of no support for the exploration or development of onshore conventional oil and gas in Scotland.

3.2.2 - Onshore unconventional oil and gas

In October 2019, Scottish Ministers announced their finalised position of no support for unconventional oil and gas. Following a comprehensive evidence-gathering and public consultation exercise and the required statutory and other assessments, Scottish Ministers concluded that the development of onshore unconventional oil and gas is incompatible with our policies on climate change, energy transition and the decarbonisation of our economy.

3.2.3 - Coal extraction

In line with statutory requirements, the Scottish Government is developing a policy position for coal extraction in Scotland. On 21 June 2022, we published a call for evidence seeking views on this matter; the responses to this call for evidence have been independently analysed and considered by Ministers alongside wider policy on energy and climate targets. This has allowed Ministers to confirm a preferred policy position of no support for coal extraction in Scotland. Impact assessments for this policy will follow a similar approach as outlined above for conventional oil and gas; the finalised policy position will be confirmed on conclusion of this process.

3.2.4 - Nuclear

The Scottish Government's position on traditional nuclear energy has not changed. We do not support the building of new nuclear power plants under current technologies. Existing nuclear is expensive: under the current contract awarded by the UK Government to Hinkley Point C, the electricity that will be generated will be priced at £92.50 per megawatt hour, whereas the electricity being generated from offshore wind is currently priced at £37.65[61] per megawatt hour. In addition, the UK Government recently announced plans to take forward a £700 million stake in the new reactor of Sizewell C. That investment of £700 million could insulate and significantly improve the energy efficiency of approximately 200,000 homes[62]. The construction of new nuclear plant will do nothing to alleviate the current energy price crisis, as nuclear power stations take years, if not decades to build. Indeed, support for nuclear risks pushing bills even higher in the near- to medium-term.

Whilst there is increasing interest in the development of small modular reactors, or SMRs, these use the same nuclear fission technology as the power generating process found in larger traditional nuclear power plants and carry the same environmental concerns.

We are also aware of increasing interest in the development of fusion energy – which is different from traditional nuclear fission energy. However, we are clear that there is a long way to go in terms of fully understanding both the risks and opportunities that fusion energy technology presents. Any request to build a fusion energy plant in Scotland will require the consent of Scottish Ministers and will be assessed on safety, environmental concerns, cost and the contribution to Scotland's low carbon energy future.

3.2.5 - North Sea oil and gas

Scotland's North Sea Oil and Gas sector has provided highly skilled and valuable employment, income and supply chain activity, since the 1970s. The revenues generated by North Sea Oil and Gas have made a significant contribution to UK finances for more than 50 years.

This draft Strategy provides focus on energy usage and supply up to 2030 and how the transformation of our energy system will help to decarbonise our economy and society, and meet Scotland's net zero targets in 2045. In considering the role of oil and gas within this strategy, we must consider not just our climate obligations, but also the challenge presented by the maturity of the North Sea basin and the natural trajectory of production that comes with that maturity.

The oil and gas industry had a transformational impact on Scotland and the UK, but now as a result of the extraction of oil and gas over decades and the geology of the North Sea, the reality is that the oil and gas available for extraction from the waters off the coast of Scotland is a declining resource.

While higher prices or tax incentives could make it economic to extract more marginal reserves from the North Sea, they cannot change the overall trend that comes from being an older and more expensive basin for extracting oil and gas.

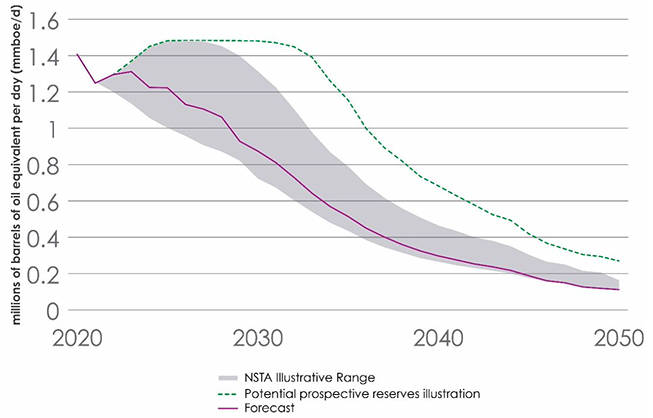

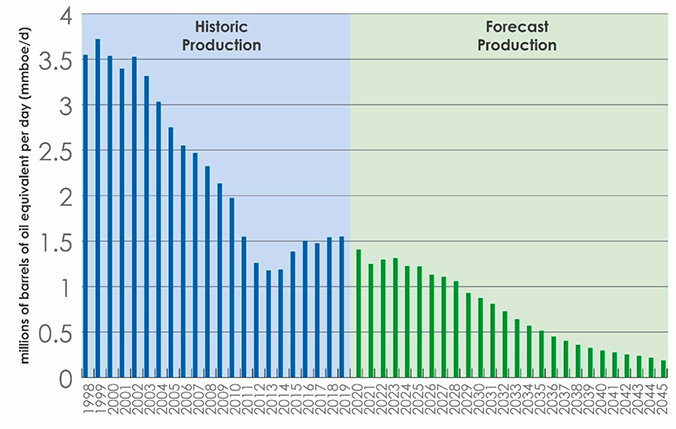

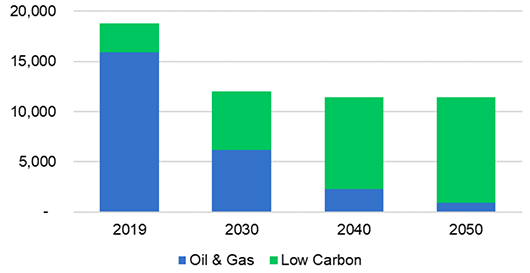

Production will decline, even with the UK Government's position on new exploration[63]. Figure 22 illustrates the projected future total oil and gas production and reserves.

Source: Ernst and Young analysis, North Sea Transition Authority. The chart includes estimates that illustrate the how cumulative NSTA reserves could apply as a production trajectory.

Ernst and Young analysis suggests that over 80% of future production is expected to arise from existing sanctioned fields, with the remainder of forecasts coming from new developments. The waters off the coast of Scotland have been well explored and, as a mature basin, there are unlikely to be large fields which have not been exploited. Further production levels will be dependent on a number of factors including price and technical and economic limitation. It is unlikely that all potential reserves will ultimately be exploited. The opening of the 33rd licensing round by the UK Government is only likely to have an incremental, not a transformative, effect on production forecasts. Figure 23 shows that production in Scotland is expected to be around a third of 2019 levels by 2035 and minimal (less than 3% of the 1999 peak) by 2050[64].

Source: Scottish Government, EY[65]

This means that, irrespective of the climate imperative, as an already established mature basin in gradual decline, planning for a just transition to our net zero energy system and securing alternative employment and economic opportunities for workers is essential if Scotland is to avoid repeating the damage done by the deindustrialisation of central belt communities in the 1980s, and to capitalise on our potential as a location for low carbon and renewable energy expertise.

Scotland's energy transformation is therefore urgent and inevitable.

Fortunately, the skills, drive and innovation of workers in the sector, the communities in which it is based and the companies that enabled Scotland to become a global source of energy expertise are already supporting a new energy revolution, repositioning Scotland as a centre of green energy excellence.

Bute House Agreement

As part of the Bute House Agreement between the Scottish Government and the Scottish Green Party, the Scottish Government committed to undertake a detailed analysis to better understand the future prospects for the North Sea including the pathway of oil and gas production projected for the basin, Scotland's energy requirements, how our energy activity aligns with our climate change commitments and the just transition impacts of a declining north sea basin at the same time as a rise in employment in low carbon and renewable energy industries. This work was conducted independently and overseen by an independent expert panel. It has provided an analytical evidence base that has been used to underpin the relevant parts of this draft Strategy and Plan, including the evidence presented in this section. The independent report, once completed and reviewed by the independent panel, will be published during the consultation period for the Strategy and Plan.

Global export and domestic usage

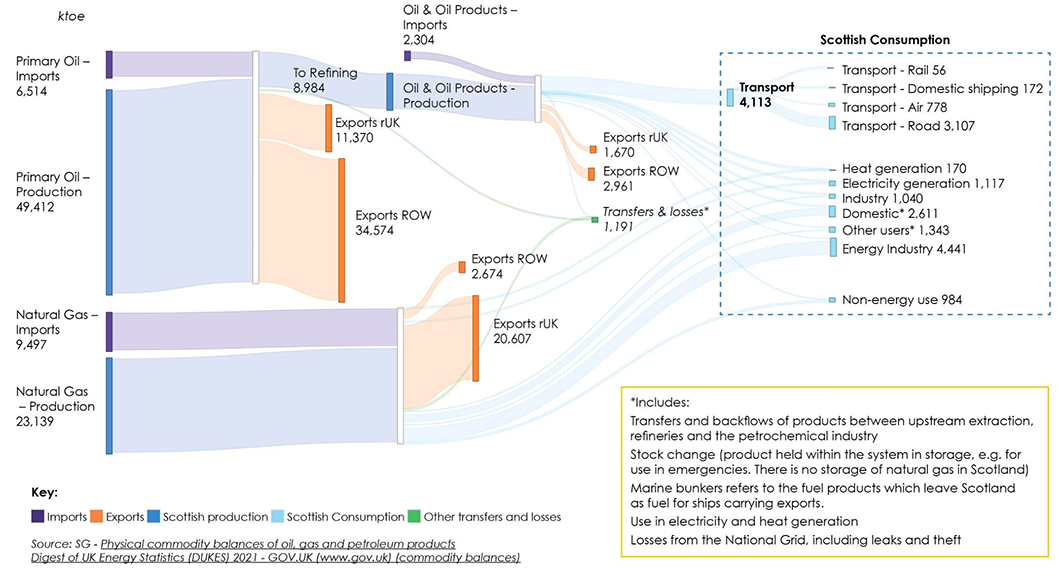

The oil and gas produced from the waters off the coast of Scotland[66] are global commodities, traded on international markets. In 2019, only a small proportion (about 16%) of the oil and gas coming in to Scotland (including imports from Norway and beyond), is consumed in Scotland. 81% of this oil and gas is exported, with oil exports primarily[67] going to the rest of the world and gas exports largely entering the UK gas grid for use throughout the UK, contributing to the UK's energy security. Figure 24 shows oil and gas flows through Scotland.

However, the decline in the basin has already meant a resultant decline in our export of oil; in 2019 we exported 49% less oil to the rest of the world than we did in 1999. Of the oil and gas consumed in Scotland, the biggest users are the energy industry itself, transport and heating. Oil and petroleum make up 42.0% of all Scottish consumption and gas makes up a third (35.6%).

Impact of Scotland's fossil fuel production on affordability of energy bills

Scotland's status as a fossil fuel producer has not insulated Scotland from the associated cost of living crisis because as a globally traded commodity, prices are set by international markets and Scotland's offshore gas reserves are too small to meaningfully change global gas prices. Scotland produced just 1% of global oil and gas production in 2019.

Oil and gas prices have surged since countries started to recover from the Covid pandemic and Russia invaded Ukraine. In 2022, wholesale natural gas prices increased more than 6-fold from their long-term average, resulting in upward pressure on household energy bills.

The importance of a just transition for the oil and gas sector

The maturity of the North Sea basin means a managed and just transition is essential in order to ensure that the move to renewable and low carbon sources of energy supports the oil and gas workforce, the communities in which they live and work, and the regional economies that have greatly benefited from oil and gas activities and have much to gain from the transition to net zero.

In 2019, 57,000 people had jobs that were directly or indirectly, through the supply chain, dependent on the offshore oil and gas sector[68]. Jobs in the industry are well paid - the average salary for those working in extraction was £88k, while for those working in the supply chain it was £51k, compared with an average salary in Scotland of £29k.

Jobs in oil and gas production, and the associated supply chain, are expected to decrease over the coming decades, as production from the North Sea basin declines. However, accelerated diversification of traditional oil and gas businesses and significant growth – as set out in this Strategy – in renewable electricity, hydrogen, heat and transport decarbonisation, and more will mean that low carbon jobs increase in number, with the total number of jobs in the energy sector expected to remain fairly constant. Energy production sector jobs are expected to hit 82,000 in 2030 as onshore wind development rapidly expands. Most new roles in the sector will build on existing skills sets from oil and gas, industrial research, manufacturing, and civil engineering, providing employment over the long term for those already working in the energy production sector and exciting opportunities for individuals beginning or switching to an energy-based career.

The pace and extent of replacement will be determined by wider energy policy decisions. For example, we continue to call on the UK Government to support the Scottish CCUS cluster. Modelling suggests that with the right support there could be a net increase in energy sector jobs from as early as the mid-2020s. Figure 25 shows direct and indirect employment by sector.

Source: EY analysis, Scottish Government.

A just transition for energy jobs

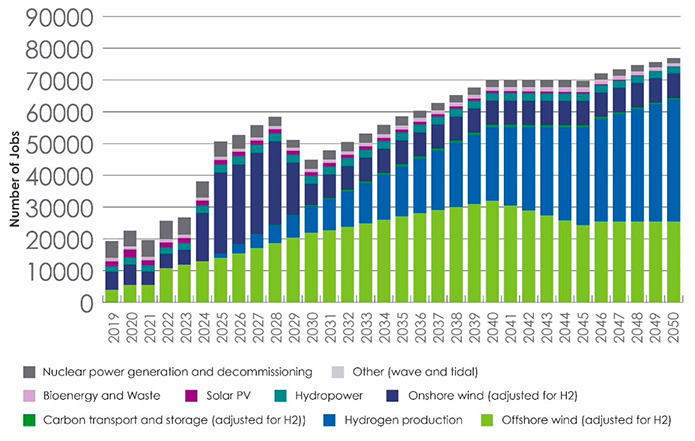

The projected employment shown in the graph below (figure 26) is direct and indirect employment by sector and is taken from two data sets – the assumed decline of production in the North Sea basin, which helps inform the calculation of future oil and gas jobs, and the 'Balanced options' (BOP) scenario in the Energy Systems Catapult (ESC) Scenarios, which establishes a trajectory for low carbon energy. The Energy and Just Transition analysis work then calculates low carbon jobs based on the amount of energy generated i.e. the more energy generated, the higher the number of jobs. The graph demonstrates that following the BOP scenario results in 83,000 jobs in the overall energy production sector by 2050, from a baseline of 76,000 in 2019. This increase of 7,000 jobs in the energy sector is of course positive, but it is also only part of the just transition picture. In 2019, there were just over 19,000 estimated jobs in the low carbon energy sector, but with around 6,000 jobs remaining in oil and gas sector by 2050 the number of low carbon jobs will rise from 19,000 to 77,000 – a 58,000 increase in low carbon jobs in energy production created by 2050 as the result of a just energy transition. The nature and the pace of our transition to net zero will impact the overall number of jobs created and different pathways for the decline of the oil and gas sector can further impact the number of jobs supported.

Source: EY analysis using Energy Systems Catapult Balanced Options Scenario

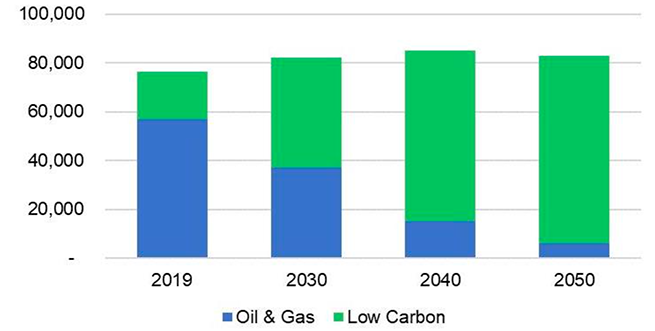

The GVA per job of the oil and gas extraction sector is £ 1.1 million, 15 times higher than the average for the Scottish economy. A significant proportion is paid to the UK Government through taxation and dividends are paid to shareholders, but the industry has made a very significant, if declining, contribution to Scotland's economy. While the number of workers employed, and economic value created by the oil and gas sector are expected to continue to decline as fossil fuel production in the basin declines, low carbon-based activity is expected to increase with the expansion of renewables. Importantly, although not projected to fully offset the decline in GVA from the oil and gas sector, the expansion of renewable energy production / generation will make a very significant contribution, and will substantially narrow the gap that would otherwise emerge. See figure 27.

These estimates do not include the GVA potential of exports of Scotland's renewable or low carbon energy – such as the potential for Scotland to develop a hydrogen export economy, which we expect would further boost GVA from the low carbon and renewable energy sector as a whole and help to reduce the impact of a decline in the export driven oil and gas sector.

Source: EY analysis, Scottish Government.

The role of the North East

The North East of Scotland is a global centre for the energy industry. With more than 50 years of knowledge and experience in offshore energy exploration and production.

Of the 25,000 jobs directly dependent on offshore oil and gas production (2019 figures), 98% are located in Aberdeen and Aberdeenshire. The industry has brought prosperity to the region, transforming the North East into a global energy hub, with many of the sector's workforce enjoying international careers from a local base. The personal and economic impact of oil and gas on the region has been profound.

Estimates from Robert Gordon University suggest that realising our ambition to retain the region's role as a hub for continuing energy innovation may require 14,000 people in the region to move from oil and gas to renewables and up to 16,000 new people to join the industry between 2022 and 2030[69]. Over 90% of the North-East of Scotland's existing oil and gas workforce has medium or high skills transferability to renewable energy roles meaning a just transition can create a significant economic and employment opportunity[70].

A just transition

The opportunity for a just transition is not just in the North East. All regions of Scotland will have a role to play in creating our future energy system, with the development of energy hubs with the potential to accelerate the industry to a net zero future, whilst continuing to support our energy ambitions. We are already seeing this in action through the Shetland Energy Hub which will accelerate the development of key technology to create an integrated energy future for Scotland and enable the region to transition to a hydrogen economy.

Grangemouth is ideally placed to produce future products in a net zero economy, and the region can also enable decarbonisation across other regions and sectors within Scotland. There is significant potential for carbon intensive industrial clusters, such as Grangemouth and Mossmorran, to unlock deeper decarbonisation across Scotland. In particular, Grangemouth's wealth of investment, infrastructure, skills, knowledge and productivity has strong potential for supporting a net zero economy.

Whilst the age profile of oil and gas workers means a significant proportion are expected to retire within this timeframe - a recent survey found 35% of oil and gas workers are over 50 - support will be needed for those who require retraining and to bring a new generation into the energy industry. Many young people are already choosing renewable or low carbon roles and the same survey found only 12% of the oil and gas workforce is under 30[71].

As the energy industry evolves, Scotland is well placed to harness and retain the existing skill set by securing new jobs and investment through the energy transition. To deliver a just transition for energy workers we must work with the energy sector to plan for a multi-skilled workforce, one that can benefit from opportunities across the energy system. This includes transitioning skilled offshore workers into jobs in CCUS and decommissioning or diversifying oil and gas business models into renewable energy portfolios, including offshore wind, CCUS and hydrogen sectors. Our oil and gas workers, and their vital skills, will be essential to the transition. Workers, and trade unions, will be at heart of everything we do as we work on our just transition plans.

Energy Sector Workers Survey

We worked with trade unions and employers to survey energy sector workers' views on the net zero transition. Detailed analysis of c. 900 responses will be published in early 2023.

Just under half of all respondents worked in the oil and gas sector, with around a quarter in the nuclear industry. Almost half of all respondents lived in the North East of Scotland. The largest cohort, by age group, were aged 50-55. Less than a quarter of respondents were female.

Initial findings:

The majority were not aware of the term "just transition". Once explained, the majority supported the Scottish Government's definition and approach. However, respondents tended to express low confidence in a just transition for the sector.

The majority believed the transition would have a big impact on their jobs. Early analysis indicates that oil and gas workers tended to believe this impact would be negative, whilst those in renewables tended to believe it would be positive.

Most thought the transition could create new energy jobs and saw themselves transitioning to a green/low carbon job in the future (either immediately or over the long term).

Respondents identified several key barriers to moving to green/low carbon jobs. These included not wanting to leave their current job; not being able to find equivalent good pay and a lack of information around reskilling/retraining and job opportunities.

Some said that they could never see themselves moving into a green job and this was typically due to either a lack of equivalent pay, or retirement plans. Others indicated they would benefit from improved support such as: more information on job opportunities, clearer information on retraining pathways, help with mapping their skillset and financial help for retraining.

Our £500m Just Transition Fund is providing financial support to help address some of the concerns raised in the Workers Survey around the ability to reskill and find good jobs and to build confidence in the potential for a just transition. The following projects have already been allocated funding from the Just Transition Fund.

Project: Skills Passport

Lead Organisation: OPITO

Description: Development and deployment of an industry led digital offshore energy skills passport to support the transition of skills and jobs across the rapidly changing industry.

Funding Awarded: £4,986,000

Project: Advanced Manufacturing Skills Hub

Lead Organisation: ETZ and North East Scotland College

Description: Creation of the Skills Hub in Altens as a focal point of the Energy Transition Zone Skills Campus.

Funding Awarded: £4,500,000

Project: Pilot Energy Transition Skills

Lead Organisation: National Energy Skills Accelerator (NESA)

Description: Pilot scheme to determine the skills required to reach an energy transition.

Funding Awarded: £1,000,000

Project: Net Zero Bottlenecks in Moray

Lead Organisation: UHI Moray

Description: Feasibility study to identify the current skill gaps in Moray and what is holding it back in transitioning to net zero.

Funding Awarded: £210,000

Recognising that depletion of the North Sea basin means that the era of oil and gas production will inevitably come to an end, the Scottish Government is determined to ensure we protect opportunities for workers and bolster our regional and national economies. Further, we believe the energy transition presents considerable economic opportunity, if we act early and with ambition. The Scottish Government, through our £75 million Energy Transition Fund (ETF), is supporting the energy sector to diversify and innovate and attract private sector investment into the region.

The Energy Transition Zone in Aberdeen will receive £26 million from the Scottish Government to become a focal point and catalyst for high-value manufacturing, research, development, testing and deployment with significant opportunities in offshore wind, hydrogen, and carbon capture and storage.

In delivering a just transition, and in giving workers and communities confidence in a just transition, it is essential that all parts of the current oil and gas industry and the communities connected to it, embrace the opportunities. This will mean working collaboratively with existing oil and gas businesses, low carbon and renewable energy businesses, across further and higher education and with local authorities, public agencies, trade unions and enterprise bodies to maximise the potential of the energy industry and areas such as the North East and Shetland. We already have successful partnerships with Opportunity North East, the Net Zero Technology Centre, Global Underwater Hub and Aberdeen City Council.

Decommissioning opportunities

As a mature basin, North Sea oil and gas infrastructure is coming to the end of its use for oil and gas production and decommissioning presents new opportunities.

The global decommissioning market is expected to be worth around £67 billion over the next 10 years[72] and offers significant opportunities for Scottish companies. As one of the first oil and gas sectors globally to require decommissioning on a significant scale, Scotland is already a centre of decommissioning excellence, and we want to ensure that the world class Scottish supply chain continues to develop competitive capabilities and can export its expertise. We urge the UK Government to provide more support directly to the decommissioning sector to ensure as much of this growing area of work as possible is carried out in Scotland, creating and protecting jobs and economic opportunities.

Much of the supply chain, skills and expertise in the industry currently are transferable to offshore decommissioning. The NSTD Integrated People and Skills Strategy[73] noted that 38% of current oil and gas workers saw working on decommissioning as their preferred destination as part of an orderly energy transition.

We have announced our intention to invest £9 million in the development of an ultra-deep-water port at Dales Voe, Shetland through the Islands Growth Deal to further increase the competitiveness of the decommissioning sector in Scotland.

Benefits of decommissioning to the climate and the environment

We are committed to ensuring that decommissioning is carried out to the highest safety and environmental standards, minimising the risk to the environment and other users of the sea. Decommissioning at Scottish ports should be undertaken in line with the principles of a circular economy and promote the reuse of materials over recycling and disposal. A circular approach has the potential to reduce the energy intensity and emissions from decommissioning structures, create new jobs and business opportunities, and provide cost savings for manufacturing processes that use decommissioned material.

Exploration and new production

Oil and gas exploration and production, including licensing, remains reserved to the UK Government. In 2014, Scotland's Independent Expert Commission on Oil and Gas recommended a policy approach based on Maximum Economic Recovery (MER), to maximise the total value added to Scotland from the oil and gas resources in the waters off Scotland. This position was reflected in our 2017 Energy Strategy: Future for Energy in Scotland.

In response to growing global understanding of the scale and implications of climate change, 192 countries and the EU joined the UN Paris Agreement. In 2019 the Scottish Government was one of the first in the world to declare a global climate emergency, making a commitment that Scotland's contribution to global emissions would end definitively within a generation.

Emissions impacts of oil and gas activity, and existing action in the sector on climate and the environment

Around 20% of the emissions associated with North Sea production are from the extraction and production process. Of this, more than 2/3 is a result of using natural gas or diesel in the energy intensive production process. Just over a fifth relates to flaring with less than 3% due to venting.

The North Sea Transition Deal[74] commits the sector to reduce emissions associated with oil and gas production by 50% by 2030. Key actions to reduce emissions include powering equipment by electricity instead of gas, and reducing flaring and venting. Total UK offshore flared volumes fell by 20% and venting by 22% in 2021. The OEUK Methane Action Plan also identifies a 50% reduction in total methane emissions by 2025.

The Scottish Government is committed to ensuring secure, reliable and affordable energy supplies and supporting the long-term decarbonisation of our energy generation in Scotland. Through the INTOG leasing round we are helping offshore oil and gas platforms to reduce their emissions by using electricity generated directly from local wind turbines to meet the targets in the North Sea Transition Deal.

The remaining 80% of emissions created from oil and gas is associated with end use of the products. 16% of this is in Scotland and the remaining will be attributed to the emissions of the countries where the products are ultimately used. See Chapter 4 for information on how we are reducing reliance on fossil fuels across our demand sectors.

In 2021 the International Energy Agency advised that no new oil and gas fields beyond those already approved for development as of 2021 should proceed if the global climate goal of net zero emissions by 2050 is to be met.

In 2021, taking account of these developments, the Scottish Government set out that Maximum Economic Recovery was incompatible with our climate obligations and no longer government policy.

In their letter of February 2022, to the UK Department for Business, Energy and Industrial Strategy, the UK's independent advisors on climate change, the Climate Change Committee, noted that whereas the evidence against any new consents for coal exploration or production is overwhelming, the evidence on new UK oil and gas production is not clear-cut.

Source: EY analysis, Stanford University [75]

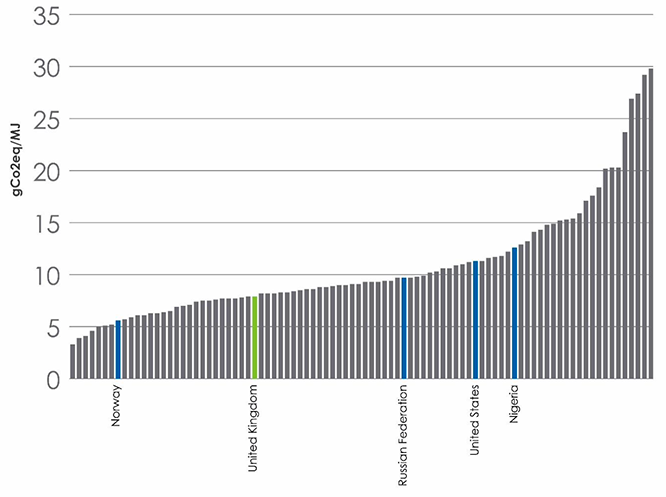

While there remains demand for oil and gas as an energy source through the transition, it is difficult to establish the net impact on global emissions of new UK oil and gas production as UK extraction carries a relatively low carbon footprint compared to other producers[76] (figure 28). However, the availability of production from the UK supports a larger global market than if there were less production overall.

Despite these difficulties, the Climate Change Committee concluded that it would support a tighter limit on production, with stringent tests and a presumption against exploration, observing that an end to UK exploration would send a clear signal of commitment to net zero to investors and consumers. This could have an important impact while businesses and individuals make decisions regarding how and when to adapt to net zero. The Climate Change Committee noted that there are additional important considerations, such as UK energy security, that extend beyond its statutory remit.

The Scottish Government is clear that unlimited extraction of fossil fuels is not consistent with our climate obligations. It is also clear that unlimited extraction, even if the North Sea was not a declining resource as outlined above, is not the right solution to the energy price crisis that people across Scotland are facing or to meeting our energy security needs.

As a country with a rich oil and gas heritage, and in a time of geopolitical crisis, we have a responsibility to balance energy security and national economic and social benefit with our international climate commitments.

As a result, in establishing a renewed policy position on oil and gas, whilst licensing is reserved to the UK Government, the Scottish Government is consulting on whether, in order to support the fastest possible and most effective just transition, there should be a presumption against new exploration for oil and gas.

Climate Compatibility Checkpoint

In September 2022, the UK government introduced a climate compatibility checkpoint for all new licensing rounds as part of the 33rd licensing round. Whilst in the absence of a presumption against exploration, we welcome this in principle, we believe that the assessment criteria are not rigorous enough to align with climate commitments under the Paris Agreement and should be strengthened.

In particular, any credible and effective package of climate compatibility tests must reflect the full global emissions impacts of oil and gas activity – in particular considering the emissions associated with the use of oil and gas (regardless of whether this occurs domestically or internationally), as well as its production.

While international bodies such as the International Energy Agency have developed global reduction pathways for fossil fuels (including oil and gas) production consistent with the Paris Agreement, there is no agreed method to allocate a production share to individual countries. However, the Paris Agreement more widely states that "The Agreement will be implemented to reflect equity and the principle of common but differentiated responsibilities and respective capabilities, in the light of different national circumstances." As part of the Bute House Agreement, analysis is underway to provide an evidence base to support efforts to ensure Scotland's energy activity is consistent with the Paris Agreement.

In this draft Strategy and Plan, as well as consulting on whether there should be a presumption against new exploration, we are also consulting on what factors should be considered in assessing the impact of new oil and gas production (i.e. from fields that are already consented but not yet in production) in the context of the global goals of the Paris Agreement.

We are consulting on whether the following principles should be considered in the development of a more rigorous package of tests:

- The impact of any new oil and gas production on global greenhouse gas emissions in the context of meeting the Paris Agreement goals, particularly in efforts to limit warming to 1.5°.