Bringing empty homes back into use: audit of privately owned empty homes

An independent audit of long-term empty homes policy and interventions in Scotland.

4. The progress and barriers in bringing empty homes back into use

The impact of empty homes

The Scottish Government literature review[28] draws together insights on the impacts of empty homes. It notes that bringing long-term empty homes back into use, and minimising their negative environmental and social impacts on communities is important for the effective functioning of the housing system.

The deterioration of homes that fall into disuse can attract vermin, cause problems for neighbours and adversely impact on the value of nearby properties and investment. Empty homes are also associated with physical decline, antisocial behaviour and other social problems that add to the pressure on public services and adversely impact community cohesion. (Action on Empty Homes 2019[29]; Wilson et al 2020[30]).

There are wider impacts of empty homes on an area, in terms of demographics and the housing market (Scottish Government 2019[31]; National Assembly for Wales[32]; Davies 2014[33]). De-population may also lead to a decline in amenities and infrastructure, discouraging people from moving to the area when they can’t access services or schools (Scottish Government 2019[34]). A large number of long-term empty homes can also restrict the types of accommodation available in local housing markets, and the lack of suitable accommodation may drive up house prices and rents (Breach 2021[35]),and increase the incidence and risk of homelessness (Davies 2014[36]; Feantsa 2019[37]). Long term trends concerning an ageing population and the increase of single person households alter demand for certain property types and impact on the suitability of the existing housing stock (Seirin-Lee et al 2018[38]).

The benefits of addressing empty homes

The Scottish Government literature review also highlights a number of opportunities provided by addressing empty homes. UK-wide studies have found that, in cities and regions with pressured housing markets, the nature of supply, demand and shortage is complex, but bringing empty homes back into use can form part of strategies to meet housing need. It is noted that, in light of the scale of housing need in these areas, it is wise to consider how existing stock is used as new-build housing alone cannot be carried out at the pace and scale required to address the housing crisis (Dunning and Moore 2020[39]). The Scottish Parliamentary Inquiry into Empty Homes suggested that tackling empty homes can contribute to regeneration and is an important component of maximising available housing supply.

In Scotland, one of the key work strands set out in relation to the Remote, Rural and Island Communities Housing Action Plan[40] is in relation to the effective and productive use of existing properties. This includes providing local authorities with additional powers that will help them to manage the number of second homes where these are contributing to housing pressures. There is also a stated commitment to consider ways in which to increase the number of empty homes in rural and island communities being brought back into use.

The 2020 Value Tool developed by the Scottish Empty Homes Partnership outlined a number of benefits of tackling empty homes, providing Value for Money opportunities[41] including reduced refurbishment costs compared with new-build costs, benefits to house prices/market confidence and positive local economic impacts.

In March 2022, the Scottish Empty Homes Partnership’s publication ‘Why Empty Homes Matter’[42] outlined the role of empty homes in delivering on Housing to 2040 through various mechanisms –

- Through operating buyback schemes or encouraging owners to bring empty properties back to use at affordable rents, local authorities can increase the supply of affordable homes in villages, towns and cities across the country.

- A number of local authorities run matchmaker schemes where empty homeowners can find out about people looking to purchase empty properties in their areas.

- Bringing empty homes back to use as part of wider town-centre regeneration can help reverse area decline and support the development of 20-minute neighbourhoods. It can also benefit neighbourhood quality and feelings of safety and security.

- Encouraging and supporting community groups to take ownership of empty properties and return them to use as affordable housing also has a vital role to play as part of long-term strategic plans to revive and sustain fragile communities.

- Third sector organisations taking ownership of empty homes can provide affordable housing options while also improving the quality and range of services they can offer to adults and young people.

- Retrofitting existing homes can improve the energy efficiency of occupied housing stock and also reduce the carbon emissions caused by housing construction.

- Repurposing empty homes so that, for example, larger older homes are converted to smaller units that can help to meet demand from older and disabled people looking to move within their existing community.

Reasons for empty homes

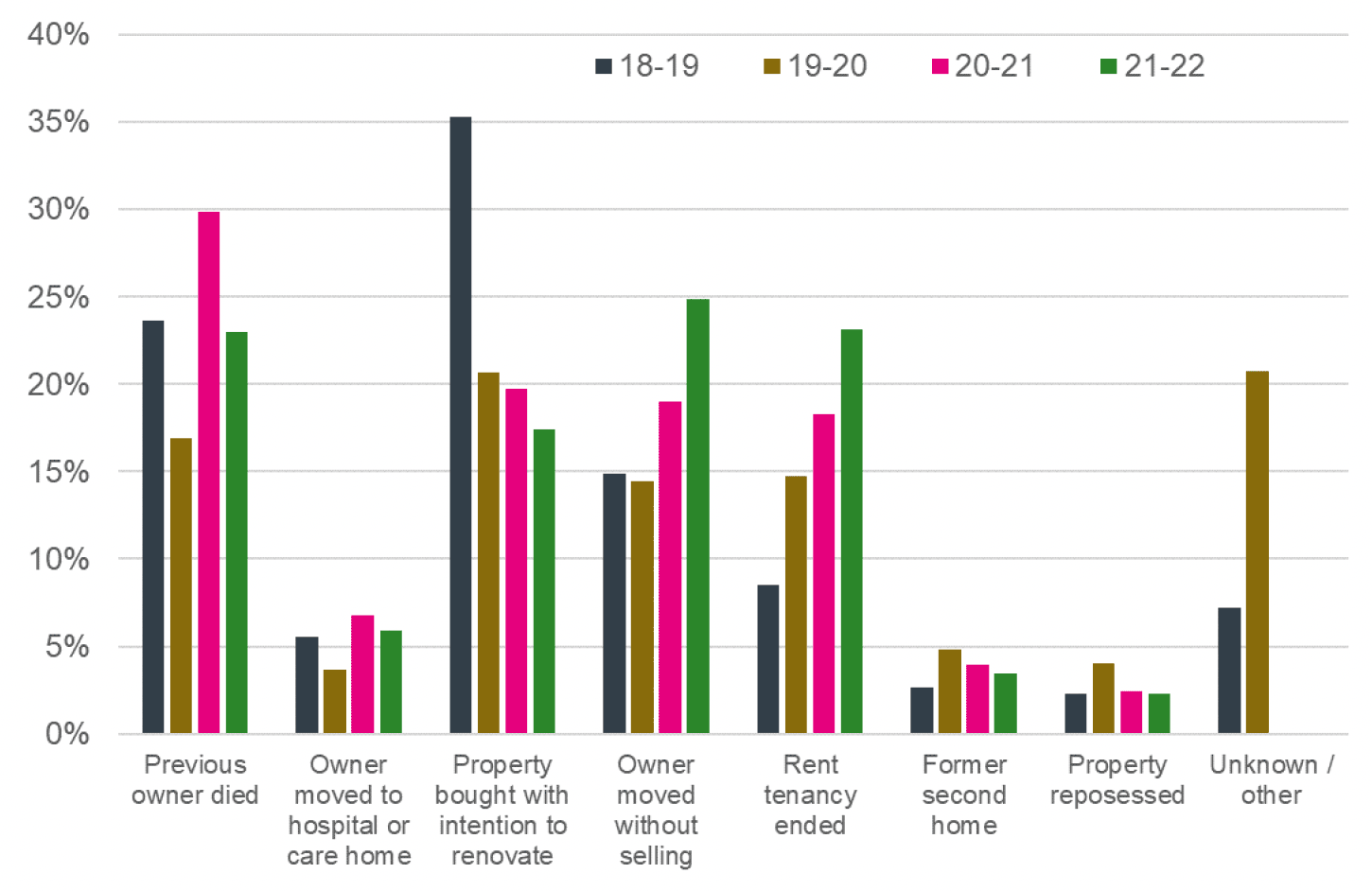

Analysis by the Scottish Empty Homes Partnership over several years shows the reasons that properties become empty. Although there is some year-on-year variation in the reason judged most important by Empty Homes Officers, the previous owner dying and the property being purchased with the intention to renovate tend to be most common (Figure 8). However, in 2021-22 the owner moving without selling and the rent tenancy ending became more frequent. The most significant increase over the last four years was rent tenancy ended (up 15 percentage points), and the most significant decrease (apart from unknowns) has been the property being bought with the intention to renovate (down 18 percentage points).

Source: Scottish Government analysis of SEHP annual reports About us | Scottish Empty Homes Partnership

Progress in bringing empty homes back into use

Between 2010 and March 2023, a total of 9,014 empty properties had been brought back into use through the partnership work between local authorities and the Scottish Empty Homes Partnership (SEHP)[43]. In addition, a further 161 empty homes have been brought back into through other interventions where Scottish Government has directly funded empty homes loans and grant schemes.[44] The total homes brought back into use which have been monitored through local authority or Scottish Government interventions is therefore 9,175 since 2010.

Figure 9 shows an anonymised breakdown of the homes brought back to use by local authority area between 2014-2015 and 2022-2023, as reported in SEHP annual surveys. Pre-2014 detailed data was not available by local authority. The average across the 32 local authorities was 270 properties (around 30 properties per year), ranging from zero properties to over 1,600 properties. In around two-thirds of local authority areas fewer than 200 properties were brought back to use over the nine-year period.

Source: SEHP annual survey returns

The areas where most properties were brought back to use tended to be larger local authority areas with some of the largest numbers of empty properties. However, there were also a couple of smaller local authority areas with fewer empty properties that had brought more than 400 properties back into use. Likewise, in some larger local authority areas where there were significant numbers of empty homes, relatively few properties had been brought back into use.

The latest published SEHP Annual Impact Report[45] showed that 1,152 properties had been reported as brought back into use by local authority Empty Homes Officers (EHOs) in 2021/2022 and data from SEHP shows 1,257 were in 2022/23. Of the properties where information was provided on how long the home was empty, almost 50% had been empty for between 2 and 5 years and a further 19% had been empty for more than 5 years (including 43 properties that had been empty for more than 10 years). This means that, despite the challenges in bringing longer-term empty homes back into use, the majority brought back to use have been empty for a considerable time. The 2022 SEHP report showed a greater focus on longer-term empty properties compared with previously. The 2020 and 2022 SEHP annual reports showed that 24% (2020) and 7% (2022) of homes brought back into use had been empty for less than a year, and 30% (2020) and 24% (2022) had been empty for 1 to 2 years. So the focus has shifted from mainly recently empty properties to mainly very long-term empty properties.

Table 2 shows the percentage point change in the proportion of dwellings that were long-term empty between 2016 and 2021. The left-hand column shows the local authorities that saw the greatest percentage point (pp) reduction in the proportion of all dwellings that were long-term empty properties between 2016 and 2021 (i.e. after the period where the council tax deduction rules would have had an impact).

| Reduced most | 2016-2021 |

|---|---|

| Orkney Islands | -1.40% |

| Argyll & Bute | -0.90% |

| Dundee City | -0.70% |

| East Ayrshire | -0.70% |

| West Lothian | -0.50% |

| Renfrewshire | -0.40% |

| Inverclyde | -0.40% |

| Similar | 2016-2021 |

| Fife | -0.20% |

| Moray | -0.10% |

| Perth & Kinross | -0.10% |

| Scottish Borders | -0.10% |

| Stirling | -0.10% |

| Angus | -0.10% |

| East Dunbartonshire | 0.00% |

| East Lothian | 0.00% |

| East Renfrewshire | 0.00% |

| Falkirk | 0.00% |

| Glasgow City | 0.00% |

| Midlothian | 0.00% |

| South Ayrshire | 0.00% |

| Dumfries & Galloway | 0.10% |

| West Dunbartonshire | 0.20% |

| South Lanarkshire | 0.30% |

| Scotland | 0.20% |

| Increased most | 2016-2021 |

| Aberdeenshire | 0.40% |

| North Ayrshire | 0.40% |

| Shetland Islands | 0.40% |

| North Lanarkshire | 0.50% |

| Clackmannanshire | 0.50% |

| City of Edinburgh | 0.70% |

| Highland | 1.20% |

| Na h-Eileanan Siar | 2.10% |

| Aberdeen City | 3.30% |

Thes local authorities seeing the largest percentage point reductions were: Orkney Islands; Argyll & Bute, Dundee City; East Ayrshire; West Lothian; Renfrewshire and Inverclyde.

All of the local authorities with significant reductions in the proportion of long-term empty homes had ‘Matchmaker’ schemes in place to link owners with potential purchasers who may wish to develop properties, most (but not all) had an Empty Home Officer, some had Empty Homes or Private Sector Strategies, while others had significant demolition programmes since 2015/16, which will have significantly contributed to the reductions in empty homes[46].

The local authorities during this period that saw the greatest percentage point increase in the number of long-term empty properties as a proportion of all dwellings between 2016 and 2021 were: Aberdeen City; Na h-Eileanan Siar; Highland; City of Edinburgh; Clackmannanshire; North Lanarkshire, Shetland Islands; North Ayrshire and Aberdeenshire.

Again, in some of these areas ‘Matchmaker’ schemes existed, but in some areas there is perhaps less evidence of strategic focus on empty homes work, but four are significant tourism areas - Na h-Eileanan Siar, Highland, City of Edinburgh and Shetland, and the number of holiday homes may have an impact of the long-term empty home estimates[47]. The following chapter examines the various approaches and interventions used across Scotland, and analyses the effectiveness of these, including EHOs resources available and the co-ordinating role of SEHP all of which may have impact on the rate of empty homes being brought back into use.

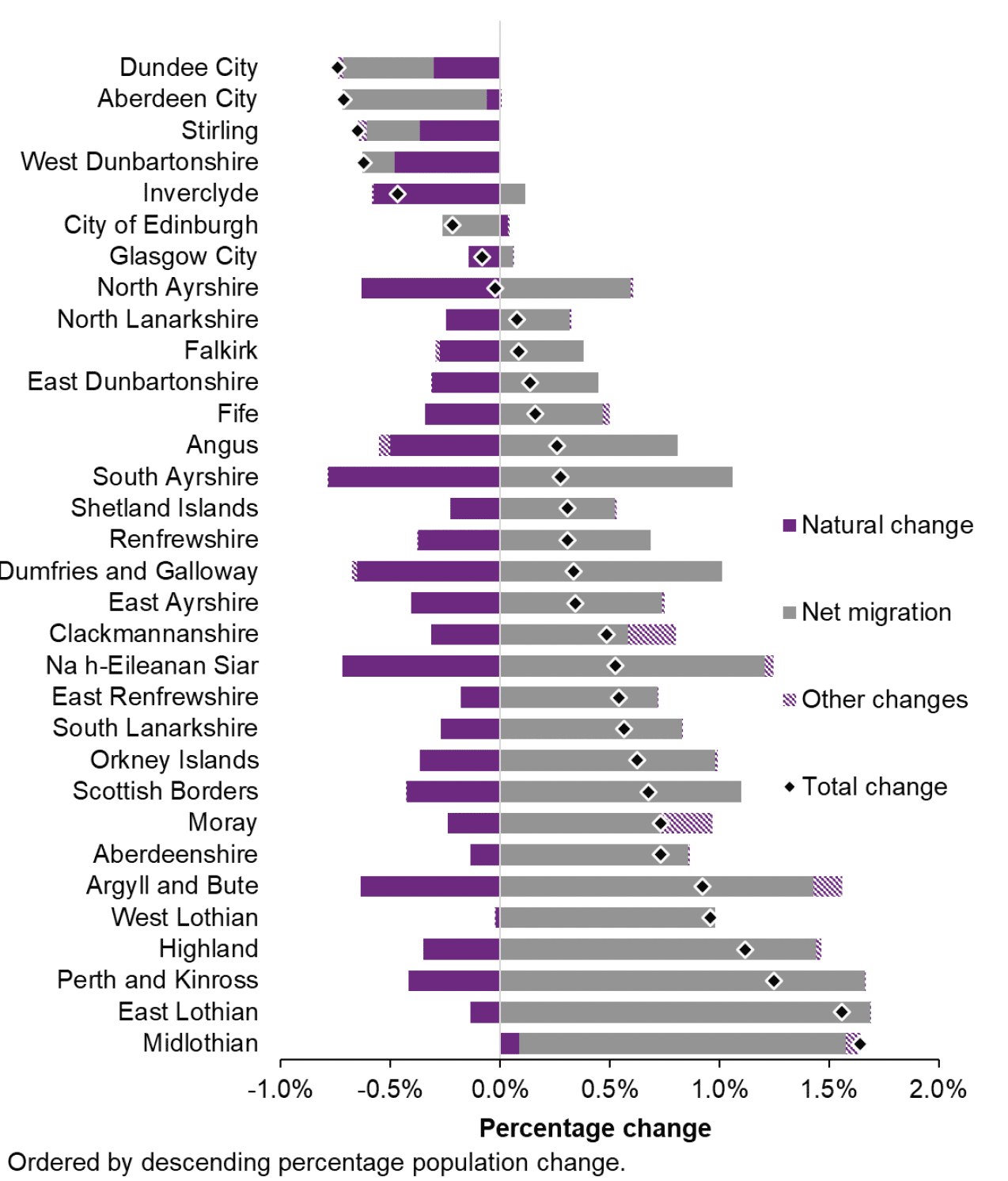

Recent economic change and population decline (Figure 10) may also impact on the housing market, which may also be a factor affecting progress in bringing empty homes back into use, for example, in Aberdeen and Dundee, as well as Inverclyde. Aberdeen in particular has experienced significant net migration associated with the downturn in the oil and gas sector, which started in 2014 and which led to a decline in relative economic performance across the region, with the number of employees falling by more than 15,000 between 2015 and the start of the pandemic in early 2020[48].

Source: Components of population change by council area, mid-2020 to mid-2021, Figures for Mid-Year Population Estimates for Scotland, mid-2021

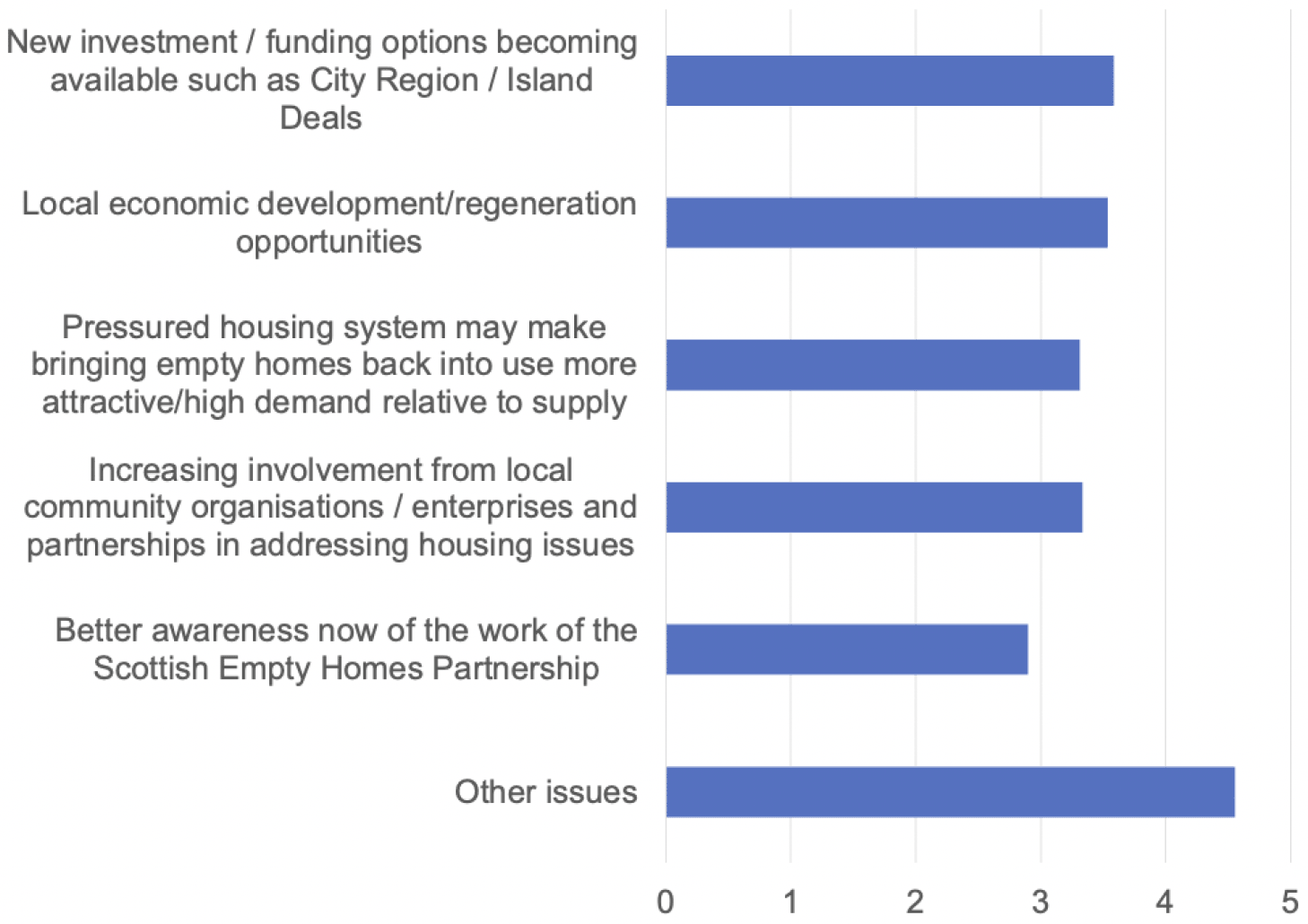

The local authority survey also showed that the influence of external factors has potential positive impacts in bringing properties back into use. When asked what impact external factors had on helping bring long-term empty homes back into use, those factors related to increasing resources were felt to have had the most significant impact – new investment and funding options becoming available and local economic development/regeneration opportunities scored highest overall. Pressured housing systems potentially making bringing empty homes back into use was also seen as a similarly positive factor.

The ‘other issues’ mentioned were important – but tended to be negative rather than positive factors – lack of funding being the most common, followed by the need for better communication (for example with banks, on the issue of possession).

Source: LA survey (base=28) Score 1=No impact at all, 5=A significant impact

Therefore, based on the above analysis, while there is some evidence of the benefits of local authorities’ more proactive engagement in relation to empty homes on recent progress, this has to be considered carefully against the impact of external factors e.g. the local housing market conditions, demolition schemes, the local economy including the prevalence of tourism and holiday homes, and strategic economic development initiatives including new investment.

Barriers in bringing empty homes back into use

Local Authority and wider stakeholder opinion on barriers in bringing empty homes back into use

The Scottish Empty Homes Partnership has examined the reasons why homes remain empty over time. This tends to be because of difficulty engaging with or locating the owner, the owner being unsure of the end use, and repair work being in progress or stalled due to financial reasons, as shown in Figure 12.

Source: Scottish Government analysis of SEHP annual reports About us | Scottish Empty Homes Partnership

The local authority survey demonstrated similar reasons for barriers in bringing empty homes back into use, with the three most significant issues identified being financial barriers such as lack of resources (inability to afford repairs needed or bankruptcy), difficulty in locating and engaging with owners, followed by owners’ personal reasons (such as emotional attachment to the property, mental incapacity, imprisonment or hospitalisation).

Source: LA survey (base=28) Score 1=Not an issue, 5=A significant issue

Open comments in the survey, combined with in-depth interviews provided further insight into the barriers to bringing empty homes back into use. The most common explanations in interviews related to problems in identifying ownership, engagement with owners (including financial difficulties and problems with implementing improvements), delays or complications in legal and administrative processes, and limited local authority resources.

Determining ownership was often the most difficult problem for local authorities to deal with. Identifying an owner was a particular problem in cases where the landlord was not resident in Scotland and even if identified could be outside of legal jurisdiction. A few interviewees spoke of problems associated with institutional investors, reluctance by solicitors and other professional advisers to provide information due to data protection requirements, and perception around owners moving abroad for a variety of reasons including the pandemic.

Even once ownership had been established, owner engagement was identified as problematic, including their willingness or ability to resolve their empty home issue. Participants spoke of a need to establish a relationship with property owners and offer constructive suggestions in managing their property. However, in many cases, engagement with owners presented a strong barrier and there were a variety of intractable problems encountered. Owners were often reluctant to sell or rent property due to financial commitments; these could be related to the availability of contractors or the costs of materials and labour, the cost of energy efficiency improvements, or due to concerns about the housing market and the value of their property. One wider stakeholder spoke of the sometimes unrealistic expectation of the value of the property that empty homeowners had and spoke of the skills required in persuading owners of the best course of action. Several open comments from the survey identified issues relating to a lack of understanding of how older buildings can be improved, and few incentives for owners to become private landlords – due to energy efficiency legislation and wider private rented sector legislation. This was also discussed in the qualitative interviews. For example, from two different local authorities:

“The big issue as well that you know where the way mortgage rates are and the cost of materials and things like that a lot you owners are still struggling financially to do anything with their properties” (Urban/rural local authority)

“a lot of people don't want to feel like if they sell the property and they've made losses on it, that's, you know, that's the get into kind of stuck position where they don't want to sell because of made a loss. They want to hold on to the property, but they can't do the repairs (Urban/rural local authority).

Most participants highlighted the difficulties which arise after a owner is deceased and their estates. Significant difficulties arise due to lengthy legal and administrative processes associated with the owner’s estate (including data protection and confidentiality issues, and grant of confirmation[49]), but there may also be issues related to inheritance, family disputes, and individual beneficiary circumstances. One interviewee highlighted that it is not always the case that inheritance provides beneficiaries with an asset, and it could in fact be a liability, and therefore there may be no incentive to do anything with the property. There may also be individual circumstances where a beneficiary does not have the ability or willingness to do something with the home. This includes beneficiaries with learning difficulties and/or lack of capacity with examples were provided of local authority social services working with EHOs and owners to support the inheritance process. It was also mentioned that for people on very low incomes, including those claiming social security benefits, inheritance may present difficulties for a variety of reasons including benefit regulations:

“They are the ones that cause most difficulty…we don’t know if there is a solicitor appointed or [don’t] know anything about the family members…we are at a loss really. Sometimes we will go with the genealogy companies and work with via the Scottish Empty Homes Partnership. It’s a bit of a loophole, even if there is a will. We don’t have access to that. They can choose not to get a will confirmed and can get a council tax exemption and leave the property empty with no council tax obligations.” (City local authority)

“If the owner of a property dies and there's a will and the estate is over £30,000 then the executor has to get a grant of confirmation. If the executor doesn't actually get that grant of confirmation, it can just sit there as just an unresolved estate. It's not that somebody does not have a right to it. It's sort of in limbo because nobody's taken that right on. And strictly speaking, in terms of council tax legislation, there's no council tax payable…So you could actually have an exempt property just sitting indefinitely with no grant of confirmation having been taken.” (City local authority)

“If you had an estate which is basically a liability to you would you want that inheritance? You know, it's all very well for talking about quarter of a million pound flats and that you're going to inherit and in that case you say, well, why wouldn't you just take it on? It might be capital gains tax, maybe that you're on benefits. That's a big one for me, the beneficiaries on benefits.” (City local authority)

Other reasons that some owners may be reluctant to sell (or rent) were connected to an emotional attachment to the property:

“The long and the short of it is they would rather bury their head in the sand and not deal with that. And that could be for all sorts of reasons. It could be sentimental issues in terms of dealing with…their parents’ property or something like that… if they can look the other way, they will.” (City local authority)

“No matter how much we guide them, people just don't want to part with their properties… A lot of these properties would sell or rent so easily, but it’s getting over that attachment and getting them to do something”. (Urban/rural local authority)

Administrative and confidentiality/data protection barriers were also cited as problematic in repossession, or other cases where lenders were involved. This meant that often EHOs have to leave the legal process to conclude and properties were described as being ‘stuck in limbo, because the banks aren’t dealing with it’. As one survey respondent illustrated:

“Couldn't get anywhere with the lenders I spoke to, although the staff agreed... it’s not the timescales for the legal process, but the administration delays in the banks/ lenders that could be reduced and therefore reduce the stress and strain for owners, lenders and the house market.” (Local authority survey respondent)

Almost all interview participants mentioned a lack of resources within local authorities, where finances were stretched and there was limited capacity for empty homes work. This was also mentioned in open comments in the local authority survey. Whilst local authorities said managing empty housing was a strategic priority, there was less evidence of the resource to undertake effective action including many having part-time EHOs, often with roles combined with other functions. These comments also related to the lack of financial incentives that local authorities could offer empty homeowners:

“There's one of me and [the authority] is 200 miles roughly, from top to bottom. But it includes so many housing market areas, islands, you can't physically be out and about in all those areas. It's not like having one town or small local authority to manage.” (Rural local authority).

“I think what we can offer as empty homes officers is very limited. A lot of the time when we were speaking to owners in new cases, we don't feel we've got a lot [to offer]… We don't have a grant scheme…and we don't have the empty homes loan fund, so a lot of what we can offer is very limited. To try and get people to engage with the small tools that we have is quite challenging. We have a small scheme of assistance budget, but it's not really geared towards empty homes.” (Urban/rural local authority).

Finally, one EHO summed up a common view that for some owners there was nothing that could be done to bring a property back into use:

“Whilst there are people allowed to have empty homes, there's nothing to stop them doing that if they're paying the premium on it or whatever they're due, they're looking after it and it's not causing an issue. There's very little we could really do about that.” (City local authority).

Homeowners experience in bringing properties back into use

Homeowners responding to the survey were asked if over the past 5 years they had a long-term empty property but which no longer met the definition of a long-term empty property (base: 197) (empty home for longer than 6 months). Over half, 58% of respondents confirmed they no longer had an empty property and confirmed the reasons why this was the case as set out in Table 3 below.

| Outcome | % of Empty Homes |

|---|---|

| Made ready for occupation and then rented out | 37% |

| Made ready for occupation and then occupied by yourself / your household | 28% |

| Made ready for occupation and then sold | 16% |

| Sold without improvements having been made ready for occupation | 13% |

| The use of the home was changed (please state what the use of the home was changed to) | 7% |

| The home was demolished | 1% |

| Other | 10% |

| Base | 115 |

Source: Homeowners survey

Most commonly, properties that were previously long-term empty were ‘made ready for occupation and then rented out’ (37%) while a further 28% were ‘made ready for occupation and then occupied by respondents or their household’. Significantly fewer (16%) were made ready for occupation then sold, and 13% were sold without having been made ready for occupation. In 7% of cases the use of the home was changed and most commonly this was changed to a holiday let (where this was not the case, the outcome was unclear from the respondent’s comments). A further 1% of homes were demolished and 10% had an “other” outcome. The most common “other” outcomes were that the home is still being renovated or refurbished but other comments noted issues such as delays to such renovations or other current circumstances such as the home being used on a temporary basis by refugees or being occupied by a family member.

Homeowner respondents were also asked about the condition of their current long-term empty properties. Just over half (51%) of respondents (base: 197) said they currently had at least one long-term empty home that had not been occupied for a period of 6 months or greater. Based on these responses, the majority of current long-term empty properties required at least some investment to make them ready for occupation (73%) and 42% required a significant level of investment. A little over a quarter (27%) of empty homes were said to be ready for occupation with little or no investment required (see Table 4).

| Condition | Number of Empty Homes | % of Empty Homes from responses | Base number of respondents |

|---|---|---|---|

| Ready for occupation with little or no investment | 33 | 27% | 23 |

| Requires some investment to make ready for occupation | 39 | 32% | 26 |

| Requires significant investment to make ready for occupation | 52 | 42% | 45 |

| Total | 124 | 100% | 87 |

Source: Homeowners survey

It should be noted that the individual bases do not sum to the total base as some respondents have empty homes in more than one of the categories of condition provided.

Respondents were then asked to comment on why any homes that they had were currently long-term empty. A range of sometimes related themes arose with the most common themes listed below, along with illustrative quotes:

- Property condition and renovation

- Personal circumstances

- Financial concerns and investment requirements

- Market and regulatory conditions

Property condition:

“As a listed building it took time to get planning permission.”

“Farm inherited but not inhabitable due to damp, collapsed flooring and other issues. In process of getting plans to apply for new build to replace but can’t afford to fix property at present.”

Personal circumstances:

“Owner of house was in prison and died in 2022. Executors are left dealing with the estate.”

“It was my parents’ house. Sentimental value.”

Financial and investment concerns:

“Couldn’t afford to complete the renovation and fell behind on the mortgage. Property on the market for sale.”

“Bought it to restore just before lockdown. Lockdown and a change in finance has delayed it significantly.”

“Could not sell at valuation or even close to.”

Regulatory concerns:

“Belonged to my parents and initially I began to do it up to rent out until I moved back to the area and planned to live there. However, with the change in law I have now changed my mind about letting as under new regulations I may have trouble getting a tenant out.”

“The tenancy rules are increasingly being stacked against the private sector landlord. Inability to increase rents, constrained ability to remove tenants, uncertainty over energy efficiency regulations.”

Survey respondents were also shown a list of potential barriers to bringing a long-term empty property back into use and asked to rate each on a scale of 1 to 5 where 1 is "not an issue" and 5 is a "significant issue". These results are detailed below for respondents with homes that were currently empty, or were long-term empty at some point over the past 5 years. The analysis below shows the distribution of responses and the mean rating for each on the scale of 1 to 5 for each barrier.

| Barrier | Mean | 1 | 2 | 3 | 4 | 5 | Base |

|---|---|---|---|---|---|---|---|

| Practical reasons such as repairs / refurbishment taking longer than planned | 3.44 | 23% | 7% | 13% | 15% | 42% | 175 |

| Financial barriers - for example, not being willing or able to commit sufficient financial resources | 3.14 | 28% | 9% | 15% | 16% | 32% | 176 |

| Housing market factors making investment in empty homes unviable | 2.36 | 52% | 7% | 14% | 8% | 19% | 174 |

| Personal reasons - for example, your emotional attachment to property, other personal circumstances | 2.25 | 57% | 7% | 9% | 8% | 19% | 175 |

Source: Homeowners survey

The most common barrier for bringing empty properties back into use related to practical reasons such as repairs / refurbishments taking longer than planned (mean rating of 3.44 on the 1-5 scale, with a total of 57% giving this a rating of 4 or 5 as a barrier). This was followed by financial barriers (mean rating of 3.33 on the 1-5 scale, with a total of 48% giving this a rating of 4 or 5 as a barrier). The other issues were less likely to be perceived as barriers. For housing market factors making investment in empty homes unviable the mean rating was 2.36, with 22% giving a rating of 4 or 5 as a barrier; for personal reasons, the mean rating was 2.25, with 27% giving a rating of 4 or 5.

Respondents were then asked to comment on any other barriers that they have found to bringing a long-term empty home back into use, many of which repeated the themes listed on why properties were empty (listed above). The most common themes are listed below, along with some illustrative quotes:

- Supply of labour and services to complete renovations

- Costs and perceived lack of support, incentives or sanctions

- Personal circumstances or knowledge

- Regulations and attractiveness of investment in the private rented sector.

Supply of labour and services to complete renovations:

“It is hard to find builders / plumbers / electricians with capacity to take on work.”

“Can’t even get quotes.”

“Costs and scale of refurbishments required.”

Costs and perceived lack of support, incentives or sanctions:

“Council tax levies and gradual increases instead of help.”

“Money, VAT and the lack of grant aid.”

Personal circumstances or knowledge:

“Just tired and not energised to empty or refurbish flat.”

“The building has eight owners and none of us have the knowledge to undertake a major building renovation.”

Regulations:

“Not easy to find trustworthy tenants.”

“The current tenancy regime is so overly penal and weighted towards tenants.”

In-depth interviews with empty homeowners also explored the barriers for bringing empty properties back into use. The key barriers highlighted through these interviews related to three key themes, again repeating what was found in the homeowners survey: housing market values and cost of works and therefore the impact on viability for bringing properties back into use; the construction industry; and, the regulatory framework for rented properties.

In relation to housing markets and viability issues, empty homeowners with properties in more remote and island areas emphasised that the local market presented significant barriers to getting a property back into use, mainly due to relatively low property values (sale or rent) relative to the cost of improvement. For one private landlord comparison was made of rents in some urban areas, and that he couldn’t ‘just hike up rents like you can in Edinburgh’. Another owner who was undertaking major renovation of a rural cottage reflected on the cost of the works, explaining that the property was located in a less desirable location and that it wasn’t feasible to improve the property without major capital support. One owner also explained the specific nature relating to crofting tenure and she felt a lot of empty homes in her community were due to owners not having the right knowledge or access to specialist crofting legal advice. A few owners in more urban areas also felt that housing market forces in play were not conducive to bringing properties back into use, some of which was put down to post Covid-19 pandemic recovery. For example, one owner expressed surprise at not being able to sell or rent her one-bedroom city-centre flat following lockdown due to lower market demand, despite struggling to secure that same home only a few years prior as a first-time buyer. Another owner in a different urban area explained how he was still experiencing a time lag in renovation due to having lost the services of an architect during the pandemic period.

The market for construction workers was also identified as a barrier to getting renovations completed to bring properties back into use. This related to both lack of availability of labour, and high cost of works. Examples of the frustrations included a few owners who pursued an empty homes loan but could not satisfy the requirement of securing three competitive tenders because ‘no one wanted the job’[50], and one owner who stated that for renovation jobs in rural areas you had to depend on tradesmen who were not VAT registered, and therefore the 5% VAT discount was not helpful. Another owner with a property on a remote island explained that the tradesmen that were available billed her for more than £40k in transport costs alone. The availability of skilled trades was a particular problem in more remote locations, but not exclusively so, with frustration also expressed by an owner of a tenement property in a large urban area, explaining that she felt ‘really lucky’ to have found a building surveyor who was willing to take on the job appreciating the challenges involved with tenemental improvement works, and working with a number of different owners where a common repair was involved to get her property back into use.

Finally, the regulatory environment was identified by some owners as presenting a barrier towards bringing empty property back into use. One owner who had four empty properties in a rural area explained that he had intended to renovate them for private letting, but if, as he believed “the Scottish Government continued it’s anti-PRS stance” through new legislation including rent control, then he would need to change strategy such as renovating the properties as holiday homes. Similarly, other owners felt they were being penalised for doing “the right thing” by not going down the short term let route, and even though one owner thought short term lets ‘kill communities’, he had no viable alternative. A few owners also spoke about the additional requirement for landlords of residential properties to achieve an Energy Perfornance Certificate (EPC) rating of C or higher by 2028[51] which caused one owner to look into changing the use of the properties to either business or short term lets (where the same level of energy efficiency requirement is currently not required). Others said they were trying to conserve their properties in the “correct historical context” but found the financial viability of doing so challenging.

Key findings summary

- Empty homes impact on the availability of housing in areas of shortage, restricting the volume, type and size of properties available in the housing system, which in turn may result in increased house prices, or may impact on the long-term sustainability of some communities. Deterioration of empty homes also have negative environmental and social impacts on communities including physical decline, vermin and anti-social behaviour all of which add to pressure on public services and adversely impact community cohesion.

- Bringing empty homes back into use can form part of strategies to meet housing need, particularly in the context that new-build housing alone cannot be carried out at the pace and scale required to meet all housing requirements. Bringing empty homes back into use can be lower cost than new build and can provide positive economic and social impacts. In rural areas empty homes strategies can help revive and sustain fragile communities, particularly where second homes contribute to housing pressure, and in urban areas, city and town centre regeneration can help reverse area decline.

- The reasons for empty homes in Scotland are most commonly associated with the previous owner dying, or the property being purchased with the intention of renovation, although there have also been significant recent increases in owners moving without selling and tenancies ending without replacement tenants.

- Between 2010 and March 2023, a total of 9,014 empty properties have been brought back into use through the partnership work between local authorities and the Scottish Empty Homes Partnership. The rate at which homes are brought into use varies significantly by area, and while there is a general correlation between areas with large numbers of homes and larger numbers of properties brought back into use, there are also areas where there is smaller volume of empty homes but where significant numbers of homes have been brought back into use. There are also some local authority areas where there are significant numbers of empty homes, but relatively few properties have been brought back into use.

- Looking at the factors which affect progress in bringing empty homes back into use, while there is some evidence of the benefits of local authorities more proactive engagement in relation to empty homes on recent progress, this has to be considered carefully against the impact of external factors e.g. the local housing market conditions, demolition schemes, the local economy including the prevalence of tourism and holiday homes, and strategic economic development initiatives including new investment.

- The barriers in bringing empty homes back into use are commonly identified across local authorities and wider stakeholders as: locating or engagement with owners; financial barriers (often associated with the cost of repairs/improvement); and personal reasons (including difficulties which arise after an owner is deceased, and a range of family and individual circumstances). Local authorities also identified the lack of resources at their disposal, including staff time committed to empty homes work and financial incentives available for owners.

- Similarly, homeowners identified the main barriers to bringing properties back into use as practical reasons around repairs and refurbishment, and financial barriers. These two reasons were often interlinked and there were challenges around engagement with the construction industry in terms of availability and cost of repairs, which led to viability issues to invest in some lower value housing markets. Other key barriers were various personal circumstances which could impinge the owner’s ability and willingness to bring the property back into use, and the regulatory environment acting as a deterrent to invest in the private rented sector.

Contact

Email: secondandemptyhomes@gov.scot