Scottish Housing Market Review: Q3 2021

Summary of the latest Scottish housing market data.

Lending To Homebuyers: Arrears and Possessions

Arrears

Please note: Covid-19 related mortgage payment deferrals are not considered to be formal arrears, and so will not be reflected in the statistics below.

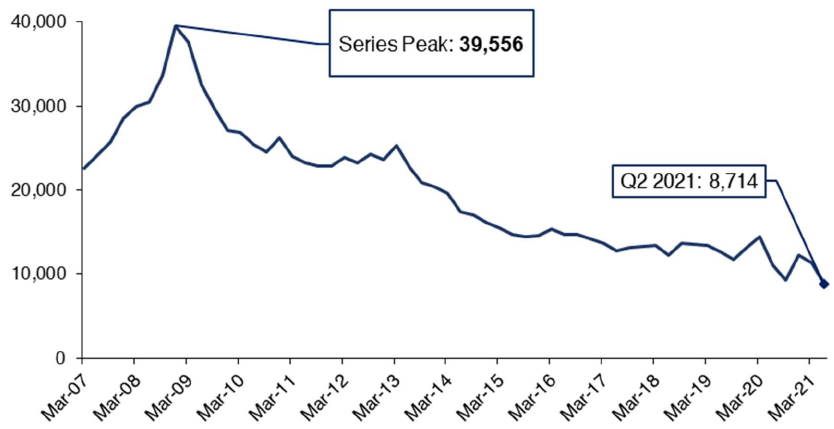

There were 8,714 regulated mortgages that went into arrears across the UK in Q2 2021, a decrease of 21.6% (2,401) on Q2 2020. As shown in Chart 4.9, this is also significantly lower than levels following the 2008 financial crisis, when the number of regulated mortgages that went into arrears peaked at 39,556 in Q4 2008. (Source: FCA)

Source: FCA

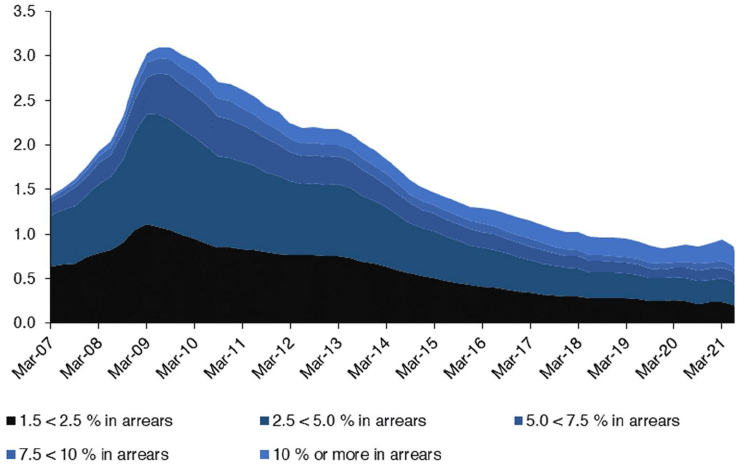

The share of lenders' outstanding regulated mortgage balances that were in arrears stood at 0.86% at the end of Q2 2021. This has remained broadly stable during the pandemic, with arrears at 0.88% at the end of Q2 2020. Chart 4.10 plots the share of lenders' outstanding balances that were in arrears by degree of severity. Arrears reported in the FCA MLAR data relate only to loans where the amount of actual arrears is 1.5% or more of the borrower's current loan balance.

Source: FCA

UK Finance data show that there were 6,020 buy-to-let mortgages in arrears of 2.5% or more of the outstanding balance across the UK in Q2 2021. This is up by an annual 20.2%, although, this growth comes from a low base. This is still low relative to the period of the 2008 financial crisis. The number of buy-to-let mortgages in arrears of 2.5% or more as a percentage of the total number of mortgages in arrears of 2.5% or more is 7.3% as at Q2 2021, up from 6.3% in Q2 2020.

Possessions

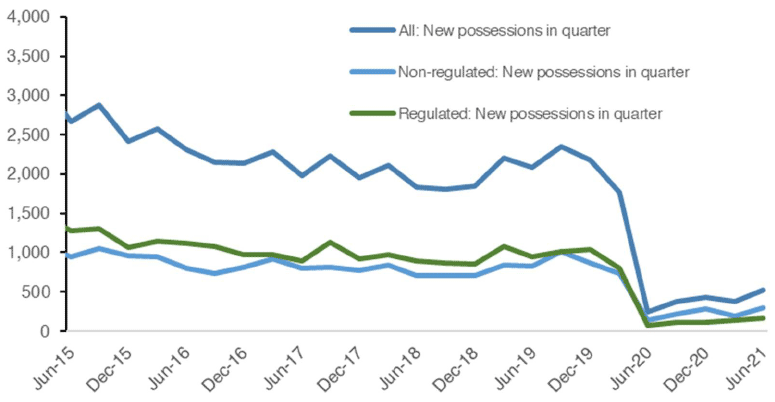

There were 227 new regulated mortgage possessions across the UK in Q2 2021, an increase relative to Q1 2021 of 44 (24%) as can be seen in Chart 4.11. However, this is significantly less than pre-pandemic levels, with possessions down by 83% relative to Q4 2019. It can also be seen that regulated and non-regulated possessions moved in a similar direction over the recent period.

Source: FCA

Guidance on evictions and repossessions

A ban on the enforcement of eviction orders in areas in Levels 3 and 4 is in place until 30 September 2021, although all areas in Scotland are currently in Level 0 or lower. The Coronavirus (Extension and Expiry) (Scotland) Bill, passed on 24 June 2021, has extended additional protections for tenants to 31 March 2022: in particular, measures increasing the notice period for social and private evictions to 6 months in most cases, giving the First Tier Tribunal discretion when considering all grounds for eviction in the private rented sector, and requiring private landlords seeking eviction on rent arrears grounds to follow Pre-Action Requirements. The Scottish Government recently announced a £10 million tenant grant fund for councils to support tenants struggling to pay their rent as a direct result of Covid-19 and who are at risk of eviction. This is part of a package of measures available to local authorities to prevent homelessness, alongside Discretionary Housing Payments and advice on maximising income. The grants come on top of the Scottish Government’s £10 million Tenant Hardship Loan Fund.

The FCA published finalised guidance for mortgage lenders in March 2021, outlining that repossessions can be enforced from 1 April 2021 but this must be in accordance with FCA guidance and regulatory requirements, which mean that repossessions should only take place as a last resort, if all other reasonable attempts to resolve the situation have failed.

The FCA guidance also recognises that lenders will need to comply with relevant regulatory and legislative requirements in the different jurisdictions across the UK. (Source: FCA). The Scottish Government extended the ban on repossession of mortgaged properties in areas under level 3 or 4 restrictions until 30 September 2021, subject to review every three weeks. However, there are no areas in Scotland currently under level 3 or 4 restrictions.

Contact

Email: William.Ellison@gov.scot