Scottish Housing Market Review: Q2 2022

Scottish housing market bulletins collating a range of statistics on house prices, housing market activity, cost and availability of finance and repossessions.

Part of

7. Mortgage Arrears & Possessions

Arrears

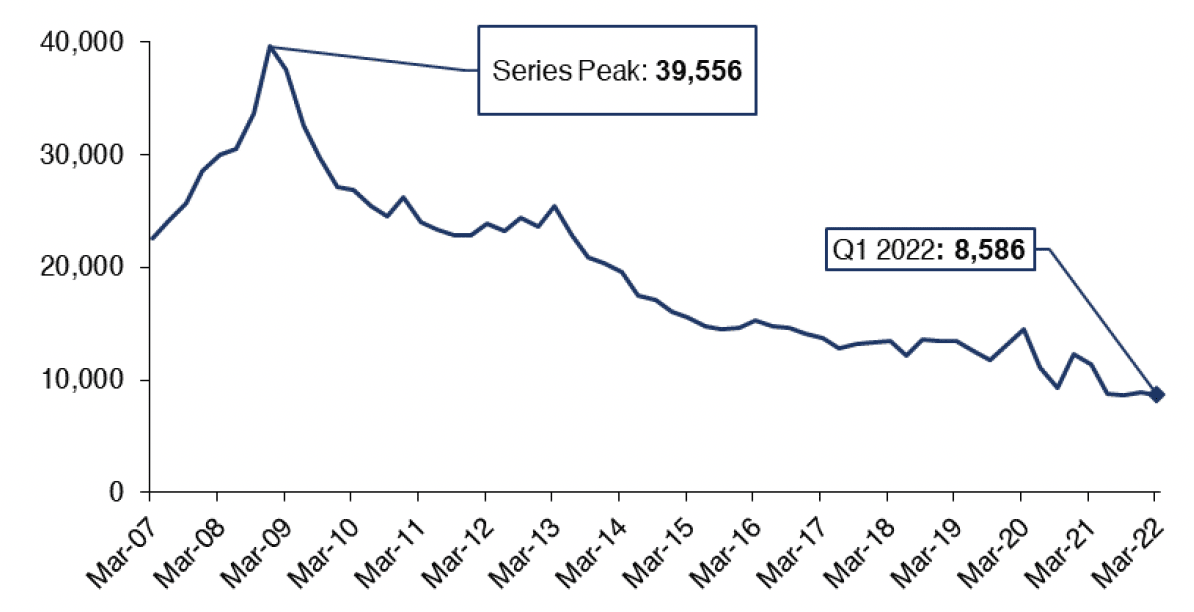

There were 8,586 regulated mortgages that went into arrears across the UK in Q1 2022, a decrease of 24.4% (-2,777) on Q1 2021. As shown in Chart 7.1, following a peak of 39,556 in Q4 2008 during the financial crisis, there has been a declining trend in the number of regulated mortgages entering arrears, which has continued despite the impact of Covid-19. It should be noted that Covid-19 payment holidays were not classified as technical arrears, and thus are not reflected in these figures; however, even though these payment holidays came to an end in April 2021, this has not result in an increase in arrears so far. (Source: FCA)

Source: FCA

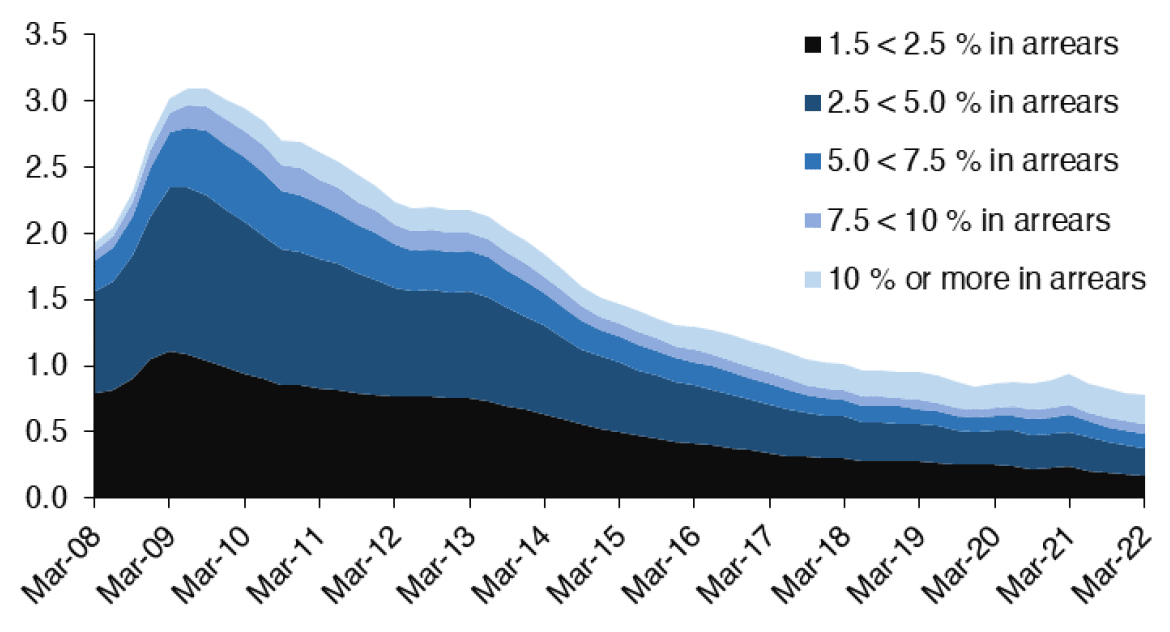

The share of lenders' outstanding regulated mortgage balances that were in arrears stood at 0.78% at the end of Q1 2022. This has remained broadly stable during the pandemic, with arrears at 0.86% at the end of Q1 2020. Chart 7.2 plots the share of lenders' outstanding balances that were in arrears by degree of severity. Arrears reported in the FCA MLAR data relate only to loans where the amount of actual arrears is 1.5% or more of the borrower's current loan balance.

Source: FCA

UK Finance data show that there were 5,860 buy-to-let mortgages in arrears of 2.5% or more of the outstanding balance across the UK in Q1 2022. This is down by an annual 5.2% (-320), and is also low relative to the period of the 2008 financial crisis. The number of buy-to-let mortgages in arrears of 2.5% or more as a percentage of the total number of buy-to-let mortgages was 0.29% as at Q1 2022, slightly lower than Q1 2021 (0.31%).

Possessions

The FCA published finalised guidance for UK mortgage lenders in March 2021, outlining that possessions could be enforced from 1 April 2021 but this must be in accordance with FCA guidance and regulatory requirements, which means that possessions should only take place as a last resort, if all other reasonable attempts to resolve the situation have failed. In Scotland, a ban on the enforcement of eviction orders in areas in Covid Protection Levels 3 and 4 ended on the 30 September 2021.

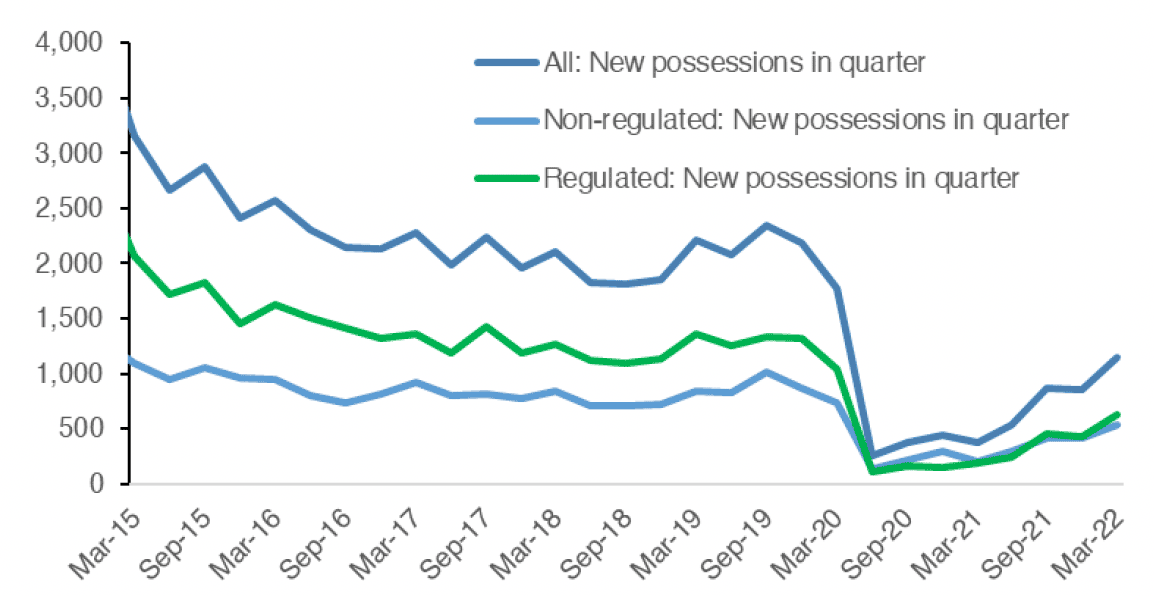

Chart 7.3 shows that despite restrictions on possessions being lifted, there were only 622 new regulated mortgage possessions across the UK in Q1 2022. While this was an increase relative to Q1 2021 of 188 (+43.3%), and the level of possessions also increased over the quarter, possessions are still substantially lower (down 420, or 40.3%) relative to Q1 2020, immediately prior to the pandemic. It can also be seen that regulated and non-regulated possessions moved in a similar direction over the recent period.

Source: FCA

Contact

Email: William.Ellison@gov.scot