Publication - Research and analysis

Scottish economic bulletin: October 2023

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business Conditions

Business conditions remain challenging with slowing business activity and persistent cost pressures further weighing on business optimism.

Business Activity

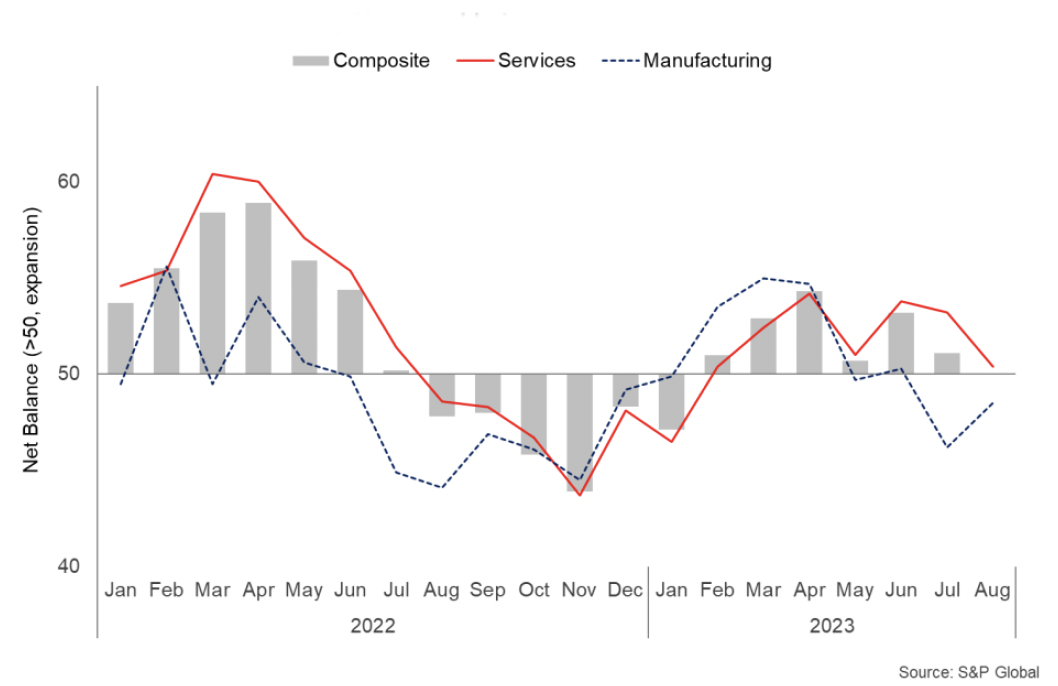

- The Purchasing Managers Index (PMI) business survey indicates that the pace of business activity in Scotland's private sector has slowed over the second quarter and through July and August.[5]

- The business activity indicator fell to the 50 no change mark in August, its lowest rate since January, driven by a further moderate fall in manufacturing activity (48.5) accompanied by a notable slowing in services activity growth (50.4).

- A key element of weaker business activity was a broad based fall in new business orders across the manufacturing and services sectors, with respondents citing that weakening demand reflected inflationary pressures, economic uncertainty and the cost of living.

Business Concerns

- The factors weighing on demand reflect the broader concerns that business are currently reporting on business conditions.

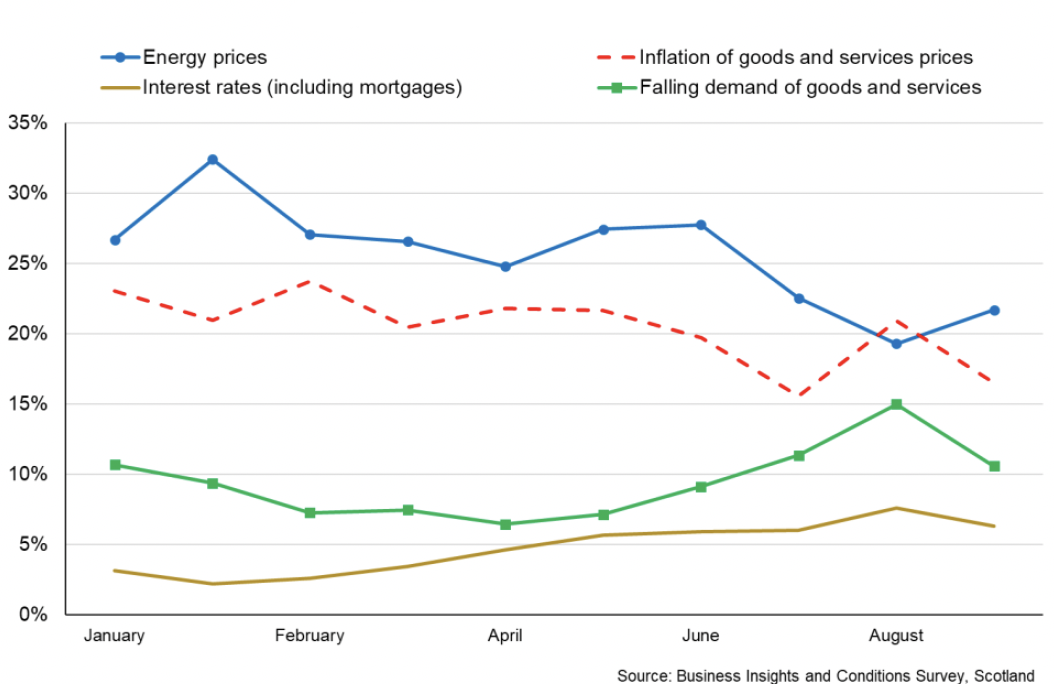

- The main concerns reported by businesses in the Business Insights and Conditions survey (BICS) for September is inflation of goods and services prices (16.5%) and energy prices (21.7%). The share of businesses reporting these as their main concern have fallen from their 39% peaks in the second half of 2022, indicating that businesses have been adjusting to the inflationary pressures of energy and goods and services over this period.[6]

- The Scottish Chambers of Commerce Quarterly Economic Indicator also showed that concern over inflation had eased generally in the second quarter, however at a sector level remained highest in construction, retail and tourism. In the retail sector in particular, the increased concern reflected the risks that sustained high inflation would have on consumer spending power.[7]

- Furthermore, the Scottish Chambers of Commerce Quarterly Economic Indicator and the Scottish Business Monitor report that labour costs have become the main cost pressure for businesses in the first half of 2023 and are expected to remain so over the next 6-months.[8]

- Rising interest rates and borrowing costs are also an increasing concern for businesses with 6.3% of respondents reporting interest rates as the main concern for their business which has been on an upward trend over the past year (up from 1.7% in September 2022). Furthermore, 10.6% of businesses are concerned about falling demand of goods and services, which has also been on an upward trend in recent months reflecting the ongoing concerns business have regarding the headwinds facing domestic and international demand from higher cost of living and borrowing costs.

Business Costs

- As set out above, cost pressures remain a key concern for business having faced rapid increases over the past eighteen months, and their source and the response by businesses have continued to evolve into the second half of the year.

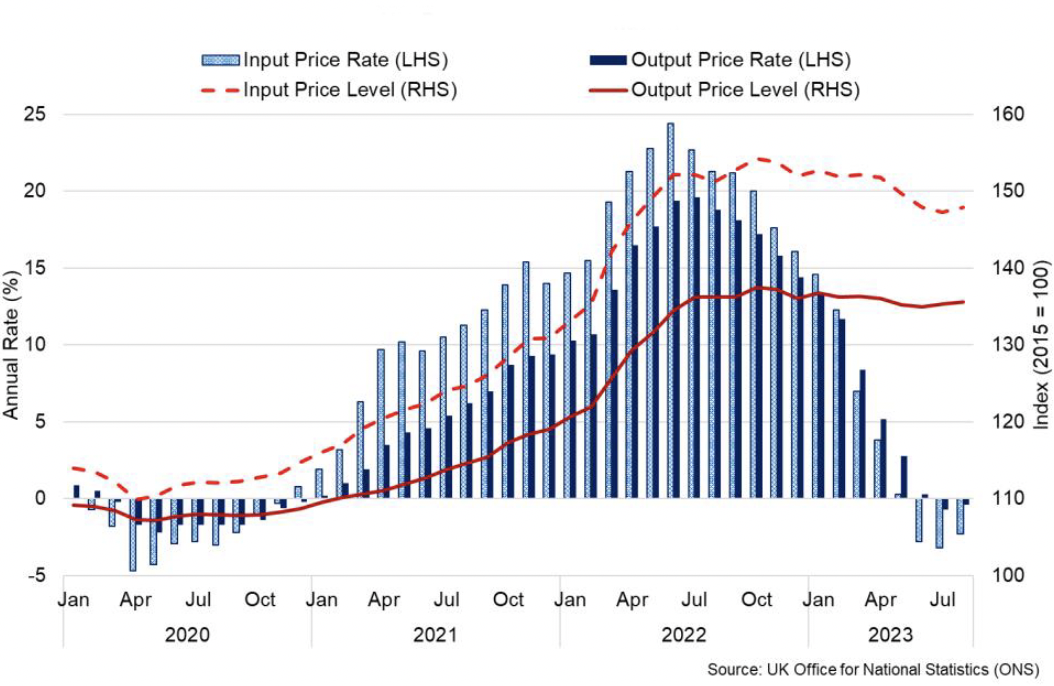

- Producer input price inflation (prices of goods bought and sold by UK manufacturers, including price indices of materials and fuels purchased and factory gate prices) fell by 2.3% over the year to August, their third consecutive month of annual decline with input price inflation having recently peaked at 24.4% in June last year.

- The change in input prices has also been reflected in producer output prices which fell by 0.4% in the year to August, their second consecutive month of decline, down from the recent output price inflation peak of 19.9% last July. [9]

- The moderation of energy and wider commodity price inflation has been a key driver of falling producer price inflation with crude oil input costs falling 21.8%. However food commodity prices have not fallen to the same extent and food materials continued to provide upward cost pressure with imported food materials costs rising 15.1% over the year. Furthermore, while the pace of fuel input cost inflation has eased in recent months, it remained elevated in August at 22.9%.

- Overall, while annual producer price inflation rates have turned negative, with prices in some sectors falling, the index levels for input and output prices are 27.4% and 23.8% higher than at the start of 2021, illustrating the rapid rise in producer price levels over this period as a whole.

- Looking across a broader range of input costs (energy, materials and staffing) the PMI business survey indicates that cost burdens continued to rise in August, albeit at a significantly slower rate than over the past year and at one of its lowest rates since February 2021.[10]

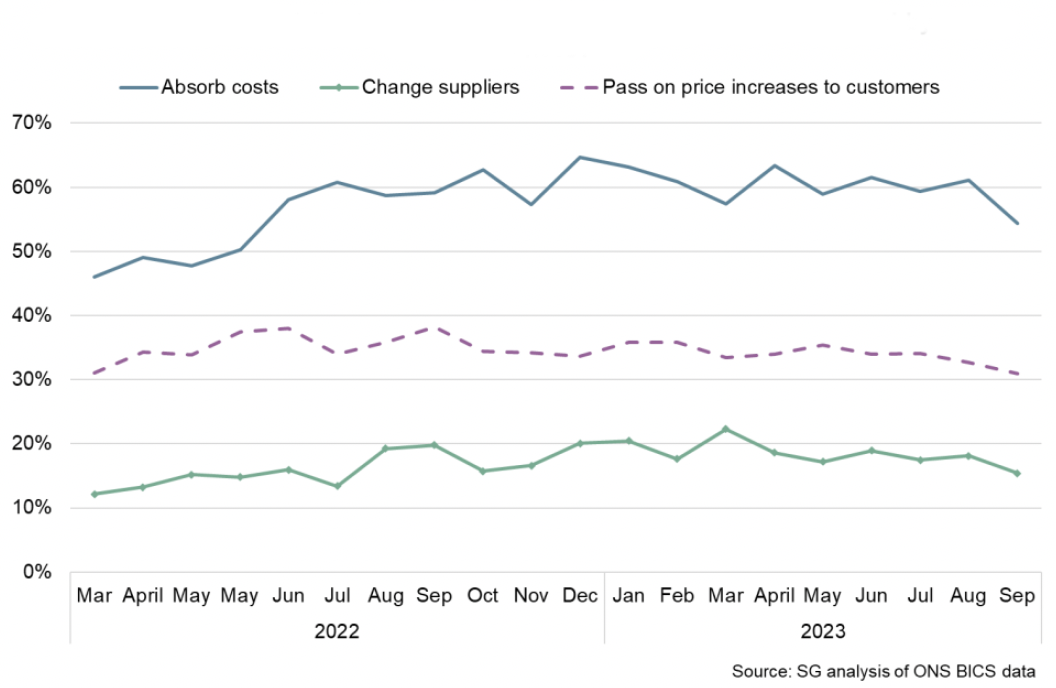

- BICS data for Scotland provide latest insights into the effects on businesses of price rises. In September, 54% of businesses reported that they had to absorb costs, 31% reported having to pass on price increases to customers and 15% had to change suppliers. A much lower percentage of firms reported having to reduce staff work hours (3.4%), make redundancies (1.9%) or access more financial support (7.8%), however the latter has been on an upward trend.[11]

- Both the scale and persistence of cost increases is an issue for firms. The Scottish Business Monitor highlights the risk to the ability of businesses to continue absorbing costs going forward. The survey for Q2 2023 found that 74% of those firms absorbed up to 50% of their increased costs. However, 35% of firms reporting that they cannot absorb costs anymore, 36% of firms expect to only be able to absorb costs for the next year, and 14% of firms are unsure how much longer they can absorb costs for.[12]

Business Investment

- The combination of business concerns around inflationary pressures, higher interest rates and weakening demand is impacting on business investment decision making.

- The Scottish Business Monitor indicates business investment remained weakened in the second quarter of 2023, with 40% of businesses cancelling or delaying planned investment over the last 12 months. Reported reasons were economic uncertainty (75%), affordability (71%) and borrowing costs (38%).[13]

- The Scottish Chambers of Commerce Quarterly Economic Indicator reported a similar stalling in businesses investment (particularly in training investment) with over half of those in financial and business services reporting no change in investment, the retail sector observing a notable fall in capital investment and over half of firms in tourism reporting that they had pulled investment altogether. [14]

- At a UK level, the Bank of England Agents' Summary of Business Conditions for Q3 2023 indicated that business investment intentions, particularly construction, remained subdued due to higher investment costs and pressure on cash flow and margins, while investment intentions in IT, digital and automation remained stronger.[15]

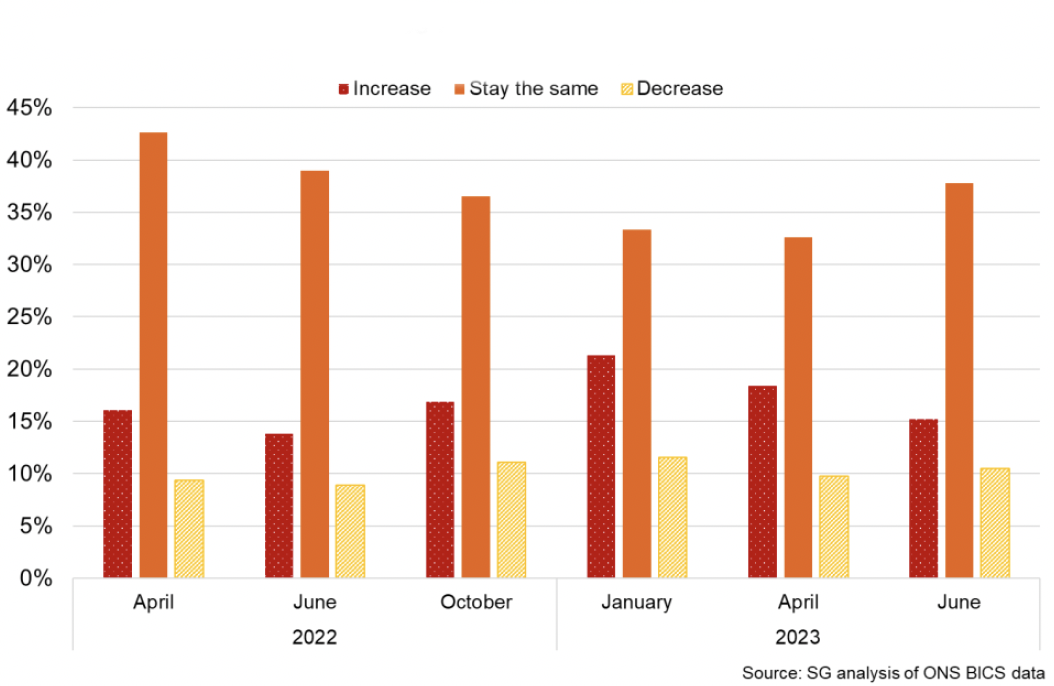

- BICS data for Scotland at the end of June and start of July show 15.2% of respondents thought their capital expenditure would increase over the next three months, showing a slight improvement from the middle of last year but lower than the start of this year, while around 10.5% of respondents continue to expect to decrease capital expenditure over the coming year.

Business Optimism

- Looking ahead PMI business survey data indicates that business confidence remains positive on balance however has fallen to its weakest rate since the start of the year, reflecting the ongoing challenging economic environment, inflationary pressures and recruitment challenges.[16]

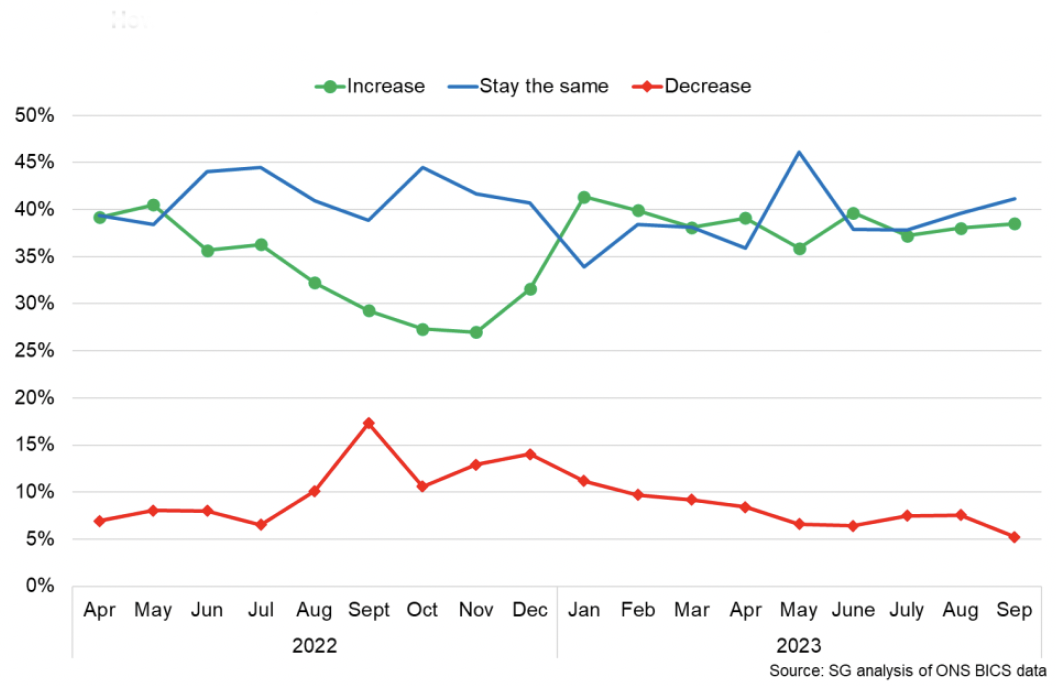

- BICS data for Scotland also indicates that the level of business optimism has eased from the start of the year and has been stabilising between July and September with 39% of firms expecting their performance to increase, 5% expecting it to decrease and 41% expecting it to stay the same.[17]

Contact

Email: OCEABusiness@gov.scot