Publication - Research and analysis

Scottish economic bulletin: December 2023

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Economic Outlook

Forecasts continue to indicate positive but subdued GDP growth for the year ahead.

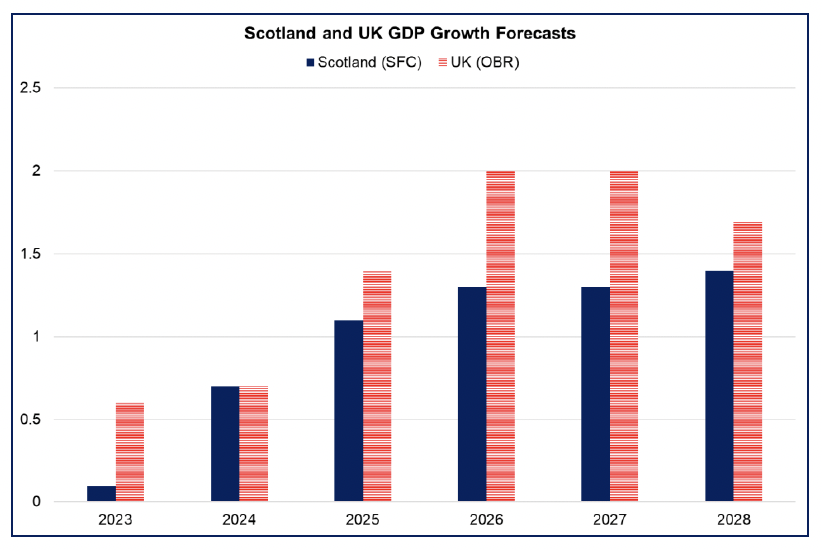

- Economic growth has remained more resilient in 2023 than was previously forecast, having been forecast in December 2022 to enter a shallow recession. However, the outlook for growth for 2024 remains subdued, with inflation expected to fall back to the 2% target more slowly than previously forecast and interest rates expected to remain higher for longer.

- The Scottish Fiscal Commission forecast the Scottish economy to grow 0.7% (previously 0.9%) in 2024, rising to 1.1% in 2025 (previously 1.3%). This is broadly in line with the OBR forecasts for the UK economy for growth of 0.7% in 2023 rising to 1.4% in 2024.[21],[22]

- The lower profile of growth in Scotland compared to the UK over the forecast period is mainly due to slower total population growth in Scotland.

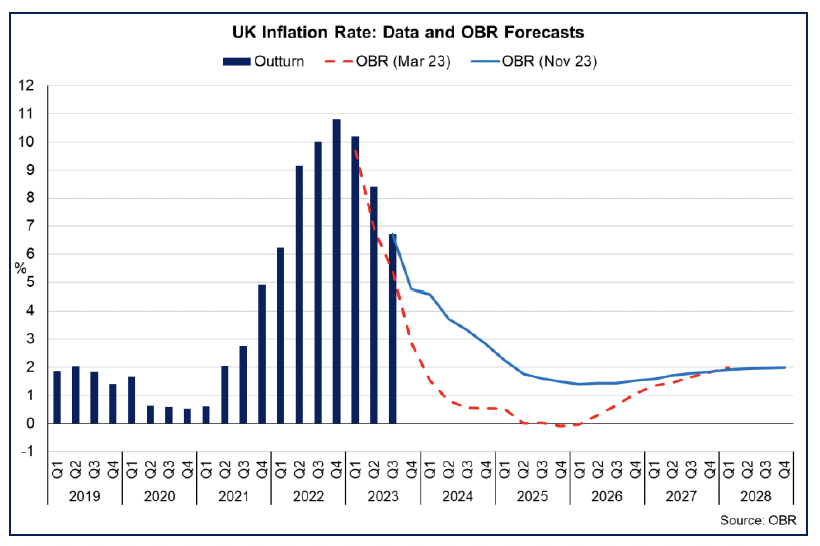

- The SFC forecast assumes inflation will fall from its October rate of 4.6% to 3% over the coming year and return gradually to the Bank of England’s 2% target rate by mid-2025. This decline is slower than previously forecast and reflects the greater than expected persistence in domestic inflationary pressures.

- Reflecting this persistence, the Bank of England, alongside the US Federal Reserve and the European Central Bank, has continued to retain a restrictive monetary policy position with Bank Rate held at 5.25% since August. In their latest forecasts from November, markets expect the Bank Rate to remain around 5% until the end of 2024 before settling to around 4% by the end of 2026.

- Overall, the resilience in economic output and the labour market, coupled with easing inflation pressures over the year has been positive. In the short term business survey data point to business activity weakening in the latter part of 2024, and the persistence of above target inflation and higher interest rates continue to present a challenging outlook. However the resilience of business optimism for the coming year, the resilience in the labour market and earnings growth and the improvements in consumer sentiment over the past year provide a strengthening basis for the growth forecast in 2024.

Contact

Email: OCEABusiness@gov.scot