Publication - Research and analysis

Scottish economic bulletin: December 2023

Provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Labour Market

Unemployment remains low while earnings growth is robust but some sectors continue to face labour shortages.

Employment, Unemployment and Inactivity

- Labour market conditions have been very tight since the start of 2022 and have been resilient in the face of subdued GDP growth and inflationary pressures. This has been characterised by low unemployment, strong demand for labour with elevated vacancy rates and some companies reporting staffing shortages.

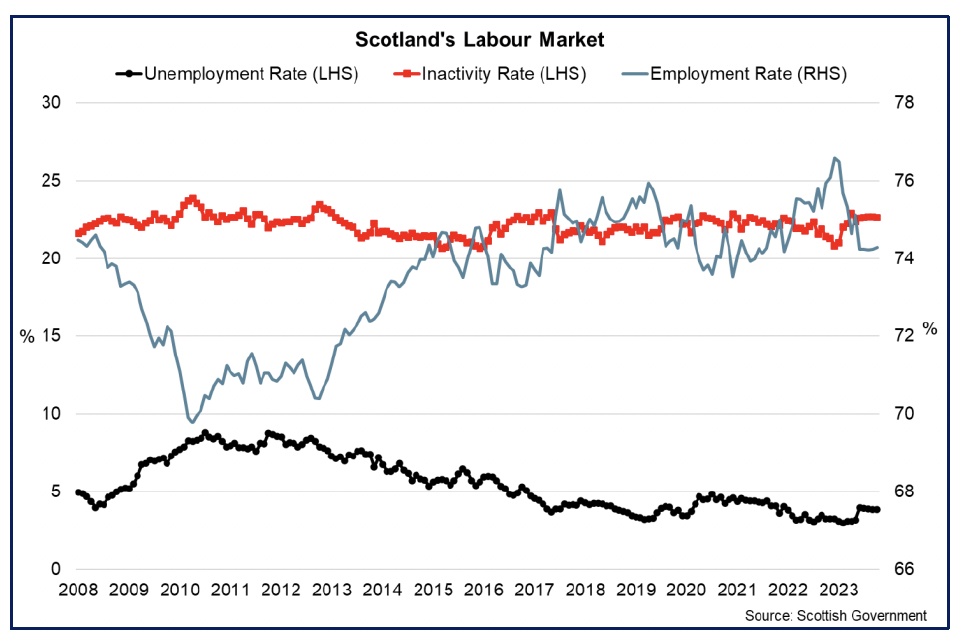

- Adjusted experimental statistics for August to October show that Scotland’s unemployment rate fell over the quarter to 3.8% (UK: 4.2%), while employment rose by 5,000 to an employment rate of 74.3%, and the inactivity rate remained unchanged at 22.6%.[10],[11]

- Labour market conditions have softened slightly over the last year as a whole, with the employment rate falling 1.7 percentage points while the unemployment rate has increased 0.6 percentage points and the inactivity rate has risen 1.2% percentage points.

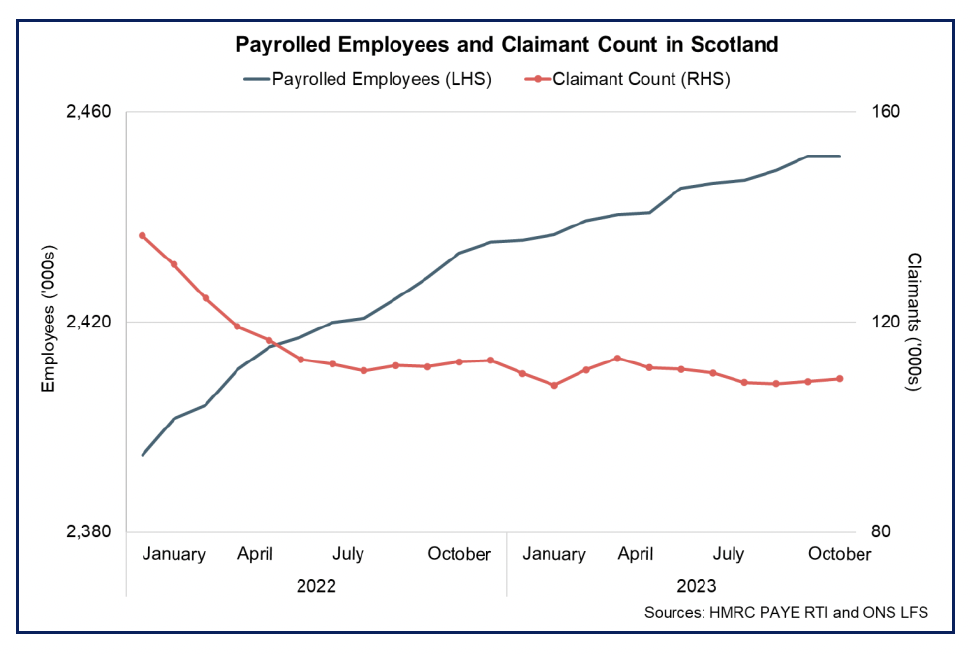

- Wider labour market data illustrates further the resilience in the labour market, indicating recent trends have remained broadly stable. The number of PAYE employees in Scotland continued its upward trend since the start of the year to 2.45 million, though was largely unchanged over the month of November, while Scotland’s claimant count rate remained unchanged at 3.6% though the number of claimants rose slightly over the month to 109,218.[12],[13]

Recruitment Activity

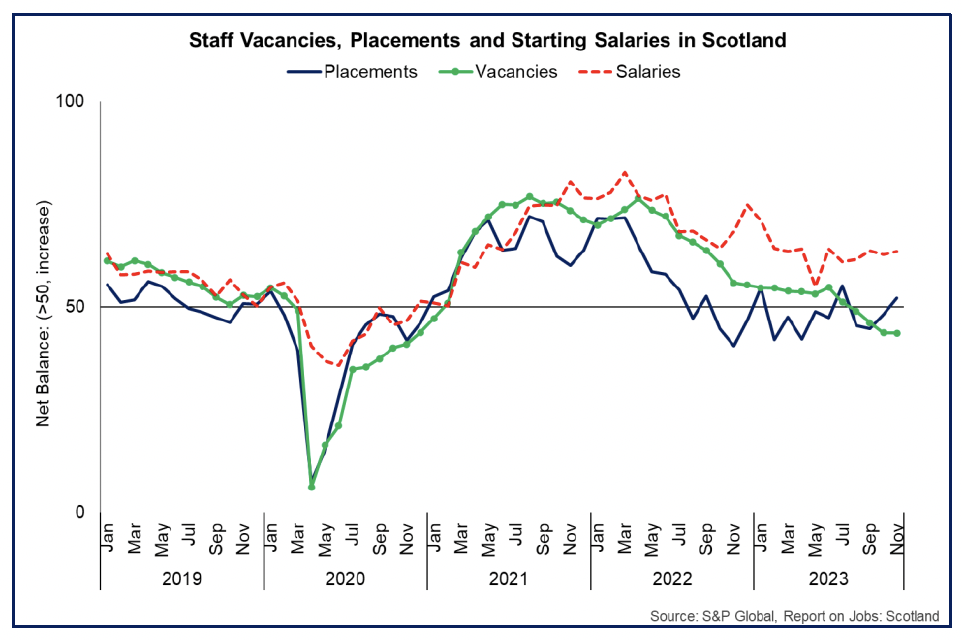

- Business survey data also signal that the extent of tightness in the labour market following the pandemic has cooled slightly over the course of the year as unemployment has remained low and recruitment activity has stabilised.

- The RBS report on Jobs for November signalled positive growth in permanent staff placements for the first time in four months (52.3), however business demand for staff fell for a fourth consecutive month and to its lowest level in three years (43.7).[14]

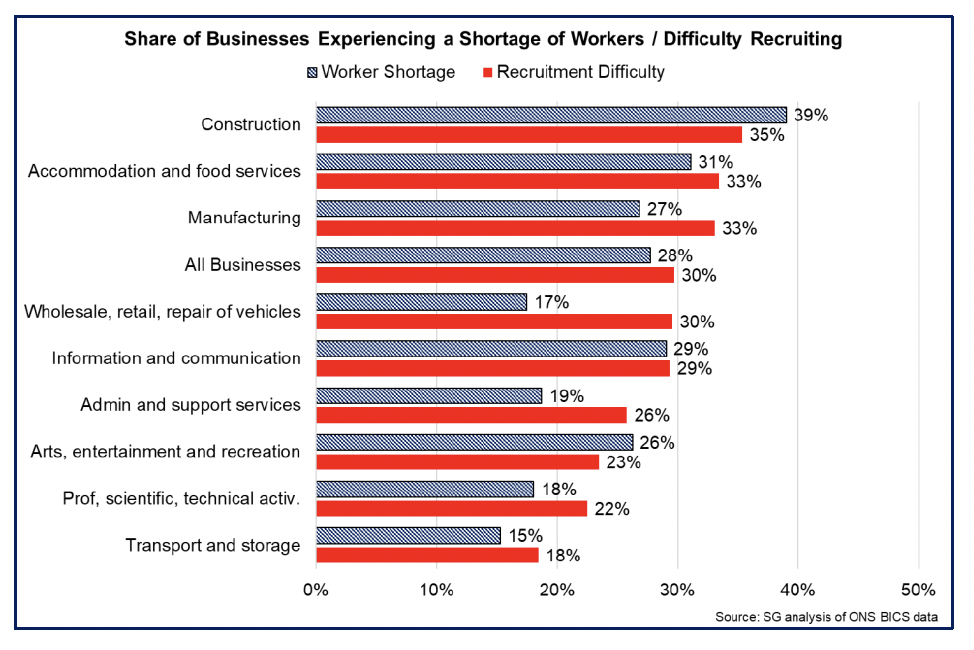

- BICS data provides further insights on labour shortages and recruitment challenges across sectors, which have been gradually easing over the past year. In November, 27.7% of businesses reported experiencing a shortage of workers (down from 43.4% in November 2022) and in October, 29.7% reported experiencing difficulties recruiting employees (down from 39% in October 2022).

- At a sector level, worker shortages remain most reported in Construction (39%) and Accommodation and Food Services (31%), with most businesses (53%) reporting that worker shortages led to employees working increased hours or the business was unable to meet demands (34%).

- Recruitment difficulties were also most reported in the Construction sector (35%) alongside Accommodation and Food Services (33%). Latest data from October shows most businesses responded that a low number of applications (50%) and a lack of qualified applicants (55%) were reasons for why they experienced difficulties in recruiting employees, while 28% reported not being able to afford an attractive pay package to applicants.

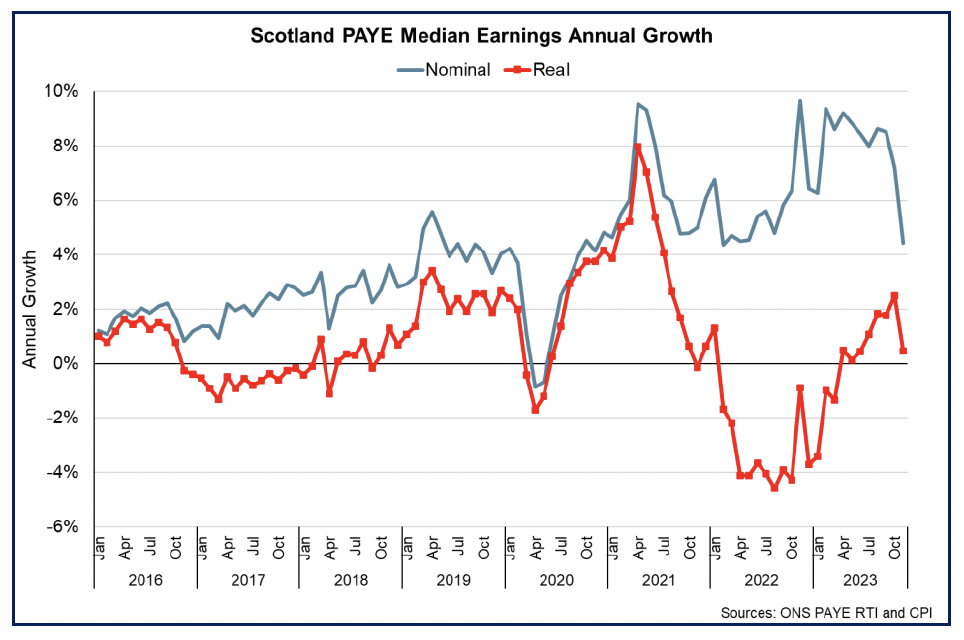

Earnings

- Recruitment challenges, staffing shortages and inflationary pressures have generated upward pressure on earnings over the past year, however there are indications that this has started to ease.

- The RBS Jobs Report for November indicates that growth in starting salaries remains robust (net balance of 63.6), though the pace of growth has softened compared to the start of the year (71.0 in January 2023).

- More broadly, nominal median monthly PAYE pay in Scotland was £2,334 in November, up 4.4% over the year. This remains above the average annual growth rate over the past eight years (4.0%), however has slowed from higher rates of growth recently (7.2% in October) and to its slowest pace since November 2020.[15]

- Adjusting for inflation, which was 3.9% in November, real median earnings grew 0.5% on an annual basis. This was the eighth consecutive month of positive growth following the period of falling real pay during 2022 and the start of 2023, reflecting the easing in inflationary pressures in recent months.

- Looking ahead to over 2023-24 as a whole, the Scottish Fiscal Commission Forecast average nominal earnings in Scotland to grow 6.6% over the year, faster than the OBR forecast of 6.2% for the UK as a whole.

Contact

Email: OCEABusiness@gov.scot