Rural Scotland Business Panel Survey October 2022

This report presents findings from the third Rural Scotland Business Panel Survey carried out in June and July 2022.

5. Viability

Key findings

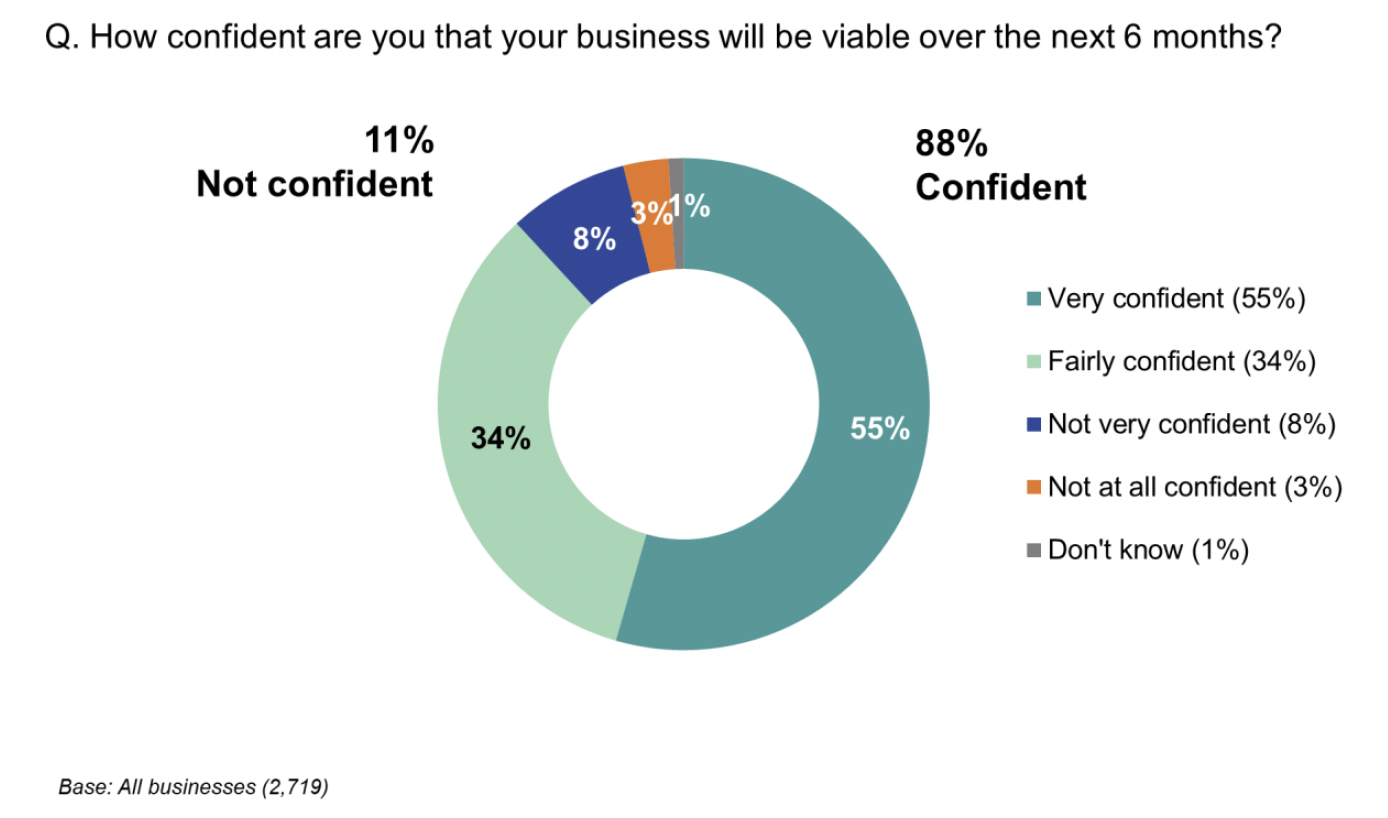

The majority (88%) of businesses were confident that their business would be viable over the next six months, while 11% were not.

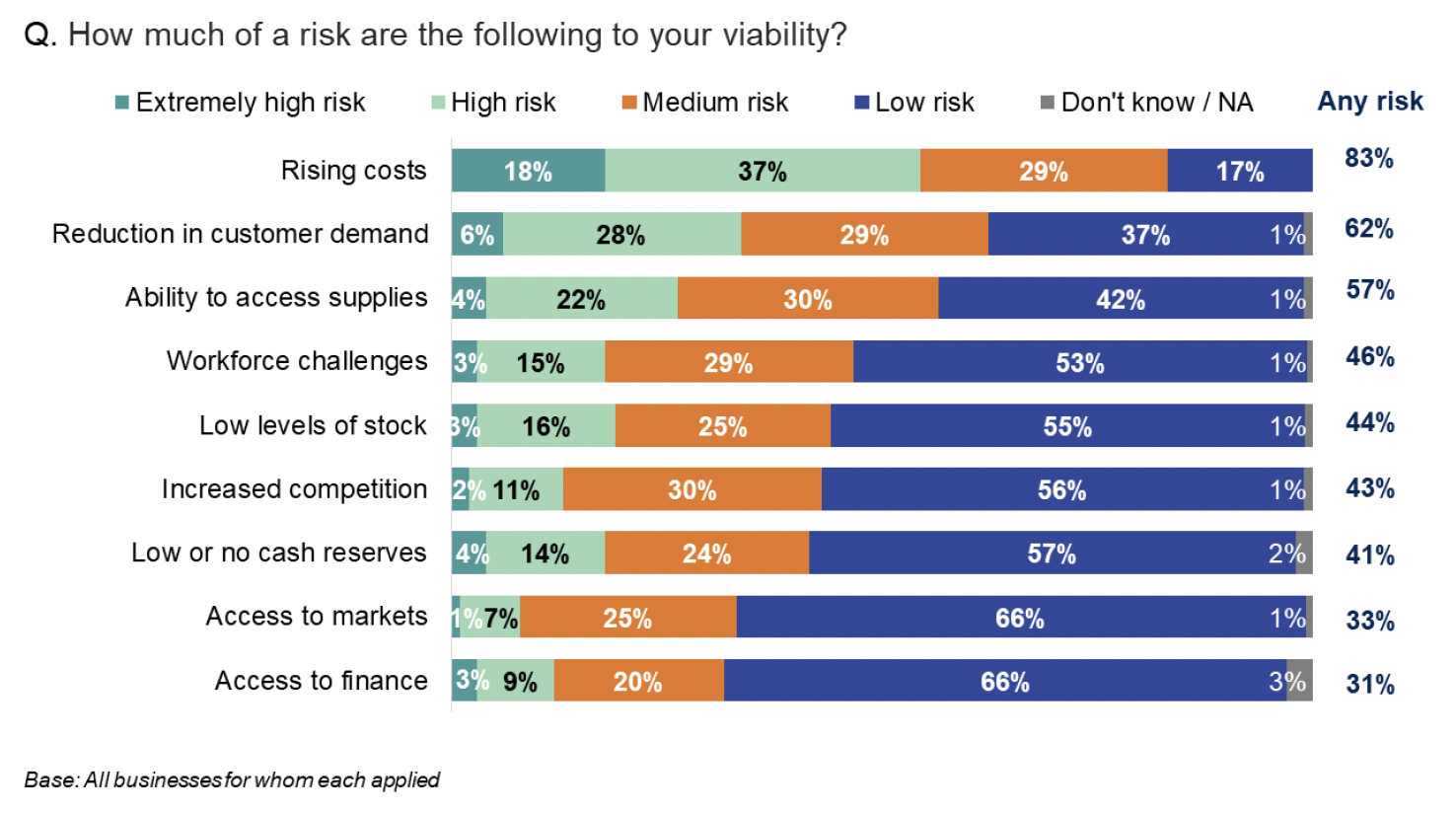

The biggest perceived risk to viability was rising costs (83% said it was at least a medium risk). This was followed by reduction in customer demand (62%) and ability to access supplies (57%). Over four in ten felt workforce challenges (46%), low levels of stock (44%), increased competition (43%) and low or no cash reserves (41%) were risks, while around a third mentioned access to markets (33%) and access to finance (31%).

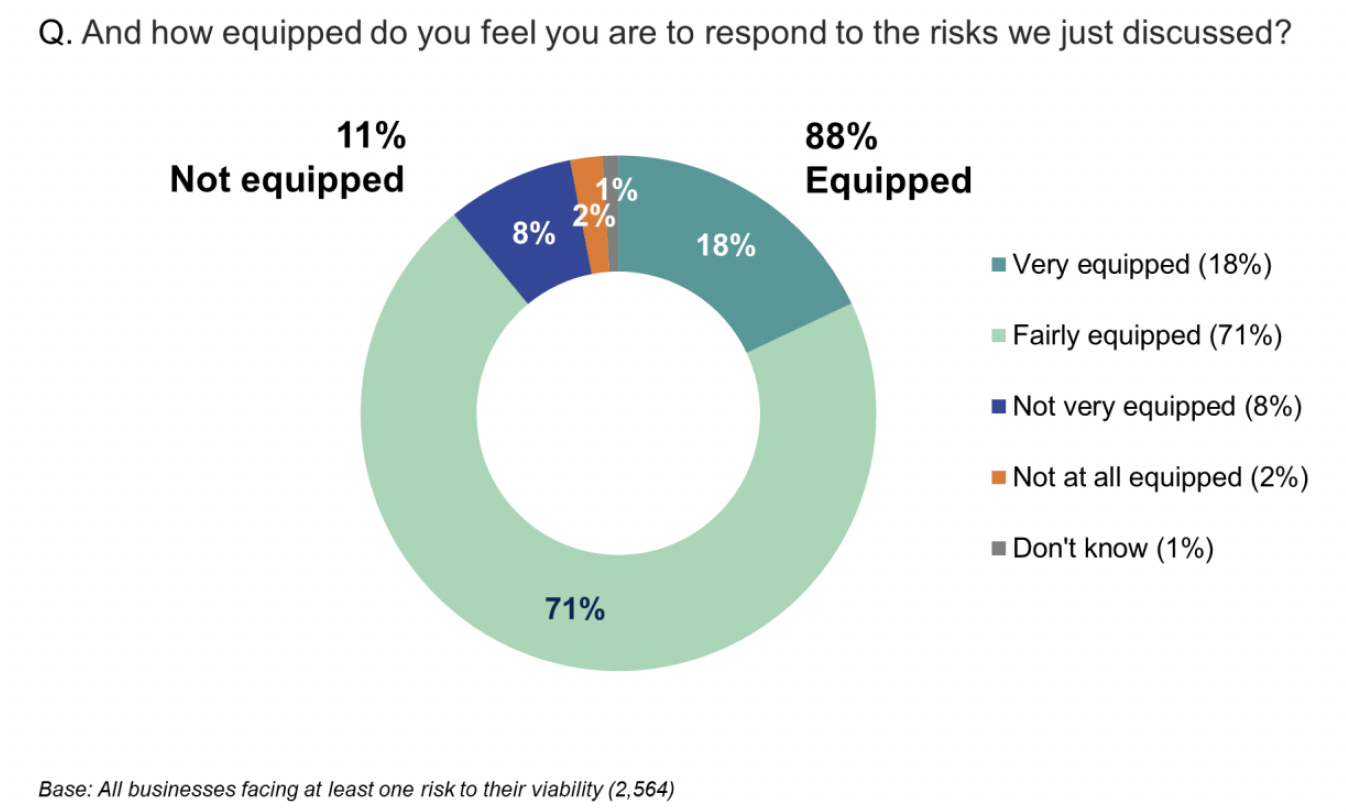

Most businesses (88%) felt equipped to respond to risks to their viability, while 11% did not.

Confidence in business viability

The majority (88%) of businesses were confident that their business would be viable over the next six months, while 11% were not (Figure 5.1).

Variation in confidence

Confidence in business viability was higher than average among:

- businesses in the Highlands and Islands (91%) and South of Scotland (91%) compared to the rest of rural Scotland (87%),

- businesses with 5-10 (94%, 11-24 (94%) or 25+ staff (95%), and

- financial and business services businesses (93%).

Confidence was lower than average among:

- those with 0-4 staff (12%),

- tourism businesses (15%),

- busineses in remote rural areas (13%),

- those impacted by EU Exit (13%), COVID-19 (13%) and rising costs (12%), and

- those behind where they wanted to be on competitiveness (25%), skills development (19%), productivity (18%), and adoption of technology (14%).

Risks to viability

The biggest perceived risk to viability was rising costs (83% said it was at least a medium risk). This was followed by reduction in customer demand (63%) and ability to access supplies (57%).

Over four in ten businesses felt workforce challenges (47%), low levels of stock (43%), increased competition (44%) and low or no cash reserves (42%) were risks, while around a third mentioned access to markets (33%) and access to finance (32%) (Figure 5.2).

Variation in risks to viability

In terms of sectoral variation:

- Tourism businesses were more likely than average to feel at risk from rising costs (91%), reduction in customer demand (72%), ability to access supplies (63%) and access to finance (37%).

- Food and drink businesses were more likely to feel at risk from: rising costs (89%), ability to access supplies (69%), workforce challenges (55%), access to markets (38%) and access to finance (37%).

- Creative industries were more likely to feel at risk from a reduction in customer demand (72%).

The following businesses were more likely than average to say most of these issues was at least a medium risk:

- Businesses operating below pre-pandemic levels

- Those striving for growth and seeking new ways of doing things

- Those impacted by EU Exit, COVID-19, the Russia-Ukraine conflict and rising costs

- Those behind where they would like to be on productivity, competitiveness technology adoption and skills performance

- Those importing from outside the UK.

Ability to respond to risks

Most businesses (88%) felt equipped to respond to risks to their viability, while 11% did not (Figure 5.3).

Variation in ability to respond to risks

The following businesses were less likely to feel equipped to respond to risks to their viability:

- Food and drink (15% not equipped) and tourism businesses (15%)

- Those operating below pre-pandemic levels (16%)

- Businesses impacted by COVID-19 (13%) and rising costs (12%), and

- Those behind where they would like to be on competitiveness (23%), skills development (18%), adoption of new technology (17%) and productivity (17%).

Ability to respond to risks was similar for each of the individual risks that businesses were experiencing (see Appendix A).

Contact

Email: socialresearch@gov.scot