Rural Scotland Business Panel Survey February 2023

This report presents findings from the fourth Rural Scotland Business Panel Survey carried out in October and November 2022.

6. Financial concerns and access to finance

Key findings

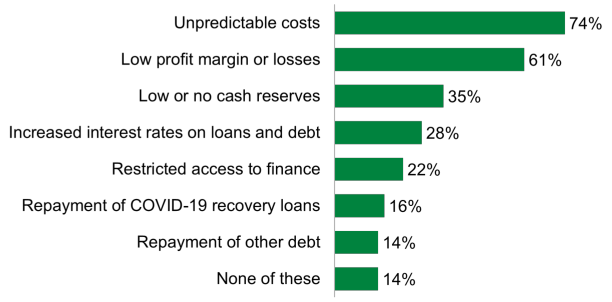

The majority of businesses (85%) had financial concerns, with the top concerns being unpredictable costs (74%) and low profit margins or losses (61%). Other concerns were: low or no cash reserves (35%), increased interest rates on loans and debts (28%), restricted access to finance (22%), repayment of COVID-19 recovery loans (16%) and repayment of other debt (14%).

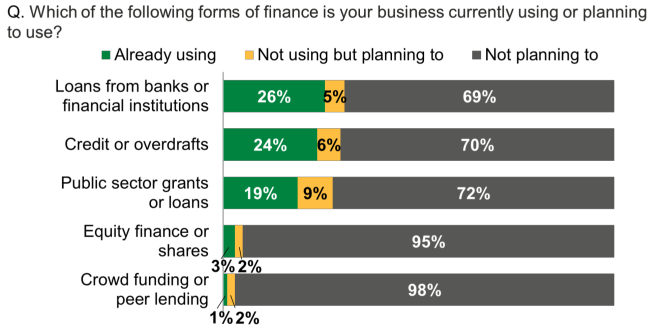

Around two in five (44%) businesses were currently using or planning to use some form of finance, a decrease since October/November 2021 (when 55% were doing so). Around a third of businesses were already using or planning to use loans from banks or financial institutions (31%) or credit or overdrafts (30%), while over a quarter were already using or planning to use public sector grants or loans (28%).

Financial concerns

The majority of businesses (85%) had financial concerns, with the top concerns being unpredictable costs (74%) and low profit margins or losses (61%). Other concerns were: low or no cash reserves (35%), increased interest rates on loans and debts (28%), restricted access to finance (22%), repayment of COVID-19 recovery loans (16%) and repayment of other debt (14%) (Figure 6.1).

Variation in financial concerns

Tourism and food and drink sectors were more likely than average to have these financial concerns:

- Tourism – unpredictable costs (87%), low profit margins or losses (70%), low or no cash reserves (43%), increased interest rates (37%) and repayment of other debt (21%).

- Food and drink– unpredictable costs (83%), low profit margins or losses (69%), increased interest rates on loans and debt (42%) and repayment of other debt (19%).

There was also variation in relation to location, size and ownership:

- Remote rural businesses[12] – unpredictable costs (77%).

- Accessible rural – increased interest rates (34%) and repayment of other debt (16%).

- Women-led – low profit margins (74%), low cash reserves (43%).

Businesses that had not performed well, that were unable to plan far ahead and importers were more likely to be concerned about most of these (see Appendix).

Those that had none of these concerns (14%) were more likely be: financial and business services (26%), those that could plan ahead beyond 12 months (24%) and those that have performed well (22%).

Access to finance

Around two in five (44%) businesses were currently using or planning to use some form of finance, a decrease since October/November 2021 (when 55% were doing so). Around a third of businesses were already using or planning to use loans from banks or financial institutions (31%) or credit or overdrafts (30%), while over a quarter were already using or planning to use public sector grants or loans (28%) (Figure 6.2).

Variation

Food and drink businesses were more likely than average to be using each of the most common sources of finance: loans from banks or financial institutions (42%), credit or overdrafts (42%) and public sector loans and grants (23%).

Use of these sources was also higher than average among certain groups of businesses:

- Public sector loans and grants: large businesses (25+ staff) (25%), those able to plan ahead beyond 12 months (24%) and importers (20%).

- Loans from banks or financial institutions: large businesses (25+ staff) (40%), those that had struggled (32%), remote rural business (29%) and both importers and exporters (29%).

- Credit or overdrafts: those that had struggled (30%), remote rural businesses (28%), and importers (26%).

Contact

Email: socialresearch@gov.scot