Architecture and Design Scotland review: background report

A background report setting out the findings and recommendations for reform of the public body, Architecture and Design Scotland, following a review process by Scottish Government.

Annex A

Economic Opportunities in the Creative Industries – Architecture and Design Overview

Based on analysis by the Scottish Government’s Office Chief Economic Advisor (OCEA) and Directorate for Culture and External Affairs

Introduction

Context

This paper considers the creative industries sub-sectors of architecture and design and aims to identify where there are economic opportunities. It explores the current situation, the potential for growth and what more could be done to support these areas of opportunity. It does not propose ways to support the wider creative and cultural businesses in Scotland, but it does present general context on the creative industries sector.

When identifying opportunities, signs of positive economic performance were a pre-requisite. Nonetheless in a wellbeing economy, opportunities cannot be measured by traditional economic statistics alone. Therefore, architecture and design have been assessed against a set of further criteria, making reasonable assumptions about how favourable the support environment and market outlook were, as well as their potential to deliver positive societal change and cultural recognition, bringing reputational and social benefits. Options for policy support are set out, drawing on examples in Scotland, the UK and abroad, and suggest how they might be supported to deliver economic and other outcomes.

Architecture & design within the creative industries

The creative industries sector is very heterogeneous. The sector contains a mix of everything from fine art to software consultancy, from companies offering business services to public entertainment.

The wider contribution of cultural and creative businesses to the wellbeing economy has not been measured in Scotland or elsewhere although there continue to be numerous research projects exploring this here and internationally.[8] [9]This paper does not set out a technical measurement for this, however, informed by wellbeing economy frameworks, reasonable assumptions of the sub-sectors’ wider impact to identify opportunities are included.

This paper reports on desk-based research with some economic analysis and social research carried out by specialists in the Scottish Government’s Office of the Chief Economic Advisor (OCEA). The outcomes are proposed as a starting point to be tested with stakeholders and the sector.

Definitions and Approach

For the purposes of the paper, the ‘creative industries’ are defined as the Scottish Government key growth sector ‘Creative Industries (including Digital),’ a grouping defined by analysts with a data base stretching back to 2008. The ‘creative industries (including digital)’ sector was one of six growth sectors defined in SG’s 2015 economic strategy.

The make-up of the sector is based around SIC codes (which are primary business activity codes). The sector has been considered as 16 sub-sectors, namely: advertising; architecture; visual art; crafts & antiques; fashion & textiles; design; performing arts; music; photography; film & video; computer games; radio & TV; writing & publishing; libraries & archives; software & electronic publishing; and cultural education.

It should be noted the Growth Sector has known limitations in how it defines, divides, and classifies this complex sector and its workforce, particularly in underestimating freelancers (if they are not registered as companies or VAT registered). Also, several sub-sectors including design, report that the sector significantly undervalues their economic contribution. Recent, separately commissioned economic studies, notably of the Scottish screen sector[10], show that when direct and indirect effects are included the total economic effect of sub-sector activity is much higher. Research[11] led by V&A Dundee stated that the majority of design employment and value generated in Scotland is within the wider economy, with 118,000 design jobs in non-design sectors eclipsing the 25,000 in design industries.

Furthermore, as already mentioned, neither of the direct or fuller direct/indirect approaches to valuing the sector measure the more intangible positive effects the creative industries (particularly those with cultural outcomes) can have, to varying degrees, on people’s health and wellbeing, on creating vibrant and cohesive places, or on boosting Scotland’s brand and international reputation. These positive effects are generally acknowledged and yet there is no readily available standard economic value for these impacts so the sector’s total value to the wellbeing economy is not known.

Finally, data and statistics used for economic analysis and comparison comes from 2019. At the time of the report, this was considered the most reliable recent year as subsequent years’ data is less reliable due to the Covid pandemic disproportionately affecting many creative industries. Additionally, certain values within tables and text may have subsequently been updated and may not now match up with equivalent figures in the current version of the industry statistics database. However, the overall picture presented by the analysis is unchanged and the findings robust.

Creative Industries Context

Creative industries sector strengths

- The economic potential of the creative industries sector has grown since globalisation and digitalisation have opened up new markets for cultural and creative services.

- Developed countries, including Scotland, have a comparative advantage in creative industries because their technology and creative sectors are both advanced and they enjoy strong IP protection, which help them develop original services and sell into emerging markets.

- The creative industries are rightly seen as a driver of the economy with the sector making above-average contributions to growth in Scotland’s employment and exports in recent years, although GVA growth has been more volatile.

- In Scotland, the sector has shown particularly strong growth in employment and exports (2013-2019). Over that period, the sector has grown at four times the average rate for Scotland in terms of both jobs and exports.

- The variation in the sector, where one sub-sector ‘software & electronic publishing’ accounts for almost half its economic contribution (49% of GVA), means overall performance figures can mask contrasting performance at sub-sector level.

Identifying sub-sectors with economic promise

- Available data highlights a disparity among the economic performance of its sub-sectors. Some sub-sectors have broadly positive economic results including architecture and design.

- There is no accepted standard way to measure the full economic contribution or opportunity offered by the creative industries and culture in a way more suited to a wellbeing economy.

- Nonetheless, the paper highlights architecture and design as sub-sectors with good economic potential, drawing on economic data with additional assessments of market outlook, favourability of the support environment, as well as considering whether its output has wider positive cultural and societal impacts.

- International practice, with examples in Scotland and Canada, suggest a holistic approach rooted in a specific industry and guided by specialists and its community is the best way to develop a sub-sector in a rounded, long-term way.

Sector background

The creative industries are a relatively new construct. From the 1980s, they attracted policymakers’ attention when several countries, including the UK, and multilateral organisations like UNESCO, began to see them as a new industrial ‘sector’ that could be a driver of economic growth, both for developed and less-developed countries, and a strong key component in making development sustainable.

In the 1980s in the UK, local development strategies (notably that of the Greater London Council) started to view cultural and creative activities less primarily as a source of cultural value and more one of employment and urban regeneration.[12] A whole new set of commercialised providers of cultural and creative goods and services were emerging that were grouped alongside more traditional ones to form the creative industries sector that drew policy-makers’ interest.

Digital and creative industries

The United Nations Conference on Trade and Development (UNCTAD) also said in its 2022 Report[13] that the digital transformation of the creative economy and new and emerging technologies were opening new opportunities for the creative sector. Digital technologies are already creating new avenues for production, distribution, and consumption of creative goods.

Countries that are strong in both creative services and technology have a comparative advantage in the sector. The UK, which is strong in both of these, has seen its creative industries sector grow at 1.5 times the rate of the wider economy over the last decade, contributing £125 billion in GVA in 2022 and supporting over 2 million jobs. (Source: DCMS)[14]

Owning and creating IP that is well-protected also supports creative services’ growth. In its recent State of the Nations report on exports, the Creative Industries Policy, and Evidence Centre (PEC) highlighted this as one of the reasons for developed countries’ such as the UK having an advantage in creative services exports.

Owing to these comparative advantages, the creative industries have opened up new export markets. According to UNCTAD’s Creative Economy Outlook 2022,[15] developed countries accounted for 82.3% of all creative services exports in 2020. Ten countries made up more than two-thirds of global exports with the US as the top exporter of creative services ($206bn) followed by Ireland ($174bn), Germany ($75bn) China ($59bn) with the UK fifth at ($57bn).

The sector has a high level of innovativeness[16] in terms of bringing new products and services to market, as well as a high propensity for spillovers of knowledge and collaboration with other sectors of the economy.

They also bring benefit to the places where they are concentrated, improving community identity and cohesion. Creative industries can increase the attraction of a place and be a draw for innovative businesses and people to relocate.

They contribute to international reputation and soft power. Creative industry products and services can be seen as innovative, world-leading, unique, and entertaining and boost a country’s reputation. This can be measured to some extent in the effect creative services can have on tourism, but there is a wider, more intangible effect in the value a legacy of creativity can bring to a country’s brand.

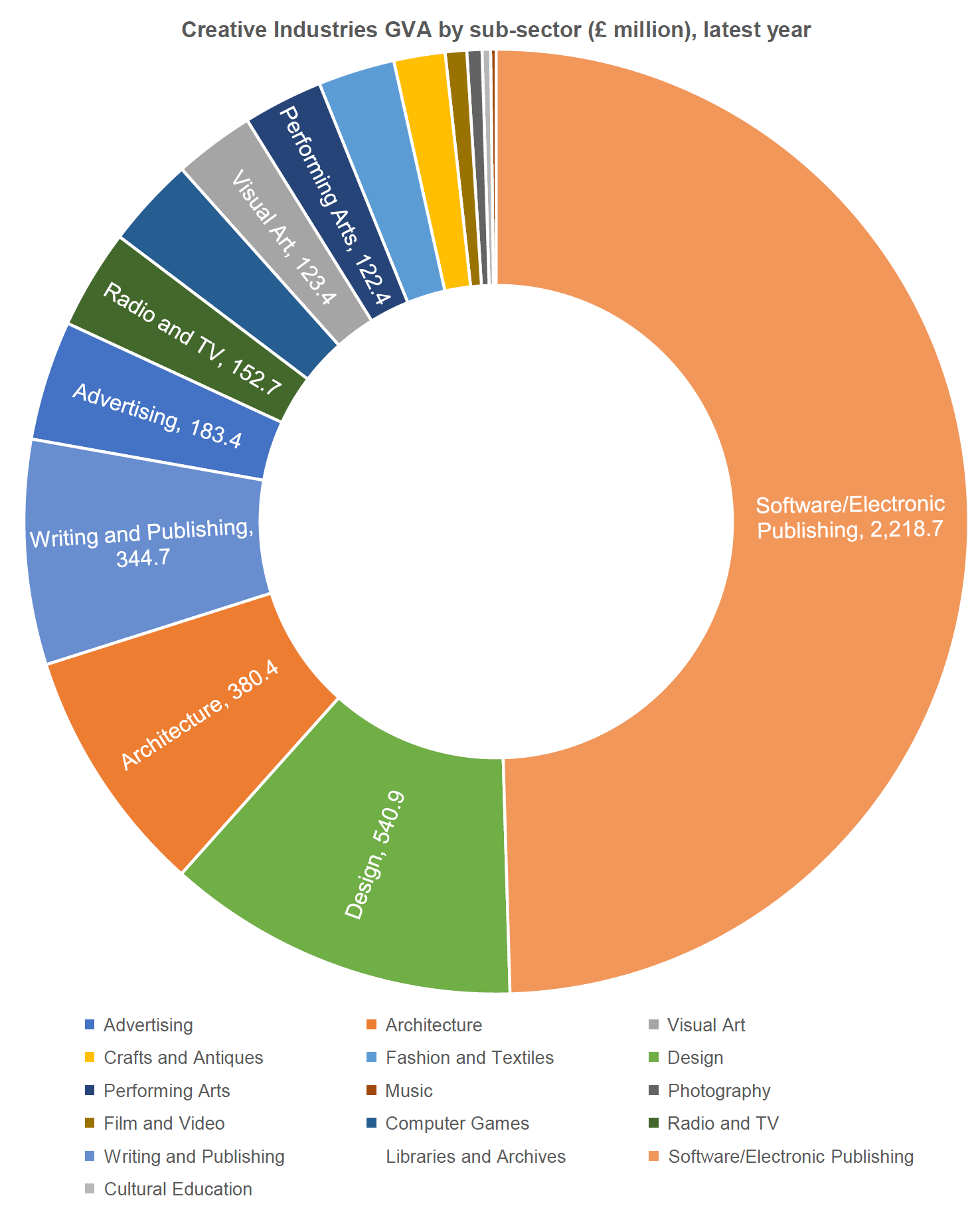

Performance by sub-sector

The chart above illustrates the composition of the sector by the size of sub-sector contribution to GVA in £m.

Key points relating to sector make-up:

Almost half the sector’s value (GVA) comes from a single sub-sector, ‘software & electronic publishing;’ however, this sub-sector does not intuitively seem to have creative or cultural outcomes. The SIC codes that make up this sub-sector include ‘computer consultancy,’ which accounts for 70% of employment and 51% of enterprises with 5+ employees. That activity is likely to have a remit far broader than the creative industries and be more akin to business services.

The ‘design’ sub-sector is made up largely by ‘engineering design activities for industrial process and production’ which seems more related to manufacturing or energy sectors than creative ones. ‘Engineering design activity’ accounts for 78% of all employment in the sub-sector and 41% of enterprises with 5+ employees.

Between them the top five sub-sectors in terms of GVA account for 81% of the creative industries’ total GVA. The software/electronic publishing sub-sector makes up 49% of the total GVA contribution, followed by Design (12%), Architecture (8%), Writing and Publishing (8%) and Advertising (4%).

The following tables show how the creative industries sub-sectors ranked by growth in GVA, employment, number of enterprises and productivity between 2013 and 2019.

Creative Industries: Sub-sector Growth Performance at a glance

Text for graphic below:

Creative Industries: Sub-sector Growth Performance at a glance Growth Rate rankings across indicators for creative industry sub-sectors (2013-2019)

Charts show the ‘at a glance’ growth rate rankings of the 16 Sub Sectors of the creative industries.

Table 1 - GVA (Gross Value Added) – ranked in the following order: 1. Visual Art, 2. Architecture, 3. Computer Games, 4. Crafts & Antiques, 5. Design, 6. Software/Electronic Publishing, 7. Fashion & Textiles, 8. Radio & TV, 9. Film and Video, 10. Photography, 11. Advertising, 12. Performing Arts, 13. Writing and Publishing, 14. Music, plus Libraries & Archives, and Cultural Education, which are not ranked as contributing to GVA rankings.

Table 2 – Employment – ranked in the following order: 1. Cultural Education, 2. Architecture, 3. Film and Video, 4. Software/Electronic Publishing, 5. Radio & TV, 6. Design, 7. Music, 8. Advertising, 9. Computer Games, 10. Crafts and Antiques, 11. Visual Art, 12. Fashion & Textiles, 13. Libraries & Archives, 14. Performing Arts, 15. Writing and Publishing. 16. Photogtaphy

Table 3 – Enterprises – ranked in the following order: 1. Film & Video, 2. Software/Electronic Publishing, 3. Design, 4. Cultural Education, 5. Performing Arts, 6. Crafts & Antiques, 7. Architecture, 8. Visual Art, 9. Fashion & Textiles, 10. Advertising, 11. Music, 12. Radio & TV, 13. Writing & Publishing, 14. Photography, 15. Computer games, 16. Libraries & Archives.

Table 4 – Productivity – ranked in the following order: 1. Visual Art, 2. Computer Games, 3. Crafts & Antiques, 4. Architecture, 5. Photography, 6. Design, 7. Fashion & Textiles, 8. Software/Electronic Publishing, 9. Writing & Publishing, 10. Performing Arts, 11. Radio & TV, 12. Advertising, 13. Film & Video, 14. Music, plus Libraries & Archives, and Cultural Education, which are not ranked as contributing to Productivity rankings.

- Enterprise figures are for enterprises with 5+ employees

- Due to disclosure issues, GVA and productivity figures cannot be provided for libraries and archives or cultural education

There is no single sub-sector that ranks consistently highest in all categories; however, design and architecture have generally good rankings across the different fields.

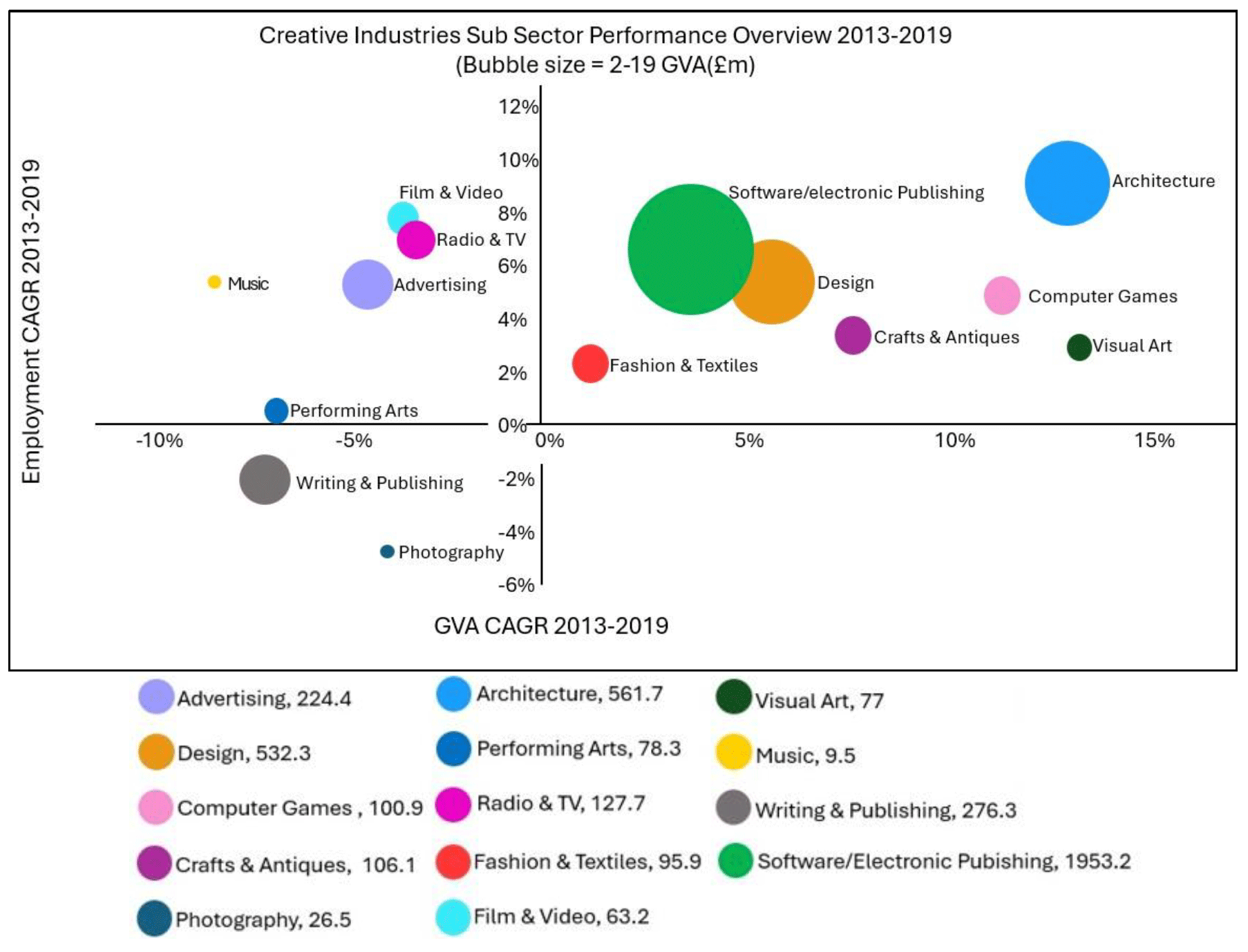

Sub-sector economic impact by size, GVA and employment growth (2013-2109)

This diagram brings together the three key indicators of size (GVA shown by size of bubble), GVA growth and employment growth.

This provides a good visual representation of where opportunity might lie in terms of economic trends. Those in the top-right quadrant show growth in both GVA and employment while all those above the horizontal axis demonstrate employment growth. This presents a picture of consistent positive data for architecture and design.

Architecture and design provide leading opportunities for creative industry sub-sectors growth. The process of identifying opportunity was based on a combination of the following:

1. Economic growth (GVA and employment)

2. Positive support environment – tax credits, support agencies, anchor organisations, specialist high-quality HE provision, funding opportunities, mentorship, business development support, skills, talent development

3. Positive market outlook – expectations of global demand, risks, threats

4. Strong professional community – informed, committed, ambitious

5. Potential to deliver cultural outcomes and reputational prestige, particularly with new IP – films/games, buildings, unique goods/services, aesthetic, imaginative output

6. Potential to contribute to place and community

7. Potential to resolve societal problems (health, loneliness, net zero)

Exports

Many creative industries are internationally focused, and creative industries account for 4.7% of total Scottish exports, ranking the industry fourth overall out of the Growth Sectors (2013-19).

While the industry is comparatively small, it has seen the highest Compound Annual Growth Rate (CAGR) out of all the Growth Sectors at 7.6%, which is four times greater than the growth rate seen for Scotland, demonstrating the strong performance the industry has seen in exports markets in recent years.

An important reason why exports in the sector are particularly valuable to Scotland is that 90% of the value of service exports from the creative industries is created domestically compared to 70% in manufacturing. This means a creative industry export is worth more to the domestic economy.

Globally the value of creative service exports has increased rapidly from 2010-2020, while creative goods exports have stagnated. This appears to be primarily driven by the digitalisation of many creative goods. Scotland predominantly produces and exports creative services, which is a positive since this is the aspect of creative industry export performance that is trending upwards.

From 2010 to 2020, global creative industry exports were primarily driven by software services (39.3%) and research and development (32.2%) followed by ‘advertising, market research and architecture’ at 14.8%, audio-visual (8.6%), information (3.5%) and cultural, recreational and heritage services (0.5%). Scotland outstrips the growth sector average and Scotland-wide average across all regional export markets as shown in the chart below:

Creative PEC’s UK Trade in a Global Creative Economy 2024 provides comprehensive analysis of UK creative goods and services exports showing that exports are growing but becoming increasingly concentrated in fewer businesses. The report found that 20% total turnover in the creative industries is generated from overseas exports, though only 7% of creative businesses are producing this. Further, the proportion of exporting creative businesses has lowered from 10% in 2013 to 7% in 2022, ‘the intensity of exports, which is the proportion of overseas turnover in total turnover, has been increasing in the creative industries, to almost 25% in 2023’ (Miaoli et al., 2024: 32).

Key points- exports

1. Generally, although this is a relatively small sector, economic results are positive in terms of GDP, GVA, employment and export growth

2. Employment is concentrated, with just under 1% of companies accounting for nearly 30% of the workforce.

3. Also, just under 2% of businesses were registered abroad, but they accounted for 27.1% of employment in this sector.

4. UK research on exports by Creative PEC[17] suggest exports are also likely to be concentrated in a very few number of companies.

Architecture sub-sector performance[18]

Overview

- Architecture is the best performing creative industries sub-sector looking at combination of GVA and employment growth (2013-19)

- Strong community with active professional body (RIAS) and public sector sponsor body A&DS

- Sector asking for more business development support and brand building

- Potential to add societal value through enhancing the benefits of good places for health, wellbeing, social interaction, resilience, and social cohesion.

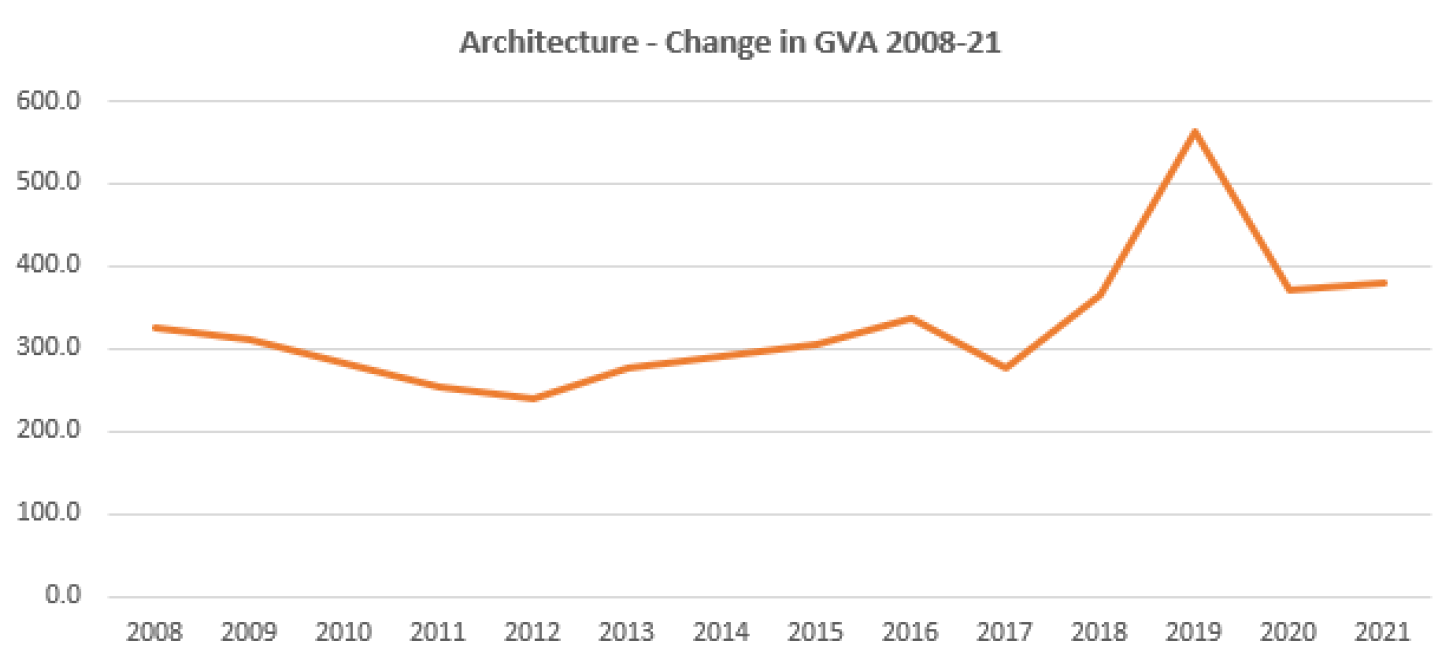

In numbers

SIC 71.11: Architectural activities

- GVA (2019) - £561.7m

- Employed (2019) – 10,000

- Employment growth (CAGR 2013-19) – 9.2%

- GVA growth (CAGR 2013-19) – 12.6%

Performance might be even stronger if a broader definition of sub-sector were used, as it is by other bodies. There are other SIC codes related to architecture. OCEA analysis suggests if they were included, the sub-sector’s performance could be higher.

Key points

- In terms of overall growth, architecture is the best-performing sub-sector in the creative industries sector based on its combined 2013-19 compound annual growth rates for GVA (12.6%) and employment (9.2%).

- Architecture was the second-largest creative sub-sector by GVA in 2019

- Strong productivity growth of 3.1% from 2013-2019, well above the creative industry negative average of -1.5% and the average for Scotland as a whole of 1.9%.

- 23% of architecture firms in Scotland have five or more employees, well above the Scottish industry average of 12.3%. Additionally, 6.8% of all architecture firms had over 20 employees, indicating a strong presence of larger established firms within the sector

- Architecture is one of the strongest performing export sub-sectors in the creative industries; the category of ‘advertising, market research and architecture’ is estimated to account for 14.8% of global creative service exports

- There is strong opportunity for architecture to contribute towards societal value through the impact of places on quality of life and environmental outcomes.

Support & funding

- Architecture & Design Scotland (A&DS) is the public body that works to help deliver Ministers’ priorities for place and the built environment by providing leadership on the place principle to help change how Scotland’s places are planned, designed, delivered, and sustained.

- SG supports the public body A&DS with an annual budget of circa £1.5m (2024/25) and a staff of 20 people.

- V&A Dundee receives £3.8m a year funding from SG and is Scotland’s National Centre for Design, which includes architecture.

- Architecture has a strong community in Scotland and industry body RIAS supports its professional development.

Risks/threats

- Capital spending has fallen sharply in Scotland. For example, in February 2024 SG paused all publicly funded health projects for at least two years.[19]

- While some architectural studios that largely depend on public spend on housing and other capital projects are being hit, others are experiencing growth, such as those specialising in repair and reform of existing housing.

- AI – the effect of AI is not clear yet although potentially it could replace jobs and remove need for some design work. Conversely there is good potential for AI to be a useful tool and improve productivity for architect studios. There is a need to upskill businesses in digital and support tech innovations.

- Skills gap – as in other sub-sectors partly because of Brexit. There is a need to break down barriers to international mobility and trade both to increase skilled staff and build business opportunities.

- After the closure of the national centre for design and architecture, The Lighthouse, in March 2020 architecture lost a focal point for the industry. The Lighthouse, sited in a Rennie Mackintosh-designed building was an exhibition centre and tourist attraction promoting Scottish architecture and design to the public.

Market outlook

- RIBA’s Future Trends Survey[20] has recorded an increase in architects expecting workload growth from an index value of -2 in January 2025 to +7 in March 2025

- this survey recorded that 27% per cent of architects' practices anticipated an increase in workloads over the three months from March 2025, while 21% expected a decline. Fifty-two per cent expected workloads to remain stable.

- practices recorded caution on recruitment, with staffing levels around 3% lower than the same period in the preceding year and the relative optimism on workload growth.

Design sub-sector performance

Overview

- Design is one of the better performing sub-sectors in the creative industries growth sector with both employment and GVA growing at a compound annual rate of more than 5% (2013-19)

- Design education in Scotland has been growing against the grain. While in the UK on average there was only 2% growth in enrolment in design studies 2019-22, in Scotland this was up 21%.

- More than half of design industries’ employment in Scotland is in digital design (53.9%) followed by architecture and built environment (31%)

- The design sector says there is untapped potential in what design can contribute in terms of better societal outcomes to financial, social, climate and democratic challenges and are calling on government to use its specialist skills in service design and help champion and sponsor greater use of design skills at all levels of planning and decision-making

- Dundee has a design legacy as UNESCO City of Design and the V&A Dundee Design Museum is located in the city

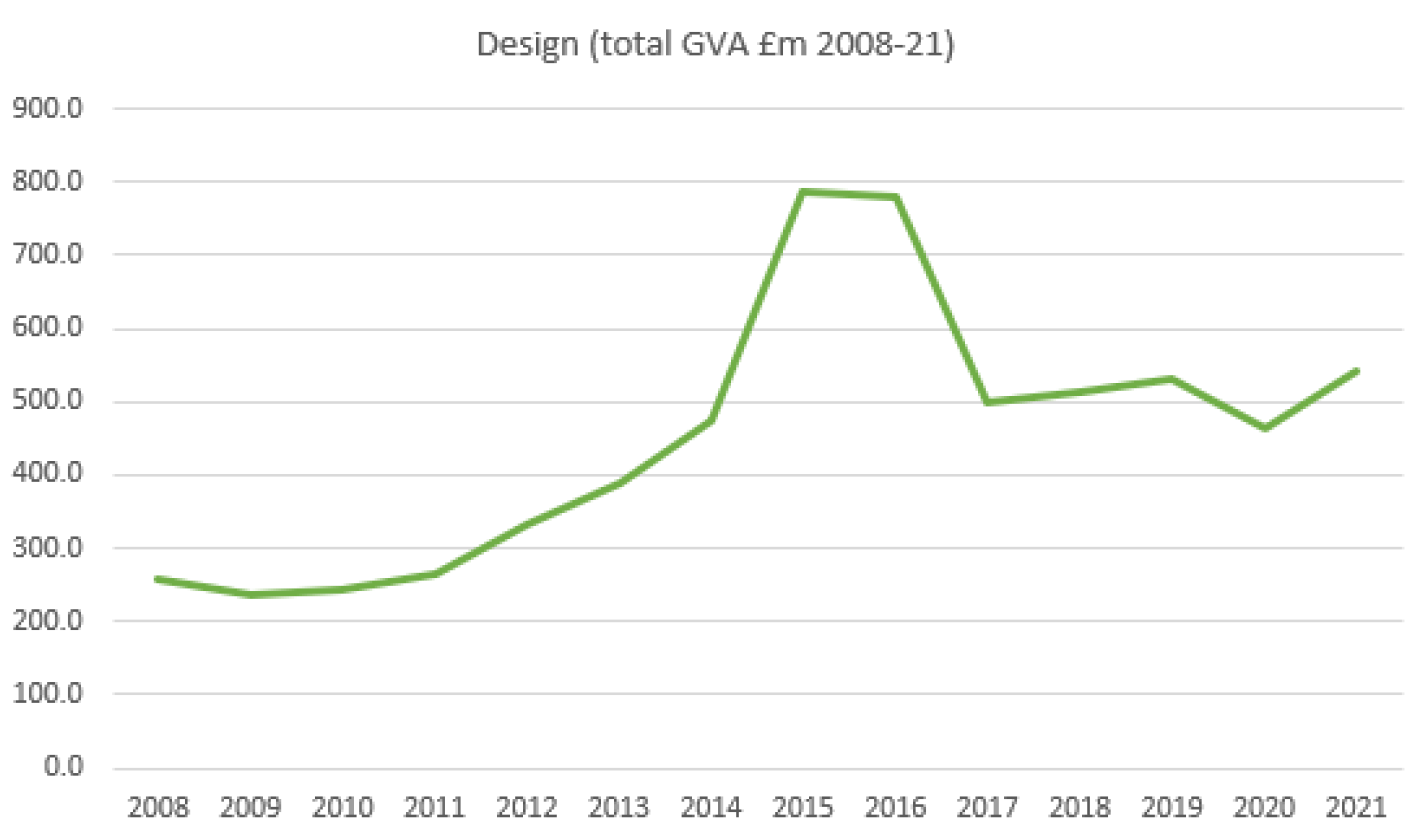

In numbers

SIC 71.12/1: Engineering design activities for industrial process and production

SIC 74.1: Specialised design activities (75%)[21]

- GVA (2021) - £540.9m

- GVA growth (CAGR 2013-19) – 5.3%

- Employed (2022) – 28,250

- Employment growth (CAGR 2013-19) – 5.1%

Note: The sector considers the figures in SG growth sector vastly underestimate activity in Scotland. Research for V&A/CS estimates design in the ‘creative economy’ including in non-design businesses contributes £6.8bn aGVA and employs 137,000 people in total[22]

Key points

- The design sub-sector in Scotland has seen healthy growth over a number of years

- There is a difference in approach between SG growth sector analysis and the Design Council’s. The latter suggests sector development should focus on design in the whole ‘creative economy’ including those working in design jobs in non-design businesses

- Based on Design Council figures, design contributes an estimated £6.8bn GVA and employs 137,000 people in total to Scotland’s economy

- Education in design in Scotland is growing strongly, compared to England where it is stagnant, so Scotland should have greater access to a skilled labour force helping business remain sustainable

- Three Scottish universities rank in the top 100 globally for Art & Design, with Glasgow School of Art consistently in the top 10.

- The V&A Dundee, which has also been named the National Centre for Design in Scotland, is a natural champion for the design community. Has received £3m per year from SG, to rise to £3.8m funding in 2024-25.

- The Scottish Government has a Chief Designer and is a champion of user-centred design across the economy

Risks/threats

- The design community is fragmented into different disciplines and other than architecture does not have a strong unified community or trade organisation in Scotland

- A large part of the design business in the sector is for engineering design, more related to energy or manufacturing. ‘Engineering design activity’ accounts for 78% of all employment in the sub-sector and 41% of enterprises with 5+ employees.[23]

- It is too early to tell if AI will reduce employment or demand but there are risks this could happen

Market outlook

- The UK, through Innovate UK and the Design Council (‘Using Design as a Force for Change’ 2020 strategy) and other countries like Denmark see great market potential in the design skills and design thinking to solve societal problems. However, success in making this an integral part of public and private sector activity requires far greater awareness and understanding of the benefits design can bring.

Summary: growth, output, and societal benefits

Architecture and design are identified as sub-sectors likely to contribute higher growth and value to the Scottish economy with targeted support. Additionally, these creative sub-sectors have good opportunity to develop solutions to societal problems.

Architecture currently receives targeted support from Scottish Government, and this is important given it is an area of economic opportunity, as well as a key cultural practice and asset.

The design sector would benefit from a business community that represents the whole sector and identifying the scale of the opportunity that service design might bring. More work is needed to illustrate and champion the expertise and resource Scotland has here.

Opportunities to support growth may include:

- development of targeted support for architecture, either giving a new remit to the public body supporting architecture and design and/or exploring links with other bodies

- supporting the design sector to build a stronger involved business community as a first step to developing an action plan to enhance its economic potential.

- considering how the needs of these sub-sectors fit with existing domestic support programmes and the International Culture Strategy

- supporting design sub-sector to develop a strengthen links and collaboration across all design disciplines so as to build a plan to help businesses but also find ways to raise awareness of the potential of using design skills across the economy

- explore ways to increase the opportunities for creative industries to help resolve societal issues and raise awareness within the public sector of how creative industries might address key societal priorities

- Strengthen and unify support for the creative industries by using the opportunity of Public Sector Reform. Sectoral development support via one body, or coordinated across multiple agencies, could support economic as well as social and cultural targets. It could be designed with hands-on support and skills in mentoring, talent development, fund-raising, and business development.

- Raise awareness of the successes and products and services of architecture and design, building the profile of a modern Scottish creative identity and supporting exports and domestic activity.

- Sub-sectors like architecture and design have great potential to address societal challenges. There is opportunity to increase awareness and understanding of how creative industry skills could help public and private sector organisations incorporate design steps that increase their effectiveness. Key sectoral bodies such as A&DS, Creative Scotland and V&A Dundee are well placed to support this.

Contact

Email: DirectorPAR@gov.scot