Architecture and Design Scotland review: background report

A background report setting out the findings and recommendations for reform of the public body, Architecture and Design Scotland, following a review process by Scottish Government.

Sector analysis - strategic context and opportunity

4.0 Alongside the functional assessment and stakeholder engagement, the strategic context and growth opportunities in architecture and design were taken into account as part of the review. This principally involved consideration of analysis and research undertaken by Scottish Government’s Office of the Chief Economic Advisor (OCEA) into economic opportunities in the creative industries.

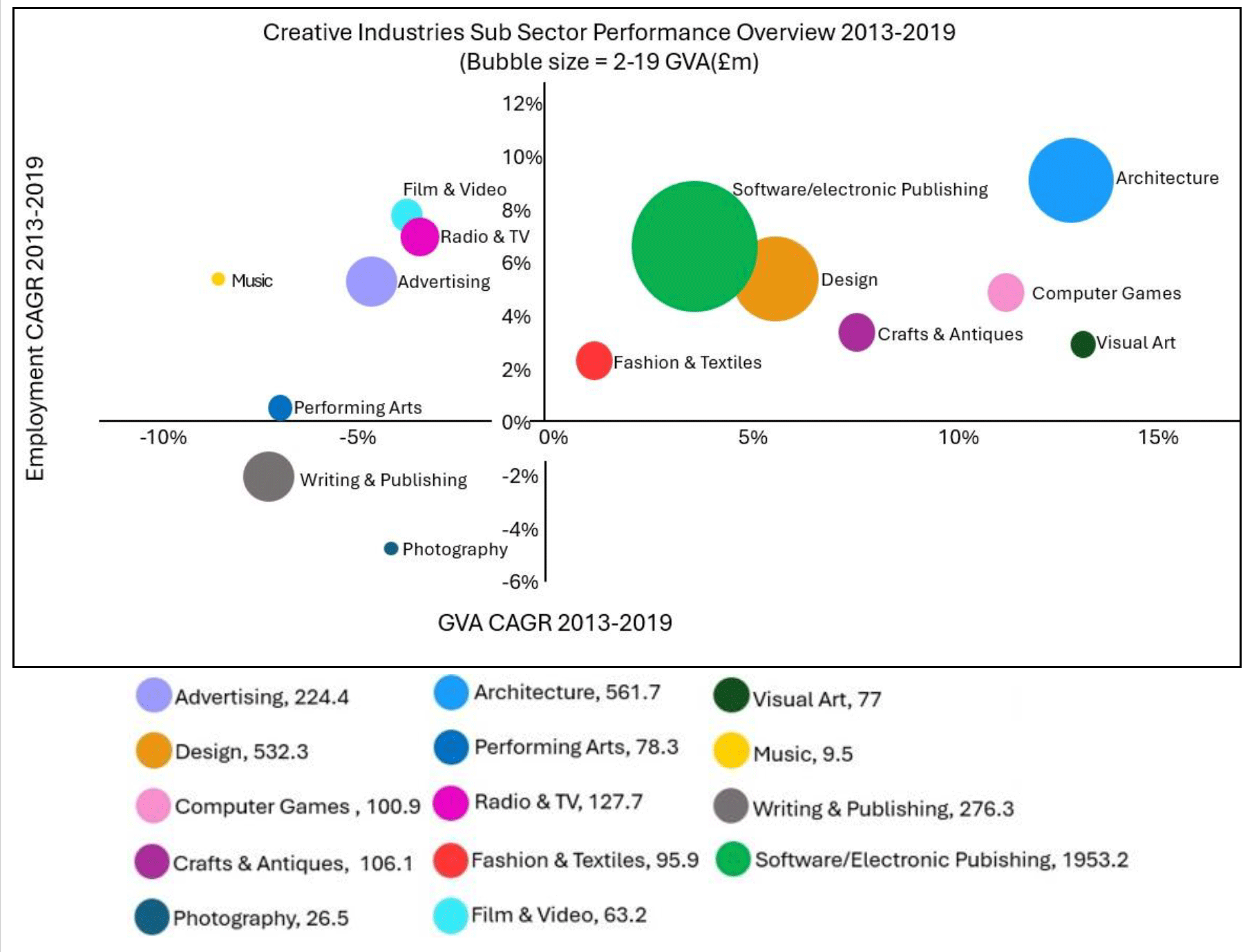

4.1 This analysis captured a profile of the economic performance of the architecture sector (below). The majority of the data used within this analysis is drawn from figures prior to 2019 due to the significant impact of the COVID-19 pandemic on the design and construction sector distorting the typical picture of performance.

Architecture Factsheet[5]

- architecture is the best performing sub-sector of Scottish creative industries looking at combination of GVA and employment growth (2013-19)

- architecture was the second-largest creative sub-sector by GVA in 2019

- architecture showed strong productivity growth of 3.1% from 2013-2019, well above the creative industry negative average of -1.5% and the Scotland average of 1.9%

- 23% of architecture firms in Scotland have five or more employees, well above the Scottish industry average of 12.3%. Additionally, 6.8% of all architecture firms had over 20 employees, indicating a strong presence of larger established firms within the sector

- architecture is one of the strongest performing export sub-sectors in the creative industries; the category of ‘advertising, market research and architecture’ is estimated to account for 14.8% of global creative service exports

- competition in the sector is driven by creativity and reputation

- Scottish architecture has a strong community with an active professional body (RIAS) and public sector body (A&DS)

- the architecture sector requires more business development support and brand building

- Scottish architecture has good potential to add societal value such as through design improvement input to public projects

In numbers:

GVA (2019) - £561.7m

GVA growth (CAGR 2013-19) – 12.6%

Employed (2019) – 10,000

Employment growth - 9.2% (CAGR 2013-19)

Market outlook

- RIBA’s Future Trends Survey[6] has recorded an increase in architects expecting workload growth from an index value of -2 in January 2025 to +7 in March 2025

- this survey recorded that 27% per cent of architects' practices anticipated an increase in workloads over the three months from March 2025, while 21% expected a decline. Fifty-two per cent expected workloads to remain stable

- practices recorded caution on recruitment, with staffing levels around 3% lower than the same period in the preceding year and the relative optimism on workload growth

Economic opportunities in the creative industries

4.2 Architecture is a key sub-sector of the creative industries. It is useful to understand the context and performance of the wider creative industries sub-sectors when considering the potential economic opportunities of Scottish architecture.

Key points

Understanding the creative industries

4.3 The creative industries is a highly varied sector that brings together businesses in the cultural, creative, and digital areas with different objectives – from non-profit performing arts companies to software consultancies or engineering designers and not all those included intuitively fit with cultural and creative goals.

4.4 The variation in the sector, where one sub-sector ‘software & electronic publishing’ accounts for almost half its economic contribution (49% of GVA), means overall performance figures can mask contrasting performance at sub-sector level.

Creative industries sector strengths

4.5 The economic potential of the creative industries sector has grown since globalisation and digitalisation have opened up new markets for cultural and creative services.

4.6 Developed countries, including Scotland, have a comparative advantage in creative industries because their technology and creative sectors are both advanced and they enjoy strong IP protection, which help them develop original services and sell into emerging markets.

4.7 The creative industries are rightly seen as a driver of the economy with the sector making above-average contributions to growth in Scotland’s employment and exports in recent years, although GVA growth has been more volatile.

4.8 In Scotland, the sector has shown particularly strong growth in employment and exports (2013-2019). Over that period, the sector has grown at four times the average rate for Scotland in terms of both jobs and exports.

Identifying sub-sectors with economic promise

4.9 Available data highlights a disparity among the economic performance of its sub-sectors. Some sub-sectors have broadly positive economic results including architecture. Data on some sub-sectors might underrepresent their activity.

4.10 There is no accepted standard way to measure the full economic contribution or opportunity offered by the creative industries and culture in a way more suited to a wellbeing economy.

4.11 Nonetheless, estimates of which sub-sectors have economic potential have been made by combining economic data with additional assessments of market outlook and of how favourable the support environment for a sub-sector is as well as considering whether its output has wider positive cultural and societal impacts.

4.12 The sub-sectors of games, screen, design, and architecture were identified as showing particular economic opportunity.

Wider opportunity to address societal problems

4.13 The other kind of economic opportunity identified was where a sub-sector has untapped skills and potential to help address business and wider societal problems through creativity and innovation. This potential exists in several creative industries, for instance architecture and design could be applied to create better systems or places with consequential societal benefits. Awareness and take-up of these services currently appears low.

4.14 OCEA analysis identified opportunity for creative sub-sectors, such as architecture, and design to develop solutions to societal problems. Innovate UK and the Design Council (‘Using Design as a Force for Change’ 2020 strategy) and other countries such as Denmark have identified strong market potential for design skills and design thinking to solve societal problems. Success in making this an integral part of public and private sector planning requires far greater awareness and promotion of the benefits design can bring.

4.15 Supporting the development of a stronger community across all design disciplines may support business growth and development as well as identifying ways to raise awareness of the potential to increase the opportunities for creative industries to help resolve societal issues.

Related activity and sectoral support

4.16 Creative Scotland provides a programme of work to support creative industries with an explicit focus on creative digital development and on design and craft practice. V&A Dundee, as the national centre for design in Scotland, is a natural champion for the design community. V&A Dundee will receive £3.8m funding from Scottish Government in 2025/26.

4.17 Aligning support for architecture with existing public sector investment in the creative industries, particularly design, can support improved efficiency and effectiveness. There is good potential to strengthen and unify support for the creative industries by using the opportunity of public sector reform to rethink the role of Architecture & Design Scotland with related public sector investment.

Contact

Email: DirectorPAR@gov.scot