Purpose-built student accommodation (PBSA) and student housing: research

This report is the main output from a research project we commissioned in January 2022. The research was commissioned to inform the work of the Purpose Built Student Accommodation (PBSA) Review Group.

3. Evidence Review

Introduction

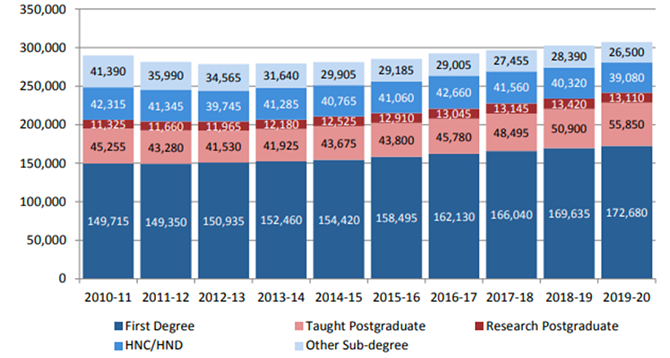

In 2019/20, 307,220 students were enrolled in HE and Further Education (FE) in Scotland. This reflects trends across the rest of the UK (rUK).

Source: Scottish Funding Council (2021)

Reflecting the continual rise in individuals engaging within HE, purpose-built student accommodation (PBSA) has boomed in popularity in the UK in recent years (Cushman and Wakefield, 2021). Recent data from Unipol (including 2022) indicates that this PBSA growth, however, may be slowing. Drawing from a number of sources (Sanderson and Ozogul, 2021; Unipol and NUS, 2021; Unipol, 2022; Revington and August, 2020; McCann et al., 2019), PBSA is defined here as accommodation specifically designed, built or adapted for the purpose of housing students. It may be located on – or off – campus, and owned or managed by a university, private or third sector provider (or some combination thereof). This includes accommodation which is occupied through nominations agreements (allocation of rooms taken by the university within a private/charitable provider block), where universities agree contracts with facilities management or other forms of private engagements, or through direct let by a private or charitable provider.

The boom in recent years in PBSA has most notably been seen in privately-owned (rather than university-owned) accommodation, with universities increasingly decoupling themselves from accommodation provision. According to NUS and Unipol's Accomodation Costs survey, university own beds provision has declined from 39% of PBSA stock in 2017/18 to 24% in 2021/22, while, notably, private direct let provision has increased from 43% of PBSA stock to 58%. The remainder (private beds used by universities) has stayed relatively stable at just under 20% (Unipol and NUS, 2021).

Source: Unipol and NUS (2021)

The Unipol and NUS surveys, however, have a participation rate of around 60-70%. Total PBSA provision is therefore higher than the numbers above. Cushman and Wakefield (2021) estimate bed numbers now to be around 700,000, having climbed from 500,000 in 2013.

According to Reynolds (2020, p.2), PBSA in the UK and Ireland typically takes the form of either: 'Halls of residence consisting of ensuite double bedrooms with shared living and social facilities' or 'Self-contained studios or flats with private kitchens, but shared living and communal spaces'. As Smith and Hubbard (2014) note, pinning down the precise number of total PBSA bed spaces in a particular location is not straightforward because complex relationships and financial arrangements between different stakeholders can obscure how PBSA is managed and controlled.

In 2022, Unipol published a briefing paper on the Scottish-only data from their 2021 survey. It suggested that their survey captured about 2/3 of the Scottish PBSA sector (i.e. 40,674 rooms relative to Cushman and Wakefield's (2021) estimate of 60,310 in total). They also note that University accommodation has shrunk by nearly a fifth since 2012-13, while private sector rooms have grown by fully 360%. While Scotland is less dependent on the private sector PBSA than England, it still accounts for 30% of provision within their survey. Comparative evidence suggests that Scotland is more traditional in its room mix than England with less self-catering en-suite (47% compared to 60% in England), 13% studios in both countries but more 'standard' accommodation in Scotland (22.6% compared to 13%).

This evidence review documents the current PBSA landscape captured by more than 80 studies across the academic and grey literatures (e.g. reports generated by government, charities and commercial groups). The items were generated by online searches using key words, as well as prior knowledge and snowballing from references. The review starts with a discussion of the drivers of the rise in PBSA including, among other things, the phenomenon of 'studentification' – the concentration of students in particular neighbourhoods (Smith, 2005). It then considers specific groups of students who face disadvantages with regard to housing including issues pertaining to international students, those facing financial hardship, homelessness, estrangement, and students with disabilities. It ends by detailing the current Scottish policy context of PBSA and the challenges it currently presents to students and other stakeholders.

The PBSA Boom

Since the mid-2000s, there has been a rapid growth in the building of private PBSA across towns and cities in the UK as well as globally (see Garmendia et al., 2012; He, 2015; Foote, 2017; Prada, 2019; Revington, 2021). PWC (2021) estimate that around one-third of students in the UK are now accommodated in the sector. In the UK, there has been a greater tendency for students to live away from home compared with other European countries and the US and Australia. Only around 1 in 5 UK students stay at home, with those from disadvantaged backgrounds being more likely to do so (Whyte, 2019).

The growth of private PBSA was encouraged by planning policies which sought to move students away from clustering in established neighbourhoods (known as studentification) whilst regenerating brownfield sites and maintaining relative proximity to university campuses (Smith, 2009). Despite the 2009 global financial crisis leading to a downturn in PBSA development (Smith & Hubbard, 2014), it is evidently on the rise once again. This recent positive trend has occurred despite the unprecedented disruptions caused by the Covid-19 pandemic (Cushman and Wakefield, 2021; Savills, 2021). Indeed, not only has PBSA 'bounced back' more so than many other sectors of the housing market since the height of the pandemic, there are reasons to think that demand will continue to increase given the rise in student numbers, evident investor appetite for PBSA in their portfolios, and constrained supply in the HMO PRS sector (Savills, 2021; 2022).

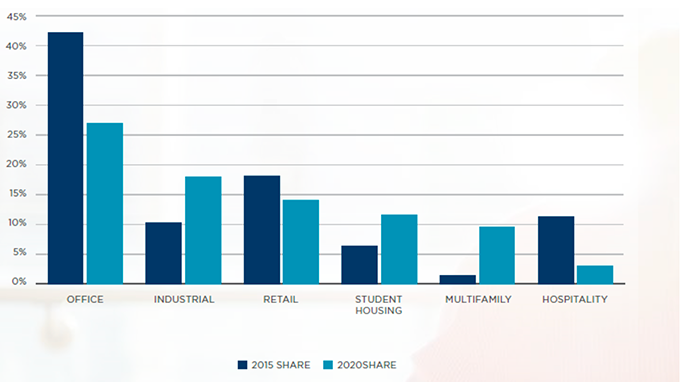

The ambiguous term 'student experience' – taken to encapsulate consumerist ideals of independence, freedom, a thriving social life and something 'more' than simply attending university and completing a qualification – has become a significant facet of university marketing in response to student demand which, combined with challenges emerging in the traditional PRS in Scotland (see below), has enhanced effective demand for this form of accommodation (Jones and Blakey, 2020; Potschulat et al., 2021; Kenna and Murphy, 2021; Farnood and Jones, 2021). The sector in the UK is now estimated to be worth £60 billion (see Figure 2.3) and is a significant and growing alternative asset class for investors (Cushman and Wakefield 2021).

Even with the impact of the pandemic on student mobility, the private sector engaged with PBSA appears optimistic that longer-term demand for PBSA will continue despite any short-term dips. For instance, in referring to the 2021/22 academic year, the Select Property Group (2020) claims that: 'Although it's likely that more lectures will be carried out virtually, students still want to maintain that freedom and sense of independence they get from living away from home and would prefer to be living with friends as opposed to their parents and siblings!' Relatedly, Unite Students (2020), one of the UK's largest PBSA providers, altered its marketing to emphasise that its accommodation was 'Covid ready'. In other words, the growth in PBSA appears to be on an upward trajectory with the pandemic being viewed as creating only short-term disruption.

Source: Cushman and Wakefield (2021)

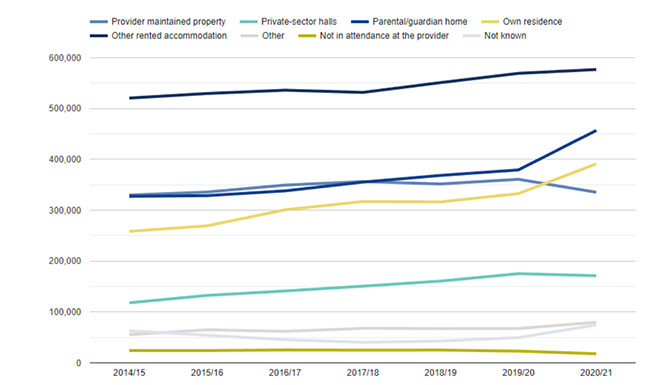

Source: HESA (2021)

Only around one-quarter of UK full-time and sandwich students live in PBSA during term-time; the more traditional private rental sector (PRS) (including HMOs) remains a popular accommodation option for many (27%), while others will stay in the family home (22%) or in their own home (19%) during their studies (HESA, 2021 – see Figure 2.4).

However, the UK PRS (and by extension university accommodation and PBSA) has emerged as the main housing option for students as there is a view that short-term tenancy contracts are preferable for this group (Rugg et al., 2002). This is tied to the image of students as being uniformly young, financially stable, geographically mobile and with no dependents, who desire a form of tenure that favours flexibility to fit around university semester dates (Christie et al., 2002). With the Private Housing (Tenancies) (Scotland) Act 2016, PRS tenancies have become more flexible for tenants compared to previous provisions; this potentially makes the sector even more attractive for students who wish to have a tenancy arrangement that does not necessarily fit with the typical academic year (for example, those who want to extend their tenancy over the summer period). This demand is reflected in recent NUS Scotland (Scottish Housing News, 2021) warnings about a shortage of PRS housing for students, particularly in Glasgow, Edinburgh and Stirling.

Existing PBSA literature provides caution about economic inequalities among students which can be seen through different accommodation types. For instance, Reynolds (2020) argues that new forms of PBSA have led to the emergence of 'a new set of exclusive geographies' (p.9) whereby a student's wealth determines the quality of their accommodation. She explains that the most affluent students reside in so-called 'luxury' PBSA, whilst the 'student precariat' congregate at the lowest end of the market which typically involves poor-quality PRS accommodation or, in the worst cases, homelessness including sofa-surfing, hostels, B&Bs and tents (see also a news article by Lightfoot (2016)). Other evidence points to the year of study being significant for housing decisions, with first year students being more likely to live in university halls of residence or PBSA before moving into the PRS as their degree progresses (Farnood and Jones, 2021). Whilst several studies have highlighted the financial struggles of students from low-income backgrounds (see 'Disadvantaged Students' section below as well as Bachan, 2014; Lewis and West, 2017; Hordosy and Clark, 2019; Lee et al., 2020), studies about PBSA have generally focused on why it has developed, its investment potential and how it has changed the urban landscape. Inequalities, as they relate to the experiences of PBSA and student accommodation more widely, have yet to be fully explored.

PBSA varies in relation to its offer. Facilities that typically come as standard include communal kitchens and lounges, ensuite bedrooms, welcome packs and help integrating new students, hospitality managers, swipe card access, on-site security staff, CCTV, laundry facilities, cleaning services, vending machines and bike racks. Rents almost always include utilities, insurance for personal possessions and broadband, which students have been found to highly value due to the simplicity of an 'all-inclusive' package (Hubbard, 2009; Sage, et al., 2013; Alamel, 2021; Unipol and NUS, 2021). This is likely to be all the more important in the future given the cost of living inflationary crisis and will distinguish it strongly from the traditional PRS, where utilities will normally be paid in addition to rent. The all-inclusive cost paid by PBSA students is clearly qualitatively different from PRS rents for this reason, and so care should be exercised when making rent comparisons.

PBSA can offer additional upmarket amenities such as gyms, swimming pools, private parking, coffee and wine bars, and cutting-edge technology (Smith and Hubbard, 2014; Scottish Government, 2022a). At the top-end of the so-called 'luxury' or 'superior' PBSA market, students can also enjoy bowling alleys, on-site shops, cinemas, saunas, games rooms, craft rooms, music and photography rooms (Kenna and Murphy, 2021; Reynolds, 2022). These latter forms of PBSA entail 'all-inclusive residential communities [original emphasis]' (Kenna and Murphy, 2021, p.139) which are often gated. As well as drawing parallels with the gated communities that are seen in other sections of the housing market, Reynolds (2022) likens such accommodation to the 'hotelization of housing' whereby the marketing of PBSA as luxurious, multi-functional and convenient reflects a hotel- or resort-like business model. The effect of such 'communities' is that they shift social activities away from university campuses towards the internal spaces of residences, ensuring that PBSA becomes more than simply somewhere to live (Kenna and Murphy, 2021).

Whilst not all PBSA is high-end, there is evidence that the quality of the accommodation for students has improved across the sector and is superior to much of the PRS HMO accommodation (Whyte, 2019). However, PBSA rents have also risen, increasing by over 60% since 2011/12 (Unipol and NUS, 2021). On average, students will pay more for living in PBSA. Knight Frank (2021) estimates that average annual costs for those staying in private PBSA is £7,200 pa compared with £6,650 pa for those living in university-operated accommodation and £5,900 pa for those living in the PRS. However, private and university PBSA provision will tend to include the cost of utilities, unlike in the PRS. Unipol and NUS (2021) estimates that the average PBSA rent now accounts for over 70% of the maximum student loan, leaving such students with less than £70 per week to live on unless they have other sources of income. This is striking but does not tell us where this fits into the distribution of costs and resources across the actual student body. Despite the generally higher costs in PBSA (albeit not comparing like with like), most students (84%) in Knight Frank's (2021) representative survey of 31,000 new and current students in 2020, said that their accommodation was affordable. However, the 2022 Unipol Scottish evidence from their 2021 UK survey identifies rising rents and worsening affordability. The average weighted annual rent was £6,853 (£7536 in England). While rents were 9% lower in Scotland (and cheaper for every room type), they had still risen well ahead of inflation since 2012-13 (rents rose by an annual average of 4.1% over that period).

Most of the grey literature is focused on industry sector bulletins for investors, providers and other stakeholder interests from the likes of Savills, Cushman and Wakefield, HEPI, Social Housing (a specialist trade journal for financing the social housing sector, including PBSA activity), local housing strategies, Parliamentary briefings and research reports on the PRS more broadly, some of which might touch on the student sector, normally if at all, only in passing. Where private PBSA is the focus, this is normally in relation to demand/supply information for investors (CBRE, 2018; PWC, 2021), advice on how to stay competitive and remain adaptable to market changes (Property Week, 2021) or to flag the advantages and potential threats for investing in PBSA (Knight Frank, 2021; Patel, 2021). It is also worth noting that, in 2020, a dedicated digital publication called PBSA News was established; this platform publishes news articles, research and information for PBSA providers.

Drivers for the Growth of PBSA

Interactions between universities and towns or cities – sometimes referred to as 'town and gown' relationships (Revington, 2021) – are complex, with student housing often central to tensions that can arise. Prior to the mid-2000s, concerns about student accommodation were spotlighted on PRS HMOs (Sage, et al., 2012). These HMOs became clustered in areas close to universities and, in many cases, they sat adjacent to inner-city gentrified neighbourhoods, leading to the concept of studentification (Smith, 2005). Sage et al. (2012; 2013) argue that whilst many instances of studentification involved middle-class students moving into middle-class gentrified areas, there were examples (parts of Brighton for example) of more marginal communities becoming overwhelmed by influxes of students.

Evidence on studentification has highlighted the tensions this created between existing residents and students, with most of this research focusing on the former group. Existing residents across multiple case study areas, including Glasgow, reported problems perpetrated by students in relation to noise nuisance, unkempt gardens, litter, poorly managed refuse disposal, parking disputes, anti-social behaviour, crime and disruptions created by cycles of moving in and out corresponding with the academic year (Hubbard, 2009; Munro and Livingstone, 2012; Sage, et al., 2012; 2013; Mulhearn and Franco, 2018). In some cases, this led to the out-migration of existing residents, which resulted in certain areas becoming 'ghost towns' during the summer months (Kinton, et al., 2016). It also led to the closure of services such as schools, churches and traditional pubs coupled with the introduction of fast-food restaurants and off-licences that appealed to the student market (Sage, et al.., 2012; 2013). Although most studies focused on negative perceptions and experiences towards students by existing residents, some evidence indicates that the tensions were felt both ways, with students being aware of the hostility that was directed towards them and likewise holding negative views about living close to existing residents, preferring instead to live in 'studenty areas'; this resulted in even greater segregation between the two groups (Chatterton, 2000; Hubbard, 2009).

Evidence suggests that PBSA was viewed by many as the solution to these problems. Local authorities, universities and lobby groups were attracted by the prospect of developing purpose-built housing for students, located in less contentious neighbourhoods. As one study explained: 'PBSA has become the backbone of many local authority policies seeking to disperse students to reinstate social mixing in studentified enclaves' (Sage et al., 2013, p.2624). Compared to PRS HMOs which typically involved older converted housing that was not always in good condition, PBSA was likely to be more attractive for students seeking better standards of living whilst likewise benefitting existing residents through a process of 'de-studentification' in which students decanted from PRS HMOs in residential areas to PBSA which is often located further away from established neighbourhoods (Kinton, et al., 2016; Mulhearn and Franco, 2018). These narratives move on, however, and we will see later on that new PBSA developments are argued by some to be part of the current studentification problem, because of both new neighbourhood succession issues but also competition for urban land that is seen to displace affordable housing.

Contemporary students appear to have higher expectations for their quality of accommodation, which has been largely driven by the emergence of PBSA (Kenna and Murphy, 2021), although (deteriorating) student 'digs' remain part of the housing landscape, particularly for those from lower-income backgrounds (Reynolds, 2020). Nevertheless, there are concerns expressed that an approach of pushing students into more private PBSA accommodation in gated communities removes them from the wider community and therefore they only play a limited role in sustaining public services, volunteering and regenerating local economies. This may also have consequences for retaining students in these communities once they have graduated and have skills to be productive community members (Whyte, 2019). This appears to be recognised in some local planning authorities, such as Edinburgh, for example, large PBSA developments now have to accommodate affordable housing planning agreements intended to help to meet local housing need as well as build a sense of community.

Solving the perceived problems of studentification is only one driver for the growth of PBSA. Another factor has been the ageing stock of existing university accommodation which creates significant liabilities for universities. Being able to outsource financial and management responsibility for accommodating students into the private sector, even where some level of accountability is retained, has been highly attractive for universities. This is particularly the case when finances for non-education activities have been depleting, student demands change (Hubbard, 2009; McCann et al., 2019) and provision of good quality accommodation is a key part of university strategies to attract large student numbers.

At the same time, financial investors have a clear interest in PBSA, particularly post

the global financial crisis, mirrored by real estate research encouraging institutional investors in the UK, Europe and North America to take the rewards of PBSA seriously (French et al., 2018; Livingstone, 2022). For example, Livingstone (2022) argues that 'A decade ago, PBSA and the PRS were seen as riskier propositions for investors, but these are now more firmly established and mainstream assets, offering attractive rewards, as […] reflections on yields and returns illustrate' (p.3). In another paper, it is simply stated that '[PBSA] is an asset class whose star is rising' (Livingstone and Sanderson, 2021, p.2). They qualify this by illustrating that overall demand for PBSA far exceeds supply although though this varies across different regions.

One attraction here is the belief that successive cohorts of students are willing to accept (or are at least cope with) rent increases and are a group who are unlikely to accrue rent arrears (Hubbard, 2009). Mulhearn and Franco (2018) explain that, in the UK, PBSA has grown in line with the growing maturity of well-established providers such as the Unite Group and Liberty Living, as well as an increasing number of international investors (particularly from the US, Singapore and the Middle East), who have capitalised on the perceived resilience of student accommodation demand even in times of financial crisis.

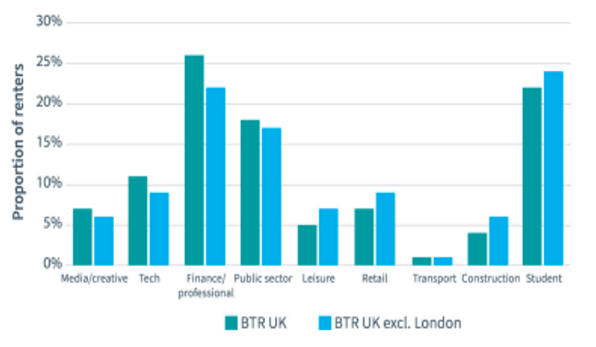

More recently, there have been warnings about the over-supply of PBSA with certain regions potentially having reached saturation (Mulhearn and Franco, 2018). Relatedly, the PBSA sector has warned investors that demand might also begin to fall due to the fragility of the international student market (Patel, 2022). Consequently, some owners of PBSA have started marketing these properties to non-students, particularly for tourism and conference purposes (see Reynolds, 2022 for examples in Ireland). This has led Revington (2021) to propose that some regions may be entering a period of 'post-studentification' in which non-students are living alongside students in PBSA. In Scotland, although with Build-To-Rent (BTR) properties beginning to emerge as an extension to the traditional PRS that can accommodate both students and non-students it is possible that we may see pressures for a similar 'post-studentification' process occurring in the future. As a recent study of people living in the BTR sector has shown (BPF, 2021), the sector accommodates a range of occupations, including students (see figure 2.5).

Source: BPF (2021)

Disadvantaged Students

When considering housing experiences according to different groups or types of students, it is possible to identify from the literature those who may be more disadvantaged in the process. Specifically, estranged students and disabled students have been identified, although more work is needed in these areas. Unipol (2022, p.2) continue to argue that there is 'not enough accommodation to meet the needs of disabled students'. This section will focus on these groups, but it is likely that there are others who are even less represented in the current evidence base but who find themselves disadvantaged in relation to housing. Such groups may include students with dependents and caring responsibilities, those with mental health issues, LGBTQ+ students and those from ethnic minority groups. More research is needed to explore the nuanced experiences of these groups in relation to student housing, something we start to address in the following chapters.

Of the groups mentioned in the literature, international students (often postgraduate) have received the most attention although most of this evidence comes from outside the UK (Obeng-Odoom, 2012; Arkoudis, et al., 2019; Fang and van Liempt, 2021; and Calder, et al., 2016). This literature indicates that finding housing is a particularly complicated for international students as they do not always understand how to find accommodation, local costs, what their options are, the characteristics of different neighbourhoods and local cultural practices (Fincher and Shaw, 2009; Arkoudis, et al., 2019). Whilst domestic students often face similar challenges, international students experience these issues on a larger scale due to structural disadvantages and discrimination (Fang and van Liempt, 2021).

New international students can often experience a lack of social integration and belonging (Arkoudis, et al., 2019) as well as a lack of social support and greater discrepancy between their expectations and experiences (Khawaja and Dempsey, 2008). Tied to these feelings are significant struggles with securing housing which can escalate and produce enormous stress (Fang and van Liempt, 2021). International students are generally reliant on finding their own housing as opposed to having the option to live with a friend or family member (Arkoudis, et al., 2019). They typically want to have their housing set up prior to arriving in the country or they are compelled by letting agents to sign up for a year-long private PBSA contract as agents will advise that they will struggle to find accommodation otherwise (Fincher and Shaw, 2009). Consequently, in some university towns, international students can become segregated from domestic students by being funnelled into specific PBSA blocks, with domestic students expressing preferences not to be housed in a predominantly international apartment block (Fincher and Shaw, 2009), although international students often prefer to be housed in this way (Paltridge, et al., 2010; Obeng-Odoom, 2012).

From an international student perspective, it is claimed that universities do not provide enough support in helping them to navigate these complex processes or, where support is provided, it tends to be generic and not specifically tailored to international students who lack the knowledge that domestic students will already have (Obeng-Odoom, 2012). Arkoudis et al. (2019) found that students often feel cheated when they arrive at their accommodation as the images on websites often do not reflect the reality, and many find themselves having long commutes between their accommodation and university building. The same authors found that international students also want information about student housing neighbourhoods, including safety (Arkoudis, et al., 2019). Indeed, Paltridge, et al. (2010) highlighted the significance of safety and security for international students, due to their heightened vulnerability to crime, with university-provided accommodation being reported by students to meet these needs more so than other forms of accommodation.

An NUS survey (NUS, 2021) found that the majority of students (presumably mainly UK-based) worked during term time: a full 24% worked full time, and 41% part time (including 10% on zero hour or casual contracts). These figures had increased since the year before, when Covid-19 rules were more restrictive. The impact of Covid on incomes was adverse for over 70% of students surveyed, including 30% who said that their income had suffered a 'major impact'. 85% had cut back on their spending. Over 70% expressed concern at their ability to manage financially during the pandemic and more, 76%, were concerned about managing financially in the post-pandemic period.

Unipol and NUS (2022, p.1) focus on their survey evidence on affordability problems in the sector. They note for the UK, rent increases outstrip inflation by a big margin, that there are many locations where there is insufficient affordable student accommodation, that private PBSA providers are continuing to provide more ensuite accommodation with higher rents and that universities are often constrained to work with a rent escalator linked to long term loan finance deals. Private operators typically use their competitors as a rent-setting benchmark driving a further wedge between PBSA rents and inflation (and student budgets). Unipol expresses concern that rent increases are on an upward trajectory. This will make housing costs even more unaffordable for the expected growing share of less advantaged students predicted to be coming into the sector over the next 15 years. The NUS survey (NUS, 2021) does not offer a breakdown by current living circumstances, but found that of those paying rent, around two thirds were concerned that Covid-19 had affected their ability to afford rent payments, and 22% had been unable to pay their rent in full over the last 4 months. Overall, in the NUS survey, 37% said that their rent was not affordable (with 46 % of students saying it was or having no opinion). Turning to Scotland, Unipol argues that the Covid pandemic shut down many of the part time hospitality jobs students depended upon, making them more reliant on their parents (or running up further debt) to continue studying.

While there are very striking images of unaffordability among students, we should be cautious – there is little evidence on either more disaggregated (or quality-adjusted) rent costs or on the size and distribution of actual student incomes (including a measure of parental support). We also know that there is considerable variety in costs and quality in student accommodation across the country. As in many other areas of this work, we need more and better data to monitor and understand what is going on.

Financial hardship is also experienced by domestic students, with socioeconomic backgrounds playing a significant role in how students fare. In the UK, much of the literature on student finances focuses on England and Wales, due to the tuition fee system which now sees students leaving university with significant debts that need to be paid back once reaching a certain salary threshold in paid employment. Although Scottish students studying in Scotland do not pay tuition fees, many still accrue debt throughout the course of university (Carney, et al., 2005) and non-Scottish students studying in Scotland do still need to pay tuition fees. Bachan (2014) explains that the expansion of the UK HE sector and widening participation strategies led to a funding crisis which saw grants and bursaries becoming increasingly replaced with loans from the mid-1990s onward. Coupled with rising tuition fees, there is evidence that financial hardship among lower-income people is a barrier to accessing HE in the first place (Kaye, 2021). For those who do make it to university, students are less likely to anticipate high levels of debt if they have financial support from their parents, if both parents are university educated and their parents are homeowners (Bachan, 2014). Thus, students from lower socioeconomic backgrounds expect to struggle financially during and after university, with many working part-time jobs to try and mitigate some of these challenges which, in turn, can negatively impact on their studies (Purcell and Elias, 2010).

An additional affordability issue is the experience of fuel poverty for those students living in PRS HMOs in the UK. Given that the PRS can be a cheaper option than PBSA, those on lower incomes are more likely to live there. This, coupled with many PRS HMO properties being older, in poor condition and thus energy inefficient, results in high fuel costs which students struggle to afford over and above their other living costs (Bouzarovski and Cauvain, 2016). Evidence suggests that students take measures to keep fuel costs as low as possible. For instance, Morris and Genovese (2018) reported that students would wear extra layers of clothes, use hot water bottles and cut back on food costs to be able to keep up with energy bills. These issues were reported by students living in both the PRS and in university-provided accommodation. Likewise, Petrova (2018) found that students living in the PRS would limit the use of the oven, take short lukewarm showers, keep the lights switched off so they could prioritise charging their laptops and spend lengthy periods of time in university libraries or friends' houses to stay warm. These points are highly germane as current and anticipated energy price inflation drives the ongoing cost of living crisis, even if such costs are included in PBSA bills (i.e. they will need to be dealt with in subsequent charging the following year).

Finally, in relation to financial hardship, it is likely that some students will experience homelessness during their studies although this area is considerably under-researched (see O'Neill & Bowers, 2020, for such research in the USA). NUS (2021) found that 12% of students said they had experienced homeless at some time, including 2% currently homeless. The experience was even more common amongst widening access groups with 33% of students estranged from their families and 29% of care experienced students (the worst affected groups) having experienced homelessness.

One sub-group of students who can be at heightened risk for homelessness are those who are estranged from their families. A Scotland-based study, which conducted qualitative interviews with 21 estranged students, found that several had experienced homelessness whilst others constantly worried about the possibility of homelessness due to financial hardship (Costa, et al., 2020a). This was particularly so when the academic year ended, at which point first-year students had to leave their halls of residence with the expectation that they would return home to their families for the summer. Having no such family support, estranged students found themselves in housing precarity. Recent research commissioned by the Scottish Government similarly found that estranged students had been homeless, or felt at risk of homelessness. The research found that estranged students had limited choice of accommodation, due to restricted budgets, and struggled to access rent guarantorship (Scottish Government, 2022b).

Despite universities offering accommodation support for estranged students over the summer, some were put off by the idea of needing to prove their estrangement status (something we return to later in our qualitative research). Indeed, although estranged students can be entitled to government financial assistance, they may be reluctant to go through the process of proving their estrangement due to feelings of shame, humiliation, and concerns about stigma (Bland and Blake, 2019; Costa et al., 2020b; Scottish Government, 2022b). Costa et al., (2020a) concluded that to fully support estranged students, universities need to better support them to find accommodation which is affordable and which students can remain in for the duration of their degrees.

The final group of students we consider are those with physical disabilities who are not only faced with the challenges that have been discussed so far (i.e. a lack of available and affordable housing), but often have the added challenge of finding housing that is accessible. Writing in 2013, Ahmed (2013) , a disabled wheelchair-dependent student at Queen Mary University of London, described that she was unable to find a single wheelchair accessible flat or house near to the university campus and claimed that the nearest suitable accommodation was 60-miles away in Northampton. UK evidence generally points to a significant lack of accessible accommodation available to students across university halls and the PRS. Soorenian (2013) reported the experience of one student who had to initially live in an inaccessible flat in university halls because the only available accessible flat was not ready for her arrival meaning that, for the first two weeks at university, she was unable to cook as the kitchen was located up a flight of stairs. A lack of lifts, steep stairs, narrow corridors, heavy doors, inappropriately positioned furniture, a lack of visual smoke alarms (for hearing impaired students), being located next to a busy road with no pedestrian crossing and not being close to accessible public transport - were all issues raised by students in Soorenian's (2013) study. She also noted that sometimes disabled postgraduate international students are placed in accommodation alongside first year undergraduate domestic students because this is where the only accessible housing is – meaning that these international students are separated from their peers which adds to their lack of integration. Whilst newly-built PBSA can potentially offer more accessible housing compared to older university and PRS buildings, the Scottish Government (2022a) expressed concern that accessible rooms are often more abundant in the more expensive PBSA buildings, compounding financial problems that many disabled students already face.

The Scottish Context

The evidence reviewed thus far has only touched upon the Scottish context, with most UK-based research based in England. This is important as housing and education are devolved matters and Scottish students studying at Scottish universities do not pay tuition fees, which may have implications for their chosen accommodation. There are clear cultural and social distinctions between Scotland and the rest of the UK, as well as across different Scottish regions. To date, the nuances of PBSA and other forms of student accommodation in Scotland can only be found in the grey literature produced by relevant government, third sector and commercial stakeholders. At the same time, discussions about Scotland make up only a small proportion of UK-focused reports.

However, evidence from Unipol and NUS (2021) does demonstrate that the main trends observable in the rest of the UK are also evident in Scotland: private PBSA has also grown rapidly in Scotland over the last ten years; it now accounts for the majority of bespoke student accommodation; and rents are rising considerably faster than inflation. Average weekly rents in the PBSA sector for students attending university in its main cities (Aberdeen, Edinburgh and Glasgow) are around £125-£167, which is in line with other cities in the UK and considerably below London (£238 per week) (Cushman and Wakefield, 2021).

The policy context for the current research derives specifically from linked government commitments in the 2021 Programme for Government, Housing to 2040 and the current New Deal for Tenants consultation. The Scottish Government is seeking to improve affordability and housing conditions in the rental market, including the large student sector, and also to provide the evidence and steer for a strategy for student accommodation, including PBSA as a critical part of that sector. However, it is worth noting that PBSA is not unregulated; there are UK national codes of practice from ANUK/Unipol (2022) that apply to all parts of the UK. While the codes are voluntary, they are an important signal to the market and they set compliance criteria on building management and student satisfaction in the sector. Moreover, and rather oddly, PBSA is also regulated by the HMO system which has a particular bearing on building quality and safety.

There are important evidence needs, policy and process dimensions that inform the rationale for this evidence review and wider study for the Scottish Government. The data is far from comprehensive, especially for Scotland. Two recent analyses based on survey evidence draw self-reported findings from provider and educational institutions involved in student accommodation (Unipol and NUS, 2021; Scottish Government, 2022a). The Unipol and NUS (2021) survey presents some Scottish-level data and is based on returns from a subset of Scottish Higher Education Institutions (HEIs): the Universities of Glasgow, Strathclyde, Heriot-Watt, Aberdeen, Edinburgh and Edinburgh Napier, as well as a number of private and charitable providers (although the report does not state where they operate or which part of the HE/FE sector they operate within). The survey suggests that Scottish rents are rising in real terms and, as we saw earlier, that they can readily exceed the annual provision of maintenance support, which is a stark indictor of the lack of affordability for students. There are longer term concerns about universities' relative lack of control over the cost/quality offer to students and, as affordable supply appears to shrink, worries grow that this will coincide with demographic, widening access and other reasons for increasing student numbers.

The Scottish Government (2022a) scoping study was based on 46 survey responses with key stakeholders from universities, colleges, student associations, local authorities, PBSA providers and representatives. It found that rents ranged from £100-225 per week (which aligns with the figures presented above from the Unipol and NUS (2021) survey), with some providers charging extra for additional services such as broadband, parking and gym access. Student representatives reported that rents were unaffordable and that students often had to rely on financial support from family or part-time jobs to keep up with rent payments. Most providers did not offer non-term time or holiday rent reductions. PBSA providers appeared to recognise the mental health needs of students and there were efforts to provide support, although the report raised concerns about consistency, challenges of joined up working between private providers and universities and the impact of poor living conditions on mental health (similar findings were uncovered in Wales by Shelter Cymru and NUS Cymru (2021). Mental health problems were exacerbated during the Covid-19 pandemic, particularly when students were living in sub-optimal accommodation. As mentioned in the previous section, concerns were also raised about the lack of adapted rooms suitable for accommodating students with disabilities; with accessible rooms being more frequently found in more expensive accommodation which compounded affordability problems. Some PBSA providers also mentioned extra measures in place to support estranged or care-experienced students but this support is not consistently provided or good practice detailed.

The exemption of student accommodation from the Scottish Private Residential Tenancy regime means that students have fewer protections and rights in relation to their living conditions, rent increases and notice periods. This was particularly problematic during the pandemic when many students were forced to keep paying rents for accommodation they were not using, although coronavirus legislation enabled students to overcome these issues by allowing students to leave or cancel their contracts in university halls and PBSA with 28-days' notice for those who signed a contract after 27th May 2020 or with 7-days' notice for those who had signed a contract before that date. The 28-day notice to leave period was extended initially until September 2022 under the Coronavirus (Scotland) Act (Amendment of Expiry Dates) Regulations 2022, although it was actually suspended from July 1 2022.

Although the Scottish Government (2022a) scoping report revealed several issues with the PBSA sector, the limited sample and method mean that such findings need to be treated with caution and explored on a larger scale. What seems to be particularly needed is more detailed experiential data from students from different backgrounds.

Finally, analysis of demand levels in Scotland predicts a levelling off, and possible slowdown, in PBSA demand due to a demographic dip caused by low numbers of 18-year-olds in the population. Given the pipeline of PBSA units, there is a possibility of excess demand over the next 12 years if present trends continue (PWC, 2021).

Key Messages

- The evidence indicates that PBSA has and is continuing to grow at a significant rate, with no indication that current investment is slowing down.

- PBSA is believed to hold several advantages over more traditional forms of student accommodation, such as traditional private renting, and, in theory, is of better quality, is more professionalised, is a solution to tensions created by studentification and aligns with ideas of enhancing the 'student experience'.

- However, not all PBSA is the same and there are indications of varying quality as well as problems with unaffordability, at least for some student groups.

- PRS/HMO accommodation remains the preferred choice for students in some areas. Cushman and Wakefield (2021) estimated that the largest student PRS HMO markets in the UK were in Edinburgh and Glasgow.

- The Scottish Government (2022a) scoping study also highlighted challenges relating to student mental health, adapted accommodation for students with disabilities, inconsistencies in support for estranged or care-experienced students as well as broader issues linked to the fact that student housing is exempt from the Scottish Private Residential Tenancy.

- Much more research is needed to explore the nuanced experiences of different groups of students who are likely to be disadvantaged in relation to housing. What appears to be especially remarkable is that most evidence has not included the voices and experiences of students themselves. Much existing evidence is based on elite stakeholders, secondary data such as census reports, financial projections and analysis of online PBSA advertisements. This study has sought to rectify this by capturing data from both key stakeholders and students to explore how PBSA is working in practice for these groups.

Contact

Email: socialresearch@gov.scot