Public sector leadership on the global climate emergency: guidance

Guidance to Scotland’s public bodies on their leadership role in the shared national endeavour to tackle the global crises of health, climate emergency and biodiversity loss.

7. Greenhouse Gas Reporting

All public bodies must report on their corporate greenhouse gas emissions that result from their organisational activities and services.

Reporting should align with the Greenhouse Gas Protocol and can be completed through the standard Scottish Government reporting template. Detailed guidance on public bodies climate change reporting and supporting resources are available on the SSN website.

Greenhouse gas reporting is based on the following principles:

Relevance – Ensure the GHG inventory appropriately reflects the GHG emissions of the organisation and serves the decision-making needs of users – both internal and external to the company.

Completeness – Account for and report on all GHG emission sources and activities within the chosen inventory boundary. Disclose and justify any specific exclusions.

Consistency – Use consistent methodologies to allow for meaningful comparisons of emissions over time. Transparently document any changes to the data, inventory boundary, methods, or any other relevant factors in the time series. Where methodologies change, as more accurate data becomes available, this should be indicated.

Transparency – Address all relevant issues in a factual and coherent manner, based on a clear audit trail. Disclose any relevant assumptions and make appropriate references to the accounting and calculation methodologies and data sources used.

Accuracy – Ensure that the quantification of GHG emissions is systematically neither over nor under actual emissions, as far as can be judged, and that uncertainties are reduced as far as practicable. Where uncertainties do exist ensure that they are highlighted. Achieve sufficient accuracy to enable users to make decisions with reasonable assurance as to the integrity of the reported information.

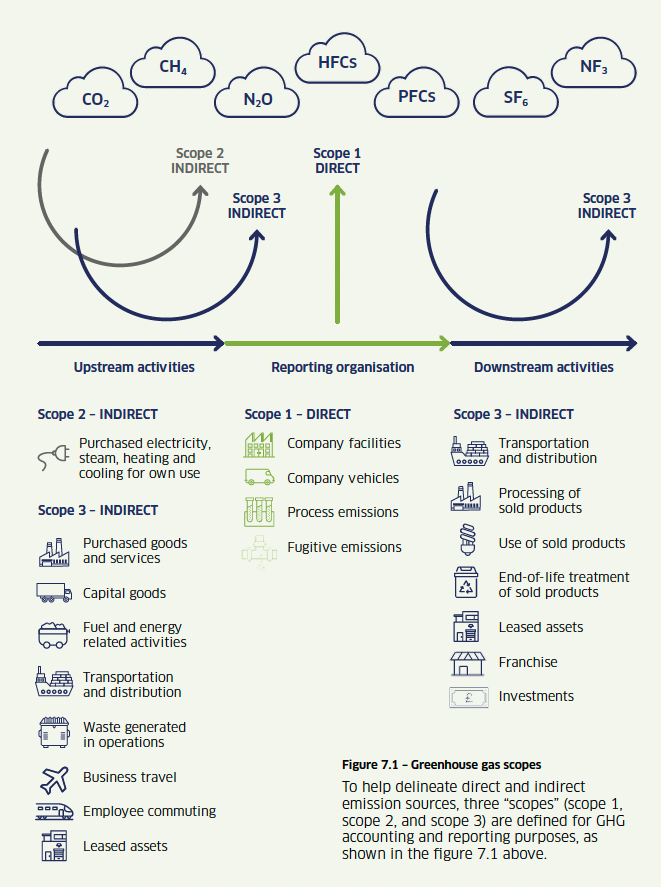

To help delineate direct and indirect emission sources, three “scopes” (scope 1, scope 2, and scope 3) are defined for GHG accounting and reporting purposes, as shown in the figure 7.1 above.

Where relevant, the following emissions sources must be reported:

| Category | Reporting Requirements | Emissions Source | Example |

|---|---|---|---|

| Scope 1 | All scope 1 emissions must be reported. |

|

|

| Scope 2 | All scope 2 emissions must be reported |

|

|

| Scope 3 | All relevant and significant areas of the organisation’s indirect emissions should be reported. Any categories 1% of overall emissions can be treated as de minimis | ||

| Out of Scope | CO2 emissions attributed to the burning of biomass and other biofuel | Biomass or biofuels | Combustion of biomass in a boiler |

| Land Use & Land Use Change | Land use emissions are very important and land will play a key role in the transition to net zero. Public bodies are not currently required to report these but, where appropriate, land-based emissions should be considered and reporting considered. | ||

Scope 3 Reporting

Scope 3 covers all indirect emissions (aside from those accounted for under scope 2) from the value chain of an organisation and looks at both upstream and downstream activities. Full information on scope 3 reporting can be seen in the GHG Protocol Corporate Value Chain Accounting Standard, and further guidance on how to calculate scope 3 emissions is provided in the SSN Net Zero Manual that supplements this guidance.

It is common for an organisation’s scope 3 footprint to be significantly larger than its scope 1 and 2 footprints, therefore it is important to include scope 3 in reporting to better understand the organisation’s overall climate impact. Scope 3 emissions are also likely to have significant uncertainty – however this should not be a barrier to reporting, as the poor data maturity of some areas of scope 3 reporting can be included in reporting for transparency.

As scope 3 emissions are from the value chain, they are not considered under the direct control of the organisation, however many areas of scope 3 can be heavily influenced by the organisation through behaviour, supply chain engagement and decision-making.

There are many categories of scope 3 emissions, and they will not all be relevant for all organisations, therefore public bodies must review their reporting boundary and clearly understand which categories are relevant for them.

Over time public bodies will be expected to report on their scope 3 emissions as fully as possible.

The categories of emissions in scope 3 are summarised in the table below.

| Upstream or Downstream | Scope 3 Category | Example | Example Calculation Methodology | Expected Data Maturity |

|---|---|---|---|---|

| Upstream | Purchased goods and services | Cradle to gate emissions of purchased goods and services | Estimated | Red |

| Capital Goods | Cradle to gate emissions of capital goods | Estimated | Red/Amber | |

| Fuel and energy that’s not scope 1 or 2 | Transmission and distribution losses from electricity Cradle to gate emissions of purchased fuel (well to wheel) | Calculated by energy data | Green | |

| Upstream transportation and distribution | Transportation of products purchased | Estimated or provided by suppliers | Red/Amber/ Green | |

| Waste | Waste collection emissions, emissions from landfill | Provided by suppliers | Green | |

| Business travel | Air travel | Provided by travel suppliers | Green | |

| Employee commuting (and home working) | Employee commuting; home working (telecommuting) | Estimated – based on government data or employee surveys | Red/Amber | |

| Upstream leased assets | Student halls not owned by institution | Estimated or provided by supplier | Amber | |

| Downstream | Downstream transportation and distribution | Transportation of products sold (in vehicles not owned by organisation) | Estimated | Red |

| Processing of sold products | Processing of intermediate products by downstream organisation | Estimated or provided by organisation | Red/Amber | |

| Use of sold products | End use of goods and services | Estimated | Red | |

| End of life of sold products | Waste disposal of products sold at their end of life | Estimated | Red | |

| Downstream leased assets | PFI | Estimated | Red | |

| Franchises | Operation of franchises e.g. international campuses for universities | Estimated or provided by franchise | Amber/Green | |

| Investments | Operation of investments | Estimated | Red |

Data maturity varies for different categories of scope 3 and therefore different methodologies of emissions reporting are to be expected. These are outlined below and have been given a red/amber/green status so that the level of data maturity is transparent for each reporting category.

Data Maturity Rating

Red - Data is estimated and has a large margin of error – e.g. based on industry norms/estimated factors

Amber - Data is estimated and has a moderate margin of error – e.g. based on spend data

Green - Data is measured/supplier specific and has a smaller or known margin of error

It is not appropriate to set reduction targets for reported emissions that are high level estimates e.g. red or in some cases amber. However action to reduce such emissions are still expected.

Over time, emissions data for categories that contribute the larger share of an organisation’s total emissions should mature e.g. by reducing uncertainty, moving from estimation to measurement, where possible.

Assurance and Verification

All greenhouse gas reporting data must meet the GHG protocol principles (Relevance, Completeness, Consistency, Transparency, Accuracy). Going through a formal assurance or verification process to ensure the organisation’s processes and data satisfy these principles can have many benefits including:

- Increased credibility of publicly reported emissions information and progress towards GHG targets, leading to enhanced stakeholder trust.

- Increased senior management confidence in reported information on which to base investment and target setting decisions.

- Improvement of internal accounting and reporting practices (e.g. calculation, recording and internal reporting systems, and the application of GHG accounting and reporting principles), and facilitating learning and knowledge transfer within the organisation.

As a minimum, public bodies must have a formal internal assurance process signed off by a senior leader.

Public bodies may also wish to have some level of external assurance or verification which could be through:

- a formally appointed third party who provide verification services; or

- peer-to-peer review with other public bodies.

Corrective Actions & Recommendations

Verification and assurance may identify areas of non-compliance or improvement. These should be captured through a corrective action plan and any required changes implemented before completing the subsequent annual report.

Contact

Email: gavin.barrie@gov.scot