A New Deal for Tenants - draft strategy: consultation

We are consulting on the draft A New Deal for Tenants - rented sector strategy, which seeks to improve accessibility, affordability choices and standards across the whole rented sector in Scotland.

Chapter Four: Affordable Rents

Introduction

In order to realise the right to an adequate home, and for the overall housing system to work well for the people of Scotland, there must be options for people to live in quality, affordable rented accommodation.

Influences on rent levels are multiple and complex and the picture of both rent levels and rent inflation are not the same across the country, with huge geographical differences in experiences.

Supply of, and demand for, private rented accommodation can be impacted by a wide range of circumstances including the prevalence of holiday lets and second homes, investment in the sector, macro-economic changes such as changes to interest rates, levels of demand, the cost of home ownership and demographic change to name a few.

This means that rent levels set by the market can end up being unaffordable and unfair in some areas, with rent increases substantially above the rate of inflation or maintenance and upgrade costs leading to people struggling to find suitable homes.

However, we also know that ambitions to improve the quality and standards of homes in the rented sector mean that investment is needed and the regulation of rents must be achieved while also ensuring the quality of properties is maintained and raised, in order to meet our ambitions around standards set out in Chapter Six.

A shared understanding of housing affordability

The Scottish Government’s aim is for everyone to have a safe, high-quality home that is affordable and meets their needs in a community they want to be part of.

Scotland has led the way in the delivery of affordable housing across the UK.

The Scottish Government is investing £3.6 billion in affordable housing in this parliamentary term towards the delivery of more social and affordable homes, continuing to ensure the right homes in the right places.

Since 2007, we have delivered more than 105,000 affordable homes and we have committed to deliver a further 110,000 energy efficient homes through the Affordable Housing Supply Programme by 2032, with the aim that at least 70% of those homes will be for social rent and 10% in Scotland’s remote, rural and island communities[34].

Delivering this ambitious affordable homes’ target will support a total investment package of around £18 billion and up to 15,000 jobs each year, while contributing to Scotland becoming a net zero nation through modern, energy efficient housing.

Rent affordability plays a crucial role in tackling poverty and, whilst the majority of households enjoy good housing conditions, we know that the housing market as a whole does not work as well for some – with poorer and younger households in particular more likely to be in the rented sector[35].

Research suggests that high housing costs are one of the biggest drivers of poverty in the UK, especially affecting poorer and younger households. Many private renters are being priced out of home ownership because saving for a deposit is unrealistic for them, given that a high proportion of their salaries is being spent on rent. Low-income households might also lower their housing standards in order to meet their non-housing needs, which can affect health and other social outcomes.

Child poverty, in particular, featured as one of the key themes in stakeholder engagement and public consultation for Housing to 2040. There was consensus among stakeholders that housing and child poverty are inextricably linked and that there is a relationship between expensive, poor quality housing and mental health; educational attainment; excess winter deaths; and child and fuel poverty.

Affordability of homes, rising rents, the roll out of Universal Credit resulting in the increase of rent arrears, and access to secure and reliable employment were also highlighted as factors impacting on child poverty levels.

Housing affordability also interacts with fuel poverty and access to affordable housing has a role to play in ending homelessness and ensuring the right to an adequate home.

During the development of Housing to 2040, many respondents called for affordability to be more clearly defined in relation to housing. At present, there is no consensus on what housing affordability means and no universally accepted definition. Measures of affordability exist but there is a tendency to rely on simple measures in spite of their shortcomings. That said, housing affordability problems are not new and the debate on how to define affordability has been going on for decades, without consensus. There have been improvements in the last century (e.g. less overcrowding, better sanitary accommodation) but the proposed solutions to affordability problems have remained similar.

Action: We are continuing to work with stakeholders to develop a shared understanding of affordability that is fit for the future and takes into account the drivers of poverty and inequality, the housing market, the distribution of homes, the supply of affordable homes, the financial sustainability of the affordable rented sector and the real costs of living in a home and a place.

This work on affordability will consider how the housing market works for different households with different levels of income and at different stages in their housing careers.

While having a shared understanding of housing affordability will not directly benefit people with protected characteristics, it will help us to measure how effectively Scotland’s housing system is serving people with protected characteristics and enable us to take action to address any disadvantages that exist.

Consultation Question: What are the most important factors to be incorporated into a shared understanding of housing affordability (e.g. household size and composition, regional variations, housing standards, treatment of benefits)?

Consultation Question: If we are successful in reaching a shared understanding of affordability in Scotland, how should it be used and evaluated?

Affordability in the Scottish rental sector

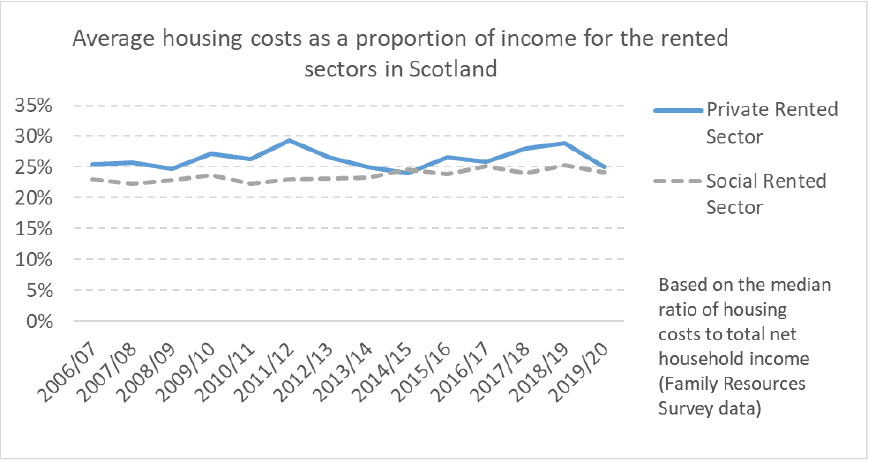

At a national level since 2006/07, people living in the private rented sector have spent the highest proportion of their income on housing (26%) of all the tenures, this is compared to 24% for social rented[36] and for owner occupiers with a mortgage the average proportion of income has fallen from 12% in 2006/07 to 7% in 2019/20.

Of course a direct comparison of the costs of renting and buying is difficult to make because the capital element of a repayment mortgage creates an asset for the owner, which rent does not, and conversely renters will need to provide a smaller deposit than home owners or landlords. In addition, an owner or landlord will be liable for costs such as buildings insurance, repairs and maintenance and Land and Buildings Transaction Tax whereas tenant will not pay for these separately and such costs are factored into the rent.

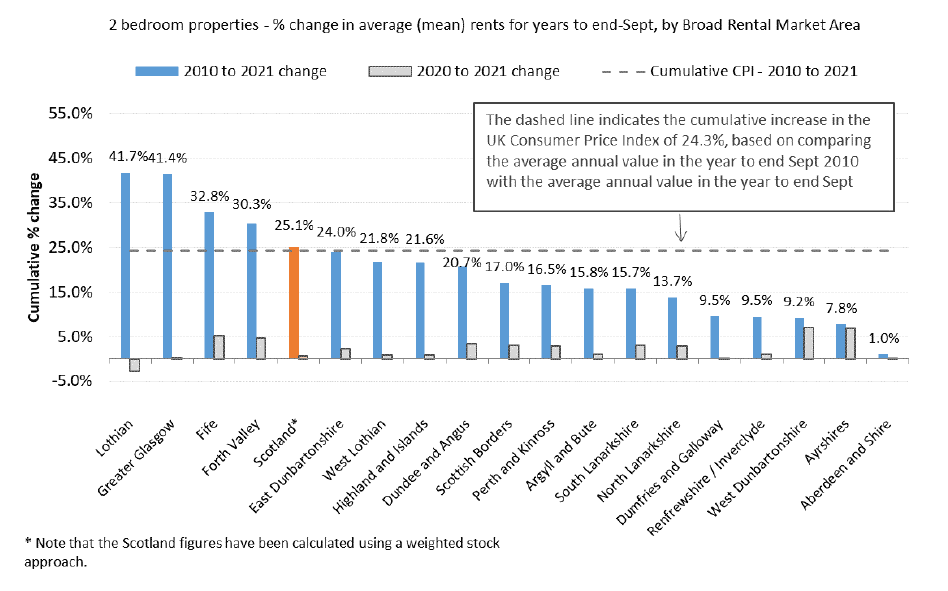

At a national level, average 2 bedroom private sector rents (the most common size of private rented sector property[37]) have risen at a cumulative rate that is broadly similar to inflation over the years 2010 to 2021, with the average 2 bedroom monthly rent increasing from £554 in 2010 to £693 in 2021, an increase of 25.1% and which compares to an increase in inflation of 24.3% (see chart below[38]).

However, behind these national trends it is important to note that average private sector rents have changed at vastly different rates across different areas of the country with Lothian and Greater Glasgow seeing average 2 bedroom rents increase substantially above both the rate of inflation and the increase in median private rented sector household incomes across the period 2010 to 2021, leading to significant financial pressure being place on those tenants.

Conversely, some other areas of the country have seen average 2 bedroom rents rise below inflation. In addition, Aberdeen City and Aberdeenshire has seen some notable changes in rents across this period in which average rents increased to 2014 before dropping back down following the downturn in the oil industry.

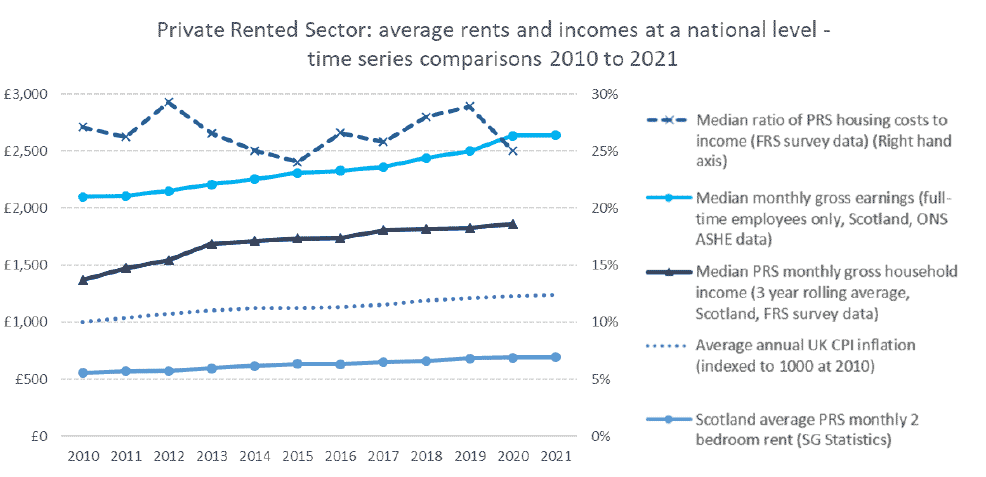

Of course, to understand affordability we also need to consider how incomes have changed overtime in comparison to rents. The chart below provides some more detail on changes over time at a national level for average rents in comparison to earnings and income.

Median gross earnings for full-time employees in Scotland have increased by 26% between 2010 and 2021, similar to the cumulative increase in average rents (25%), although the earnings figure is based on employees across all housing tenures.

There has been an estimated increase of 36% in the median monthly household income in the private rented sector from 2010 to 2020 (3 year rolling averages for each year), although this is based on measuring total household income and is unadjusted for any changes to household sizes or composition over time.

At a national level, average 3 apartment (2 bedroom) social sector rents in Scotland have risen by 24% between 2013/14 and 2020/21[39], a larger percentage increase compared to the 12% increase over this period for average 2 bedroom private rents. However social rents remain much lower on average than private sector rents, with the average monthly social housing rent of £359 for a 3 apartment (2 bedroom) property in 2020/21 equating to about half (52%) of the average 2 bedroom monthly private rent of £693.

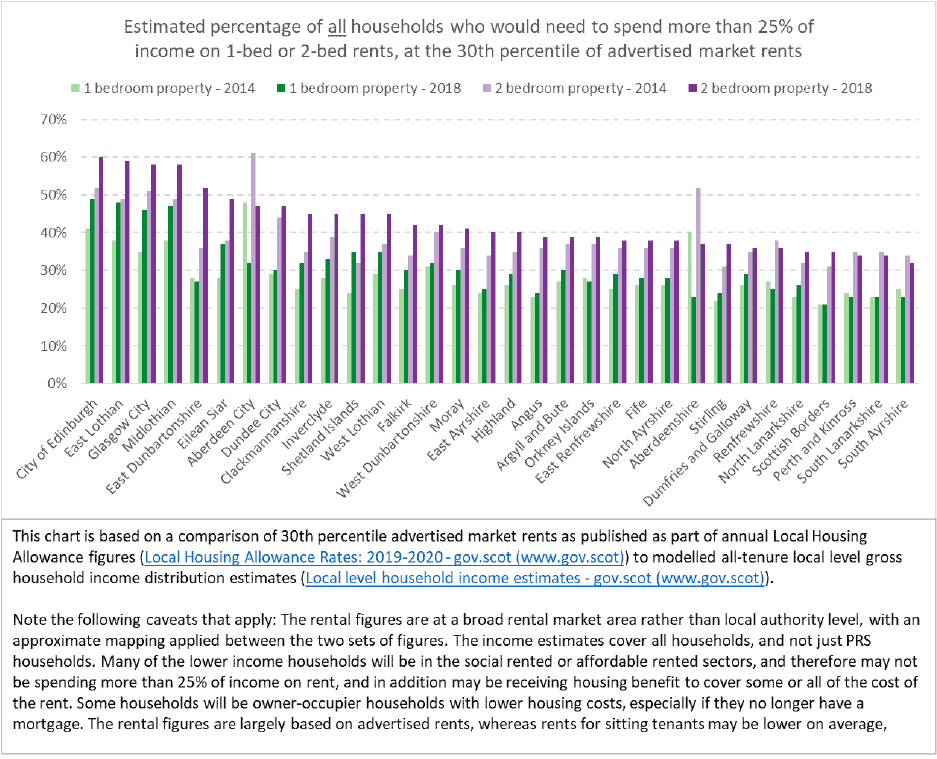

The chart below provides an illustration of variability in private rental affordability at a local level, based on a comparison of 30th percentile market rents at a broad rental market area level with separate modelled gross household income distribution estimates at a local authority level. This measure of affordability is currently used within the Housing Need and Demand Assessment (HNDA) Tool[40], when estimating future demand for housing by tenure.

For example, the 2 bedroom 30th percentile weekly rent for City of Edinburgh was £184 for the year to end September 2018, based on the average rent over the whole Lothian broad rental market area. The required weekly income so that this rent is less than 25% of the household weekly income is £736 (£184 multiplied by 4), which equates to an annual income of £38,272. The percentage of households in Edinburgh with an annual income below £38,272 in 2018 is estimated to be 60%.

For the year 2018, the areas with the highest estimated percentage of households who would need to spend more than 25% of income on 2 bedroom rents at the 30th percentile include City of Edinburgh (60%), East Lothian (59%), Glasgow City (58%), and Midlothian (58%), whilst the areas with the lowest estimated percentage include Perth and Kinross (34%), South Lanarkshire (34%) and South Ayrshire (32%).

Figures are also presented for the year 2014, in which it can be seen that Aberdeen City and Aberdeenshire had higher percentage for this year compared to 2018, which is likely to be attributable to the drop in average market rents between 2014 and 2018 following the downturn in the oil industry.

The chart also includes figures based on 1 bedroom rents, which for the year 2018 are estimated to range from 49% for City of Edinburgh to 21% in the Scottish Borders.

Note that there are a number of caveats around this analysis, which are listed below the chart and therefore the results should be treated as illustrative examples of rental affordability.

It is this spectrum of experience across the country that supports the idea of a national framework of rent regulation, which should also be capable of responding to variations in local markets.

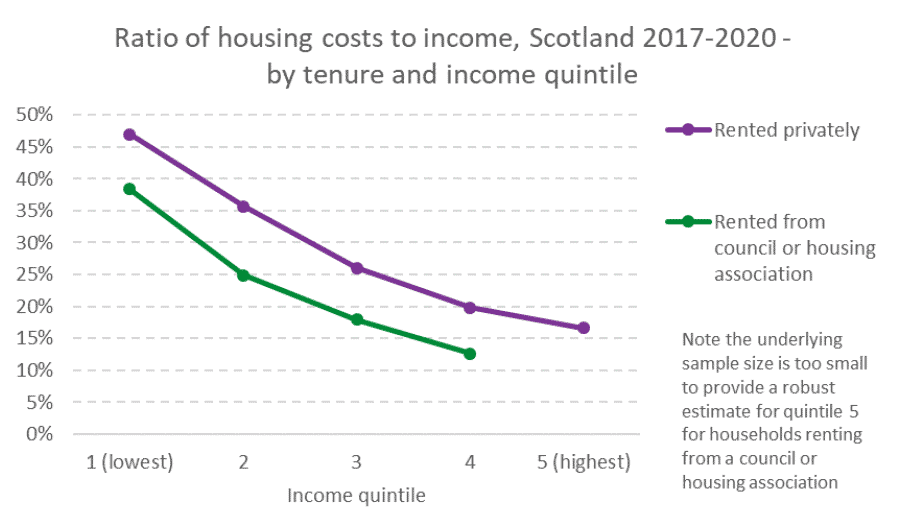

As well as variations in average rents and affordability across different areas of the country, there are also differences in affordability by level of household income. Over the latest period 2017-20, at a national level, private rented sector households in the lowest income quintile were paying an average of almost half (47%) of their household income on housing costs with the equivalent figure for social rented households in the lowest income quintile being 38%, which are much higher than for households in higher income quintiles[41].

One important contextual aspect to consider when looking at trends in affordability is the changing levels of stock over the past 25 years in which the social rented sector has shrunk by 227,000 dwellings, accounting for 23% of homes in 2018 (down from 38% in 1993).

This has been mirrored by an equivalent increase of 217,000 dwellings in the size of the private rented sector (up from 7% to 14% of the stock) and which may therefore have impacted on the affordability of rented stock overall[42].

Furthermore, as the number of households in the private rented sector has increased, the number of people in the private rented sector in relative poverty has increased and a quarter of a million (250,000) people in the private rented sector are estimated to be in poverty in the latest period 2017-20, an increase from 160,000 in 2003-06. An estimated 60,000 children were living in poverty in the private rented sector in the latest period 2017-20, up from 30,000 children in 2003-06.

In terms of support for housing costs for households in the rented sectors, in 2017 an estimated 61% of social rented households in Scotland were receiving either Housing Benefit or the Housing element of Universal Credit with the equivalent proportion for private rented households being 23%. Although it is worth reflecting that a significant number of private tenants, such as students, are not eligible for support through Universal Credit.

When looking at social rented households in Scotland in receipt of Housing Benefit across the period 2015/16 to 2017/18, the median value of the ratio of Housing Benefit to rental costs for social rented households receiving Housing Benefit was estimated to be 100% (i.e. more than half of social rented households receiving Housing Benefit were receiving an amount that covered their rent by 100%) with an estimated 67% of social rented households receiving Housing Benefit having their rent fully covered by Housing Benefit[43].

These interactions between housing costs and benefits are of potential interest to note when considering potential impacts from any future reductions to housing costs that may occur.

Improving our evidence base

There is a widespread consensus around the need for more comprehensive national collection of private rental sector data in order to better understand rental levels and how they change from year to year and to inform policy development and interventions. The collection of such data is supported by both tenant and landlord stakeholders, who are calling for future policy on rent controls to be based on clear evidence.

The lack of sufficient rental data below Broad Rental Market Area (BRMA) level and on sitting tenants, as well as the challenges associated with collecting robust statistical data at a local level, have been cited by local authorities as one of the reasons why current legislation to enable the introduction of Rent Pressure Zones (RPZ) to address areas of high rents, has never been utilised.

In response to these challenges, we committed in Housing to 2040 to put in place robust data collection approaches to ensure we can gather information to the necessary standards required for statistical purposes, helping to identify issues and problem areas and ensuring evidence-based policy making. This commitment to robust data will then support our pledge to implement an effective national system of rent controls.

It is important, that in developing our approach, we do so in a way that takes account of the wider future regulatory context. For example, the commitment to create a new housing regulator for the private rented sector in order to improve standards and enforce tenants’ rights and its potential future role in relation to data collection, rent controls and registration systems. This is examined in more detail in Chapter Six.

Learning from others: Private Residential Tenancies Board, Ireland

In the Republic of Ireland, they have a Private Residential Tenancies Board (RTB) that is a public body set up to support and develop a well-functioning rental housing sector.

The RTB remit includes regulating the rental sector, providing information and research to inform policy, maintaining a national register of tenancies, resolving disputes between tenants and landlords, investigation into improper conduct by landlords and providing information to the public to ensure tenancies run smoothly and no issues arise.

As part of their information and research role they provide accurate and authoritative data on the rental sector, such as the Quarterly Rent Index, which allows them to monitor trends in the rental sector but also allows individuals to check and compare rents in particular locations.

As at 30 December 2020 the RTB operational expenditure for the year stood at around £15 million (€18,028,712). A proportion of which is funded through registration, dispute fee income.

Existing private rented sector rental data

Nationally collected rental data currently provides information on average rents across different property sizes and is published annually in November in our Private Sector Rent Statistics in Scotland publication.

Rent Service Scotland, which is part of the Scottish Government, is responsible for collecting market rental evidence. This Market Evidence Database helps fulfil a number of statutory obligations placed on Rent Officers, including: determining annual Local Housing Allowance (LHA) levels; Local Reference Rent and Universal Credit Housing Entitlement monthly rates across 5 property sizes within BRMA[44]; Fair Rents and rent adjudications[45]; and supported accommodation referrals. Rent Service Scotland also provide data to the Office of National Statistics (ONS) and to Scottish Government Communities Analytical Division Statisticians for the publication of the Private Sector Rent Statistics in Scotland.

This market evidence data on private rents is sourced through a variety of means, including private landlord and letting agent returns, mailshot initiatives, as well as advertised rental information on internet websites. In the latest year, an estimated 90% of records were based on advertised rents, with the remainder being based on actual rents from landlord returns or where advertised rents were followed up with data suppliers to obtain further information.

Rent Service Scotland is also required to make certain information publicly available including a Fair Rent Register under the Rent Scotland Act and certain information in relation to rent adjudications.

We also get additional data and information from the existing registration systems. Landlord Registration data is gathered by local authorities and through this we get key information on the number of registered landlords and the number of registered properties by local authority.

However, as this only captures the landlord information, it does not provide a complete picture and there are risks of duplicated data due to errors in the imported data from the previous system and some double counting of rental properties in certain instances for joint owners.

Letting Agent data is available as part of the national letting agent register managed by the Scottish Government. The register captures the details of individuals and businesses acting as letting agents but does not hold information on landlords or properties that any individual agent provides services for. The Scottish Government also manages the national Property Factors register, which holds details of all individuals and businesses offering property factoring services, including details of all properties that individual factors manage on behalf of homeowners. This data covers all types of property and does not relate specifically to the private rented sector.

Additional data required

The Scottish Government has commenced work to assess and analyse what information we would need to collect in order to establish a meaningful and robust rental data evidence set, which could be used to inform future policy development and as part of fulfilling statutory requirements in relation to the setting of Local Housing Allowance.

In broad terms, the data required would need to cover all 340,000 private tenancies in Scotland (there are a number of unconventional tenancies such as agricultural tenancies, regulated tenancies or informal sub-let arrangements that would need further consideration about their inclusion but the numbers are small); collect the property address and actual rental cost of each property at the start of a new tenancy; and any in-tenancy rent increases. It would also need to be accompanied by additional information to make the rental data meaningful and usable enough for informing and monitoring the introduction and operation of national rent controls. Rental value, on its own, is unlikely to result in the ability to sufficiently analyse the data for policy or operational purposes.

Action: To ensure the evidence base on the private rented sector in Scotland is improved and can provide key evidence to support future rent control policies, we will include provisions in a Housing Bill to be introduced in 2023, that will mandate the need for private landlords to provide a range of rental data and other property information.

Whilst further work by a range of housing, analytical and IT experts is required, a list of the potential additional data that could be collected at an individual property level is set out below:

1. Rental amount (£) and whether this includes the value of any communal services charges or fuel bills (£) separately identified.

2. Propertyaddress - along with a Unique Property Reference Number to ensure every property is uniquely identified and referenced.

3. Tenancy type (i.e. regulated, assured, short-assured, private residential or another form of tenancy e.g. agricultural tenancies).

4. Type of let/re-let – we would need to know for each rental value if this relates to a property that has been rented for the first time, if it relates to a property that was previously rented and now being rented to a new tenant, or if it relates to a change to rent for an existing tenant.

5. Date - that the rental amount was applied.

6. Rental period (monthly, weekly etc) – needed so that each rental amount can be converted into a standard period e.g. monthly.

7. Property sizeand age, number of bedrooms, living rooms, kitchens, bathrooms - to allow analysis of rental changes by these key characteristics.

8. Property type (detached, semi-detached, terrace, flat etc) - to allow analysis of rental changes by this key characteristic.

9. Furnished/Unfurnished - to allow analysis of rental changes by this key characteristic.

10. Property condition - type of heating system, double glazing, car parking, garage, garden etc, plus details of any other property condition factors that may determine the rent.

11. Property improvements – we would need to know whether the rental change/increase was due to a property improvement including energy efficiency measures, and also possibly details of what type of improvement had been made.

In order to collect information on all private tenancies in Scotland, we will need an accurate and up to date register of properties and their landlords. This will also enable us to monitor the impacts of the Rented Sector Strategy on the size and structure of the sector.

We will work with Registers of Scotland, our IT partner for the Scottish Landlord Register, as well as local authority colleagues responsible for the administration of landlord registration to address known data quality issues, for example duplicate records and imported data errors from previous system, to provide this information.

Any system introduced for collecting data will also need to gather information to enable verification of the data provided, to ensure it meets necessary statistical standards and to ensure the information provided is accurate - for example, a copy of the tenancy agreement or rent increase notice.

The system will require a quality assurance facility, so any data queries can be raised with landlords. The system will also need to find a way to ensure data is provided for all properties that have had a change in rents, or a change in tenancy or other property changes that may affect the rent.

Further work from experts is needed to be clear about what data is necessary, how it will be used, processed and quality assured to stand up to public scrutiny and how it will be protected and stored. This will require a full exploration of the spectrum of different delivery mechanisms, including existing systems and the development of new ones, to decide what option would deliver best value for money.

Action: We are establishing a working group with IT, legal, policy, operational and statistical experts, to take this work forward. The group will aim to report to Ministers by March 2022 with proposals to procure a full feasibility study into possible options and the best mechanism for delivering data collection required.

Consultation Question: Do you think the data we are proposing to collect will provide all the necessary evidence to inform national and local rent control considerations? Please explain your answer.

Consultation Question: What can we do to ensure that landlords and agents provide accurate rental data (and other relevant property information), as soon as any changes are made? Please explain your answer.

In order to ensure that landlords (and letting agents acting on their behalf) provide the data that we believe must be collected to help build an effective evidence base on the private rented sector in Scotland, there is likely to be a need for a mandate.

It is currently a criminal offence for landlords not to update their landlord registration details where there is a change in circumstances. However, in practice, we know this is not a particularly effective deterrent given police capacity - therefore, a more productive deterrent may be to consider the introduction of Rent Penalty style notices by the body who will collect the data. A Rent Penalty notice is a legal notice that suspends the rent liability of the tenant(s) of a property. Local authorities can currently use a Rent Penalty Notice where a landlord has failed to register.

In order to provide tenants with information on rents for properties they are considering renting, including rents paid by previous tenants, we also propose to make this information publicly available.

Consultation Question: What is your view on making rental and property information publicly available for tenants and others to view?

Consultation Question: What is your view on enabling Rent Penalty notices to be issued where a landlord fails to provide up to date registration, rent data and property details?

Consideration of appropriate forms of rent controls

The Scottish Government has already committed to taking action so that the rented sector offers a range of high-quality homes that are affordable for those who choose to live in it, and where the affordability, accessibility and standards of the whole rented sector improve and align – and the evidence set out earlier in this Chapter provides a clear need.

Part of this action will be through introducing an effective national system of rent controls, with an appropriate mechanism to allow local authorities to introduce local measures by the end of 2025.

Existing legislation controlling Rents

Key Private Rented Sector Legislation

The Private Residential Tenancy came into force on 1 December 2017 and included new rights to help tackle increasing rents by:

- limiting rent increases to once in 12 months, with a landlord required to give three months’ notice in advance of the increase;

- enabling tenants to challenge unfair rent increases via adjudication by a Rent Officer; and

- introducing the ability for local authorities to apply to Scottish Ministers to designate an area as being of Rent Pressure Zone status.

The Private Rented Tenancies introduced sweeping reforms which meant that private tenants now have more protection in Scotland than any other part of the UK. However, we have been monitoring the impacts and now is the time to strengthen the parts of it that have not worked as anticipated.

The three particular provisions (set out above) were introduced to limit landlords being able to impose unfair or multiple rent increases at short notice, and that has proved popular and successful. However, whilst all private tenants with a Private Residential Tenancy agreement do have the ability to challenge unfair rent increases, very few people have requested a rent adjudication, in fact between 1 December 2017 and 30 November 2021, only 89 applications have been made. There may be a number of reasons for this including:

- tenants being unaware of their existing rights to challenge rent increases;

- people feeling worried that by taking such action, it could have repercussions on their tenancy or relationship with their landlord;

- Rent Service Scotland (and the Tribunal, on appeal) are in principle able to increase the rent that a landlord charges – above that being requested – to bring it in line with market levels; and

- Landlords not increasing rents during a tenancy and instead increasing them between tenancies, which is not covered in the Private Residential Tenancy.

The Scottish Government have already taken action on raising awareness of all existing rights for private tenants, through awareness raising and media campaigns, but, as set out in chapter 3 and re-iterated here, we also plan to do more so people can make best use of the existing rent adjudication process.

Action: For private tenants seeking rent adjudication, we will change the legislation to only allow adjudications that either decrease or maintain it at the level proposed by the landlord.

This action would allow people to challenge in-tenancy rent increases without fear that such action could result in an increase in rent beyond that being proposed by the landlord in the rent-increase notice. It would still balance the rights of landlords and tenants, as the rent that a landlord has fully considered and set themselves, could either be maintained or reduced.

Consultation Question: Do you agree that the rent adjudication process should only result in rents being decreased or maintained? Please explain your answer.

In relation to Rent Pressure Zones, we are aware that the lack of data has meant that they have not been established, as we would have hoped. For this reason, and because of the need to tackle high rents, the Scottish Government has instead committed to implementing an effective national system of rent controls, with an appropriate mechanism to allow local authorities to introduce local measures, by the end of 2025. The principles and approaches to this are detailed later in this chapter.

Key social rented sector legislation

There are a number of safeguards, legal requirements and checks in place in the social rented sector in relation to rent levels, rent setting and affordability. The Housing (Scotland) Act 2001 requires a social landlord to consult its tenants and have regard to their views where they are proposing to increase rents or any other charges for Scottish Secure Tenants.

The Scottish Social Housing Charter reinforces this legal duty and includes outcomes on value for money, rents and service charges and requires that social landlords set rents and service charges so that a balance is struck between levels of services provided, the cost of the services and how affordable they are to both current and prospective tenants. Social landlords also need to demonstrate transparency in how rents are calculated.

The Scottish Housing Regulator is responsible for monitoring landlords’ performance against the Charter. Rent affordability is also part of the Regulators annual risk assessment of all social landlords. Its “National Report on the Charter Headline Findings 2020 – 2021” reported that despite a small reduction of 1% from the previous year, 83% of tenants are satisfied that their rent is good value for money. In addition, average planned rent increases went down to 1.2% from 2.5% last year.

The Scottish Government also considers the proposed rents for Registered Social Landlord social rented homes at the point of first let when assessing applications for grant funding through the Affordable Housing Supply Programme. At tender stage, proposed Registered Social Landlord rents (which should be projected to the date of completion) are compared against relevant social rent benchmarks. RSLs are required to justify why a proposed rent is considered affordable if the benchmark is exceeded by more than 5%, with the approval of rents exceeding benchmark by more than 10% being given only in exceptional circumstances.

Recent statistics also suggest that between 2014 and 2021, on average rent increases have risen twice as fast in the social rented sector (24%) compared to the private rented sector. However, they still remain on average half the level of the private rented sector[46].

In Housing to 2040, we set out a vision for tenure neutral outcomes - in other words, people have a warm, comfortable home that meets their needs no matter what tenure they are in. At the moment, the social rented sector already has a number of safeguards in place to protect tenants in a meaningful and demonstrable way. In addition, the very premise of social rents mean that all money is re-invested for the good of tenants in the sector overall. This is not true in the private rented sector where approaches to rent setting can be very different between landlords, and there is a greater need to ensure there are reasonable rents and that tenants can challenge where this isn’t the case.

Proposition: National rent controls only apply to the Private rented sector

However, that is not to say that the Social Rented Sector cannot be improved and we are aware of higher rents in certain areas, therefore we will continue to consider how to build on the strong work already put in place around rent setting in the social rented sector in the future.

Consultation Question: Do you agree with the proposal not to extend any national rent controls to the social rented sector?

Yes, No, Don’t know - Please explain your answer.

Consultation Question: Do you think the current safeguards for rent setting in the social rented sector are sufficient and, if not, how could they be strengthened?

Please explain your answer.

Vision and principles of future rent controls

Our vision is for people to have equality of outcomes no matter what tenure they live in and ensuring rent affordability in the private rented sector is an absolutely essential part of realising that vision.

Rent control policies are aimed at regulating the rental prices of properties with the objective of making rents more affordable and tenants less likely to be ‘priced out’ of housing due to rent increases. Rent control is a wide term that encompasses a number of differing types of interventions.

Most commonly, the research literature refers to first, second and third generations of rent controls. First generation rent controls introduce a rent freeze of nominal rents. Second generation refer to rent regulation, setting an automatic rent increase percentage based on inflation. Third generation see rent increases controlled within a tenancy but with no control between tenancies.

Taking action to ensure affordable rents aims to ensure that tenants will have stability and value for money. It will also contribute towards wider policy ambitions of reducing poverty and improving housing allowance systems. However, some have argued that the introduction of rent controls could restrict supply, should investors feel they cannot realise the levels of return which make new supply viable or attractive.

Any reduction in supply may unintentionally create increased demand for existing homes and lead to rising rents as a result. Equally, any system should not discourage investment in the management and maintenance of properties. We need a clear understanding of the interaction between rent levels, demand, and supply of both new housing for rent and the movement of existing properties in and out of the rented sector.

Consideration must therefore be given to how a workable and evidenced system of rent controls will interact with supply and quality within the sector. Regulatory intervention on rent controls must also be seen in the wider, future legislative context, whereby a Regulator for the sector will be in operation and tenants will have significantly increased rights.

We will be undertaking a separate consultation with detailed proposals for rent controls later in this Parliament, but as part of this consultation we are seeking views on the proposed underlying vision and principles that we believe should underpin future rent control regulation:

Proposition

Vision for future rent controls: Tenants pay affordable and reasonable rent for good quality homes, helping to support efforts to reduce poverty and improve outcomes for low income tenants and their families.

Underlying principles for national rent controls:

- They will have an appropriate mechanism to allow local authorities to introduce local measures.

- They will be evidence based.

- Their design will support and encourage the private rented sector to improve the quality of rented properties.

- Policy development on rent control legislation will seek to learn from the processes already in place for social sector tenants in relation to rent levels.

- Policy will be developed taking into consideration the views of all stakeholders but with a particular focus on giving private tenants a stronger voice.

Consultation Question: Are there elements of the existing Rent Pressure Zone system that could be built upon when designing a new system of rent controls? Please explain your answer.

Consultation Question: Do you agree with the vision and principles set out above in relation to a future model of rent controls for the private rented sector in Scotland? Please explain your answer.

Conclusion

This chapter demonstrates that the influences on rent levels are multiple and complex, with significant variations experienced across the country.

It demonstrates the clear need to improve our data collection in the private rented sector – and sets out how we intend to do so, so as to develop a sound evidence base for future policy development in this area.

However, it also acknowledges the risks that exist and the impact this could have on wider supply – an area we go on to explore further in the next chapter.