A New Deal for Tenants - draft strategy: consultation

We are consulting on the draft A New Deal for Tenants - rented sector strategy, which seeks to improve accessibility, affordability choices and standards across the whole rented sector in Scotland.

Chapter Two: Sector Overview And Policy Context

Scotland’s Rented Sector

Around 37% of households in Scotland currently rent the home they live in. While in the past the majority of rented homes were provided by local authorities, we now have three major sources of homes for rent providing broadly similar numbers of homes: private rented homes (14%); local authority housing (14%); and homes for social rent provided by Housing Associations (10%)[2].

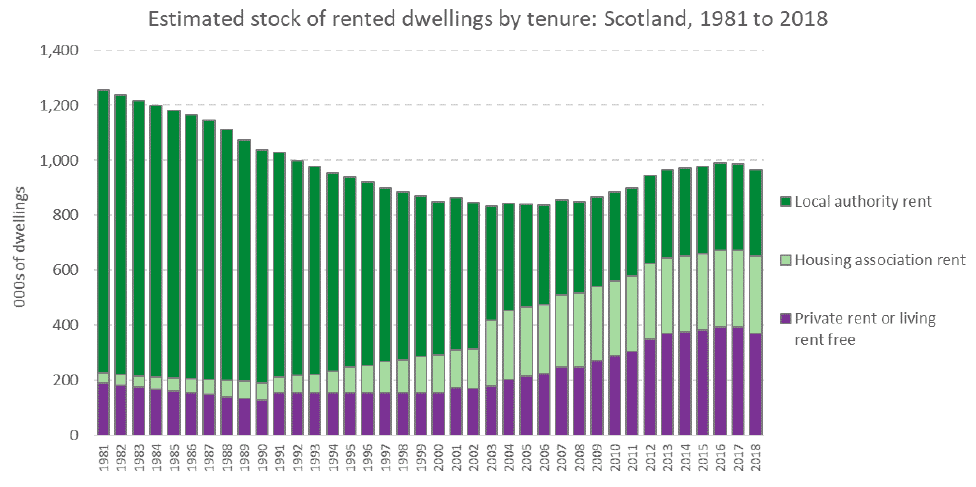

The nature of the private and social parts of the rented sector have evolved over time. Over the longer term, since 1981, the number of local authority rented homes has shrunk by some 713,000 properties due to Right to Buy sales as well as stock transfers to housing associations over this period.

However, the rate of decrease has slowed in recent years due to an increase in new supply of local authority housing from 2007 onwards and the Right to Buy scheme ending in 2016. In addition, the proportion of homes that are social rented (23%) remains a notably higher proportion than in England or Wales (17% and 16% respectively in 2018[3]).

This long-term decline in the percentage of social housing has been accompanied by substantial changes in the profile of its tenants. Results from the Scottish Census[4] show that in 1981 the profile of social sector tenants was similar to the profile of all Scottish households in terms of size, composition and social and economic characteristics.

This is no longer the case, with household characteristics in more recent years showing some marked differences by housing tenure, with households in social housing now being more likely to consist of single pensioners and single parents.

Tenants of social landlords are less likely to be in employment than those in households generally, with less than half of tenants being in employment. Social tenants are also more likely to be unemployed or chronically ill than other households. Consequently, 60% of social rented households have incomes of £20,000 or less a year and around 61% are in receipt to some extent of housing benefit or the housing element of Universal Credit[5].

Social rented homes are provided by around 150 housing associations and 26 out of 32 local authorities (with 6 authorities no longer managing housing stock due to previous stock transfers to housing associations). We know there is high demand for social homes with an estimated 130,000 (5%) of households on a housing list in 2019, with a further 20,000 (0.7%) of households estimated to have applied for social housing using a choice based letting system within the last year[6].

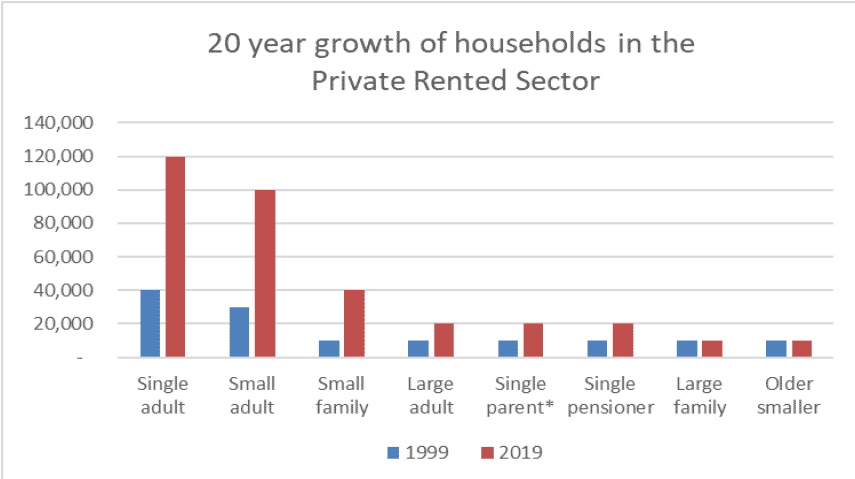

Meanwhile over the past 20 years the private rented sector has grown by more than 2 and a half times from 130,000 to 340,000 households, during which period the percentage of younger households owning with a mortgage decreased over the years from 2003 to 2015, likely due to the increases in house prices from 2002 to 2008 and the subsequent impacts of the financial crisis from 2008 onwards. In 2019, the private rented sector was home to 710,000 people, including 120,000 children, about 13% of the Scottish population.

Much of the growth has been in single adult and small adult[7] households, although there have also been noticeable increases in other household types, especially small families.

There is more variation in experience and circumstances among those living in the private rented sector. Whilst the private rented sector is dominated by younger households, there are a mix of household types living in the sector, with over a third (37%) having a household income of £20,000 or less, over a fifth (22%) of households having children, almost a fifth (17%) of adults being in further or higher education, and 8% of adults being retired from work.

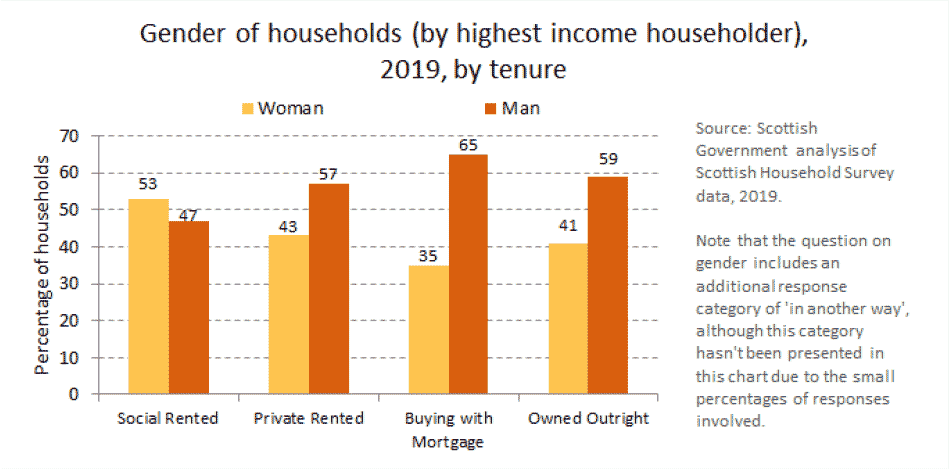

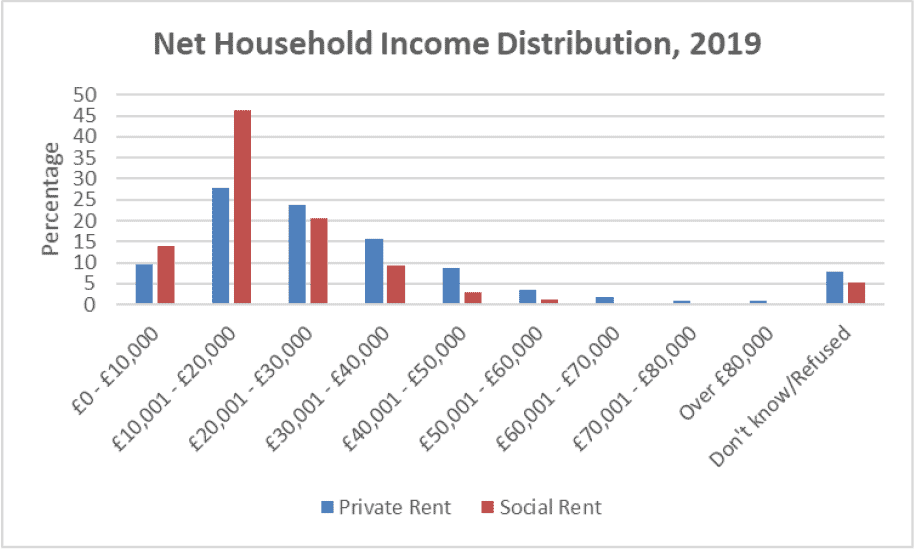

In the social rented sector, an estimated 54% of households have a highest income householder who is female, with the equivalent percentage for private renting households being 43%[8]. Scottish Household Survey findings for 2019 show that 53% of householders in the private rented sector are under 35 years old (based on the HIH), and that 59% of households in the social rented sector in Scotland have someone living with a long term physical or mental health condition or illness[9]. The findings also show that 37% of private rented sector households and 60% of social rented sector households have a net household income of £20,000 or under.

The experience of affordability within the private rented sector is also likely to be very different for tenants with lower incomes compared to the tenants with higher incomes. Over the latest period 2017-20, private rented sector households in the lowest income quintile were paying an average of almost half (47%) of their household income on housing costs, compared to only 17% for private rented sector households in the highest income quintile[10].

Housing experiences for minority ethnic households

As highlighted in a recent evidence review of the housing needs of minority ethnic groups in Scotland[11], the minority ethnic population in Scotland is not a homogenous group and each ethnic group has differing practical and cultural needs, which often vary from white Scottish/British households. Evidence suggests that, in respect of tenure, the private rented sector can offer greater flexibility and choice for some minority ethnic groups. However, there are indications that the specific housing needs of some minority ethnic groups are not being fully met. There is evidence that a higher proportion of minority ethnic highest income householder (HIH) households had some level of disrepair to the dwelling and overcrowding for minority ethnic HIH households was a particular issue. This is likely due to higher rates of disrepair found in the private rented sector combined with the higher prevalence of minority ethnic households in this tenure.

Minority ethnic households are more likely to live in the private rented sector and on the whole are less likely to live in the social rented sector or in owner occupation than white Scottish/British households. Combined Scottish Household Survey data from 2017-2019 indicates that where the HIH is from an ethnic minority group, households were more likely to be living in the private rented sector than white Scottish/British HIH households. Depending on ethnic group, 32-50% of minority ethnic households live in the Private Rented Sector, compared to 11% of white Scottish/British households.

People from minority ethnic groups are also more likely to be living in relative poverty after housing costs than people from the ‘White – British’ (including white Scottish) group. In 2015-20 the poverty rate was 41% for the ‘Asian or Asian British’ ethnic groups, and 43% for ‘Mixed, Black or Black British and Other’ ethnic groups, compared with 24% for ‘White - Other’ and 18% for ‘White - British’[12].

Secondary analysis of the Scottish House Condition Survey (SHCS) found indications that occupancy levels in minority ethnic HIH households were much higher than in white Scottish/British HIH households and, as a consequence, these households were more likely to be overcrowded. Some minority ethnic households contained larger families, with 3 or more dependent children, or engaged in extended family living. For these families, a lack of affordable larger properties in the private rented sector often meant living in housing which didn’t meet their need for space.

For some ethnic groups, the risk of experiencing homelessness may be higher. 13% of main applicants in households assessed as homeless/threatened with homelessness had a reported ethnicity other than ‘white’; this compares to only 5% of the Scottish (adult) population. Factors that increased the risk of experiening homelessness were experiences of domestic abuse and recent arrival in the country.

Although evidence in Scotland is limited, some UK studies have shown that while individuals from minority ethnic communities face common housing problems and may find accessing services difficult, certain groups can face particular challenges where ethnicity intersects with other protected characteristics. In particular, minority ethnic women and older people may face particular challenges in accessing and securing housing. For some minority ethnic women, isolation, language difficulties and experiences of racism, may increase their risk of experiencing homelessness or prevent them from escaping domestic abuse. With regards to older people, a lack of language skills, low awareness of housing services and mobility issues often left them in accommodation which was unsuitable and did not fully meet their needs.

A recent evidence review by the Scottish Government found limited evidence on the ways in which ethnicity intersects with disability. However, data from the Scottish Survey Core Questions 2018 indicates that minority ethnic groups were less likely to report that they were living with a limiting long-term physical or mental health condition than their white Scottish/British counterparts. Although, these lower levels may, in part, be attributable to the younger age profile of some minority ethnic groups.

Housing experiences for people with disabilities

A Scottish Government report from 2016 on housing pathways for people with disabilities found three key issues affected their housing experiences, including a lack of suitable housing; struggles accessing and maintaining support; and the expectations of housing officers, care professionals and parents. Positive housing experiences for people with disabilities were seen to be characterised by five factors, including location; space; participation (including choice in housing decisions); information; and social and emotional understanding[13].

The report showed that unsuitable housing can leave disabled people and/or their carers ‘trapped’ within their home and this feeling can lead to poor mental health. Housing should allow its occupants as much independence as possible and greater control and choice on how they live.

Housing experiences for women

Rental experiences can also have a gendered dimension. According to the Wealth in Scotland report[14], lone parents (of whom 76% in Scotland are women) and working-aged women with no children are the least likely groups to own any property. According to the Scottish Household Survey, households where women are the highest earner are less likely to own or rent a private property than those where men are the highest earner, and are overrepresented in the social rented sector (see chart below).

Within Scotland, single women are more likely to be recipients of Housing Benefit than single men. Whilst a precise gender breakdown isn’t available for other household types on Housing Benefit or for households receiving the housing element of Universal Credit, the available data suggests that it is likely that women in Scotland are overall more likely to be in receipt of Housing Benefit or the housing element of Universal Credit than men[15]. Additionally, although the gender pay gap in Scotland is lower than that of the UK more widely, its continued existence means that women are likely to pay proportionately more of their income to obtain a mortgage.

In a 2020 review of evidence related to Gender, Housing and Homelessness in Scotland, Engender[16] found that women's access to adequate and safe housing is linked to structural and systemic gender inequalities such as women’s economic inequalities, violence against women, and women's position in domestic spheres. Within the labour market, women are more likely to be in part time and low paid/precarious work but are also likely to shoulder unequal responsibility for unpaid caring.

More generally, women also spend a higher proportion of net income on housing (and fuel and food)[17]. Additionally, while men are more likely to present as homeless, women are more likely to provide reasons for homelessness as violent household dispute, fleeing non-domestic violence or harassment (men are more likely to give a reason of non-violent household dispute).[18]

Affordability of rents in the rented sectors

Affordability of rents is a recurrent debate in the rented sector, most obviously in the private rented sector where rents are higher. Above, we highlighted the stark contrasts in rent to income ratios between higher or lower income groups in the private rented sector. Similar contrasts can be seen looking at rents in different market areas.

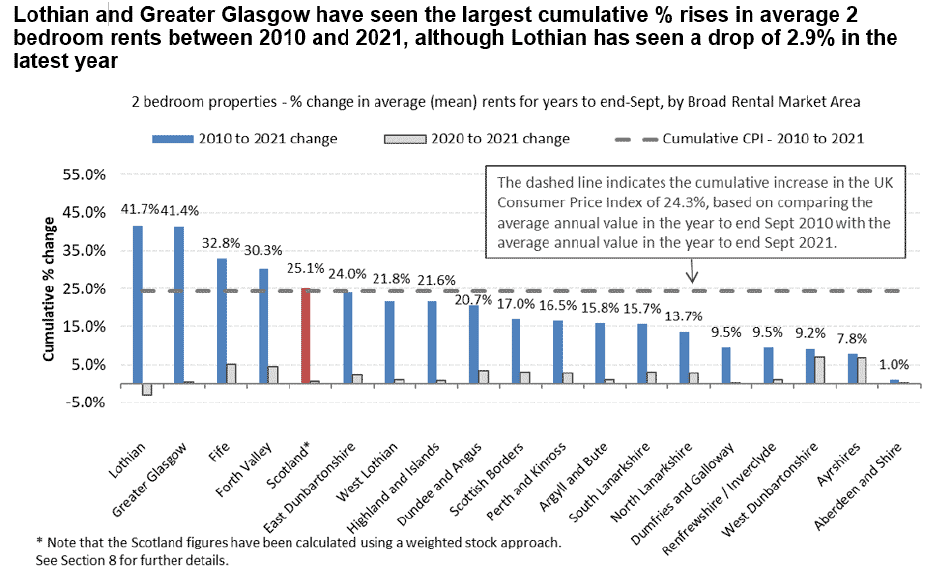

At a national level, average rents for 2-bedroom properties, the most common property size in the private rented sector, have increased around the rate of inflation over the past 10 years. However these trends have not been uniform across all regions of Scotland.

In particular, Lothian and Greater Glasgow have seen rent increases of 41.7% and 41.1% respectively, compared to the corresponding inflation rate of 24.3%. Fife and Forth Valley have also seen above inflation increases, whereas all other regions of Scotland have seen increases below the rate of inflation.

There is a higher risk that some households in the private rented sector areas who have experienced large rental increase or who have limited options but to move into properties with high rents, cannot afford to stay in their homes without having to compromise on other necessities to maintain an acceptable standard of living. As a result, some of these households will be in income poverty, child poverty or fuel poverty after housing costs have been taken into consideration.

At a national level 37% of households in the private rented sector have a net household income of less than £20,000, rising to 61% with less than £30,000. In the social rented sector, 81% of households have a net household income of less than £30,000. Market rents in the private rented sector are higher than social rents. These two factors combine to result in similar levels of average housing affordability across these sectors.

Crucially, it also means that households on a low income in the private rented sector are more likely to struggle with being able to afford their rents than households on a low income in the social sector, especially if living in areas such as Lothian and Greater Glasgow where rents are high and have increased greatly in excess of inflation over the past 10 years.

The situation of high and rapidly increasing rents in the private rented sector, especially in areas with low to moderate household incomes needs will be addressed by the introduction of rent controls as part of this strategy.

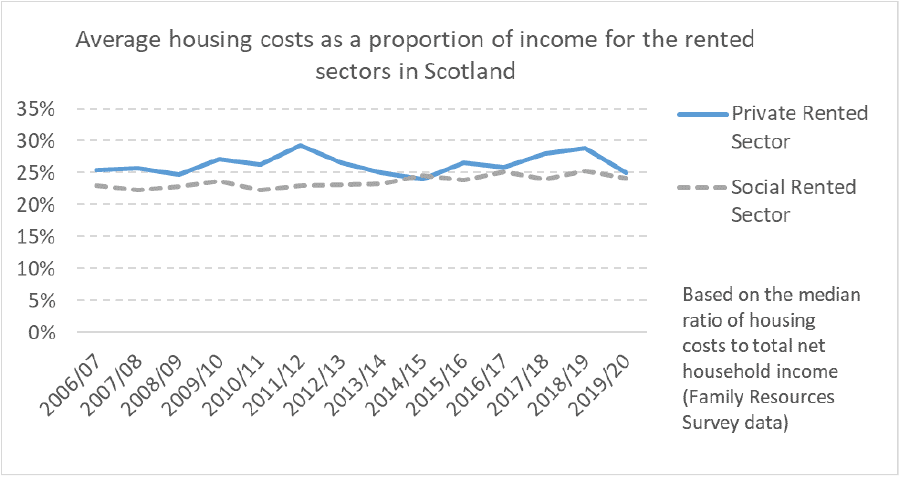

At a national level, the average affordability of housing costs (including rents) as a proportion of income has fluctuated for the private rented sector over the past 13 years, with identical proportions of 25% in both 2006/07 and 2019/20.

To some extent this will reflect increases in average incomes of households in the private rented sector, where median income increased 35.9% (over the 10 year period 2007-10 to 2017-20), considerably above the rate of inflation of 24.3%. For much of the past 13 years, affordability in the private rented sector by this measure has been worse than in the social rented sector, although by 2019/20 the two rates had converged again at around 25%.

Although these national average trends are informative, we need to assess subnational levels of housing affordability, where local rents and local incomes can be taken into account. Furthermore, we need to focus in on those households in the private rented sector on lower incomes, who are experiencing most financial hardship from unaffordable rents.

In the social rented sector, average 3 apartment (2 bedroom) rents have risen by 24% between 2013/14 and 2020/21, a larger percentage increase compared to the 12% increase over this period for average 2 bedroom private rents. However social rents remain much lower on average than private sector rents, with the average monthly social housing rent of £359 for a 3 apartment (2 bedroom) property in 2020/21, equating to about half (52%) of the average 2 bedroom monthly private rent of £693. When looking at average affordability of housing costs (including rents) as a proportion of income, this average has remained relatively stable over the past 13 years in the social rented sector, with similar proportions of 23% in 2006/07 and 24% in 2019/20.

In a similar way to the private rented sector, the experience of affordability in the social rented sector is likely to be very different for tenants with lower incomes compared to the tenants with higher incomes. Over the latest period 2017-20, social rented households in the lowest income quintile were paying an average of 38% of their household income on housing costs, a much higher percentage than for households in higher income quintiles[19].

Condition of properties in the rented sector

Overall, the condition of properties in the private rented sector is not as high as in other sectors. This needs to be addressed in order to ensure everyone has a warm, safe, affordable home to live in.

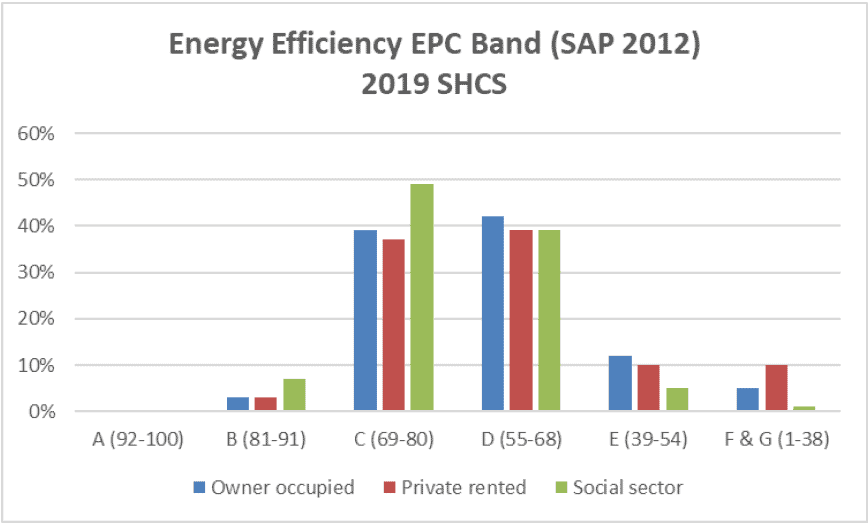

In 2019, 20% of dwellings in the private rented sector were in the lowest energy efficiency bands E,F,G (as measured by Standard Assessment Procedure (SAP) 2012), compared to 17% in owner occupation and 6% in the social rented sector.

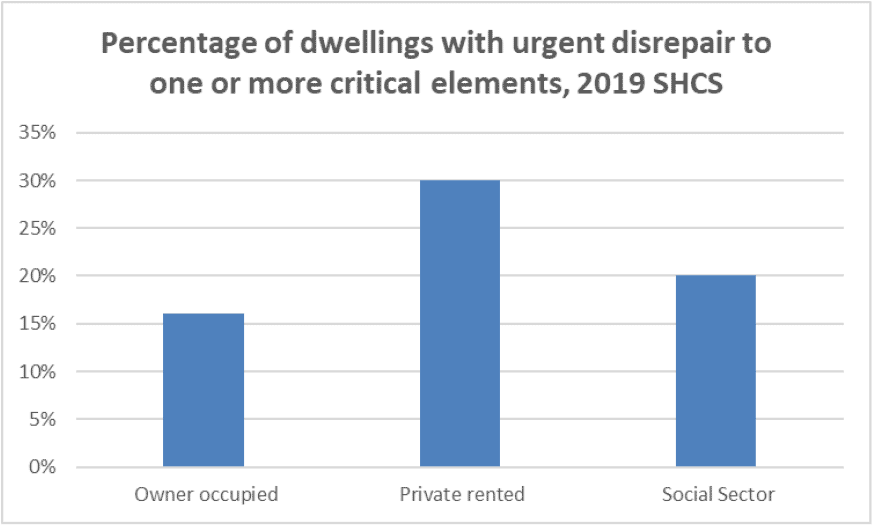

30% of dwellings in the private rented sector in 2019 had an urgent disrepair to one or more critical elements, compared to 20% in the social sector and 16% in owner occupation.

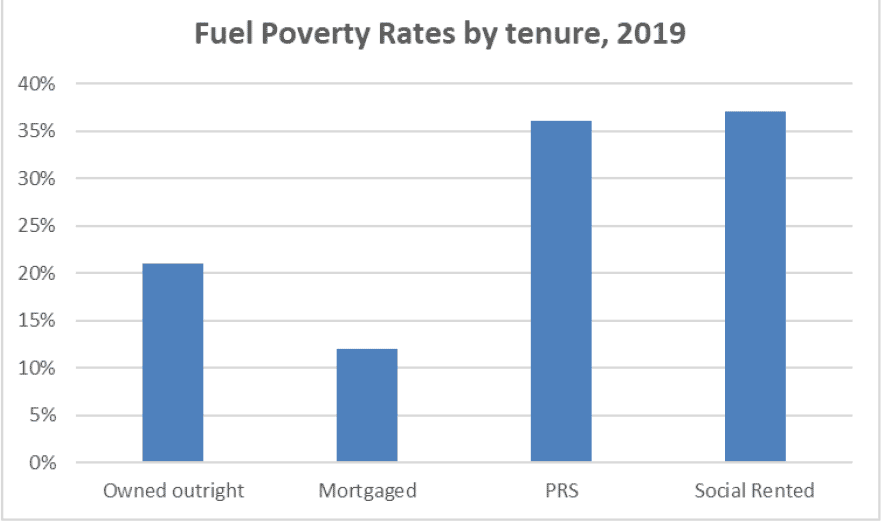

In 2019, the fuel poverty rate, which reflects household incomes, rents and other housing costs as well as levels of energy efficiency was 36% in the private rented sector. This is similar to 37% in the social rented sector, but higher than the 12% for owner occupiers with a mortgage and 21% for those who own outright.

Current Regulatory Framework

The social and private rented sectors in Scotland have fundamentally different characteristics and are structured very differently, which must be considered when attempting to align standards, approaches and outcomes.

Regulation plays an important role in the effective and efficient functioning of the private and social rented sectors, although there are different opinions on the adequacy or impact of the range of measures that regulate both.

For example, in the private rented sector, the introduction of the Private Residential Tenancy in 2017 saw a range of new rights provided to tenants – however many claim it does not go far enough and measures such as rent adjudication and Rent Pressure Zones have not achieved the desired policy outcome.

In the social rented sector, with the establishment of the independent Scottish Housing Regulator in 2011, the focus of regulation is on landlord self-assurance and the promotion of a strong tenant voice.

Private Rented Sector

The following diagram highlights the main provisions governing regulation of the private rented sector in Scotland, and when they were introduced:

PRS Regulatory Framework

- The Assured Tenancy Regime (1989)

- Housing in Multiple Occupation (2000)

- Landlord Registration (2006)

- The Repairing Standard (2007)

- Private Rented Housing (Scotland) Act 2011

- Tenancy Deposit Schemes (2012)

- Regulation of Property Factors (2012)

- Housing and Property Chamber Tribunal (2016)

- Private Residential Tenancy (2017)

- Regulation of Letting Agents (2018)

As the diagram illustrates, the framework for regulation of the private rented sector has evolved incrementally over a significant period of time.

Social Rented Sector

Regulation of housing associations has been in place for decades, with the extension to local authority housing and homelessness functions more recently. The Scottish Housing Regulator, which was established by the Housing (Scotland) Act 2010, is responsible for the regulation of all social landlords in Scotland.

The Scottish Housing Regulator is the independent regulator of social landlords (local authorities and Registered Social Landlords) and has the single statutory objective of safeguarding and promoting the interests of current and future tenants of social landlords and other users of social landlord services.

Their regulatory framework sets out how they regulate Registered Social Landlords and the housing and homelessness services provided by local authorities with landlord self-assurance at its heart.

The main duties of the Scottish Housing Regulator are to:

- monitor, assess and report on social landlord performance, particularly against the standards and outcomes in the Scottish Social Housing Charter;

- monitor, assess and report on the financial health and governance of RSLs; and

- support social landlords to become compliant with the regulatory standards and – where appropriate – take intervention action, including statutory intervention, to protect the interests of current and future tenants and other users of social landlord services.

Scottish Housing Regulator (2011)

- Regulates the financial health and governance of Registered Social Landlords

- Regulating to protect the interests of tenants, people who are homeless, and others who use social landlords' services.

- Regulates the performance of housing services by all social landlords

- Scottish Social Housing Charter (2012)

Conclusion

In pursuing significant change in the rented sector to promote greater affordability, quality and fairness it is essential we consider proposals in the context of both the private and social rented sectors, along with the regulatory framework within which they currently operate, as set out in this chapter. This provides a useful overview when considering what further changes we can make to help provide affordable choices and to ensure tenants’ rights are enhanced, which we examine in greater detail in the following chapter.