Publication - Research and analysis

Monthly economic brief: September 2021

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business Activity

Business activity remains broadly stable following a strengthening in Q2 as the majority of lockdown restrictions are removed.

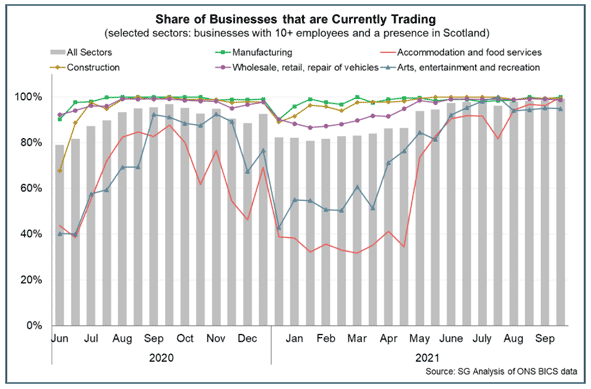

Proportion of business trading

- The phased easing of restrictions since April and the move to beyond level 0 restrictions in August (with some protective measures remaining place) has continued to enable stronger business activity in Scotland, particularly in consumer facing services.

- In September, the share of businesses trading continued to edge upwards to 99.4%, its highest level since comparable estimates began in June 2020, having fallen to a low of 82% during lockdown in January.[3]

- The difference in trading status between sectors which have been most directly impacted by restrictions in the first half of the year and those to a lesser extent, has very much narrowed in recent months. In August, 100% of business in accommodation and food services and 95% in arts culture and recreation were trading (up 65 and 44 percentage points respectively from April). For arts, culture and recreation, this remains slightly lower than in non-consumer facing services sectors (e.g. information and communication) and manufacturing and construction, which have been less directly impacted by restrictions with generally over 97% of business trading over this period, reflecting the ability to continue operating through home working or adapting workplaces.

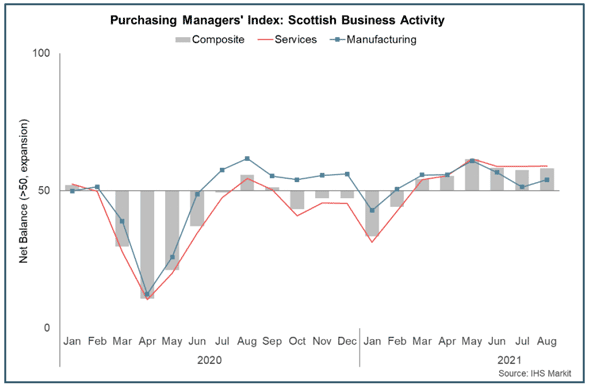

Business output

- The Purchasing Managers Index (PMI)[4] business survey reported a slight pick-up in business activity growth in August (58.1), supported by further growth in new business and with services sector activity continuing to outpace manufacturing at this stage of the recovery.

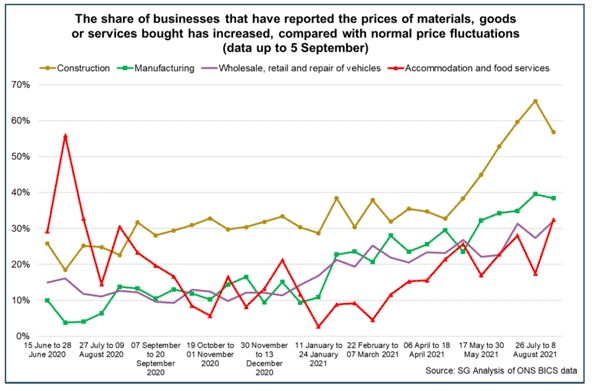

- On the supply side, input cost pressures (e.g. raw materials) have risen sharply over the past year, although to date this has only been partly passed on to sale prices. At the start of September, 26% of businesses reported above normal price increases in materials, goods or services bought by the business while 9% of businesses reported an above normal increase in the prices of goods or services sold by the business.[5]

- However, there are large differences across sectors with 57% of construction businesses reporting an above normal increase in input costs compared to 38% in manufacturing, 32% in wholesale, retail and repair of vehicles, and 32% in accommodation and food service businesses.

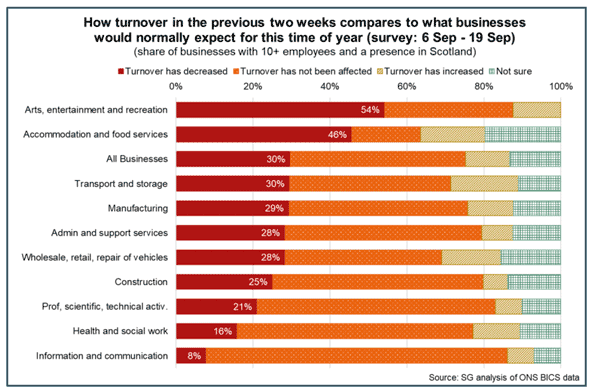

- In terms of business turnover in September, 30% of businesses reported having lower turnover than normal for the time of year, while 46% reported that turnover was not affected and 11% reported that it had increased.[6] However, lower than normal turnover continues to be most widespread in the arts, entertainment and recreation services sector (54%) followed by the accommodation and food services sector (46%).

- In line with the easing of restrictions there has been a downward trend in the estimated share of businesses reporting lower turnover. For example, since March the proportion of business reporting lower turnover has fallen from around 45% to 29%, while the proportion reporting a rise in turnover has increased from around 6% to 11%. However, trading conditions remain challenging alongside the specific challenges that different sectors are facing at their stage of recovery.

- Looking to the year ahead, the PMI business survey reported that business optimism has softened from recent months, however remains elevated overall, with strong expectations from businesses of further strengthening in business activity to come over the year. The Flash UK PMI signalled that business activity continued to soften in September, particularly in the manufacturing sector amid ongoing severe supply chain disruption while input costs continued to rise.[7]

Trade

- International trade and supply chains have experienced significant challenges in 2021 arising from the impacts of the pandemic and the transition to the new trade agreement between the UK and EU which includes the introduction of new regulatory and administrative compliance checks on goods trade.

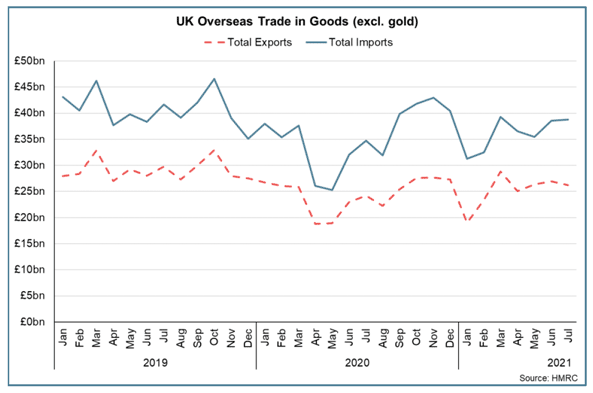

- In the first quarter of 2021, the value of Scotland's goods exports were £6.2 billion, down 15.2% compared to Q1 2020, while imports were £5.3 billion, down 3% over the same period.[8] The fall in exports was mainly driven by a 36% fall in exports of oil and gas, with notable falls across other commodities including food (-20%) and beverages (-2.9%). However, there was a 19% increase in exports of chemicals.

- More recent monthly UK data for July[9] signals that trade has strengthened from the falls at the start of the year, however total goods exports fell 2.6% over the month with an 11% fall in exports to the EU offsetting a 7% rise in exports to non-EU countries. Furthermore, goods exports in 2021 so far (Jan – July) remain 11% below the equivalent period in 2018. In terms of key exporting sectors for Scotland, in July, total exports of Scotch whisky were up 3% over the month and in the first seven months of 2021 were the same as in the corresponding period in 2018. Exports of fish fell 5% in July and in the first seven months of 2021 were 11% down on same period in 2018.

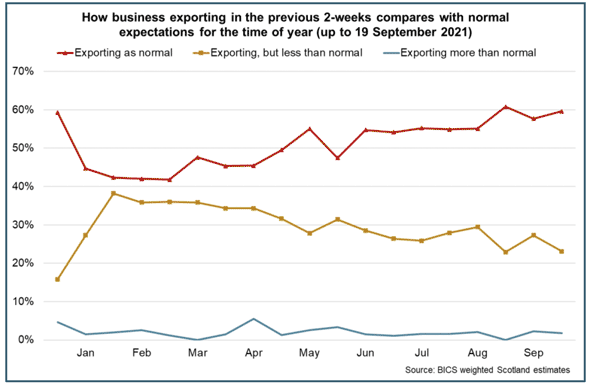

- More recent business survey data for September also indicates improvement in trade activity from the start of the year with 60% of Scottish businesses reporting to be exporting as normal for the time of year (up from 42% at the start of February) while 23% were exporting less than normal (down from 38% at the start of February).[10]

- However, supply chain bottlenecks have emerged as the global economy adjusts and rebalances from the impacts of restrictions during the pandemic, while for some sectors, the new trading relationship with the EU provide further challenges.

- In August and September, 36% of exporters and 39% of importers reported facing changes in transportation costs while 13% of exporters and 16% of importers reported a lack of hauliers to transport goods or lack of logistics equipment.[11]

Contact

Email: OCEABusiness@gov.scot