Publication - Research and analysis

Monthly economic brief: March 2022

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business Activity

Business activity has strengthened with the removal of Omicron restrictions, however cost pressures continue to build alongside concerns about the situation in Ukraine.

Business activity and trading status

- Covid restrictions continued to be eased over February and March with the removal of remaining legal requirements for business and services providers, except for the use of face coverings on public transport and most indoor public settings, while international travel restrictions for people coming to Scotland also ended.

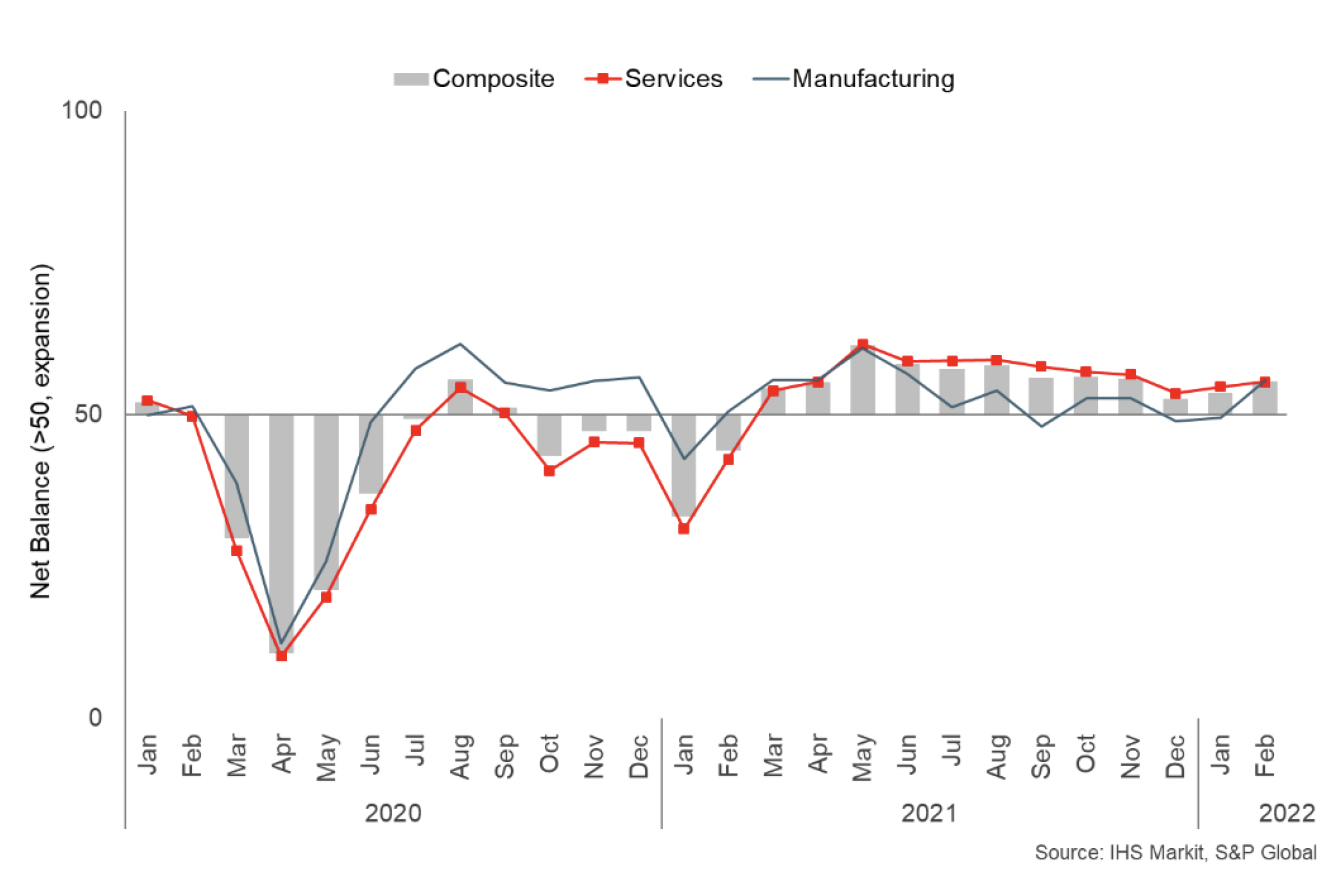

- The Purchasing Managers Index (PMI) business survey signalled a strong pick-up in growth in February (55.5, up from 53.7 in January), with the momentum returning back towards similar levels of that in November 2021 prior to the Omicron wave.[2]

- The pick-up in activity was supported by growth across the services and manufacturing sectors, with the manufacturing indicator returning to growth for the first time since November 2021. Panellists cited stronger demand as a result of the ending of restrictions as a driver of growth while the rate of increase in new business/orders accelerated to a three-month high.

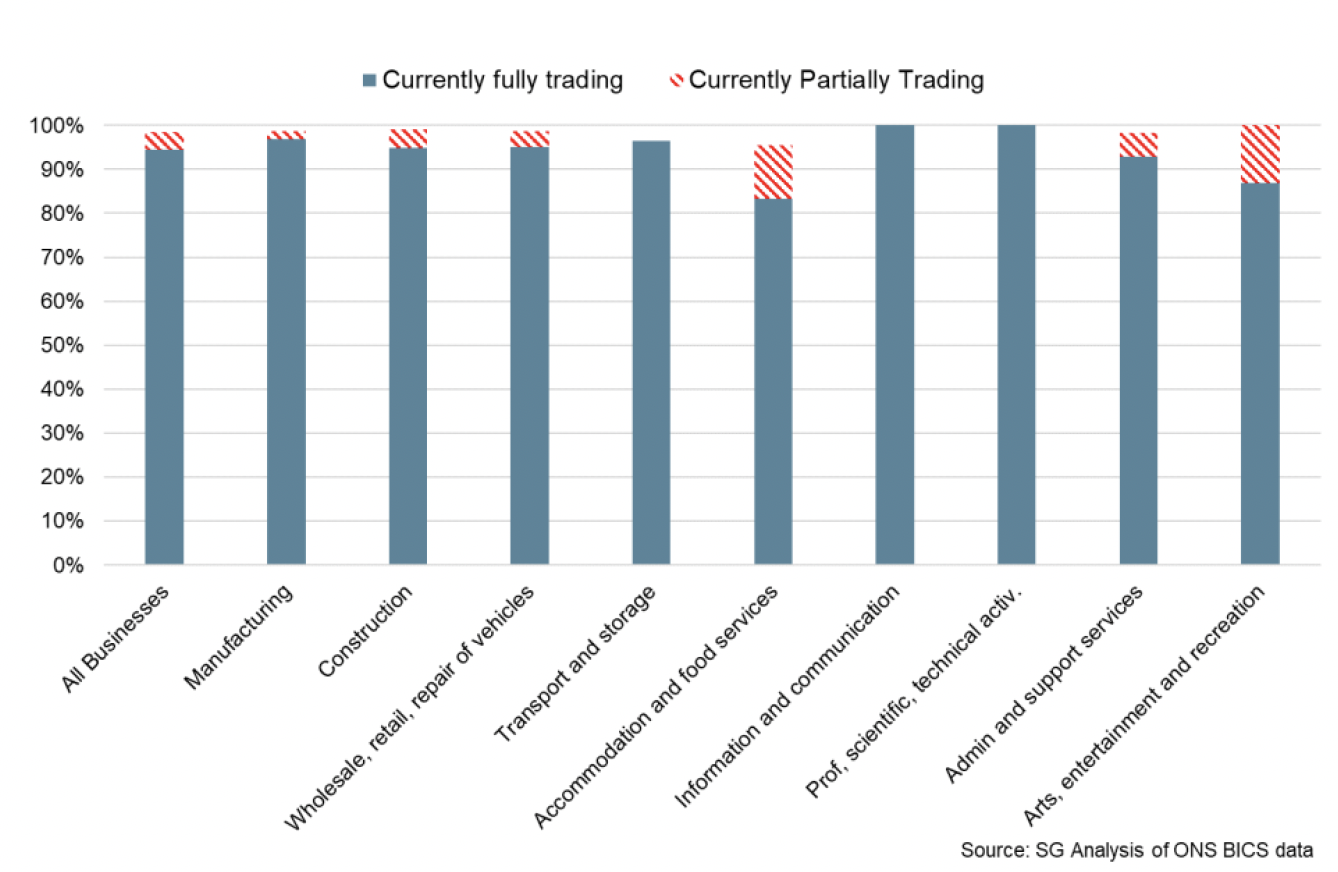

- Building on this, the trading capacity of sectors, particularly those most directly impacted by the Omicron restrictions (hospitality and leisure) have continued to strengthen. At the start of March 83% in Accommodation and Food and 87% in Arts, Entertainments and Recreation reported as fully trading (rather than partially), up from 63% and 57% respectively during January.[3]

- These remain below the average for all businesses (95%), continuing to reflect the different pace in recovery across sectors, however the gap has naturally closed further as restrictions have eased.

- Most recently, flash UK PMI data for March indicated further robust UK private sector growth during the month, though at a slightly softer pace than in February (59.7, down from 59.9 in February) as the economy continued to rebound from the easing of restrictions.[4]

Business turnover and input costs

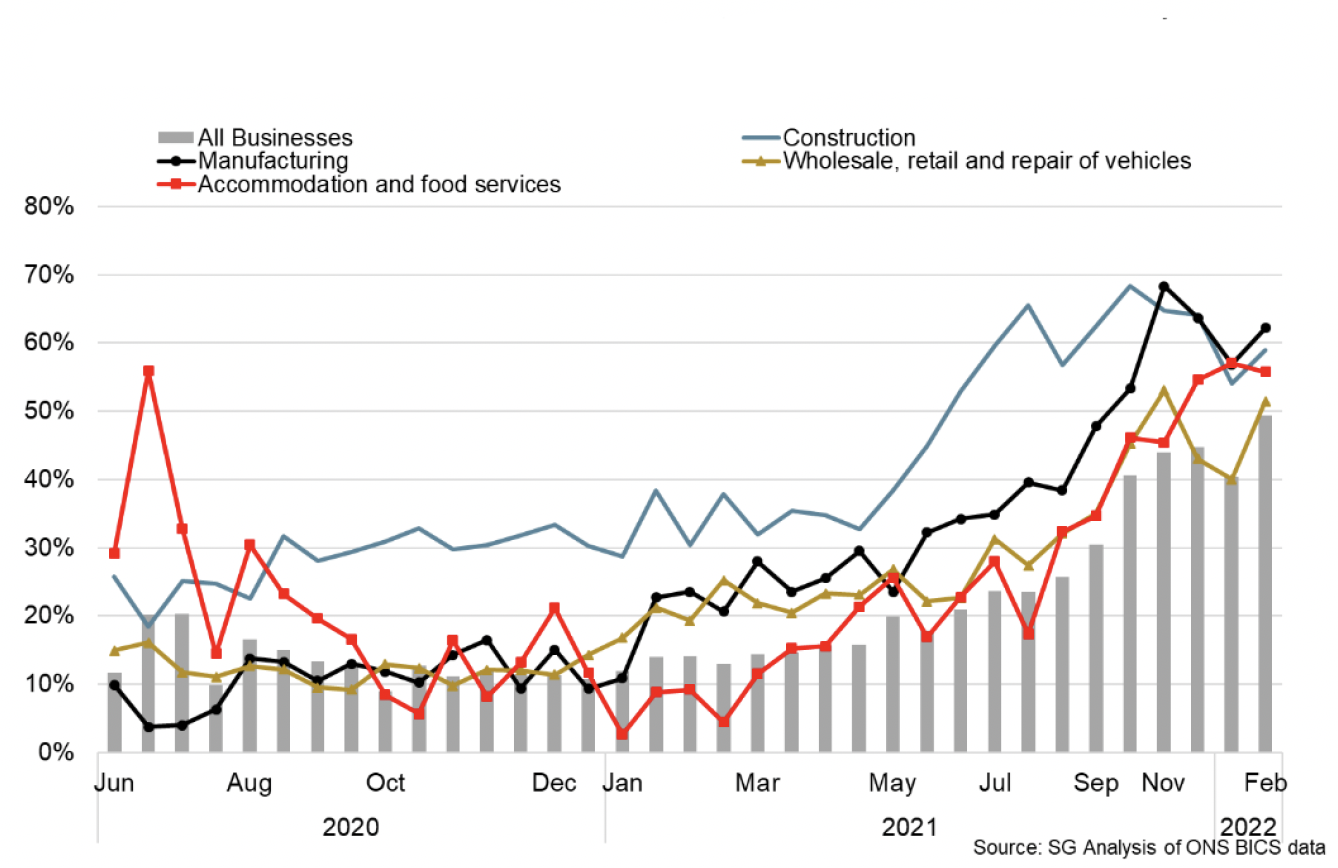

- Improved businesses activity in response to the loosening of restrictions across February and March has also been reflected in business turnover indicators.

- At the beginning of March, the proportion of all businesses reporting a decrease in turnover fell to 24.8%, its joint lowest rate in the time series and, down from around 30% at the beginning of 2022. Similarly the proportion of all firms reporting that turnover had increased improved to 13%, up from around 8%, while over 50% reported that turnover had not been affected.[5]

- As has been the general trend over the course of the pandemic, lower than normal turnover continued to be most widespread in the accommodation and food services sector, and picked-up in March to 52%. However, this is down from 59% at the beginning of 2022 and continues to be notably lower than earlier in the pandemic.

- However, input cost pressures for businesses continued to intensify in February with 49% of all businesses reporting that prices increased more than normal, its highest rate in the time series and up from 40% in January. Increased prices remained most widespread in manufacturing (62%), construction (59%) and accommodation and food services (56%).[6]

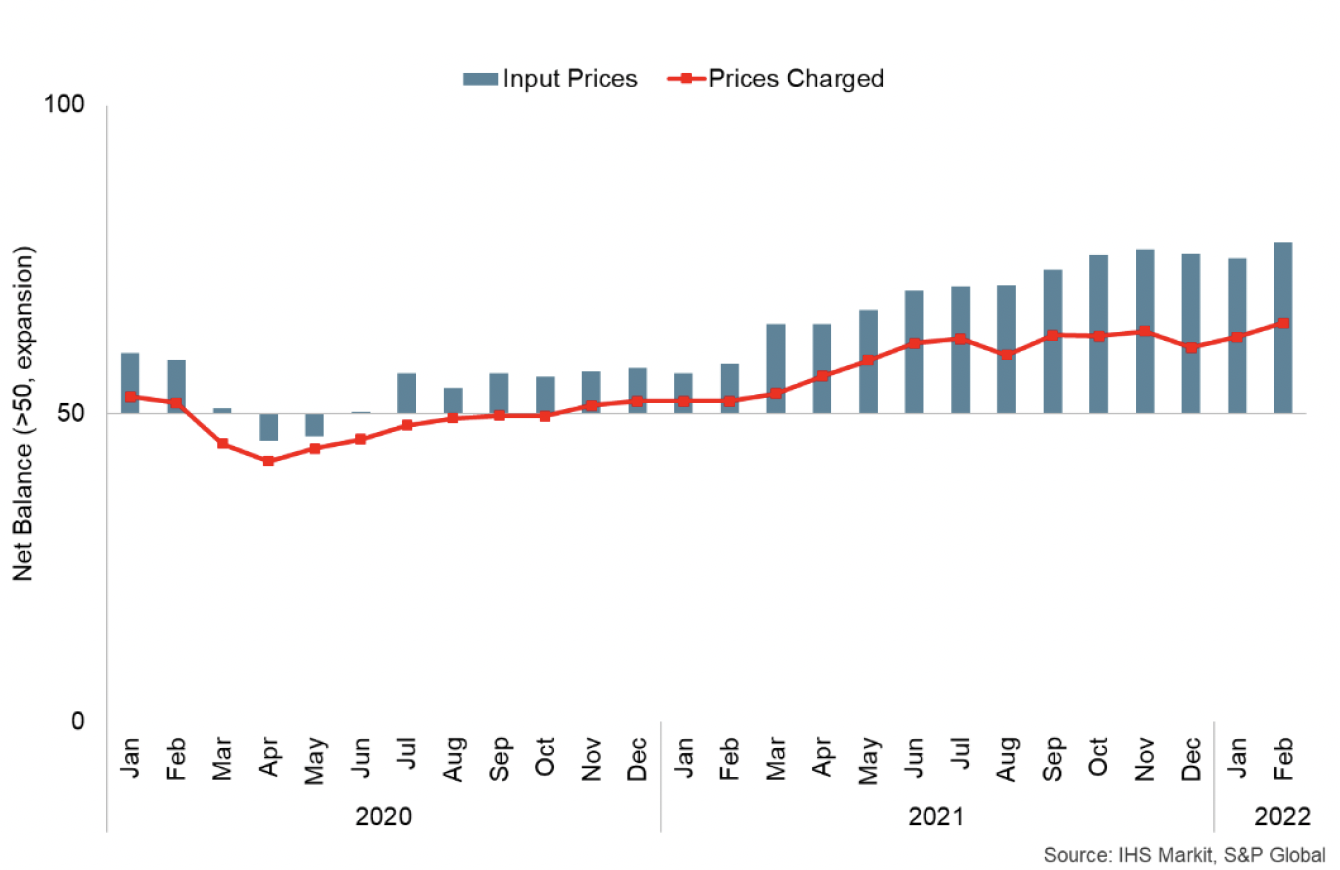

- Scottish PMI data also showed the indicator for input cost inflation continued to rise in February, to its highest level in the time series. A range of factors including higher fuel, energy, material and wage costs were the primary drivers of cost inflation. As a result, firms continued to pass higher costs through to customers, with prices charged also increasing at the sharpest rate in the series.[7]

- The latest flash UK PMI for March signalled that alongside ongoing concerns around rising inflationary pressures, the situation in Ukraine also started to weigh on the outlook for businesses, with business optimism falling to its lowest level since October 2020.[8]

- Business Insights and Conditions Survey data show supply chain bottlenecks continued to present significant challenges going into March 2022, though slightly less so than around the turn of the year. 26% of all applicable businesses reported that their business had experienced global supply chain disruption over the previous month (down from 37% a month earlier), most notably in the manufacturing (48%), construction (36%), transport and storage (36%) and wholesale, retail and repair of vehicles (31%) sectors.[9]

Channels of economic impact from the situation in Ukraine

- The situation in Ukraine and the sanctions imposed on Russia are impacting on the global and Scottish economy through a range of channels. The overall impacts currently remain highly uncertain and will depend on how the severity and duration of the situation evolves.

- The direct economic impacts of the situation in Ukraine on Scottish output are expected to be relatively small. Less than 1% of Scotland's international exports are destined for Russia.[10] However, indirect economic impacts arising for businesses and households from intensifying inflationary pressures are expected to be more prominent.

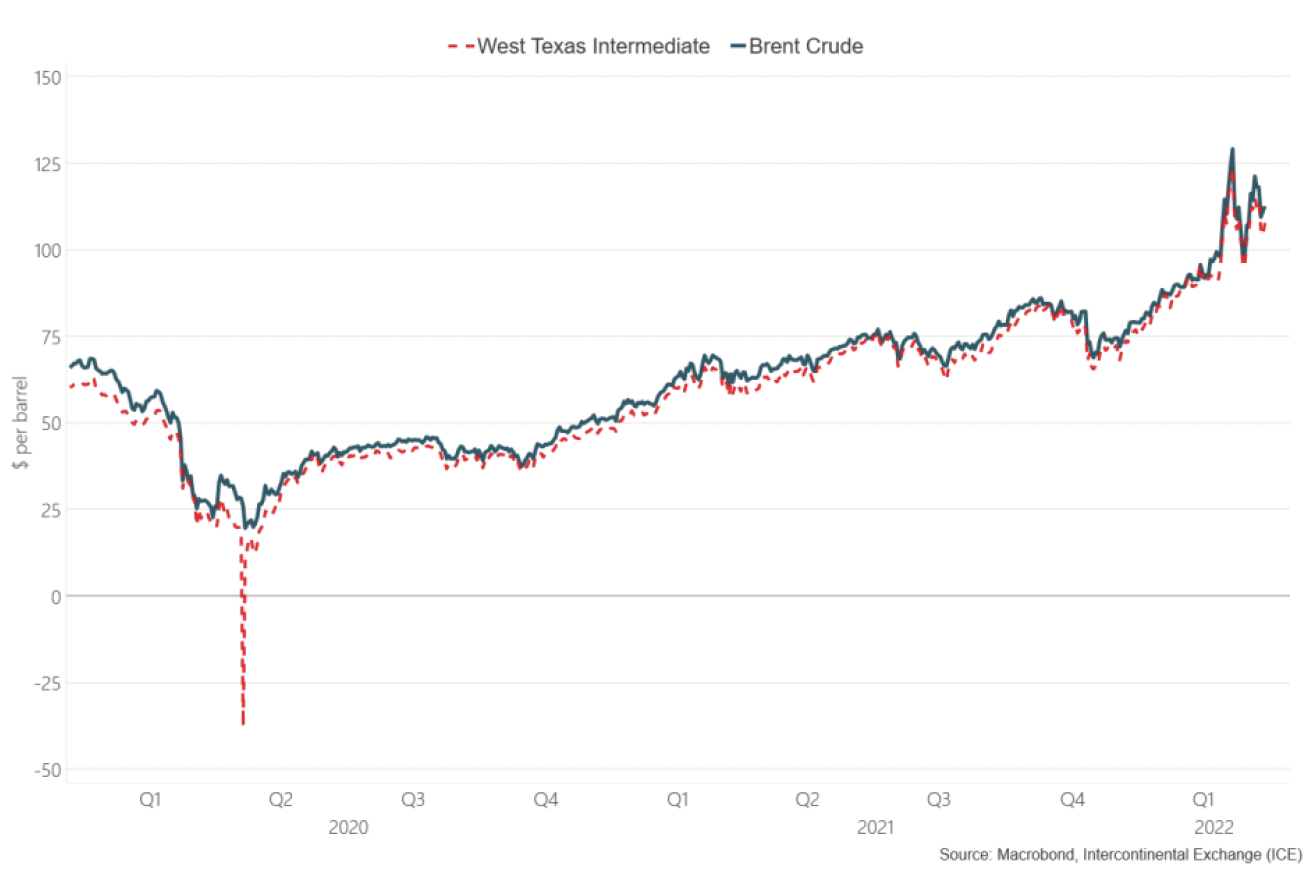

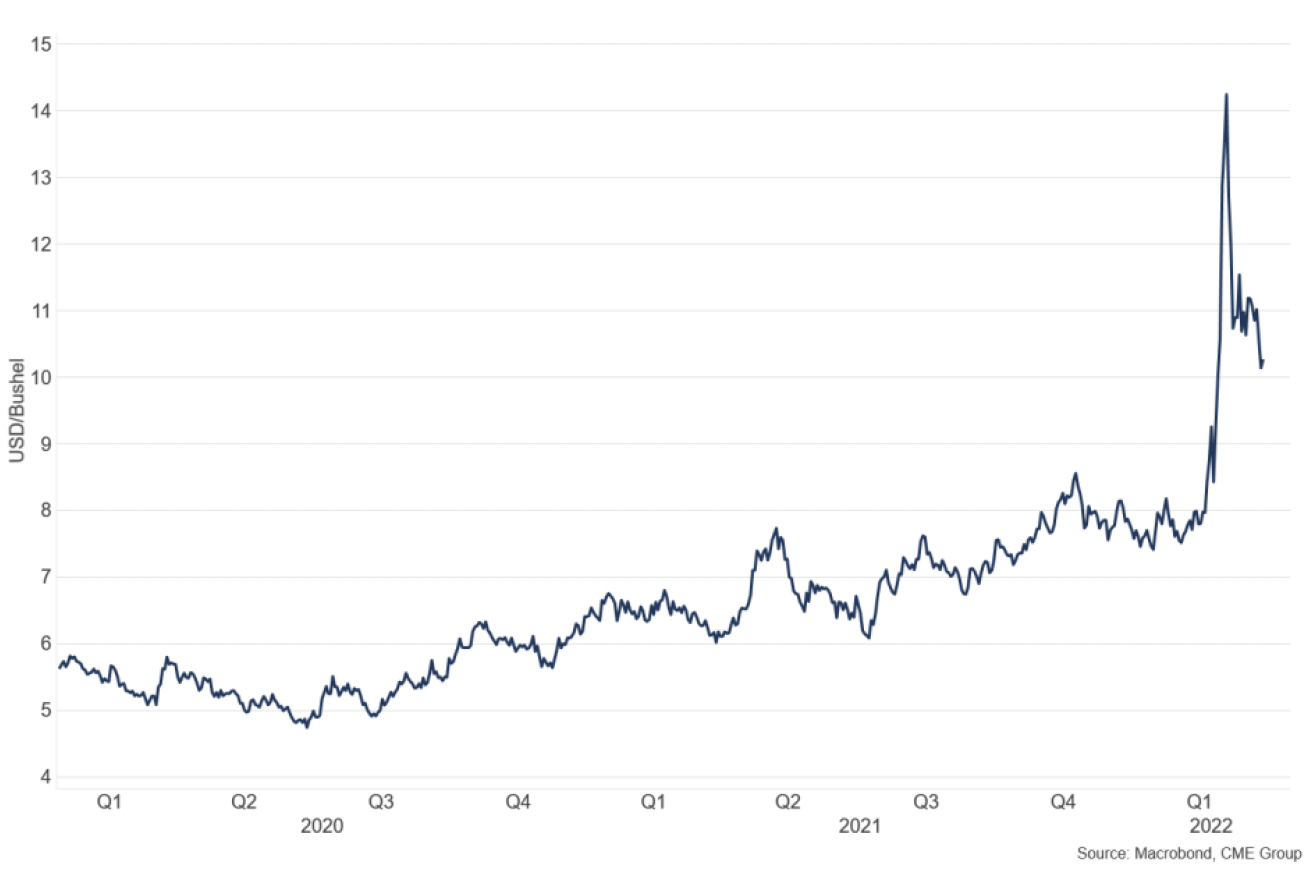

- Russia and Ukraine are key producers of a range of global commodities such as oil and gas, grains and metals. For example, they together account for about 30% of global exports of wheat and around 11% of oil.[11]

- Since the start of the invasion, prices across a range of global commodities have increased sharply, reflecting concerns regarding future availability of supply and uncertainty over the scale of the economic implications. While some prices have since moderated, they remain significantly elevated. For example, since the start of the invasion, the Brent crude oil price remains 15% higher and wheat prices are 17% higher.[12]

- As these price rises feed through to consumers on the back of existing inflationary pressures as the global economy stabilised from the pandemic, this is expected to weigh significantly on real household incomes and consumption over the course of the year and ultimately dampen economic growth.

- In March, the Office for Budget Responsibility (OBR) revised down their UK GDP growth forecast to 3.8% in 2022 (revised down 2.2 percentage points from October) and 1.8% in 2023.

- The downward revision in the near term reflected higher inflation weighing on real incomes and consumption with inflation forecast to rise to almost 9% in Q4 2022, mainly reflecting higher global energy prices.[13]

Contact

Email: OCEABusiness@gov.scot