Publication - Research and analysis

Monthly economic brief: June 2023

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Consumption

Consumer sentiment continues to strengthen however remains negative overall.

Consumer sentiment

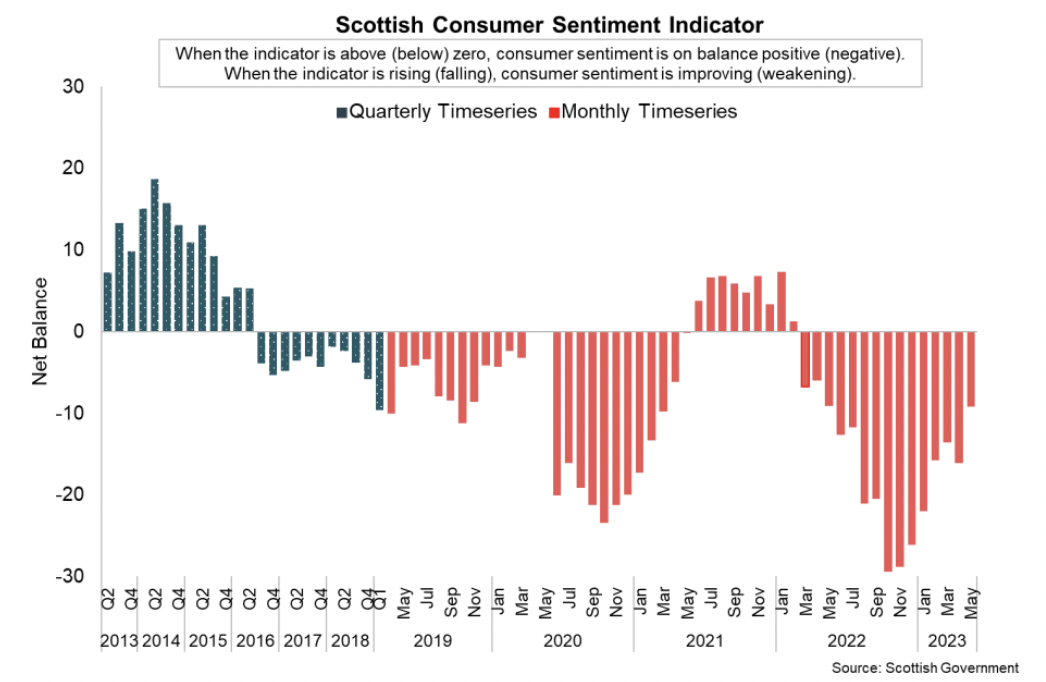

- Consumer sentiment indicators continue to highlight the pressures that households and consumers face from high inflation and the rapid increase in the cost of living. These challenges intensified over 2022 which was reflected in a sharp drop off in the Scottish Consumer Sentiment Indicator. However sentiment has strengthened significantly in recent months albeit remaining negative overall. [18]

- In May, the Scottish Consumer Sentiment Indicator stood at -9.2; an increase of 6.8 points from April. This is a strong increase over the month, with the composite indicator now 20.2 points above the series low of -29.4 in October and at its highest rate since May 2020.

- The recent increase has been driven by strengtheing sentiment regarding the economy, personal household finances and attitute to spending, however households remain more optmistic about the outlook for the coming year than their current circumstances.

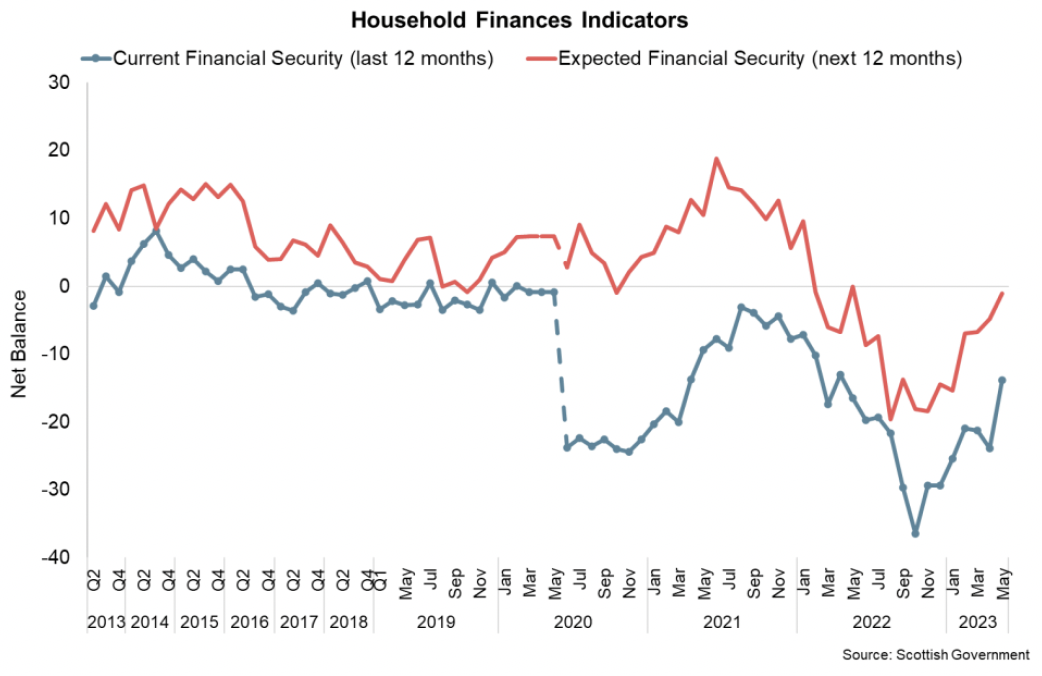

- On the economy, respondents on balance consider current economic circumstances to be worse than last year (-16.3, up from -17.4 in April) however expect the economy to improve over the coming year relative to the current situation (14.9, up from 6.6 in April).

- In terms of households' personal finances, respondents on balance continued to report that they are less secure than 12 months ago (-13.9, up from -23.8 in April) and looking ahead, respondents also continue to expect their household financial security to weaken, though to a much lesser extent (-1.1, up from -4.8 in April).

- Overall, households remain notably less optimistic about the outlook for their household financial security than they do for broader performance of the economy and is reflected in ongoing concerns about spending money.

- In May, the spending indicator increased 11.1 points to -29.7, up from -40.8 in April indicating that households continue to be uneasy about spending money, but to a slightly lesser degree than in recent months.

- The general strengthening in consumer sentiment in Scotland is consistent with findings from the GfK Consumer Confidence Index at a UK level which fell to its lowest point in September 2022 before picking up in recent months.[19]

- Despite recent strengthening, similar to the Scottish indicator, the GfK index remains in negative territory and reflects the ongoing challenges facing households from high inflation and higher interest rates. Furthermore, at a GB level, the ONS Public Opinions and Social Trends survey for June showed that 62% of respondents reported an increase in the cost of living compared to the previous month, though this had decreased from April when it was 76%.[20]

- The reasons given for the increase in the cost of living over the past month included (i) price of food shopping (96%); (ii) gas or electric bills (62%); (iii) price of fuel (34%), and rent or mortgage costs (26%).

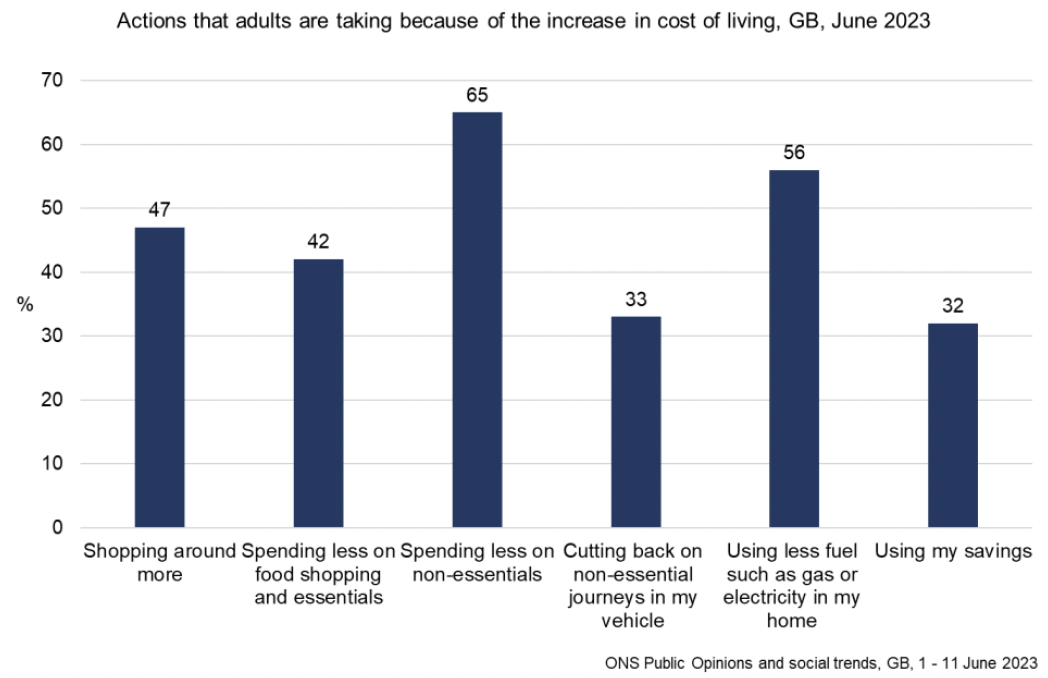

- Data from the start of June show that the most common actions people were taking in response to the increased cost of living were spending less on non-essentials (65%) and using less fuel such as gas or electricity in their home (56%), while 47% reported shopping around more and 42% reported spending less on food shopping and essentials.

Retail Sales

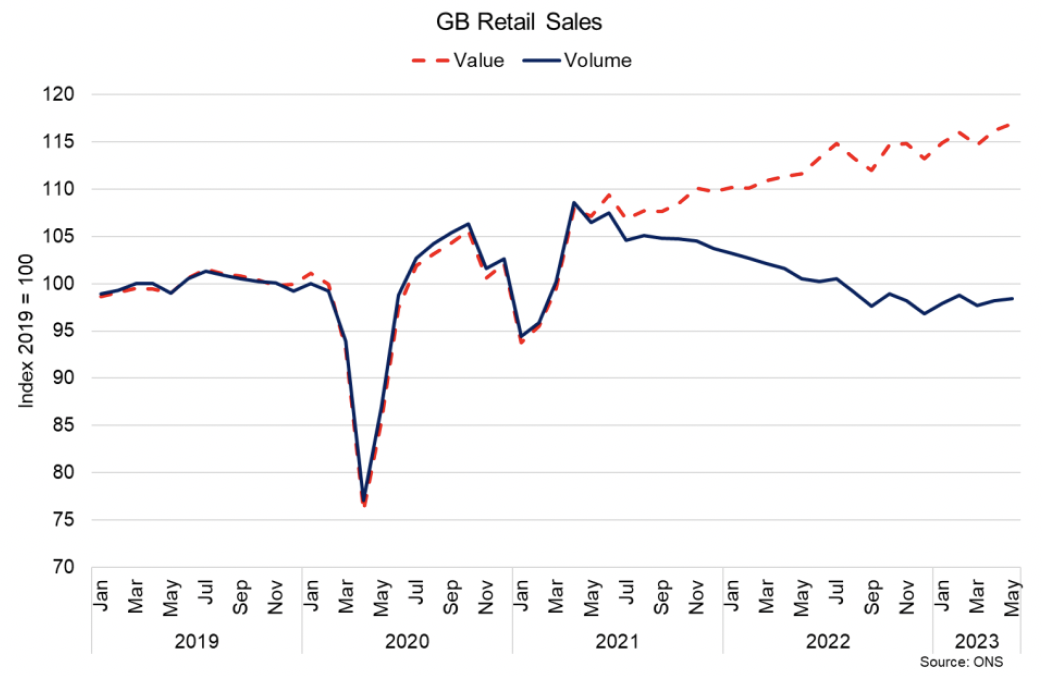

- GB level retail sales continued to show a slight improvement from the start of the year with sales volumes growing by 0.3% in May and 0.3% in the three months to May. Sales volumes remained 2.1% down over the year while sales values rose 4.8%, reflecting the impact of inflation.[21]

- Food stores sales volumes fell 0.5% in May and 1.1% over the year. Some retailers indicated that higher food prices may explain part of the fall with the food sales values rising 12.7% due to the impact of inflation.

- Non-food store sales volumes fell by 0.2% in May and 2.1% over the year, however increased 4.2% in value terms. This increase in value terms was not to the same extent as in food stores reflecting the particularly high rates of food price inflation. Household goods stores provided the largest upward contribution to non-food store sales volumes, increasing 1.5% with strong sales in DIY stores reportedly due to good weather.

Household savings and lending

- The rise in cost of living and higher interest rates are progressively feeding through to household decisions on spending, saving and borrowing.

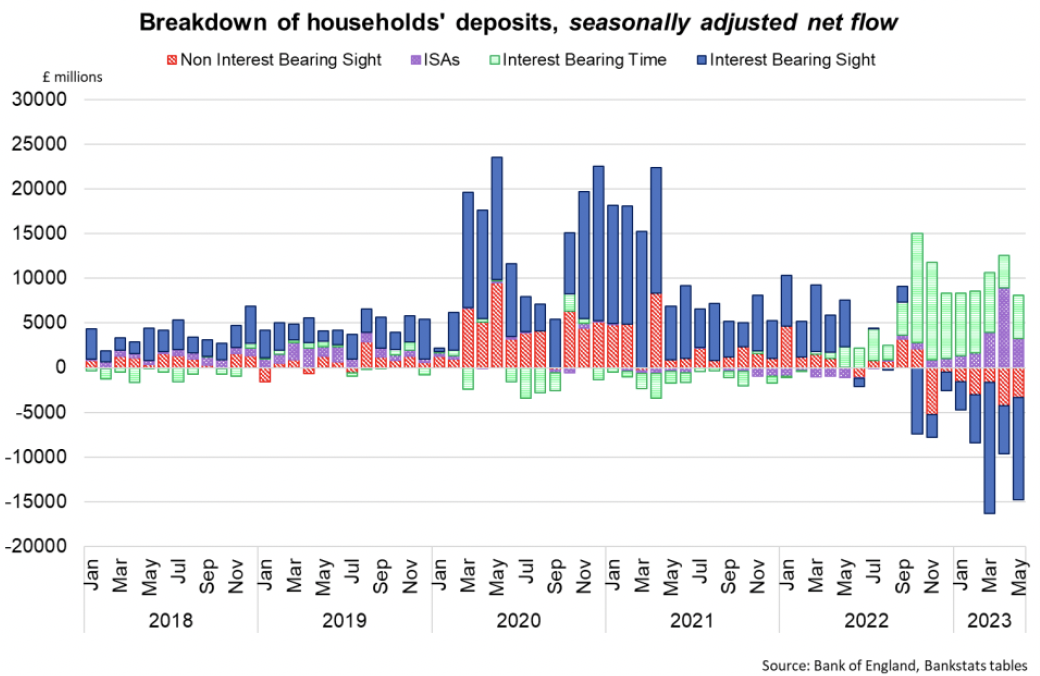

- At an aggregate level, Bank of England Money and Credit data shows households on net withdrew £4.6 billion from banks and building societies in May, the highest level of household withdrawals since records began in 1997.[22] Within this, there were further net withdrawals from interest and non-interest-bearing sight deposits of £14.7 billion, partly offset by net flows of £8.2 billion into interest-bearing time deposits and ISAs.[23]

- This indicates households are needing to use their financial resources (net outflows from banks) while are also choosing to deposit and hold money in longer term savings accounts which will tend to offer higher interest rates. The effective interest rate paid on individuals' new time deposits with banks and building societies rose by 12 basis points, to 3.95% in May, while the effective rate on stock sight deposits dropped by 8 basis points to 1.33%.

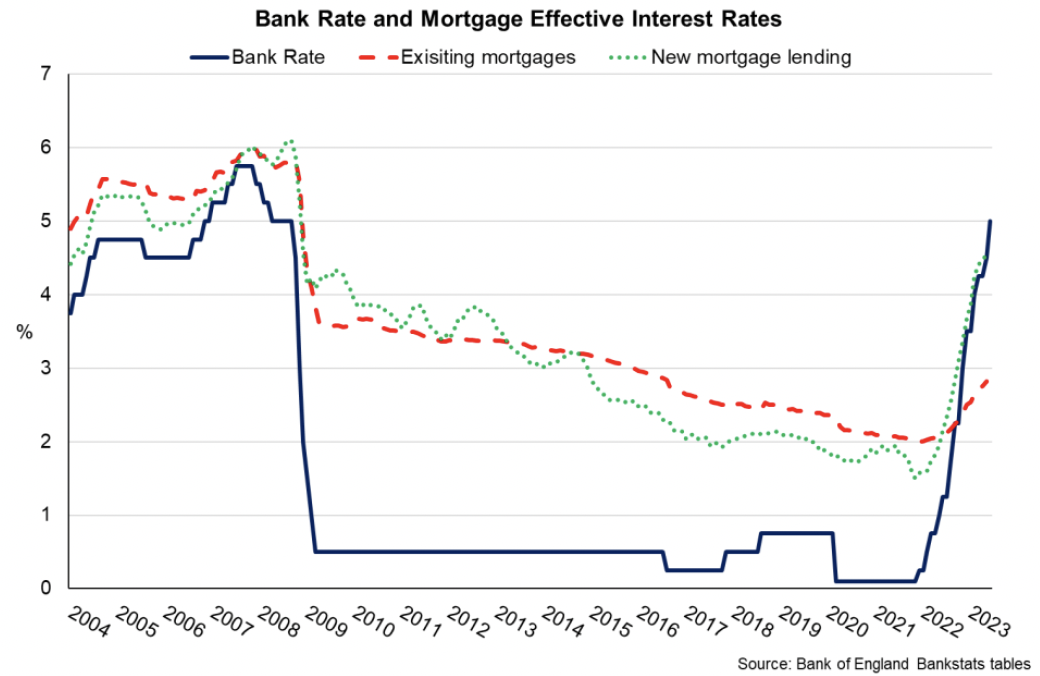

- A key channel through which higher interest rates impacts households is through mortgage interest payments. Around a third of households in the UK have a mortgage, with around 85% on fixed rate mortgages. While mortgage rates have been increasing as the Bank Rate has risen, the greater share of fixed-rate mortgages means that it will take time for the full impact of the increase in Bank Rate to be felt at an aggregate level. The Resolution Foundation estimate that 44% of households with a mortgage are yet to be impacted as they are yet to see their fixed-rate deals expire.[24]

- This is reflected in the effective interest rate on the stock of outstanding mortgages which rose to 2.8% in May while the rate on new mortgages rose to 4.6%.

- With around 85% of all mortgages on a fixed rate, as these fixed rate mortgages renew over the next 3 years, these households will face significantly higher mortgage costs. Furthermore, interest rates could rise further with markets currently expecting the Bank Rate to average 5.5% over the next 3-years.

- The Resolution Foundation estimate that, based on the latest market expectations for Bank Rate, the average rate on a two-year fixed-rate mortgage is likely to reach 6.25% this year based on current market pricing and won't fall back below 4.5% until the end of 2027.

- At a UK level, the Resolution Foundation estimate that by the end of 2026, almost all British households with a mortgage will have moved on to a higher rate and are set to have annual mortgage bills that are £2,000 higher on average compared to December 2021.

Contact

Email: OCEABusiness@gov.scot