Publication - Research and analysis

Monthly economic brief: June 2023

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Inflation

Headline inflation remained unchanged in May while core inflation continued to rise.

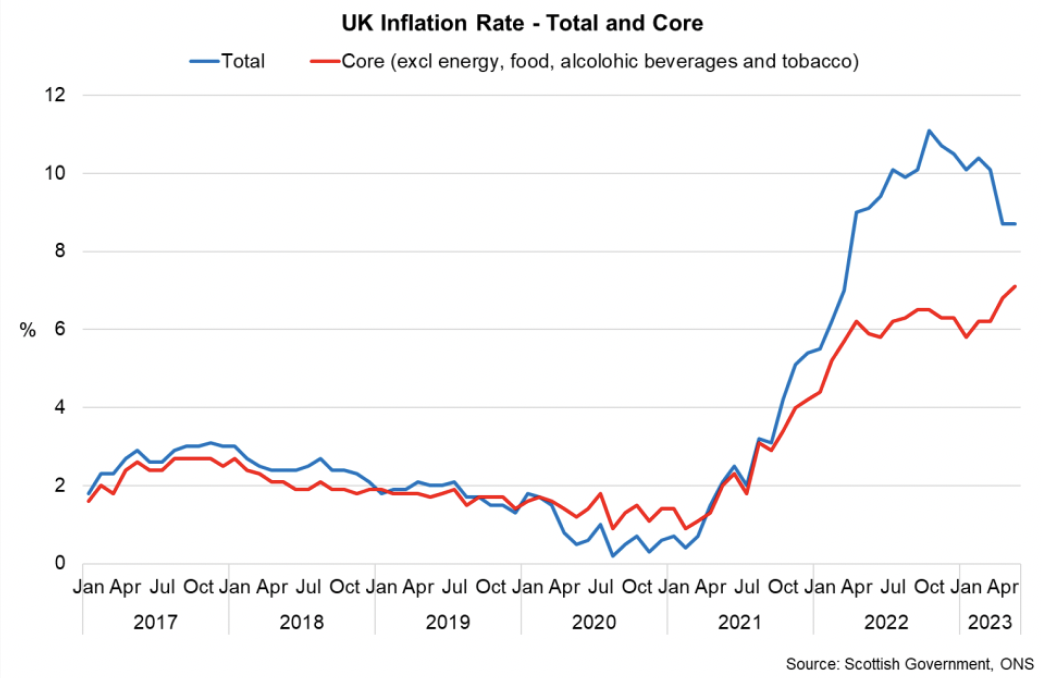

- Following the notable 1.4 percentage point drop in the inflation rate in April as the sharp rise in energy prices in 2022 started to fall out of the annual comparison, UK inflation remained unchanged at 8.7% May; slightly higher than forecast and market expectations. [2]

- Services prices in particular rose in May with the annual inflation rate rising 0.5 points to 7.4%, driven by increasing inflation rates for recreational and cultural services (4.5%) and restaurants and hotels (10.3%), while goods prices inflation eased for a third consecutive month to 9.7%. Food and non-alcoholic drink price inflation eased slightly over the month from 19% to 18.3% however remained elevated overall.

- Core inflation, which excludes food, energy, alcohol and tobacco, rose 0.3 percentage points in May to 7.1%, its highest rate since March 1992. With much of the inflationary pressures to date reflecting the energy and commodity price shock due to the war in Ukraine, the further increase in the core inflation rate reflects the subsequent breadth and persistence of current inflationary pressures.

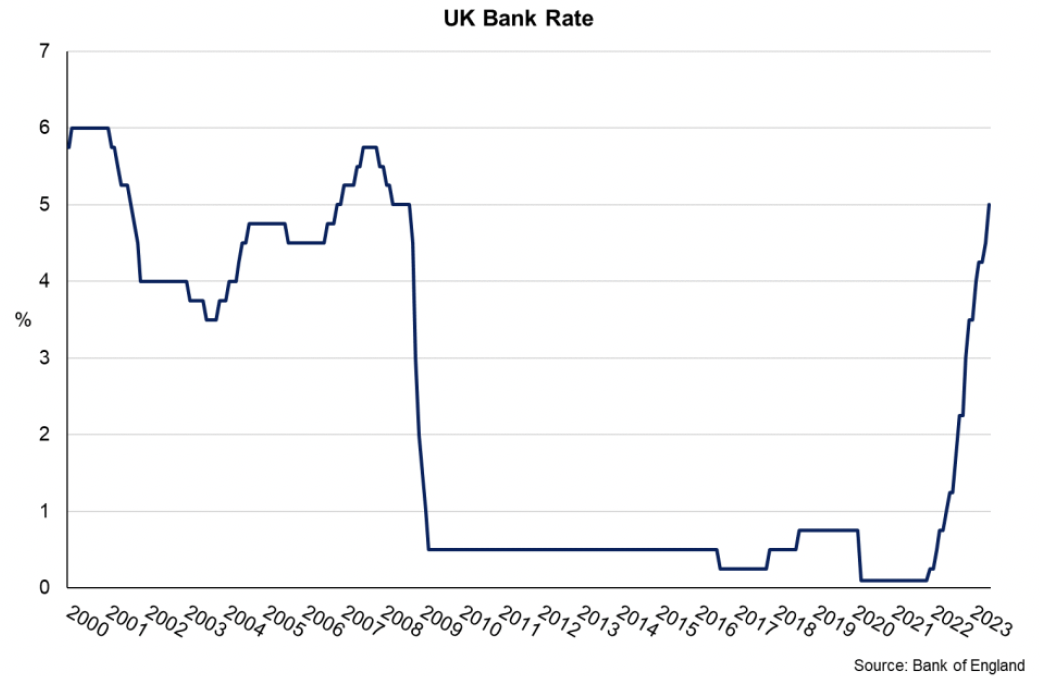

- In June, due to inflation falling more slowly than forecast and stronger than expected wage growth, the Bank of England's Monetary Policy Committee (MPC) raised the Bank Rate by 0.5 percentage points from 4.5% to 5% to further reduce inflationary pressures and expectations. It was the thirteenth successive rate rise since December 2021 when the Bank Rate was 0.1% and is at its highest rate since 2008. Markets currently expect interest rates to rise further and average 5.5% over the next 3-years.[3]

- The Bank of England's latest forecast from May is for inflation to fall to 5.1% by the end of 2023. The recent elevation of food price of inflation alongside the persistence of core inflationary pressures presents a risk that inflation will fall more slowly than this.[4]

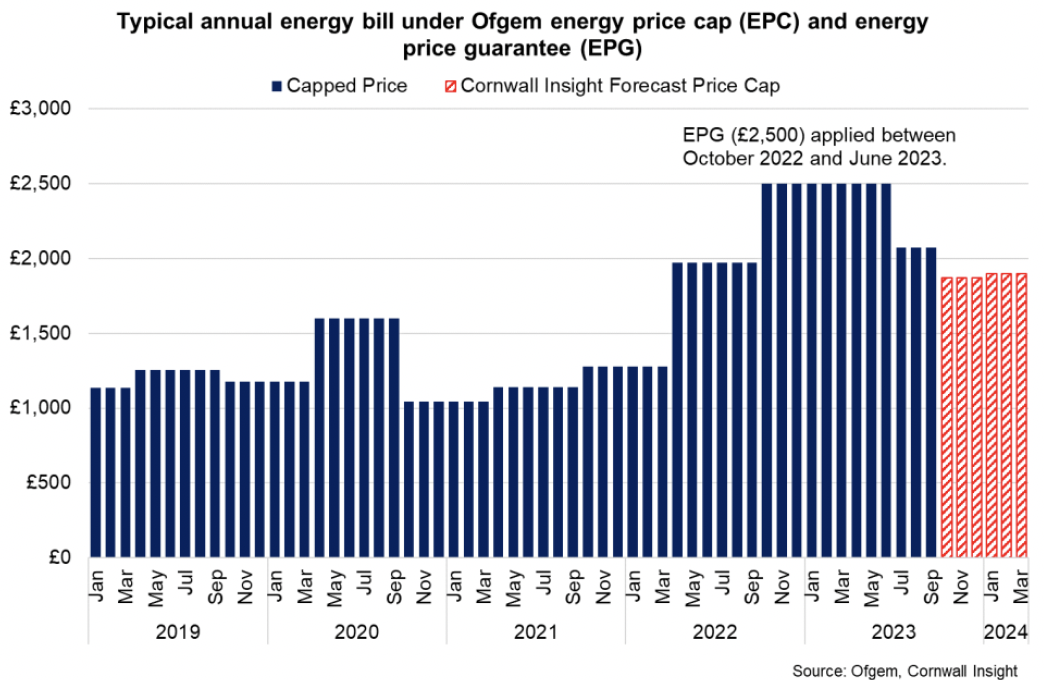

- Household energy prices are expected to continue falling over the remainder of the year, placing downward pressure on the overall inflation rate. Due to the fall in wholesale energy prices over recent months, at the start July, the new energy price cap for the third quarter is applied meaning that the typical annual energy bill will be £2,074. This represents a 17% fall from the Energy Price Guarantee of £2,500 which has been in place since October 2022. However, the capped price remains 5.2% higher than a year ago and double the capped price in January 2021, reflecting the ongoing pressure that energy prices will continue to have on household finances.[5]

- Looking ahead, Cornwall Insight forecast that the Energy Price Cap will fall further in the fourth quarter to £1,871 (-9.8%) before picking up slightly at the start of the new year.[6]

Contact

Email: OCEABusiness@gov.scot