Publication - Research and analysis

Monthly economic brief: February 2022

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business turnover and input costs

- The changes in business activity in response to increased uncertainty and the tighter guidance and restrictions over December and January has also been reflected in business turnover indicators.

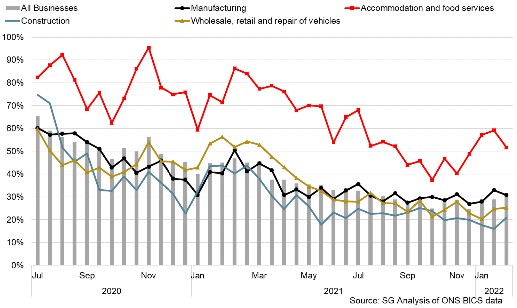

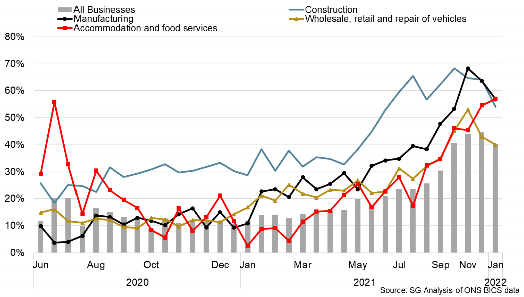

- At an aggregate level, the proportion of businesses reporting a decrease in turnover remained broadly stable in the second half of 2021, however edged back up to 30% in January and into the start of February (up from around 27% in November). Similarly the proportion of firms reporting that turnover has increased fell to 8% (down from 15% in November/December) while the proportion of firms reporting that turnover has not been affected continued its upward trend to 51%.[5]

- Lower than normal turnover continued to be most widespread in the accommodation and food services sector. The proportion reporting lower than normal turnover picked up moderately in December and January to 59% (up from around 45% in November), however eased back to 52% going into February and remains notably lower than earlier in the pandemic.

- Notable shares of most other sectors continued to report that turnover had not been affected, while 12% of businesses in transport and storage, wholesale, retail, repair of vehicles and administration and support services reported that turnover had increased, emphasising the level of variability of demand within sectors.

- In addition to the uncertainty generated by Omicron at the start of the year, businesses have continued to face existing headwinds from supply chain disruption and resource availability and energy prices, which have driven up input costs for businesses.

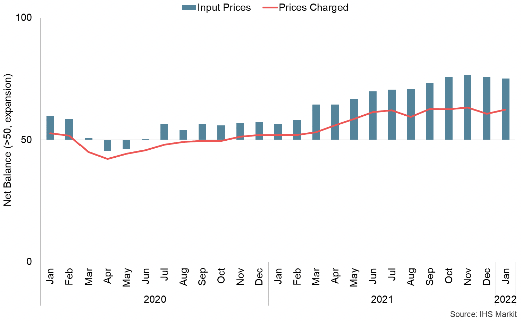

- Input cost pressures remained elevated in January with 40% of businesses reporting that prices increased more than normal, down from around 44% during November and December 2021, however remained most prominent in accommodation and food services (57%), manufacturing (57%) and construction (54%).[6]

- Scottish PMI data also showed the indicator for input cost inflation remained elevated in January, indicating that prices continued to rise, albeit at its slowest rate since September 2021. A range of factors including higher utility and food bills, material costs and shortages continued to be cited by the survey respondents as sources of inflationary pressures.[7]

- Business Insights and Conditions Survey data show supply chain bottlenecks continued to present significant challenges going into February 2022. 37% of all applicable businesses reported that their business had experienced global supply chain disruption over the previous month, most notably in the manufacturing (56%), construction (40%) and wholesale, retail and repair of vehicles (39%) sectors. Furthermore, 42% of exporters and 44% of importers reported facing changes in transportation costs while 19% of exporters and 18% of importers reported a lack of hauliers to transport goods or lack of logistics equipment.[8]

- PMI data indicated that firms continued to partly pass on higher costs through to customers, and at a faster rate than in December.

Contact

Email: OCEABusiness@gov.scot