Publication - Research and analysis

Monthly economic brief: December 2021

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Business Activity

More recent survey data indicated business activity remained broadly stable at the start of the fourth quarter, though there are signals that the pace of growth has moderated while supply chain pressures persist.

Business Output

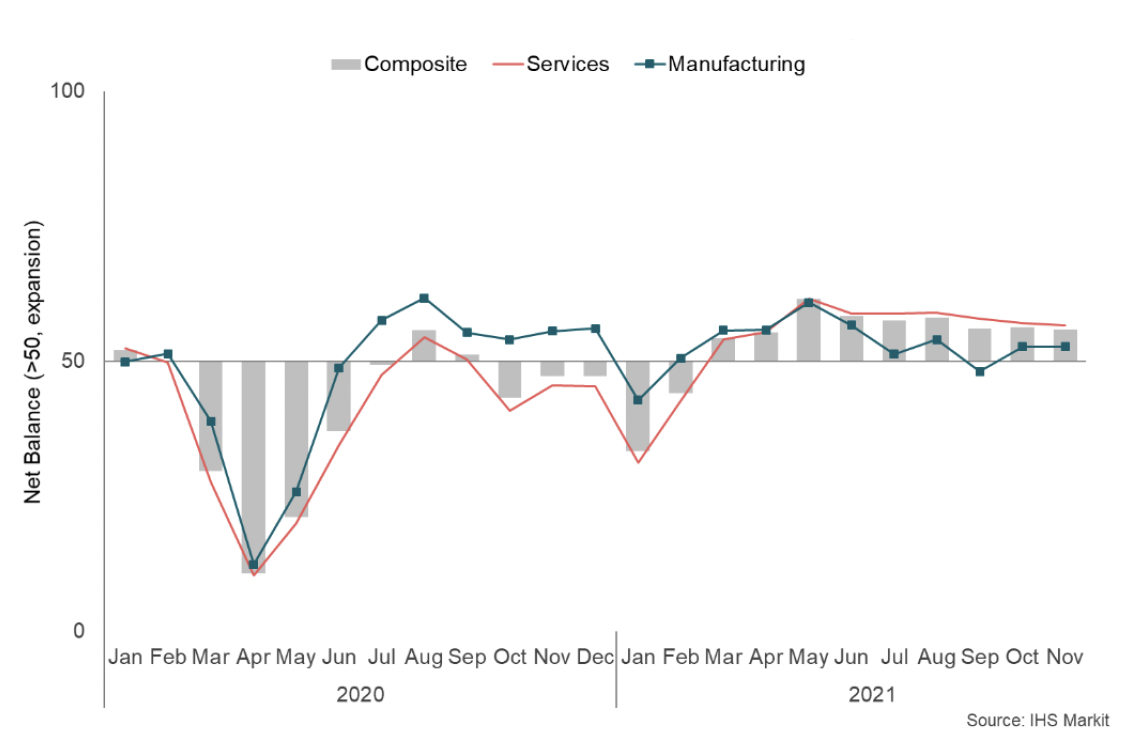

- The Purchasing Managers Index (PMI) business survey reported further robust growth in business activity growth in November (55.9), supported by continued growth in new business and with services sector activity continuing to outpace manufacturing during the month.[2]

- However, the overall pace of growth in activity has moderated over the month, signalling further stabilisation from stronger activity earlier in the year. Furthermore, latest flash UK PMI data for December indicated a further slowdown in activity, driven predominantly by the services sector, suggesting that Omicron has started to impact on spending on consumer services.

Trading status

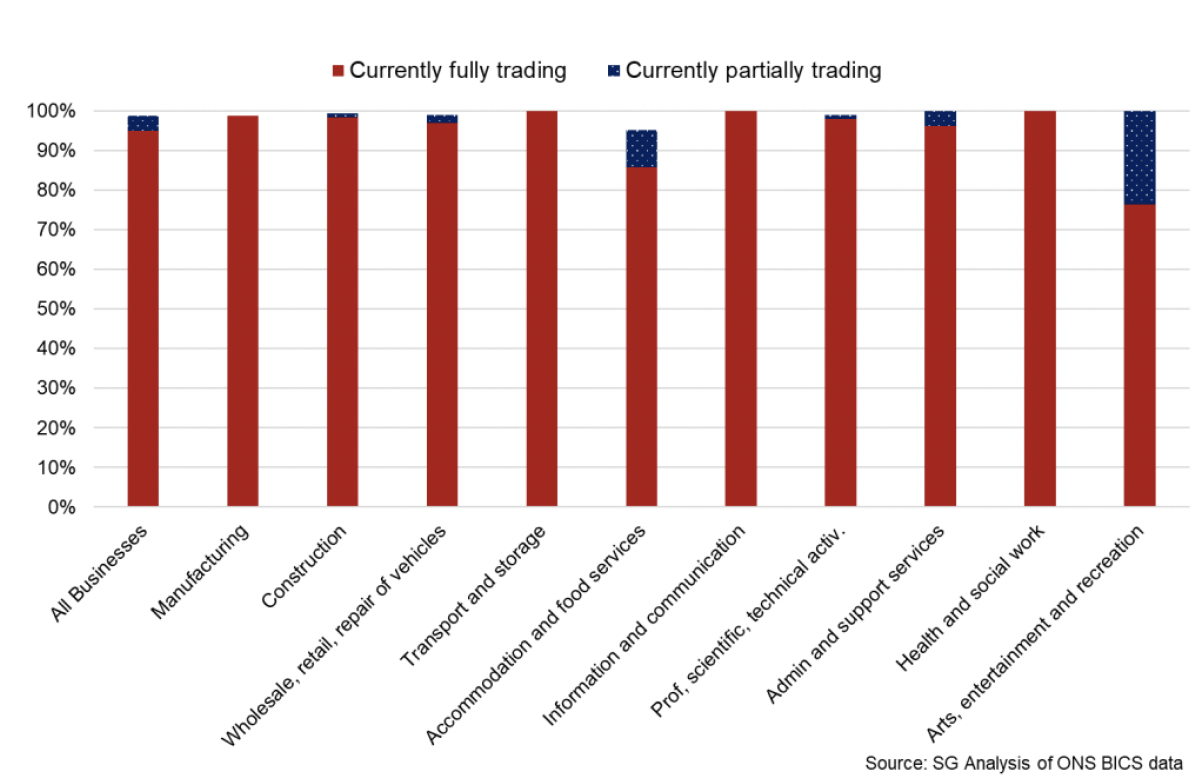

- Since August, around 99% of all businesses have been consistently trading following the move beyond level zero restrictions in Scotland (with some protective measures remaining in place) with latest data showing this continued in November.[3]

- Sector differences and the capacity at which businesses are trading remained a feature of this stage of the pandemic in November. For example, 95% of all businesses reported being fully trading (4% partially), however this was lowest in consumer facing sector such as arts, entertainment and recreation (76% fully trading and 24% partially) and accommodation and food services (86% fully trading and 9% partially).

Business turnover and input costs

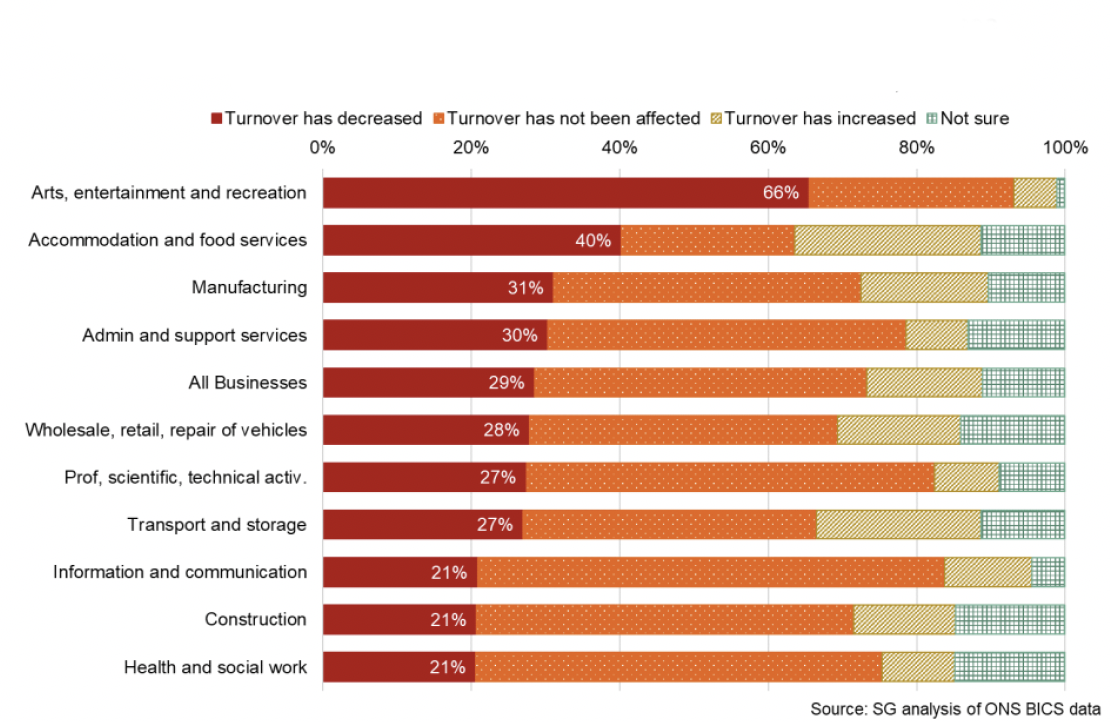

- The financial context of businesses also continues to vary across sectors. In terms of business turnover in November, 29% of all business reported having lower turnover than normal for the time of year, while 45% reported that turnover was not affected and 17% reported that it had increased.[4]

- Lower than normal turnover continues to be most widespread in the arts, entertainment and recreation services sector (66%) followed by the accommodation and food services sector (40%). However in the case of the latter, accommodation and food also had the highest share of firms reporting that turnover had increased (25%) alongside the transport and storage sector (22%), emphasising the level of variability of within sectors of customer demand.

- Overall, there has been some stabilisation in recent months, however turnover performance remains notably improved compared to March with a rise in the proportion of firms reporting an increase in turnover (from 6% to 16%) and a fall in the share reporting lower turnover (from around 45% to 29%). However, on the cost side, supply chain disruption, rising input costs inflation and employee shortages have emerged as key challenges and risks for many businesses reflecting imbalances following the sharp rebound in demand at this stage of the recovery.

- On the supply side, input cost pressures (e.g. raw materials and energy) have remained elevated in November, partly reflecting ongoing domestic and global supply challenges reflecting the imbalances which characterise this stage of the pandemic.

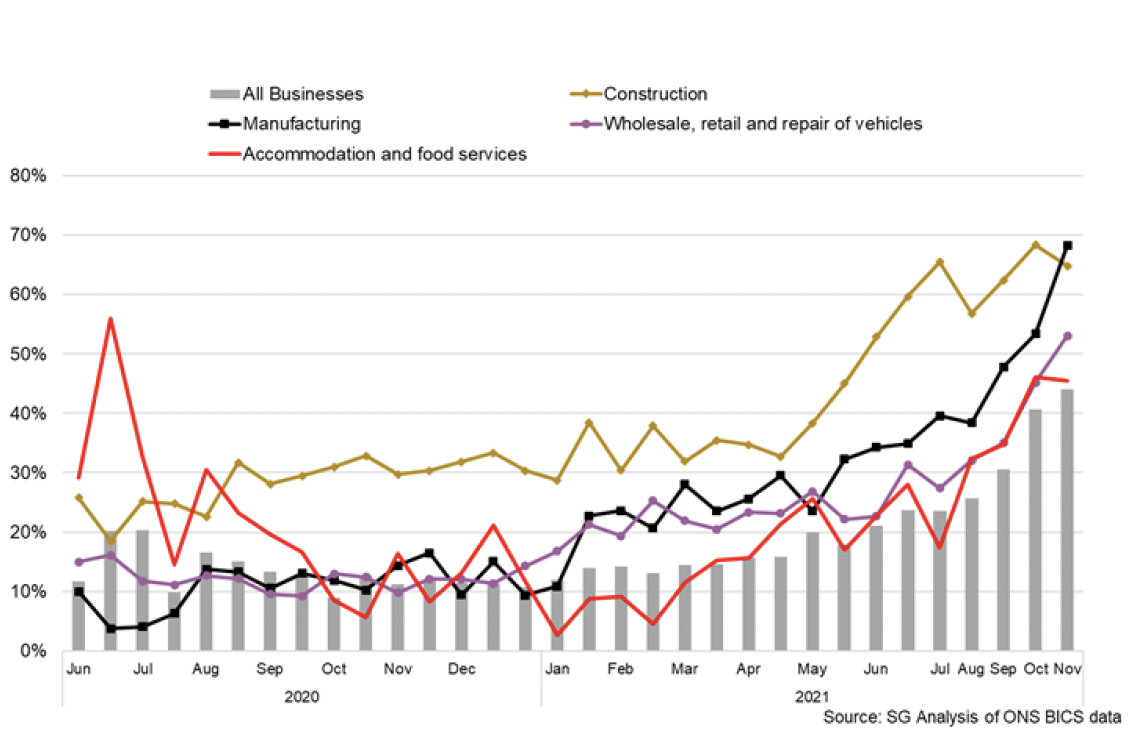

- Increased input costs have been evident across sectors. In November, the Business Insights and Conditions Survey (BICS) showed that 44% of businesses had seen prices increase more than normal, however this was most prominent in manufacturing (68%), construction (65%), arts entertainment and recreation (56%) and wholesale and retail (53%).[5]

- Scottish PMI data for November also showed the indicator for input cost inflation rose further to a series high (76.6), with respondents citing that this is due to issues around supply shortages, transport issues, the pandemic and EU-Exit. PMI data also showed that firms continued to partly pass on greater costs through to customers with the indicator for prices charged also rising to a series high (63.3).[6]

Trade

- International trade and supply chains have experienced significant challenges in 2021 arising from the pandemic and the transition to the new trade agreement between the UK and EU.

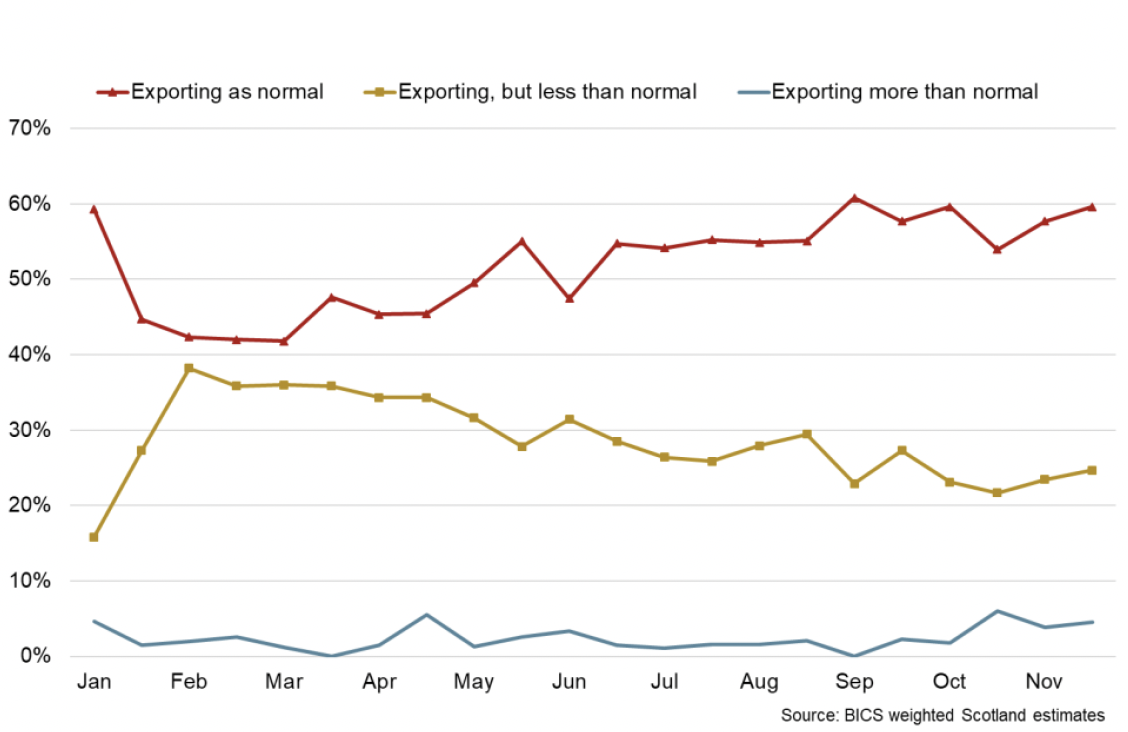

- BICS data for November indicates improvement in trade activity from the start of the year with 60% of Scottish businesses reporting to be exporting as normal for the time of year (up from 42% at the start of February) while 25% were exporting less than normal (down from 38% at the start of February).[7]

- However, supply chain bottlenecks continue to present significant challenges in November with 41% of exporters and 47% of importers reported facing changes in transportation costs while 18% of exporters and 25% of importers reported a lack of hauliers to transport goods or lack of logistics equipment. Furthermore, in November, 52% of exporters reported that the costs of exporting in the last month had increased compared to normal expectations for the time of year alongside 63% of importers.[8]

Contact

Email: OCEABusiness@gov.scot