Publication - Research and analysis

Monthly economic brief: April 2023

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Consumption

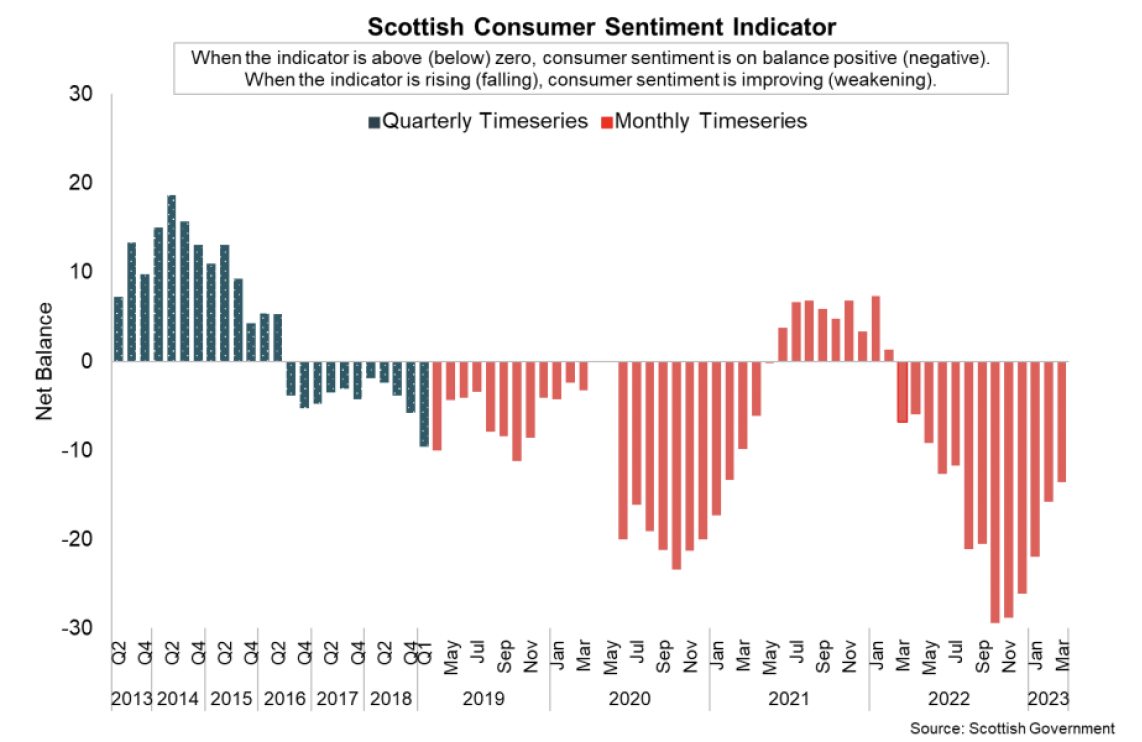

Consumer sentiment has strengthened but remains negative overall.

Consumer sentiment

- Consumer sentiment indicators continue to highlight the pressures that households and consumers face from high inflation and the rapid increase in the cost of living.

- These challenges intensified over 2022 which was reflected in a sharp drop off in the Scottish Consumer Sentiment Indicator, however latest data indicates that consumer sentiment has improved slightly over start of the year, albeit remaining significantly negative overall. [14]

- In March, the Scottish Consumer Sentiment Indicator stood at -13.6; a rise of 2.1 points from February and indicating that sentiment strengthened for a fifth consecutive month, having fallen to its series low of -29.4 in October.

- On the economy, respondents on balance consider current economic circumstances to be worse than last year (-18.7, up from -25 in February) however expect the economy to improve over the coming year relative to the current situation (15.3, up from 12.7 in February); its third consecutive month in positive territory.

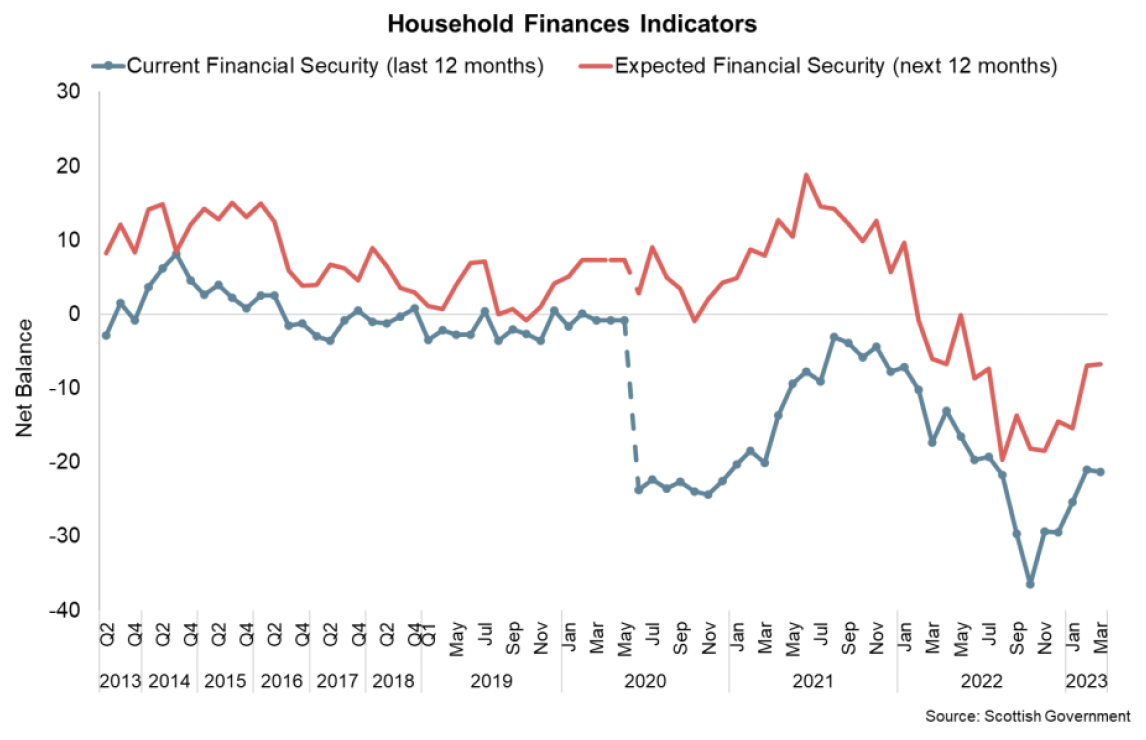

- In terms of households' personal finances, respondents on balance continued to report that they are less secure than 12 months ago (-21.3, slightly down from -21 in February). Furthermore, looking ahead, respondents continue to expect their household financial security to weaken over the coming year (-6.7, slightly up from -6.9 in February).

- Overall, households remain notably less optimistic about the outlook for their household financial security than they do for broader performance of the economy and is reflected in ongoing concerns about spending money.

- In March, the consumer sentiment spending indicator increased slightly to -36.5, up from -38.5 in February and its series low of -58.5 in October, indicating that households continue to be uneasy about spending money, but to a slightly lesser degree than towards the end of 2022.

- The general strengthening in consumer sentiment in Scotland is consistent with findings from the GfK Consumer Confidence Index at a UK level which fell to its lowest point in September 2022 before picking up in recent months. [15]

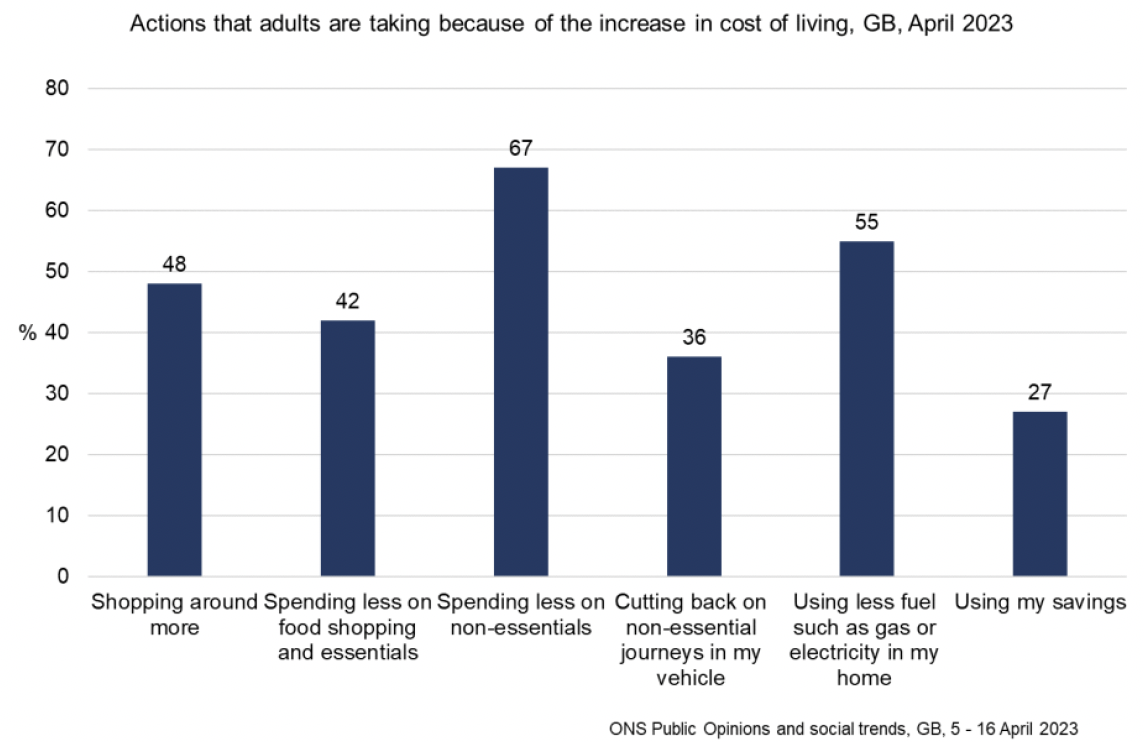

- Furthermore, at a GB level, the ONS Public Opinions and Social Trends survey for April showed that 93% of adults reported an increase in the cost of living compared with a year ago and 70% reported an increase compared to the previous month.[16] The reasons for the increase in the cost of living remain largely unchanged in recent months: (i) price of food shopping (96%); (ii) gas or electric bills (77%); (iii) price of fuel (42%).

- The most common actions reported were spending less on non-essentials (67%) and using less fuel such as gas or electricity in their home (55%), while 48% reported shopping around more and 42% reported spending less on food shopping and essentials.

Retail Sales

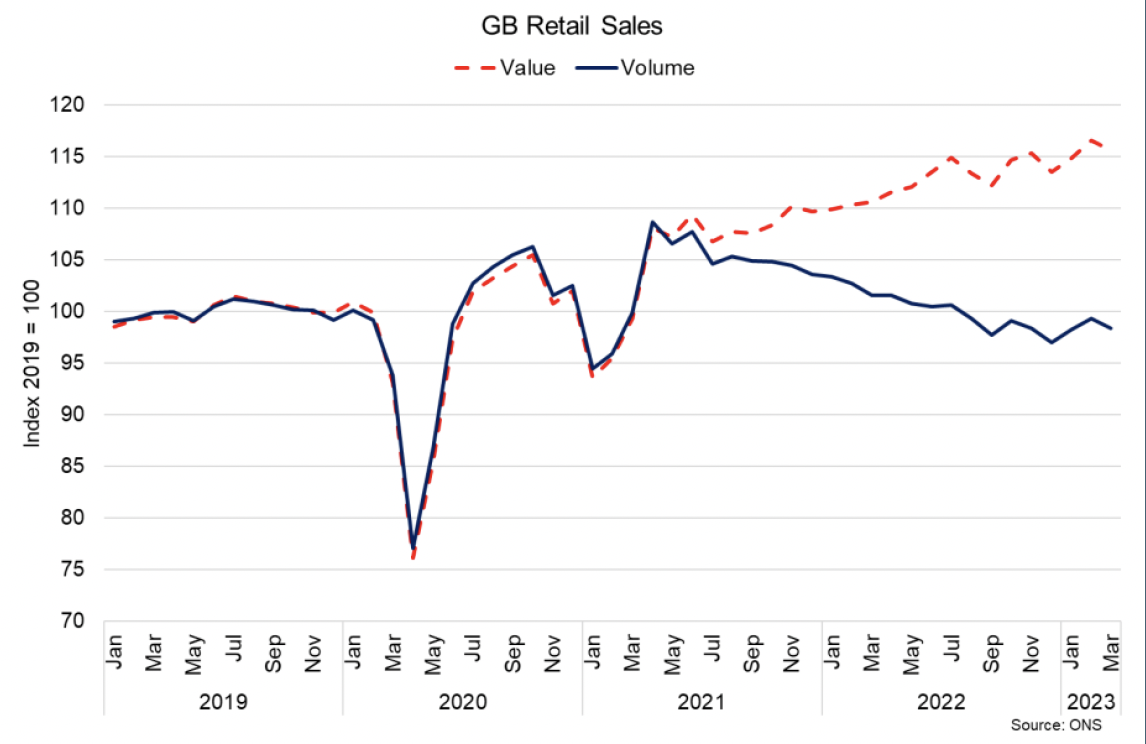

- GB level retail sales volumes fell by 0.9% in March, with a fall across non-food store sales (-1.3%) and food store sales (-0.7%). However, in the three months to March, sales volumes grew 0.6%, the first 3-monthly rise since August 2021. [17]

- Retailers indicated that poor weather conditions impacted most recent sales in March, however more broadly, retail sales volumes have fallen 3.1% over the year with retailers indicating that the increased cost of living and food prices if impacting sales volumes.

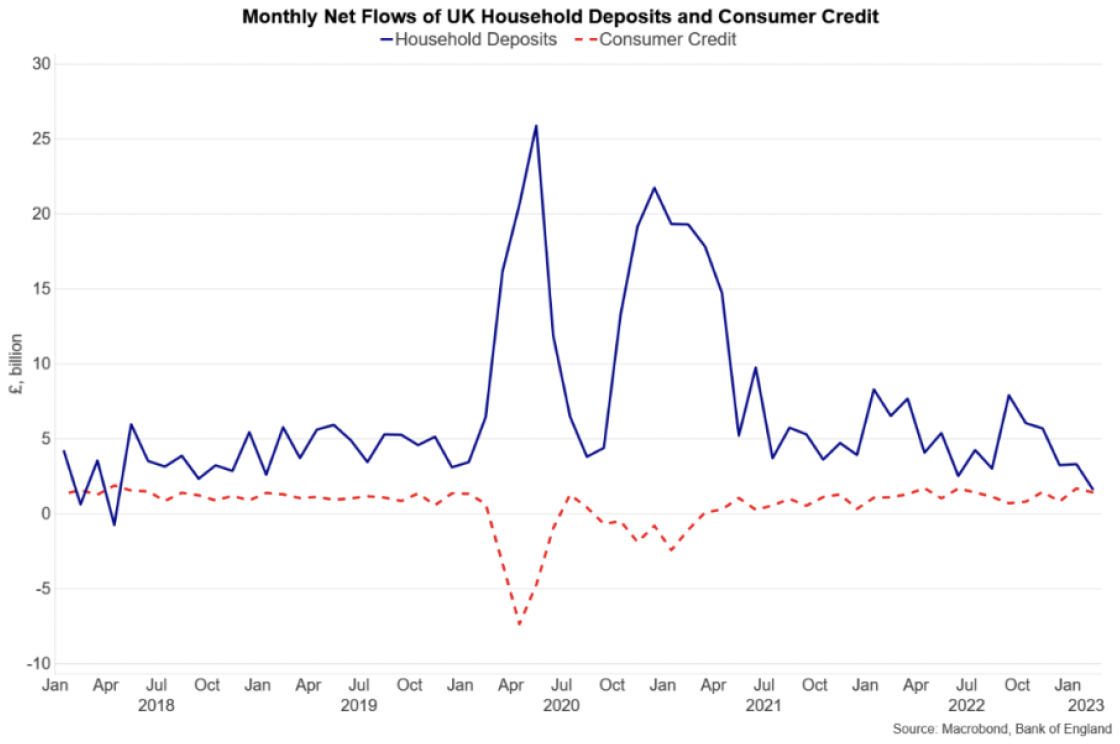

Household Savings and Consumer Credit

- The impacts of the rise in cost of living and higher interest rates on households are continuing to develop as disposable income, spending, savings and credit flows have been re-balancing over the past year following notable shifts during the pandemic.

- More recently, at an aggregate level, Bank of England Money and Credit data shows additional net flows from UK households into deposit-like accounts fell to £1.6 billion in February (down from £3.3 billion in January). [18] Alongside this, consumers borrowed an additional £1.4 billion in February, following £1.7 billion of borrowing in January.

- Additional savings built up during the pandemic and credit have provided the potential to support consumption as household finances have been squeezed in real terms through higher inflation over the past year. Where savings or borrowing have supported spending to date, we may see consumption more at risk and exposed to lower levels of savings and higher interest rates/borrowing costs in the year ahead.

Contact

Email: OCEABusiness@gov.scot