Monthly economic brief: April 2023

The monthly economic brief provides a summary of latest key economic statistics, forecasts and analysis on the Scottish economy.

Inflation

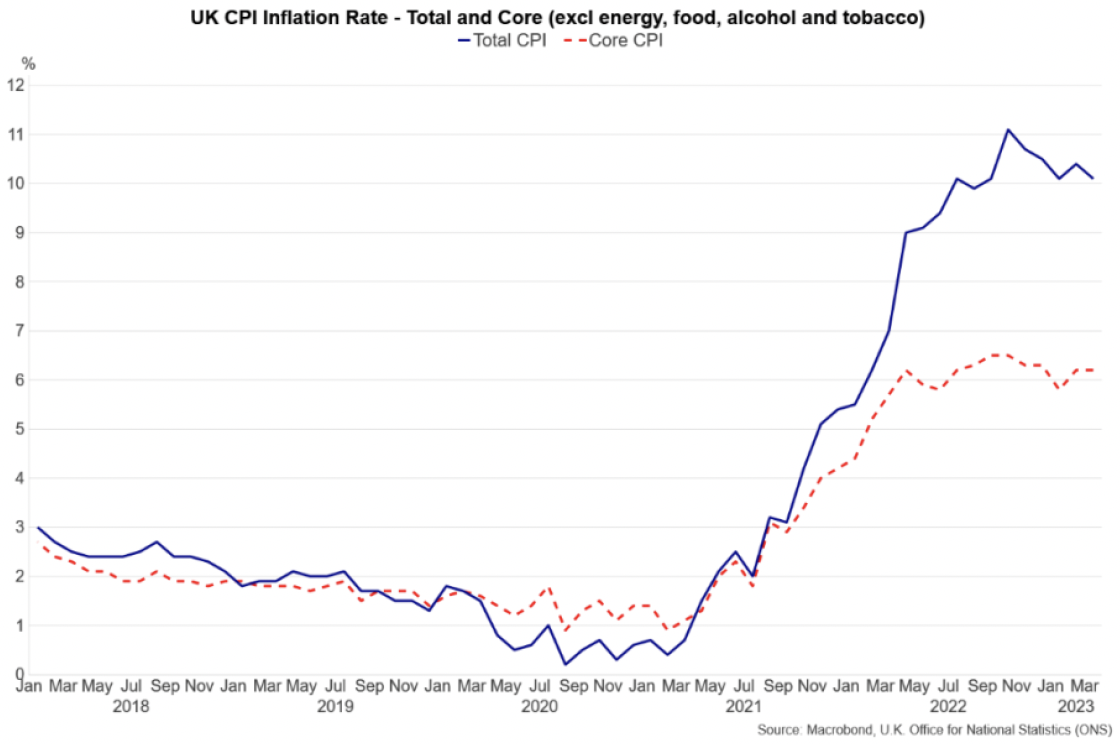

Inflation continued its downward trend in March.

- UK CPI inflation fell to 10.1% in March, following a rise in February to 10.4%, and is on a downward trend from its recent peak of 11.1% in October. [2]

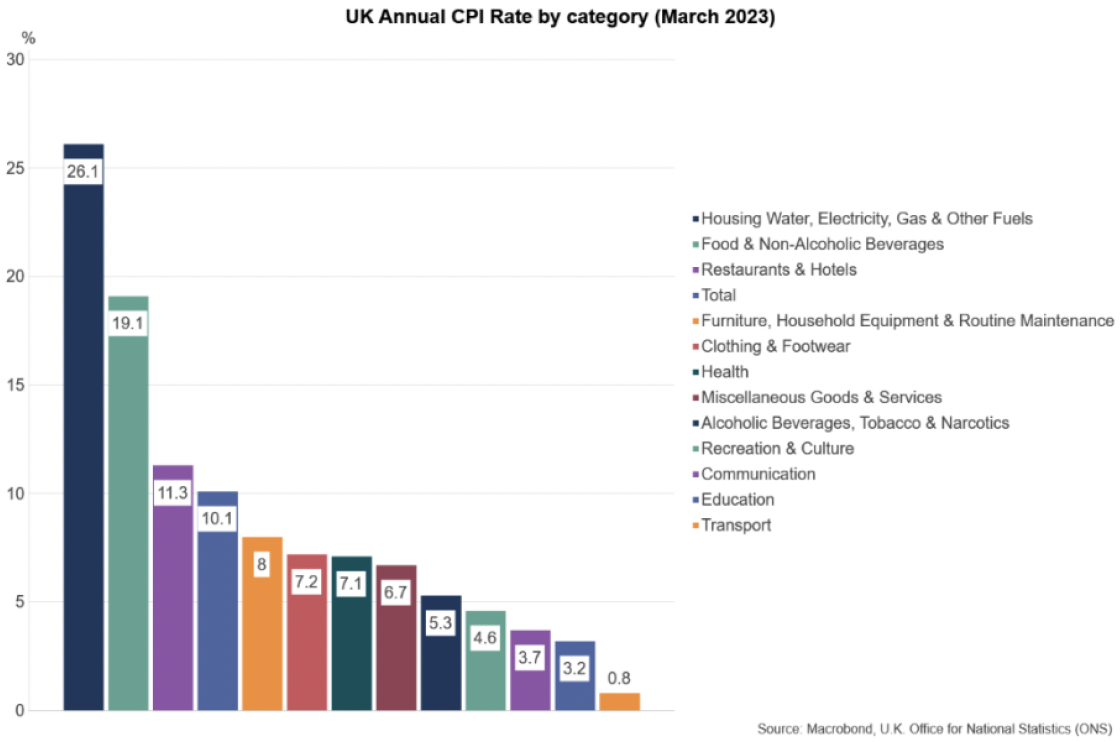

- A key driver of the fall in March was in motor fuel prices which fell 5.9% annually, however this was partially offset by a further increase in food and non-alcoholic drink prices with their annual rate rising to 19.1%, the highest rate since 1977.

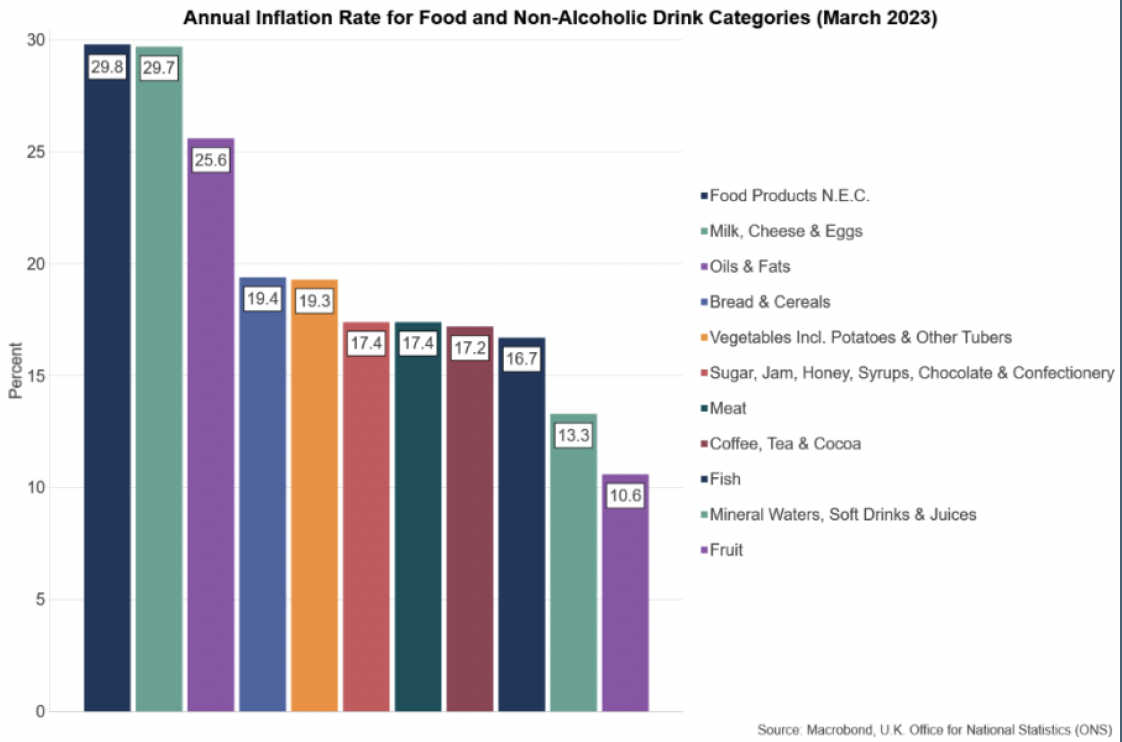

- The rise in food price inflation has been broad based in the UK. Annual inflation rates in March include: milk, cheese and eggs (29.7%), bread and cereals (19.4%), vegetables (19.3%), meat (17.4%). Food price inflation has also risen sharply internationally in part reflecting the ongoing feed through of supply side factors over the past year exacerbated by the war in Ukraine. Food price inflation in the EU was 19.6% in March, including 22.9% in Germany, 18.4% in the Netherlands, 17.2% in France and 13.3% in Italy. [3]

- Prices for housing, water, electricity, gas and other fuels continued to have the largest increase over the year (26.1%) and within that, electricity, gas and other fuels (85.6%), however the annual inflation rate for these are expected to fall sharply in April as the large increases in energy prices which occurred last year drop out of the annual inflation calculation.

- Core inflation, which excludes food, energy, alcohol and tobacco, was unchanged at 6.2% in March and is slightly lower than its recent peak of 6.5% in October 2022. Core inflation has been around 6% since April 2022, highlighting that energy price rises have been the main driver of overall inflation over this period. However, over the longer term, core inflation has risen from 1.4% at the start of 2021 and its persistence reflects that inflation has been broad based.

The Outlook for Inflation

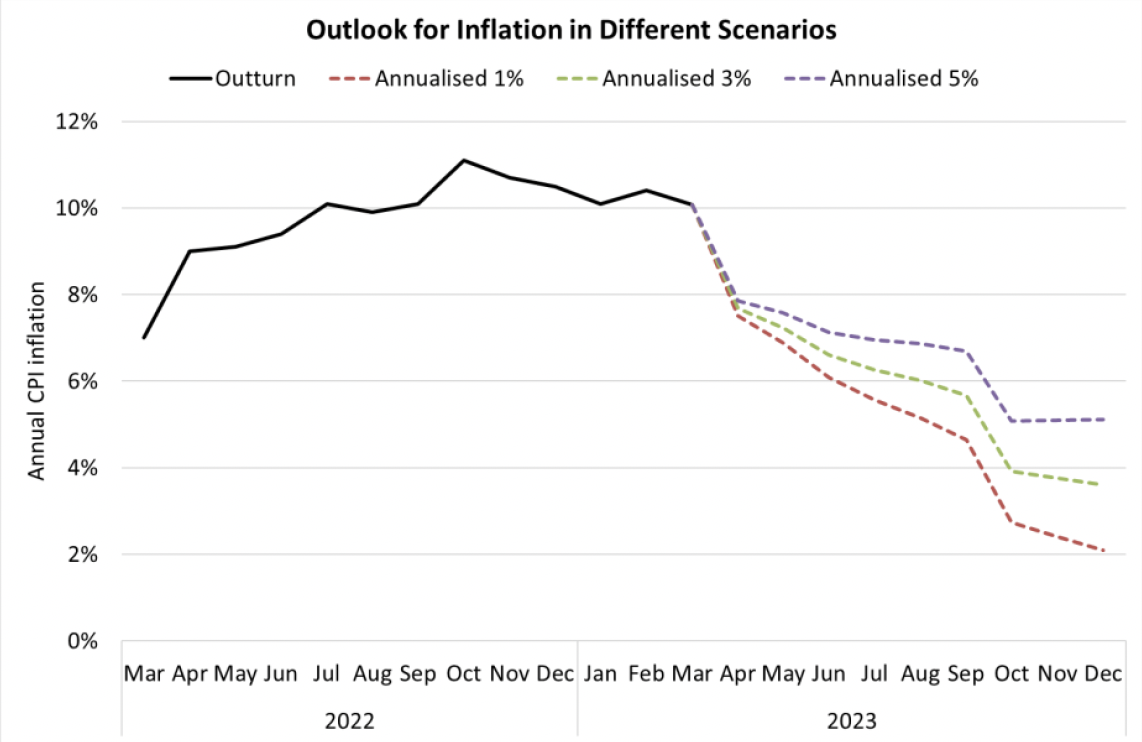

Even if inflation pressures persists, headline inflation is set to fall across 2023, although the decline will not be evenly spread.

The chart below outlines three potential scenarios for inflation, based on simple projections assuming a constant increase in the overall price index each month. In the lower scenario, the CPI index increases by 0.2% each month, an annualised rate of 1%, which sees headline inflation fall to the Bank of England's 2% target by the end of the year. In the upper scenario, the CPI index increases by 0.4% each month, an annualised rate of 5%, which is consistent with the rate in underlying core inflation over the last 3 months. The middle scenario is the mid-point of these two.

As can be seen, regardless of the path of monthly inflation, there are likely to be significant falls in headline inflation in the April and October figures, as previous increases in energy prices become part of the baseline figures. In other months, declines in inflation are likely to be much smaller. As such, it is possible that there may again be some months where there is a surprise increase inflation, as happened in February, however, despite this overall inflation is likely to be trending down until at least October 2023.

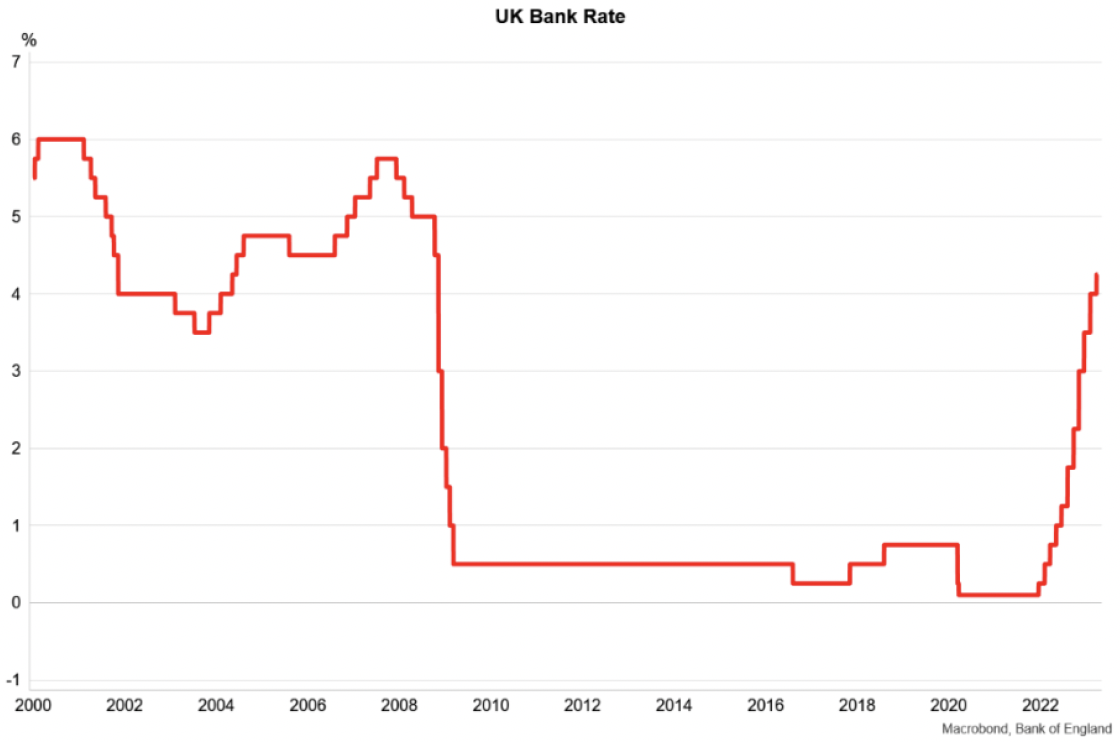

- In March, the Bank of England's Monetary Policy Committee (MPC) raised the Bank Rate by 0.25 percentage points from 4% to 4.25% to further reduce inflationary pressures in the economy. It was the eleventh successive rate rise since December 2021 when the Bank Rate was 0.1% and is at its highest rate since 2008. [4]

- The latest 0.25 p.p. increase is the smallest since June 2022 and reflected the expectation that inflation is likely to be past its peak and will fall sharply in 2023. However, the MPC judged that the latest increase was required because the inflation rate has remained higher than expected and the near-term outlook points to stronger than expected employment and GDP growth.

Contact

Email: OCEABusiness@gov.scot