Future of the Scottish Landfill Communities Fund: consultation

As a result of declining volumes of waste going to landfill, Scottish Landfill Tax revenues have reduced. This directly impacts the future viability of the Scottish Landfill Communities Fund (SLCF). This consultation seeks views on the future of the SLCF to inform future decision making.

Closed

This consultation closed 6 June 2025.

View this consultation on consult.gov.scot, including responses once published.

Consultation analysis

3. SLCF - Future Considerations

Due to the success of Scottish Government environmental and tax policy, the volume of waste sent to landfill in Scotland continues to fall.

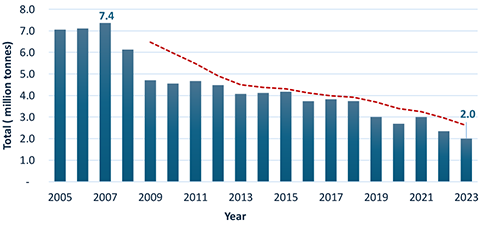

The most recent official statistics published by SEPA shows that Scotland sent two million tonnes to landfill in 2023, a reduction of 72% from 2005 (see Figure 4). This continues a long-term trend of decreasing disposal to landfill and is the lowest annual amount of waste landfilled in Scotland on record. The total amount of waste going to landfill in Scotland has halved over the past decade, and 23% of all waste managed in Scotland was sent to landfill in 2022. In the same year over 62% of waste was recycled, and Scotland met its 2025 target to reduce all waste by 15% for the second year in a row.

Source: Waste landfilled in Scotland summary data

There are two main drivers in diverting waste from landfill:

1. SLfT acts as a fiscal incentive to reduce the amount of waste going to landfill, through making it a relatively expensive option, encouraging the re-use and recycling of materials.

2. Waste reduction and circular economy policies, including the ban on the landfilling on biodegradable municipal waste (BMW) and improvements in recycling driven by Scotland's Waste (Scotland) Regulations 2012

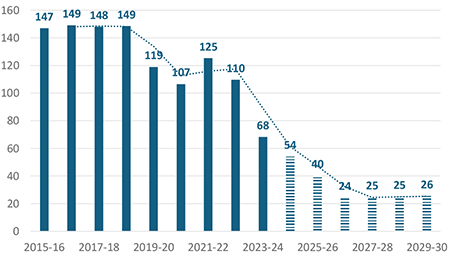

The BMW ban will significantly cut the volume of standard rated waste going to landfill. In preparation for the ban, volumes of waste have reduced substantially with many local authorities migrating towards the incineration of waste as an alternative, while also continuing to focus on waste prevention, and driving greater reuse and recycling. The reduction in volumes of waste sent to landfill is reflected in lower SLfT revenues, as shown in figure 5 below. This figure also includes Scottish Fiscal Commission forecast revenues up until 2029-30.

Source: Fiscal Framework outturn reports and SFC Dec 24 Forecasts

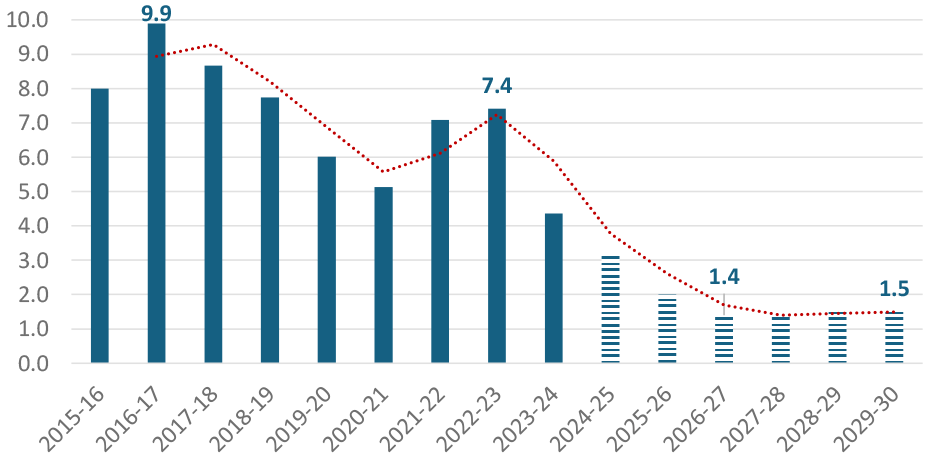

As the funding for the SLCF is directly linked to SLfT revenues, when SLfT revenues reduce the contributions landfill operators can make to the SLCF will also reduce.

Figure 6 below sets out SLCF contributions from 2015 and includes forecast SLCF contributions up to 2029-30. The figure indicates that the Scottish Fiscal Commission forecast that contributions to the SLCF will decrease to around £1.4 million from 2026 onwards.

Source: SEPA SLCF end of year reports and SFC Dec 24 Forecasts

The SLCF’s current funding model has been successful in delivering funding to projects throughout Scotland, primarily those focused on supporting community amenities. Due to the success of environmental and tax policies, revenues are however declining to the point that the continuation of the SLCF in its current form will become unsustainable by 2026-27.

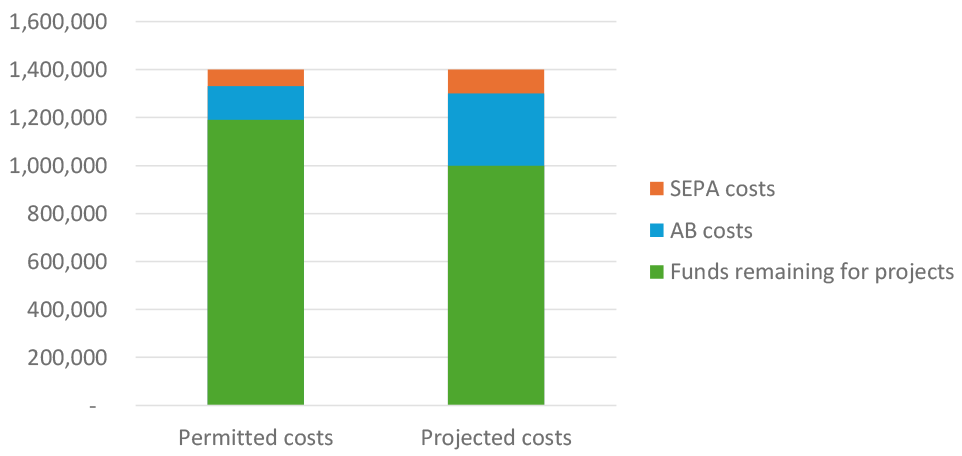

As set out above in section 2, AB and SEPA administration and regulation fees must be deducted before SLCF contributions can be attributed to projects. Based on the current methodology for calculating regulation and administration costs, 2026-27 SLCF costs are estimated to be £400,000. This equates to almost 30% of the projected total contributions to the fund for that year (£1.4m). The regulations that set out what proportion of SLCF funds can be used for administration and regulation costs however only allow a combined maximum of 15% of contributions to be used for these purposes.

This means that, all other things being equal, by 2026-27 the projected administration and regulation costs for the fund will be near double the legally permitted levels and that the ABs and SEPA could not therefore receive sufficient direct funds through qualifying contributions to meet anticipated regulatory and administration costs. This is shown in Figure 7.

A further consideration here is that, even if legislation was introduced immediately to prevent further contributions to the fund, Approved Bodies would be unlikely to be able to direct all of the contributions made by operators to projects before the end of 2025-26.

Source: SEPA data and SFC Dec 2024 forecasts

As set out above, the SLCF will become unviable in its current form as of 2026-27 at the latest, with administration costs forecast to be double those permitted within the current legislation.

The questions below seek your views on potential alternative arrangements which the Scottish Government could consider to enable a fund to continue. There is also opportunity to give your views on the implications for Approved Bodies, communities and other organisations were the SLCF to have to close. However, you can provide more detail on this aspect in the impact assessments section of this consultation.

Question 1: Without substantial change, it will not be possible for the SLCF to continue operating. In your view, what would be the implications of closing the SLCF?

Question 2: Are there changes that could be made to the tax credit element of the SLCF that would allow the fund to continue? Please provide further detail.

Question 3: Are there changes that could be made to the funding objectives element of the SLCF that would allow the fund to continue? Please provide further detail.

Question 4: Are there changes that could be made to the regulation and administration element of the SLCF that would allow the fund to continue? Please provide further detail.

Question 5: Are there alternatives to a tax credit-based model which the Scottish Government should consider? Please provide further detail.

Question 6: Are there other alternative approaches not listed above that Scottish Government should consider? Please provide further detail or supporting evidence.

Contact

Email: devolvedtaxes@gov.scot