Future of the Scottish Landfill Communities Fund: consultation

As a result of declining volumes of waste going to landfill, Scottish Landfill Tax revenues have reduced. This directly impacts the future viability of the Scottish Landfill Communities Fund (SLCF). This consultation seeks views on the future of the SLCF to inform future decision making.

Closed

This consultation closed 6 June 2025.

View this consultation on consult.gov.scot, including responses once published.

Consultation analysis

2. Scottish Landfill Communities Fund – Context and Current Arrangements

2.1 Scottish Landfill Tax

Scottish Landfill Tax (SLfT) is a tax on the disposal of waste to landfill. The tax is paid by landfill operators, based upon the weight and type of waste material. SLfT aims to reduce the amount of waste sent to landfill, thereby supporting the Scottish Government’s broader circular economy and waste reduction objectives.

SLfT was introduced on 1 April 2015, replacing UK Landfill Tax in Scotland[1]. SLfT is an environmental tax which is designed primarily to change behaviours rather than raise revenue. It seeks to dis-incentivise landfill as a waste disposal mechanism through increasing total costs, thereby encouraging prevention, reuse and recycling of waste and helping keep valuable resources circulating in the Scottish economy.

SLfT is fully devolved to the Scottish Parliament, with the Scottish Government responsible for bringing forward legislative proposals and policy decisions including setting SLfT rates. Tax rates are announced in the annual Scottish Budget. The tax is administered by Revenue Scotland, Scotland’s devolved tax authority, which is responsible for the collection and administration of all fully devolved taxes.

2.2 Landfill operators and Landfill sites

SLfT is paid by landfill operators, which are organisations that dispose of waste at landfill sites. Waste can be municipal waste from local authorities and households, as well as commercially generated waste from private sector businesses, including construction and demolition waste.

Authorised Landfill sites are the locations, licensed by SEPA, where domestic and industrial waste is disposed of. The management of landfill sites is controlled by Pollution Prevention Control (PPC) permits issued by SEPA. These permits set out conditions that must be met in order to mitigate and prevent pollution of the environment and harm to people, in line with the Landfill (Scotland) Regulations 2003 and in conjunction with the requirements of planning authorities.

There are currently 24 registered landfill operators in Scotland, managing 41 landfill sites. One of these is permitted to take hazardous waste.

Seven local authorities operate landfill sites in Scotland and are registered taxpayers for SLfT. These are primarily in more rural areas where commercial landfill sites may not be as economically viable. All other landfill sites in Scotland are operated by private companies.

Landfill operators vary in scale and type. Some operate landfill sites as part of wider a business involving waste recycling, processing, and the generation of energy from waste, while some small or family businesses operate on a smaller scale. Some companies operate their own landfill sites to dispose of particular waste streams, for example residual waste from recycling and wash plants.

As part of the waste disposal to landfill process, waste can be processed through a Transfer Station. Transfer Stations are the buildings or processing sites where waste management operators temporarily house waste. At these facilities waste can be separated to remove recyclable material, reusable material and biodegradable organic waste. The remaining waste is then sent on to registered landfill sites or energy from waste plants for incineration.

2.3 The Scottish Landfill Communities Fund

The Scottish Landfill Communities Fund (SLCF) is a voluntary tax credit scheme linked to SLfT. The fund was established to mirror the UK Landfill Tax Communities Fund when SLfT was introduced in 2015, with the purpose of benefitting community and environmental projects.

Funds contributed to the SLCF can currently be used to support projects under six key themes, known as “Objects”. The six objects (A-F) of the scheme are contained in regulation 29(5) of The Scottish Landfill Tax (Administration) Regulations 2015 and can be summarised as follows:

Object A and B can be funded anywhere in Scotland. These are:

Object A: Reclamation, remediation, restoration or any other operation intended to facilitate economic, social or environmental use on land with restricted use due to a previous activity.

Object B: Community based waste prevention, recycling and reuse projects.

Objects C, D and E must be within 10 miles of a Landfill Site or Waste Transfer Station. These are:

Object C: Provision, improvement, maintenance of a public park or other not for profit public amenity. Projects funded under object C must be able to demonstrate clear public access, by being open to the wider community for a minimum of 2 full days per week, 4 evenings per week or 12 full weeks of the year (if seasonal).

Object D: The conservation or promotion of biological diversity through the provision, conservation, restoration and/or enhancement of a natural habitat of Scotland or the maintenance or recovery of a species in its natural Scottish habitat.

Object E: Maintenance, repair or restoration of historic structures or sites of religious worship, historic, archaeological or architectural interest open to the public in Scotland, including their landscape context.

Object F provides financial and administration services to bodies enrolled with an Approved Body.

Further detail is set out below, but the roles of the main organisations and interests in the SLCF can be summarised as follows:

- Landfill Operators contribute funding to approved bodies, to be used to support community projects.

- Approved Bodies are responsible for distributing funding to projects and for taking decisions on which projects should be supported.

- Projects apply to and receive funding from Approved Bodies.

- Revenue Scotland has overall responsibility for controlling and administering the SLCF.

- SEPA has been appointed by Revenue Scotland to regulate the approved bodies within the SLCF.

- Scottish Government is responsible for setting the credit-rate and objectives of the SLCF, through legislation which must be scrutinised and approved by the Scottish Parliament.

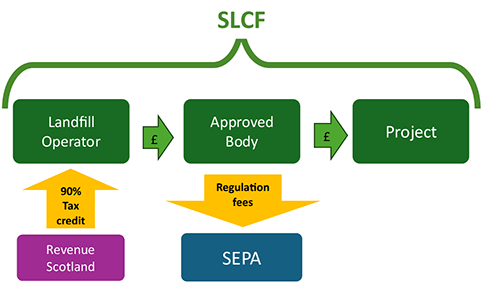

There are a number of different elements that make up the SLCF, as detailed in Figure 1.The commentary below illustrates how these elements interact to support projects.

2.4 Funding the Scheme: Qualifying Contributions and Tax credit

The funding to support SLCF projects is provided by landfill operators. Landfill operators must be registered with SEPA to contribute to the SLCF.

Participating landfill site operators can contribute part of their SLfT liability (currently up to a maximum of 5.6%) to the Fund. They can then claim 90% of any contribution back as a tax credit from Revenue Scotland. This is claimed as part of the operator’s SLfT return.

The remaining 10% not covered by the tax credit will in some cases be absorbed the landfill operator, reflecting the benefits that can be derived from participating in the SLCF and supporting community projects.

Alternatively, the landfill operator may find a third party to reimburse the 10% gap, thus making their contribution to the SLCF cost neutral. This third party is known as the Contributing Third Party (CTP). The payment by the CTP is made to ensure that the landfill operator can continue contributing to the fund.

Participation in the SLCF is entirely voluntary. As such, the continued operation of the fund depends on the levels of contributions received and can naturally fluctuate over time. Data indicates that, from April 2020 onwards, 61% of landfill operators have contributed to the SLCF.

2.5 Supporting Projects - the Role of Approved Bodies

Participating landfill operators provide contributions directly to Approved Bodies (ABs). These organisations, which are registered with and regulated by SEPA, operate on a not-for-profit basis and distribute SLCF awards to eligible projects. There are currently nine registered ABs in Scotland. More information can be found here.

The ABs manage the funds they receive from landfill operators and are responsible for assessing funding applications and attributing funds to projects. The relevant legislation provides that contributions must be used by the AB within two years of their receipt.

The current legislation allows these bodies to claim up to 10% of qualifying contributions received from landfill operators to meet their administrative costs. In addition, before funds can be attributed to projects, they must make a contribution to SEPA for its regulatory fees. This is considered further below.

Since the SLCF began in 2015, ABs have awarded over £55 million to 2072 eligible projects. Projects refer to individuals or organisations that have been awarded funding by one or more ABs.

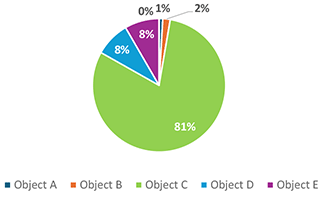

For the period 2020-25, Figures 2 and 3 below provide an overall breakdown of funding by Object, and a more detailed breakdown by year respectively. They show that projects funded via Object C have received the biggest proportion of funding over the period, receiving over 80% of total funding. In more detail:

- £21m of funding has been provided to Object C (public amenity) projects

- £2.3m has gone to Object E (historic buildings) projects

- £1.8m has gone to Object D (biodiversity) projects

- £342,000 has gone to Object B (recycling / reuse) projects

- £224,000 has gone to Object A (reclamation) projects.

Object F (services) does not appear in the above figures as projects under this Object have neither been applied for nor funded in the last 5 years.

Source: SEPA SLCF end of year reports

Source: SEPA SLCF annual reports

Further information on the distribution of SLCF funding from 2015 - 2020 is available in a 5 year review paper published by SEPA.

Further detail and examples of projects funded via the SLCF can be found here.

2.6 Regulatory bodies - Administration and regulation of the SLCF

Revenue Scotland has overall responsible for the regulation of the SLCF, as set out in Regulation 32 of the Scottish Landfill Tax (Administration) Regulations 2015. Its responsibilities include:

- approving the fund regulator (SEPA has been approved to carry out this function from 1 April 2015)

- imposing conditions on the regulator

- arranging repayment of tax credit claimed for contributions made to SLCF where necessary

- enforcing revocation of Approved Bodies.

SEPA has been appointed by Revenue Scotland to regulate the arrangements for the SLCF. This role involves:

- approving organisations as Approved Bodies

- publishing and maintaining the Register of Approved Bodies

- ensuring Approved Bodies comply with the regulations

- invoicing approved bodies for regulatory fees

- processing voluntary revocations of Approved Bodies

- complying with any directions from Revenue Scotland

- charge Approved Bodies for a regulatory fee.

Regulation 29(1) of the Scottish Landfill Tax (Administration) Regulations 2015 sets out the criteria bodies must meet if they wish to be approved by SEPA.

Once a body is approved, they will usually remain approved unless they fail to meet the criteria above and are de-registered by the regulator (SEPA). ABs can also elect to be de-registered should they wish to cease distributing SLCF funding. For example, this may be because a landfill operator who contributes to an AB closes the landfill site which they operate.

Regulation 30(1) for the SLCF states that the maximum amount that can be claimed by SEPA from ABs for regulatory costs is 5% of qualifying contributions. Each year, Revenue Scotland approve SEPA’s regulatory fee for the following financial year. As of 24-25, the maximum 5% regulatory fee has been in place.

Contact

Email: devolvedtaxes@gov.scot