Implications of the UK Government fiscal statements for the Scottish Government Budget: expert panel interim commentary

Independent economic advice to the Scottish Government on the current challenges in the economic and fiscal context and how the Scottish Government could respond to the challenges it is facing through the tax system and the wider implications for public services and the economy.

Introduction

The current economic circumstances facing Scotland and the UK are amongst the most challenging and, in some respects, complex in recent times.

Globally, the International Monetary Fund (IMF) has highlighted that the world economy is slowing and inflation rising as it adapts to the series of economic shocks including Russia's illegal invasion of Ukraine.[1]

Moreover, in addition to needing to rebuild public services and levels of investment post-Covid, Scotland and the UK face particular challenges. These challenges are linked to the loss of access to the European single market, including frictionless trade and free movement of labour.

Like many countries, the UK (and Scottish) economic performance has weakened since the mid-2000's. But as highlighted by the Resolution Foundation[2], the UK has lagged behind its neighbours, with UK economic and investment performance particularly weak since 2016.

The UK Government Growth Plan (or mini budget) set an ambition to raise UK trend growth to 2.5% each year. It aimed to achieve this through a combination of supply-side reforms, tax cuts for high earners, and scrapping planned increases in corporation tax. Instead, the immediate consequences of the mini budget were to create significant political and policy uncertainty and to undermine economic confidence, none of which is conducive to stimulating higher growth in the coming years.

The economic and fiscal environment is unstable and uncertain

The impact of the UK Growth Plan proposed on 23 September has been to create both financial and economic uncertainty in markets. There have been increased borrowing costs for government, business and households, and generally higher uncertainty for households and enterprises.

The lack of independent forecasts from the Office for Budget Responsibility (OBR) to explain the impact of the policies on the public finances and on the prospect of meeting fiscal rules led to a strongly negative reaction from financial markets. The pound initially fell to its lowest level against the dollar in 37 years, the price of government gilts fell sharply, and the Bank of England had to intervene multiple times to restore financial stability.

The ambition to improve economic performance and growth was welcome but to try to do so through tax cuts was not the right approach. Improving productivity and enhancing the supply-side of the economy takes a concerted, coordinated and consistent approach. The UK plan lacked economic coherence and at best would have provided a short-term boost to those with the highest incomes – the markets recognised this and responded accordingly.

Supply-side reforms take time to deliver stronger growth. The short-term focus on unfunded tax cuts set the wrong priority for the economy. As has been pointed out by the IMF and others, cutting taxes alone is not enough to increase growth. Rather, the tax cuts would have been inflationary, increasing the cost of living for millions and increasing inequality at a time when many low-income households face significant hardship.

Although the majority of the UK Government plans have now been reversed, it has not been cost free. The UK Government still faces higher borrowing costs as a consequence of the negative impacts on credibility and market confidence, with the Resolution Foundation estimating that the lasting hit to UK credibility means an additional £10 billion of borrowing costs a year by 2026-27.[3] This undermines economic growth, instead of supporting it.

The changes in the UK Government's fiscal approach are having a significant impact on Scottish budgets. For example, instead of seeing a potential £660 million increase to its funding position over the period 2022-23 to 2024-25, the Scottish Budget now faces a cumulative net loss of £230 million over the same period.

Real term cuts to public services now seem very likely. Not knowing the extent of any future changes in public expenditure at the UK level makes planning for public services and tax choices in Scotland near impossible.

There remains considerable uncertainty as to how the UK Government will return the public finances to a sustainable path ahead of the UK Government's Autumn Statement which, at the time of writing, is to be published on 17th November alongside updated OBR forecasts.

There is a need for a clear and consistent economic and fiscal plan

In the face of such uncertainty, being cautious in policy commitments and the likely need for interventions to support public services and economic resilience should be considered. We suggest that the Scottish Government conveys honestly and openly the issues it has faced in terms that ordinary people can understand.

Policy has a key role to support growth. The Scottish Government currently faces various policy trade-offs including:

(i) providing short-term support to vulnerable households and businesses; and

(ii) investing to grow and improve the productivity and resilience of the economy in the medium to longer term.

A clear and consistent economic and fiscal policy is required in order to provide certainty to households and businesses so that they can make informed spending and investment decisions.

Scotland has taken some steps already in this area, and the National Strategy for Economic Transformation (NSET) highlights further work underway.[4] [5] This strategy sets out clear areas for action and delivery. Being clear on the profiling and prioritisation of these steps in the current economic context is key.

The UK Government has put strong emphasis on improving economic growth through improving the supply-side of the economy. Improving the trend rate of growth is not open to a quick fix and needs concerted and joined up actions across a range of economic domains. The type of growth is also important and needs to be sustainable and in line with other wider policy objectives such as reducing inequality and the transition to net zero.

Doing this successfully will drive improvements in living standards through higher real wages and increased government revenues for public services. Ultimately, this requires increasing the trend rate of productivity growth.

Given the on-going uncertainty relating to UK future spending and tax plans, the UK Government's loss of economic and fiscal credibility and the risk of on-going uncertainty, the Scottish Government should adopt a cautious response.

Alongside focusing on key investment areas reflecting political priorities, we would suggest a continued focus on opportunities to improve productivity and growth as well as improving economic resilience – that is, reducing the Scottish economy's vulnerability to future economic and environmental shocks.

Scotland's budget is determined in part by how quickly Scotland can grow its tax receipts compared to other parts of the UK

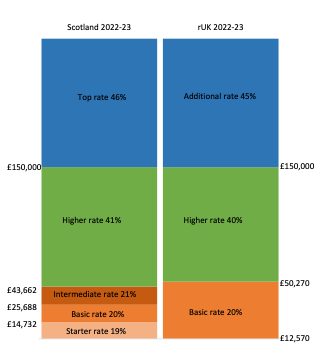

Unlike most other parts of government, the Scottish Government's budget is determined not just by the grants it receives and the tax that it raises, but also crucially by how quickly its tax receipts per head grow relative to the UK. This outcome is heavily influenced by changes in tax policy; economic performance; differences in the composition of the tax base; and differences in the sectoral composition of the two economies. This is particularly true for income tax, which is the largest single devolved tax, accounting for around a quarter of the Scottish Government's budget (see Box A).

Growth in income tax receipts is clearly linked to broader economic performance, in particular growth in earnings and employment. However, due to the progressive nature of the Scottish and UK income tax regimes, receipts are also affected by the structure of the tax base. Growth in incomes for higher earning individuals generates more tax than an equivalent increase in incomes for those on lower incomes. Scotland and the UK have different structures to their tax bases, with the UK having a larger proportion of very high earning individuals and Scotland having more middle income taxpayers.

Box A. Explainer: Scottish Income Tax and the Scottish Government's budget

Since 2017-18, the Scottish Government has set its own rates and bands of income tax for Scotland. This has led to a more progressive income tax regime in Scotland, with three rates replacing the single UK basic rate, and the higher rate threshold starting at a lower level.

Now that income tax is devolved, the amount of money that the Scottish Government receives each year from the UK Government is reduced. The amount it is reduced by depends on the relative amount of money raised in income tax in the rest of the UK. This means that the final Scottish Government budget is determined not just by the amount of revenue raised from Scottish income tax but also, crucially, whether relatively more is raised on a per head basis under the Scottish system than is raised in the rest of the UK.

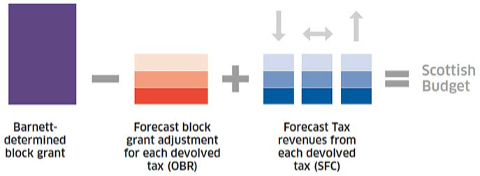

Under the terms of the Fiscal Framework between the UK Government and the Scottish Government, the Scottish Block Grant continues to be calculated by the Barnett formula. However, an adjustment is made to reflect the fact that some of the budget is now funded by Scottish tax revenues that were previously retained by the UK Government (known as the Block Grant Adjustment (BGA), see figure below on the components of the Fiscal Framework.

In the current climate, where earnings growth has disproportionately occurred in the financial services sectors in London and the South East, Scotland is likely to be worse off through relative tax performance. This might be further exacerbated by the UK Government's current plan to lift the current cap on bankers' bonuses.

The UK is relatively unusual in having different rates of income tax, with both Scotland and Wales setting their own rates, rather than a surcharge that is added to the 'federal' tax rate in many other models. Within closely integrated regional labour markets, this raises the risk of policy competition between the nations of the UK, in particular when it comes to attracting top earners who account for a significant amount of revenue.

The recent UK Government policy announcements have again highlighted the risk of behavioural responses from different tax regimes across the UK. The Scottish Government must consider, in any tax changes, whether it also creates risks of tax competition, and possible migration between Scotland and England, particularly of top-rate taxpayers. There are also risks around intra-UK migration, although research published by HMRC has suggested that these are not yet significant. However, it is too early to draw firm conclusions following the 2018-19 Scottish income tax policy reform. Moreover, behavioural changes may take several years to realise their full effect particularly if the tax change is marginal. Nonetheless, it can have important signalling effects for inward investment.

International empirical studies suggest that tax-induced cross-border migration is small in magnitude. For example, analysis of the impact of regional variations of income tax in Spain[6] finds that, although there is an impact from differences in tax rates, this is just one relevant factor in determining behaviour. Non-tax factors also influence people's location choices, such as their professional and family relationships, local amenities or strong regional identities. Indeed, evidence from Switzerland suggests that these non-tax factors are more important than tax factors.[7]

In addition, some of the observed migration responses might not be "real" migration but "paper" migration – where top earners with more than one property across the UK can easily shift their main residence - although empirical evidence is scarce. In such cases, the economic impact of tax changes will be smaller than the impact on government finances.

Overall, these studies suggest that – in the case of raising taxes over the range currently deployed by the Scottish Government - any loss from migration effects is smaller than the impact of raising taxes.

The worsening economic and fiscal outlook has increased the pressure on public expenditure and on public sector pay

The ability to fund wider public services is under strain with the UK Chancellor warning that 'eye-watering' decisions on public spending lie ahead. Independent commentators suggest that the Chancellor might have to announce £30 to £40 billion of cuts or tax increases to balance the books. This is at a time when public expenditure is already being significantly eroded by inflation, with the Scottish Government Budget for this year already worth £1.7 billion less than when it was set in December.

The value of public sector pay, which is already falling in real terms, is also falling behind the private sector. In the latest Office for National Statistics (ONS) figures, annual public sector pay growth is currently at 2.2%, compared to 6.2% for the private sector.[8] Outside the pandemic period, when private sector pay growth was affected by the furlough scheme, this is the largest gap between public and private sector pay growth since comparable records began.

If public sector pay continues to fall behind the private sector, it will be harder to attract and retain public sector workers, which in turn will impact public services. The Scottish Government therefore needs to carefully consider the balance of expenditure on public sector deals alongside other spending pressures.

Investing in productivity is key for fiscal sustainability

Improving productivity is a challenge that is facing advanced economies around the world. Raising productivity is key to raising living standards and ensuring sustainable funding for public services.

Instead of tax cuts, policy needs to focus on improving the supply-side[9] and a key part of that is removing barriers in the economy to participation such as childcare, housing, transport, and the diffusion and adoption of research and innovation. Scotland is already doing important work in this area, for example providing 1,140 hours of funded childcare to help parents of young children continue in the labour market).

The latest evidence[10] on the slowdown in UK innovation and productivity between 2000 and 2019 suggests that for the whole of the UK, including Scotland, the challenge is due to a lack of innovation within industries. In particular the biggest slowdowns in labour productivity and multi-factor productivity growth are in knowledge-intensive, digital-intensive and technology-intensive industries. UK and Scottish Governments therefore should continue to consider ways of improving that adoption and diffusion, through the actions set out in NSET that draw on a range of evidence about the actions that are required to support growth.

The evidence on productivity also suggests that lack of investment (capital deepening) is holding back labour productivity. It is, therefore, also essential to boost investment, and the incentives for additional business investment in the UK Government Growth Plan are welcome. However, as we have seen with the existing super-deduction, they will not boost investment if not supported by a favourable policy environment more generally. Given the tight labour market and shortages of key skills we would expect to see more capital investment by business.

When targeting growth it is important to understand the direction and nature of growth. This has long been recognised by the Scottish Government in successive policy documents, which have emphasised the importance of improving wellbeing and building an inclusive economy in successive policy documents. Investment must not have a short-term focus.

It is crucial to underscore the point that, for both Scotland and the UK, addressing the productivity growth challenge is necessary to sustaining the current level of public service provision, and to ensuring that standards of living can recover following the current inflationary shock to the global economy. It will be imperative for the Scottish Government to make fiscal choices which improve business investment and innovation.

Concluding comments

This commentary sets out some high level issues and advice for the Scottish Government to consider in its forthcoming Budget, in the light of the UK Government's fiscal statements which we summarise as follows:

- The Scottish Government must provide clear and consistent policy providing certainty to households and businesses so that they can make informed spending and investment decisions.

- Given the on-going uncertainty relating to UK future spending and tax plans, the loss of credibility and the risk of on-going uncertainty, we would recommend a cautious response by Scottish Government.

- Alongside focusing on key investment areas reflecting political priorities, we would suggest a continued focus on economic resilience and the opportunities to improve productivity and growth.

Contact

Email: OCEABusiness@gov.scot