Scottish Budget - implications of the UK Government fiscal statements: expert panel final commentary

Independent economic advice to the Scottish Government on the current challenges in the economic and fiscal context and how the Scottish Government could respond to the challenges it is facing through the tax system and the wider implications for public services and the economy.

Main Commentary

Background

In our interim commentary, we noted the need for a clear and consistent economic and fiscal plan. Many of the key themes we identified at the time still remain: a worsening economic outlook is increasing pressure on public expenditure and on public sector pay, and highlighting the need to improve the underlying productivity of the economy, including public services. This will require a consistent and coordinated approach to improving productivity and enhancing the supply-side of the economy, and the Scottish Government must provide clear and consistent policy to households and businesses, giving them certainty so they can make informed spending and investment decisions.

However, there have been significant announcements from the UK Government since our interim commentary. In his Autumn Statement of 17th November 2022[2] the UK Chancellor set out three priorities for the UK: stability; growth; and public services, as he sought to control inflation, repair the public finances and restore stability and confidence to the UK economy.

The Statement was underpinned by the Office for Budget Responsibility's (OBR) forecasts[3] which present a very challenging economic outlook. The UK economy is set to shrink by 2.1% and not return to pre-pandemic levels until the end of 2024. Unemployment will increase to 4.9% in 2024 and inflation will average 10.1% in 2022-23 and 5.5% in 2023-24. All of this will contribute to the largest fall in household incomes on record, with the OBR forecasting real average household disposable income to fall by 7.1% by the end of 2023-24, reversing around 8 years of growth. The outlook for Scotland is being set out by the Scottish Fiscal Commission alongside the Scottish Government’s budget, and is likely to be similarly challenging.

The Autumn Statement announced £25 billion of tax rises and £30 billion of public spending restraint, and a new set of looser fiscal rules, which aim to see borrowing brought below 3% of GDP. On spending, much of this consolidation is delayed until after 2024‑25, and so there is short term support for spending. Benefits and pensions are going up in line with inflation, and additional spending has been provided for health, social care, and schools, although despite this spending is not keeping pace with headline inflation. However, from 2025-26, most public spending growth is limited to growing 1% faster than inflation and capital investment will be frozen in cash terms.

On the revenue side, in the short term most additional revenue is being raised through expanded levies on energy companies. In the medium term, although there has been an extension of "stealth taxes" on households, freezing thresholds across a number of taxes such as income tax and inheritance tax, these raise only a relatively small amount of additional revenue. The main revenue raising comes from the decision to freeze the employer National Insurance Contributions (NICs) threshold from April 2023, which increases the amount of tax paid by businesses, the new energy levies, and a range of smaller tax increases, which together raise over £20 billion.[4]

Outside of support for health, social care, and schools, UK departmental budgets are largely unchanged since last year’s spending review until 2024-25, meaning real terms cuts to many budgets.

The Scottish budget will receive an additional £1.5 billion funding over the next two years as a result of policy decisions that do not apply UK wide. These include increases to health and education spending and changes to business rates. The £1.5 billion comprises £1.9 billion of additional consequentials offset by an increase to the Block Grant Adjustment (BGA) – and hence reduction in net funding – of around £400 million. The increase in the BGA reflects the UK Government tax announcements, most importantly the decision to reduce the UK Additional Rate Threshold of Income Tax and to maintain the UK Basic Rate at 20p indefinitely.

The freeze of capital spending plans in cash terms will likely result in a large real terms cut to the Scottish Government expected capital budget relative to the plans sets out in May’s Medium Term Financial Strategy.[5]

The economic and fiscal environment remains unstable and there is potential for economic disruption

Scotland and the UK are facing a significant economic challenges. Output has already starting contracting and both economies may already be in recession. Inflation has reached 40 year highs, squeezing households’ income and contributing to record falls in living standards.

Although the impact on GDP is forecast to be shallower than previous UK recessions it is forecast to be longer and rising inflation means that the impact on living standards will be significant, with a pronounced and material impact on wellbeing.

Against this background, the Chancellor was aiming to do three things in his Autumn Statement: cushion households and the economy from energy costs; reassure the financial markets; and minimise the pressure for the Bank of England to raise interest rates further. There is no doubt, however, that the fiscal and macro‑economic outlook has changed since the UK Government mini-budget in September. As the OBR forecasts accompanying the Autumn Statement highlight, there is the potential for severe economic disruption in the short to medium term, and for unemployment to rise.

Public finances are once again a key issue that governments need to address. Although terms such as fiscal ‘black holes’ are not helpful, there is no question that the fiscal position has deteriorated, not just in the UK but globally, as evidenced by rising yields on government bonds. But whilst this has mostly been due to global factors, it also reflects UK specific factors such as the cuts to NICs and stamp duty (£18 billion) and a £10 billion UK specific premium to interest premium since the summer.[6]

In the short term, the Chancellor decided not to cut UK spending, which we support given the economic context, but this has required additional tax increases through extended levies on energy companies and fiscal drag, particularly for employers’ NICs. Many of the difficult decisions with regard to how to return the public finances to a sustainable footing have essentially been delayed until after the next UK general election, and there remains an open question as to whether the next UK Government will implement the plans set out by the Chancellor.

As a result of the Autumn Statement, the Scottish Government is now facing a fundamentally different scenario to that following the UK Government’s mini-budget in September. The reversal of policies and the resulting changes in economic circumstances mean that, in some ways, the situation is worse. The changes to income tax in the rest of the UK also makes the situation more challenging. This highlights the direct impact that instability in the UK Government’s decision-making can have on the Scottish Government. Policy errors at UK level can lead to serious instability in Scotland’s budgetary position.

The UK Government has been able to loosen its fiscal rules, but the Scottish Government ability to borrow remains constrained

The UK Government has relaxed some of its budgetary constraints or fiscal rules and announced two new fiscal targets instead:

(i) to reduce net borrowing to 3% of GDP (rather than balancing the current budget as required under the currently legislated rules); and

(ii) to reduce debt, as a share of GDP in 2027-28 (rather than 2025-26 as under the legislated rules).

The OBR expect both of those rules to be met,[7] with £18.6 billion (deficit rule) and £9.2 billion (debt rule) headroom to spare. The existing welfare cap in 2024-25 remains in place. However, they also noted that the UK government would have missed its two previous fiscal rules, both by around £10 billion.

The stability in financial markets after the statement despite these changes highlights that the precise fiscal rules themselves are not critical, rather it is important that governments set out credible and sustainable approaches to fiscal policy. The key task for the UK Government is to set out a fiscal plans that reassure those who would lend money to the government, minimises the upward pressure on interest rates, but also do not harm the economy or delay the recovery.

These apparently small changes to how fiscal sustainability is defined offer the UK Government greater flexibility to postpone the fiscal tightening until after the forecast recession which appears sensible. However, it also gives the UK Government more scope to cut capital spending to achieve its deficit rule by treating current and investment spending equally. Cutting investment spending to meet fiscal rules can be self-defeating, potentially hampering productivity and economic activity in the long run and reducing tax revenues.

In contrast, however, the Scottish Government has to effectively balance its budget every year – and this constrains what the Scottish Government can do. It cannot borrow to any significant degree.

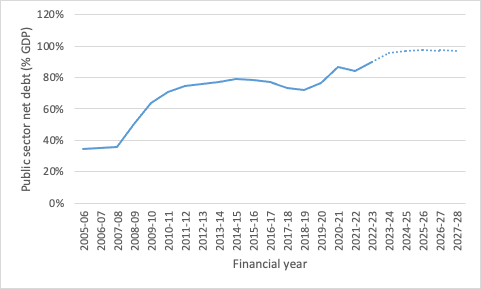

The debt to GDP ratio is projected to come down very slowly in next 5 years and reiterates the importance of making choices that boost productivity growth.

As noted by the OBR, the Government is due to meet his fiscal targets with minimal headroom. As a result, although the debt to GDP ratio is projected fall, it does so very slowly in next 5 years.

Source: Office for Budget Responsibility

Although it is normal for debt to increase during a recession, the UK has failed to address the accumulation of debt following the financial crisis and the pandemic. This is linked to the reduction in the growth rate of the economy after the crisis, and reiterates the importance of addressing the UK’s productivity growth problem. UK productivity is set to continue to weaken. The OBR have highlighted that by 2027-28 growth rate will be not only be lower than the pre-financial crisis average but lower than the growth rate seen between 2010 and 2019. Even this weak outlook is more positive than many external forecasters.[8]

This weak outlook for growth is directly linked to weakness in the public sector finances, as it results in lower revenue and higher debt to GDP ratios. Investment in productivity enhancing activity remains key for the economy and we would once again highlight importance of innovation and investment in driving productivity in Scotland and the UK. The public sector has its own direct role to play in this, as it accounts for around a fifth of all employment in Scotland.[9] It is important that opportunities to improve productivity across the public sector, including greater use of digital technologies, are a key part of the wider work to improve productivity.

There are implications (and constraints) for devolved taxation

In our earlier commentary we highlighted the risks to revenue from tax differentials between Scotland and the rest of the UK. The Chancellor announced changes to the threshold for the top rate of income tax and other freezes to UK threshold as well as the UK wide Personal Allowance, which will result in additional revenues at a time of high inflation and nominal earnings growth, as more people are brought into the tax system or pay higher tax rates.

The UK Government’s decision to reduce the UK Additional Rate Threshold to £125,140 will have implications for Scottish Government budget. If Scotland were not to follow suit it would lose out through a reduction in its funding through changes to Block Grant Adjustments, as discussed in our earlier commentary, as some top earners would pay lower taxes in Scotland than elsewhere in the UK.

However, due to the operation of the Fiscal Framework, the Scottish Government may also lose out even if it were to match the UK Government change. This is because, as set out in our earlier commentary, this policy would be expected to generate less revenue in Scotland compared to the rest of UK as Scotland has fewer top end tax payers. In other words, the deduction off the block grant is likely to be larger than the increase in Scottish tax receipts, everything else equal.

Since income tax is also a partially devolved tax, the Scottish Government faces limitations if it wanted to reduce its Top Rate Threshold below the UK’s level without creating perverse incentives. This is because the UK-wide Personal Allowance is withdrawn for taxpayers who earn more than £100,000 at a rate of £1 for every £2 earned over £100,000. Taxpayers earning more than £125,140 do not benefit from the Personal Allowance at all. These taxpayers face a marginal rate of taxation of 61.5% on earnings between £100,000 and £125,140. Reducing the Top Rate Threshold below £125,140 would increase this marginal rate even further. The Personal Allowance is a reserved power and therefore the Scottish Government cannot make changes to the taper thresholds.

The Scottish Government should begin to scope other short and medium term options on tax, including on fundamentally “new” taxes, such as taxes on property, land or wealth. The UK Government has begun to take small steps toward new taxes, such as bringing electric vehicles into the tax system, however, these remain relatively minor, and there is scope for more radical changes to deliver a fairer tax system better aligned to a wellbeing economy. There is a considerable body of work which analyses how taxes could be made fairer.[10] Although the income tax system itself is progressive, a number of forms of income, such as income from capital and business income, are taxed at a lower rate, and property taxes could also be reformed.[11] We note that there have been renewed calls for new taxes, such as taxes on wealth, to be introduced to support public services.[12] In practice, as the OECD has pointed out, aligning taxes on earned and other income could address many of the inequality issues without additionally taxing net wealth.[13]

However, it is not straightforward for the Scottish Government to introduce new taxes, as any new tax requires the approval of the UK Government. As has been shown by the lack of progress on implementing the Vacant Land Tax in Wales, the process for obtaining consent from the UK Government is not straightforward.[14] As such, it is likely that new taxes will likely take several years to progress.

In the short term, a careful balance needs to be struck between supporting public services and supporting households through the cost crisis. The Scottish Government is very constrained in this regard, as all additional funding for public services needs to come from additional taxation.

Now is clearly a difficult time to significantly increase the amount that households are paying in income tax, with rising inflation, falling real earnings, and rising interest rates. However, the UK Government’s decision to freeze thresholds will mean that many people will be paying more tax as they are pulled into higher tax brackets, and the freeze in the Personal Allowance means that this will apply in Scotland regardless of the decisions of the Scottish Government.

Nonetheless, the legacy of the decisions made at UK Government Autumn Statement may mean the Scottish Government will have to consider whether higher taxes, new taxes or other ways of raising revenue might be required to maintain investment in public services, as public spending grows more slowly. It will be important to ensure that any changes to the tax system are fair and progressive.

Real terms UK spending cuts are due to come from 2025-26 onwards and will need to be planned for

The outlook for the Scottish budget 2023-24 is challenging. The Scottish Government will need to carefully consider its choices. How can it spend its resources effectively and efficiently to ensure that it builds a wellbeing economy which supports those most in need through the cost of living crisis while improving productivity and economic resilience?

At the same time, the UK Government’s fiscal tightening is heavily back-loaded, with the reductions in spending in particular pencilled in for after April 2025, i.e. after the UK General Election and the current Spending Review period. Hence, while the current budget outlook is challenging, particularly in the need to resource public sector pay settlements in response to high inflation, there will be limited fiscal consolidation in this UK Parliament. For the Spending Review period (up to 2024‑25), plans are little changed for capital spending while day to day spending is £2.5 billion higher at UK level, reflecting increased funding for NHS, social care and schools. The cost of this additional spending has been largely offset by reducing aid spending and, while welcome, overall spending is still set to grow more slowly than headline inflation.

This will mean adjusting the budgetary path for many areas of Scottish Government spend over the next two years to align with that outlook. Adding future fiscal commitments or pressures at this time given the spending outlook is unwise and would require a larger subsequent adjustment.

Beyond 2024-25, even if inflation has reduced to lower levels, the Scottish Government will face longer term spending challenges. Spending will no longer increase in line with GDP, as previously assumed. In particular, capital spending is held flat in cash terms, implying a real-terms cut of 1.2% a year. The Scottish Government is already planning to fully utilise its £250 million annual capital borrowing limit in its plans to deliver its National Infrastructure Mission and boost investment in infrastructure by 1% of GDP. As such there is little it can do to offset these changes. In the longer term, these cuts are likely to be counterproductive to improving productivity growth. Although government investment will remain at relatively high levels, this will continue a pattern of the UK investing less than many of its international peers.[15]

While resource spending will grow by 1% per year in real terms, it will now grow more slowly than the economy. Forecasts beyond the Spending Review period are based on totals rather than detailed spending plans; however, assuming certain departments are protected (NHS, core schools, defence and overseas aid), this would imply a 0.7% real terms cut to ‘unprotected’ spending from 2025-26 onwards.[16]

The Scottish Government will need to consider the implications of these future spending cuts in its planning which should include gathering evidence on the efficiency of spending programmes and using the evidence to prioritise future spending decisions. This should include broader consideration of the opportunities for public sector reform, to ensure that public services are efficient, sustainable and delivering the outcomes that people need.

It is important to prioritise improving wellbeing and productivity across all areas of government spend

Whilst the Scottish Government does spend directly on developing a productive wellbeing economy, overall the Finance and Economy portfolio accounts for a relatively small share of overall Scottish spending at under 4%.[17] As such, spending in other portfolios is also important for the economic success of Scotland. Productivity will be affected by areas such as health, education, housing and transport, as well as also social spend that supports labour participation.

The recent speech by Andy Haldane,[18] former Chief Economist at the Bank of England, reiterated the key role public health plays in supporting the economy, with the health of the UK population now acting as a brake on economic growth as long-term sickness in the UK has reached a record high. The Labour Force Survey shows an increase in long-term sickness which is echoed in the rise in new claims for disability benefits. These have led the OBR to significantly revise up its forecasts for inactivity and spending on health-related and disability benefits.[19]

Public services and government spending provide an important stabiliser during economic downturns and can help maintain the productive capacity of the economy and the wellbeing of citizens. While the increase in the Scottish Government budget following the Autumn Statement has been driven by health and social care announcements, it can still be used to deliver improvements in productivity. It is important that spending across all portfolios is prioritised to deliver improvements in wellbeing and productivity and that the effectiveness of spend is maximised.

The Scottish Government’s Child Poverty Delivery Plan in Scotland brings together all services which impact this – including increasing employment services with the aim of supporting parents to enter and progress in sustainable and fair work through actions taken over the life of the Plan.[20]

There has never been a more important time to consider prioritisation in public services and productivity-enhancing reforms in the public sector. This will require boosting digital infrastructure across every sector of the economy. It will also require ensuring that workers have the skills they need to realise the benefits of the digital economy.

There is an inconsistency with the UK Government cutting capital spending in real terms when productivity growth is a priority

Cuts to capital and infrastructure spend could have negative impacts and are likely to be bad for growth in the long run. As part of the UK Autumn Statement, it was announced that there would be no change in the capital levels for the remaining years of the UK Spending Review (2023-24 and 2024-25), and they would then remain at the same cash level from 2025-26 for three years.

Scotland is constrained by reliance on the UK Government for capital grant allocations as well as limited capital borrowing powers. With the current level of inflation at unprecedented levels, the UK Governments decision to not enhance capital funding will lead to a steep decline in the purchasing power of Scottish Government investments and will lead to a reprioritisation of projects This may hamper the Scottish Government’s ability to meet its net zero targets and damage the economic recovery, which will in turn bring further uncertainty to industries during these challenging and turbulent times.

The UK Government’s decision to maintain levels of investment spending flat in cash terms from 2025‑26 for three years means less investment in infrastructure spending, and runs counter to supporting investment for growth. The Scottish Government should seek to maintain as much capital spend as possible and look to spend that in areas of maximum impact for Scotland’s growth potential, such as the transition to net zero, and in areas which can deliver the maximum leverage, such as generating matching spend from private investments or from UK-wide public investments.

Concluding comments

The economic and fiscal outlook for the Scottish Government budget is challenging and it is inevitable that difficult decisions will have to be made. This commentary has set out some high level issues and advice for the Scottish Government to consider which we summarise as follows:

- The Scottish Government should continue to consider ways that the tax system could be made fairer and better aligned to improving productivity and wellbeing, either through reforms to existing taxes or through the introduction of new taxes.

- Real terms UK spending cuts are likely to be forthcoming from 2025-26 onwards and will need to be planned for. This means adjusting the budgetary path for many areas of Scottish Government spend over the next two years to align with that outlook. This is also an opportunity to maximise the effectiveness of future spending.

- The Scottish Government should seek to maintain as much capital spend as possible, and ensure that it is prioritised and well targeted. This will be key in ensuring a successful transition to net zero and a more productive economy.

- In the long term, improving productivity is key to improving the economic and fiscal outlook. As well as creating a supportive environment for businesses to innovate and invest, the Scottish Government should make sure that the public sector takes advantage of the opportunities digital technology provides to improve efficiency in the public sector.

Contact

Email: OCEABusiness@gov.scot