Coronavirus (COVID-19) Scotland's Strategic Framework update – February 2022: evidence paper

This evidence paper accompanies the Strategic Framework update and provides an overview of the key analysis and evidence underpinning the Framework, published on 22 February 2022.

5. Impact on the economy

5.1 Introduction

Many parts of the economy have been disrupted in various ways and for an extended period of time by the pandemic. Restrictions have closed businesses in some sectors and have also limited the capacity at which businesses can operate through, for example, physical distancing. Businesses less directly affected by restrictions have still been affected by the pandemic as a result of changing consumer demands and ongoing uncertainty.

5.2 The recovery of the economy

As the initial lockdown lifted, and as business and society reopened, there was a reversal of the output contraction for many parts of the domestic economy.

Overall economic output in Scotland, as measured by Gross Domestic Product (GDP), has recently returned to its pre-pandemic level of February 2020 for the first time. The economy is now 0.6% above its pre-pandemic level. Latest monthly data show Scotland’s GDP grew 0.8% in November.

There remains significant differences across sectors in the pace of recovery, which continues to partly reflect the restrictions that have been in place, levels of demand across sectors at this stage of the recovery and the impact of supply chain disruptions on the pace of activity.

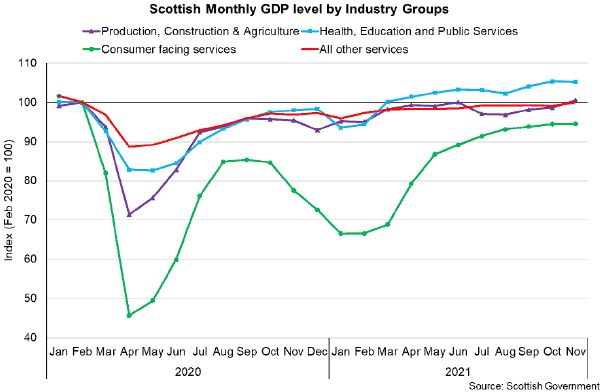

Within the services sector, output in consumer facing services remains 5.5% below pre-pandemic levels while output from health education and public services is 5.2% above its pre-pandemic level and output from all other services is back to the same level of output as prior to the pandemic (Figure 18).

5.3 Economic output has fallen in periods of restrictions

In periods of restrictions, economic output has fallen as a result of fewer businesses trading as well as the limits placed on operational capacity, such as physical distancing.

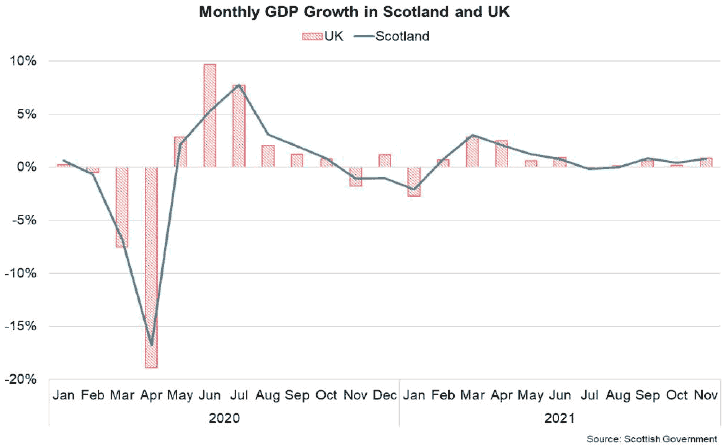

Compared to the initial lockdown in April 2020, the impact on output has been more limited, reflecting both the lesser extent of restrictions as well as the abilities shown by many businesses to adapt their business models. For example, in April 2020 GDP fell 16.7% and in January 2021 it fell 2.1% (Figure 19).

5.4 Sectoral differences in trading patterns

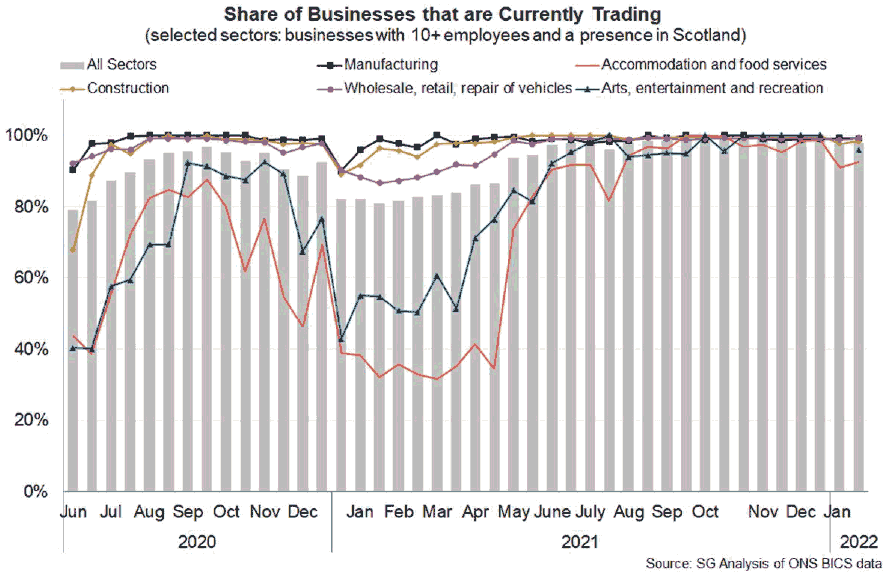

At the beginning of the pandemic, around 80% of businesses were trading in some form in June 2020 (earliest period for which data available). The share of businesses trading has fluctuated as restrictions have changed (Figure 20). There are notable differences across sectors with around 40% of businesses in the accommodation and food services and arts, entertainment and recreation sector trading in June 2020. Even if a business is trading, it may not be operating at the same level of output due to limits to capacity such as physical distancing.

Since August 2021, an average of 99% of businesses have been trading in Scotland and the gap between sectors that had been most directly impacted by restrictions had effectively closed. In January 2022, 98% of all businesses were trading in some form. The accommodation and food services sector reported a lower share of businesses trading at 92.6% reflecting the restrictions in place at that time.

5.5 Sectoral differences in economic output and recovery

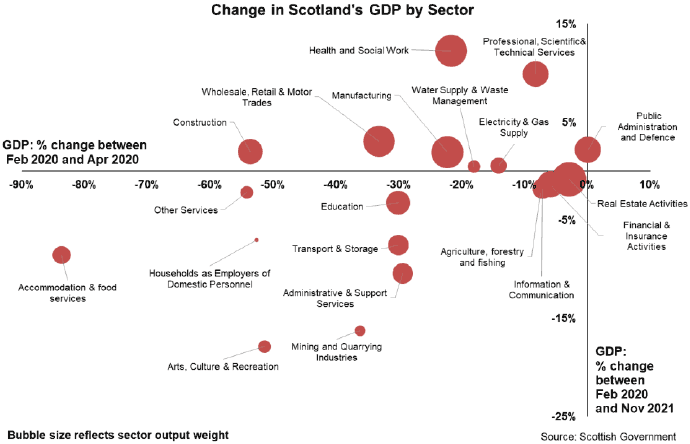

The economic recovery, at present, is K shaped and the sectors that are most impacted by restrictions remain the hardest hit. Figure 21 shows that economic output in Accommodation and Food Services fell around 85% during the first lockdown and its output is remains 8.5% below pre-pandemic levels of output. Output in the Arts, Culture and Recreation services fell around 50% during the initial lockdown and remains 17.9% below pre-pandemic levels.

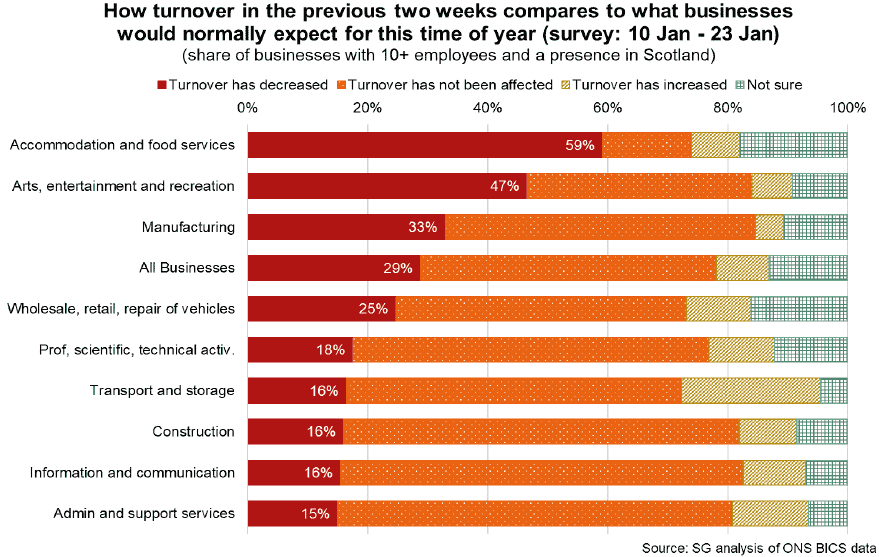

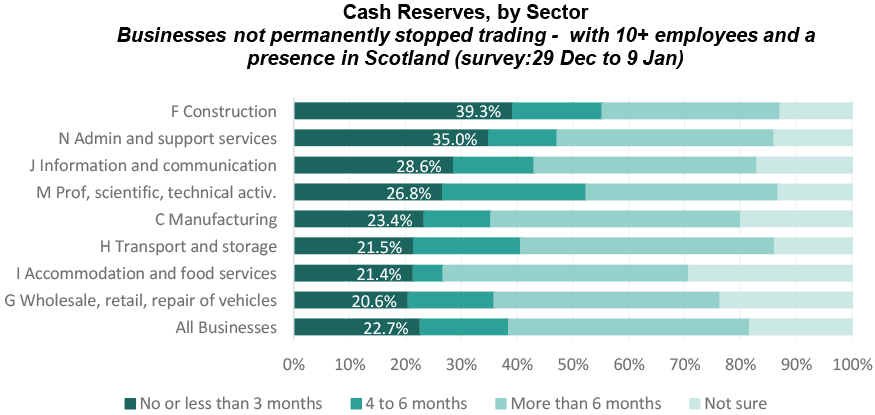

5.6 Turnover and business resilience have been impacted

The financial performance of businesses also continues to vary across sectors. Figure 22 reports views on business turnover in January 2022. It shows that, 29% of all business reported having lower turnover than normal for the time of year[187].

Lower than normal turnover continues to be most widespread in the accommodation and food services sector (59%) and Arts, Entertainment and Recreation (47%).

Figure 23 shows that business resilience remains a key challenge for many businesses, with data for January 2022 showing that 21.4% of Accommodation and Food Services businesses have no or less than 3 months of cash reserves.

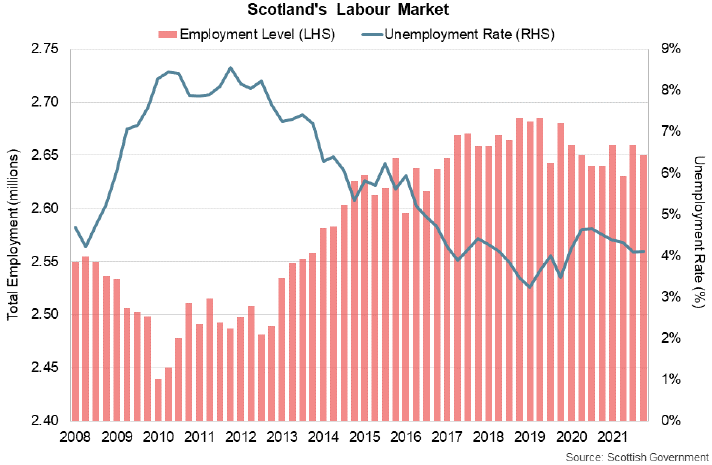

5.7 Labour market headline indicators are strong

The headline labour market indicators compare well against historical trends, reflecting the success of the furlough scheme in protecting jobs. The latest labour market statistics for October to December 2021 show that 2.65 million people were employed in Scotland, an employment rate of 74.1% (up 0.8 percentage points over the year), and the unemployment rate was 4.1% (down 0.5 percentage points over the year) (see Figure 24).

The furlough scheme supported 911,900 unique jobs in Scotland (11.7 million across the UK) and at the end of the scheme in September, 80,800 jobs were being supported - 50.9% of furloughed employments on flexible furlough and the remaining 49.1% fully furloughed[191].

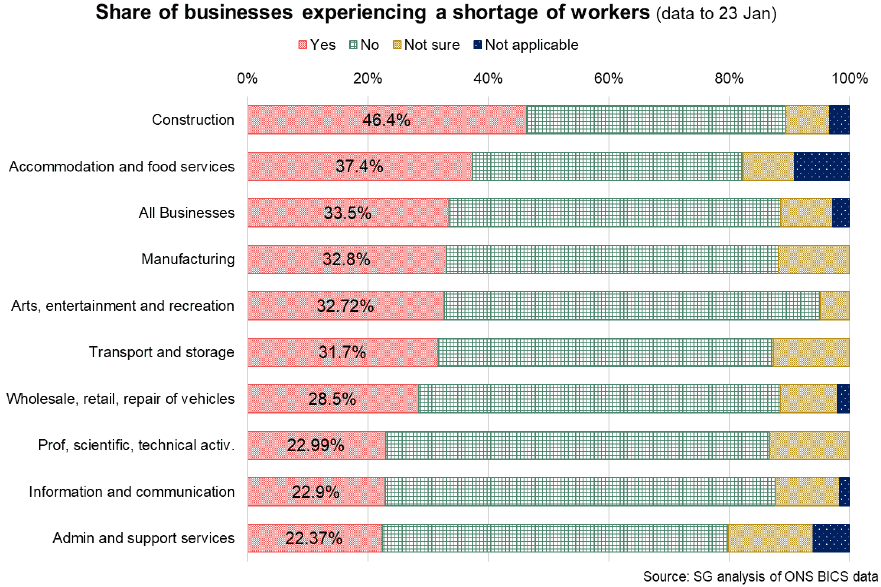

5.8 Labour shortages

Many sectors are currently experiencing staff shortages in part as a result of supply and demand imbalances as the economy has reopened. Figure 25 shows that at the end of January 37.4% of businesses in Scotland in the Accommodation and Food Services sector are currently experiencing staff shortages as the economy has re-opened.

Self-isolation rules have amplified this challenge. Latest surveys[193] show that 3.2% of the workforce were estimated to be on sick leave or not working because of coronavirus (COVID-19) symptoms, self-isolation or quarantine, this is the highest the figure has been since comparable estimates began in June 2020. The Accommodation & Food Services industry sector reported the highest absence share (6.0%).

5.9 Working from home and city centre economies

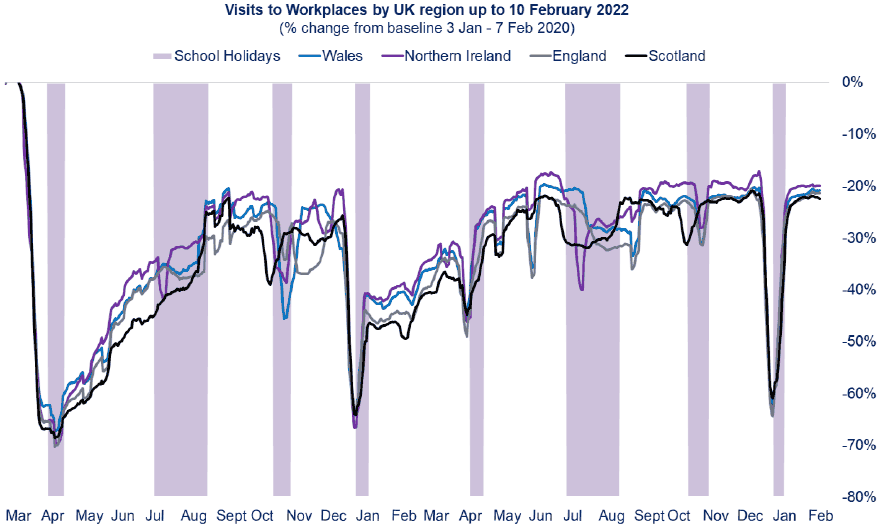

Visits to workplaces have remained consistently below pre-pandemic levels throughout the pandemic but the level has fluctuated as restrictions have varied throughout the UK (see Figure 26). As at 10 February 2022, visits to work places in Scotland are around 22% below their pre-pandemic level. In periods of lockdown, visits to workplaces have been around 60% to 70% below pre-pandemic levels.

There is also evidence that visits to work places continue to vary across Local Authorities in Scotland with cities continuing to be amongst the areas in which visits remain furthest below pre-pandemic levels. For example, in the 7 day period to 10th February 2022 visits to workplaces in Edinburgh remain 31% below and those in Glasgow 26% below pre-pandemic levels[194]. Working from home affects businesses most reliant on office trade, hospitality, retail, which tend to be in city centre locations.

5.10 Summary

Many parts of the economy have been disrupted in various ways and for an extended period of time by the pandemic. Restrictions have closed businesses in some sectors and have also limited the capacity at which businesses can operate through, for example, physical distancing. Businesses less directly affected by restrictions have still been affected by the pandemic as a result of changing consumer demands and ongoing uncertainty. This has had a negative impact on economic output at repeated points throughout the pandemic and prolonged period of restrictions in some sectors has weakened business resilience.

As the initial lockdown lifted, and as business and society reopened, there was a reversal of the output contraction for many parts of the domestic economy. However, not all sectors have recovered at the same rate - the economic recovery is at present K shaped with the sectors that have been most impacted by restrictions remaining furthest below their pre-pandemic levels of output. Moreover, even with economic output back or close to pre-pandemic levels, the economy would have grown during the pandemic period, highlighting forgone output growth from the pandemic.

Restrictions such as working from home have had a negative impact on city centre economies in particular, as a result of loss of the associated footfall from office trade in the hospitality and retail sectors.

The headline labour market indicators compare well against historical trends, with unemployment at 4.1% in the period October to December 2021. This reflects the success of the furlough scheme in protecting jobs and underlines the important role of financial and business support in protecting the productive capacity in the economy.

A future scenario within the pandemic could still pose economic challenges, even without restrictions. This is because consumers could change their behaviour, for example in response to any new variant, and voluntarily stay away from some settings, resulting in lower consumption in these sectors of the economy. Self-isolation rules could also lead to work absences with potential adverse consequences for productivity. Although businesses have adapted their business models throughout the pandemic, ongoing uncertainty makes business planning more difficult.