Renewable and zero emissions heating systems in affordable housing projects: evaluation

An evaluation of renewable and zero emissions heating systems in 21 Scottish affordable housing projects. This study assesses the estimated, actual, and counterfactual costs of the projects’ heating systems and determines the drivers behind decision making.

5. Stakeholder interview findings

In this section, findings from the 14 stakeholder interviews representing 18 projects are summarised according to key themes, including: motivations for adopting LZCGTs; the decision-making process to arrive at a given LZCGT heating system; challenges associated with these new technologies; and insights on monitoring these systems.

Supply chain insights are also presented, which have been further informed by discussions with several LZCGT suppliers. Given the many variations between project aims, scales, locations, among other factors, the findings (and the associated tables and figures) are generalised, although important deviations and nuances have been highlighted.

5.1. Chapter summary

The key findings from RSL and Council stakeholder interviews on their LZCGTs experiences are:

Motivations

Meeting tenant needs, site characteristics, regulations and funding availability were deemed as the top four motivating factors for why RSLs and Councils are using LZCGTs. Climate change and sustainability ambitions were very strong fundamental factors too, with various strategies and ambitions to achieve standards above the baseline as the norm.

Decision making

The expertise and motivations of internal and external decision makers and stakeholders strongly influenced the decision-making process in projects. Capex was one of the main influences on heating system choice, with LZCGT heating systems found to be an expensive aspect of total costs, compared to 'traditional' systems. RSLs balance out the available grant with private finance, and there is a gap in meeting higher than Silver Aspect 1 and 2 standard.

Building fabric

The building fabric specification was the key decider of whether a project qualified for the Affordable Housing Supply Programme's greener subsidy benchmark. A few stakeholders suggested that this cost an additional £6,000 to £9,000 per unit. Fabric and technology choice are interconnected through SAP, of which there were many grievances on its assumptions and inaccuracies.

Network costs

Most stakeholders were not concerned about LZCGTs impacting electricity network costs, due to these costs being considered at a much earlier stage in the project (e.g. site acquisition) and sometimes by other stakeholders. If network upgrades were required, these were perceived as a norm for new build sites.

Supply chain

The majority of stakeholders experienced no issues with the supply chain or felt that the supply chain issues were not a major problem for LZCGTs. The exception to this was stakeholders in rural and hard-to-reach areas who were experiencing higher costs and a local skill gap - an issue for construction and ongoing maintenance of LZCGTs.

Challenges to LZCGTs

There is a long list of challenges to LZCGTs that vary depending on stakeholder, site and technology type, but there was a clear top three with the additional cost of LZCGTs over default options being the biggest challenge. Tenant affordability and usability were also identified as key challenges.

Monitoring

There is a gap on monitoring LZCGTs, which could provide important evidence on real-world running costs. Monitoring was identified primarily in communal or district heating systems where it is required for billing and metering. All stakeholders recognised the benefits of monitoring, but a lack of funds was highlighted as the main reason for not establishing a monitoring program.

5.2. Motivations

There are a variety of drivers for why RSLs and Councils are using LZCGTs, as outlined in Table 5, but the stated primary key drivers were:

1. Tenant needs

2. Site characteristics

3. Meeting regulations

4. Funding availability

Despite corporate strategy, climate change ambitions and other 'softer' factors that were mentioned frequently (and scored highly in Table 5 below), the four factors above were identified as the key underlying motivators for incorporating LZCGTs into new build projects. Of primary importance to most stakeholders was the need for their developments to address fuel poverty and be affordable for future tenants, as well as any other additional tenant requirements, such as care needs. Site characteristics, in some cases, provided the motivation to consider LZCGTs due to these being the only technologies that would be viable. For example, LZCGTs were considered if a site was in an off-gas location where the default gas boiler option was not available, if the site was being developed near to an existing heat network, and if a later phase of a project was designed to replicate an earlier phase.

'[The council] declared a climate emergency … so low carbon technologies are always on the agenda as something we need to look at.'

Using LZCGTs to meet building regulations including sustainability aspects (albeit to higher standards) was a key motivator and led to LZCGTs needing to be used over default options (e.g. gas boiler on-gas and electric storage heaters off-gas). Funding availability was rated highly due to all stakeholders needing the funding to make the projects happen. However, the general rhetoric was that it was less of a driving force and more of a necessity to enable LZCGTs to be installed in new builds, due to the cost disparity over the default options.

'With the new regulations for new builds coming in 2024… [the board] took the decision that any new place would have ASHPS.'

Across all RSLs and Councils interviewed, climate change and sustainability ambitions are clearly very strong. All stakeholders discussed various internal strategies to meet their own, city-wide or Government climate goals. Moreover, all stakeholders aim to (and in most cases are) achieve standards above the baseline and are well known to be ahead of private developers in terms of LZCGT adoption.

'The grant is not a driver, but nice, welcome support.'

Having the right stakeholders present was an important factor, but not always stated, or experienced by all projects (perhaps due to the lack of these types of stakeholders). Those with the right external 'hand holders' and internal champions tended to be more motivated by LZCGT and have fewer issues throughout. Hand holders included, for example, LZCGT manufacturers, solution providers, and external consultants, including energy, architects, or engineers (discussed more in section 5.3.1). Often these stakeholders would be involved upfront and throughout the projects.

'We've been using ASHPS since 2011.'

Ongoing Operation and Maintenance (O&M) burdens and having an interest in LZCGT were influencers rather than driving forces. How O&M factors were considered varied (explained in more detail in section 5.3.4) and in some cases posed challenges too (see section 5.5). Similar to having the right stakeholders present, having stakeholders with an interest in LZCGTs led to internal 'champions', which influenced LZCGT selection.

| Driver | Description | Strength of Driver |

|---|---|---|

| Climate Change | Overarching net zero, sustainability and climate change drivers. | 3 |

| Experience of LZCGT | Previous experience of installing and operating LZCGT in homes. | 3 |

| Tenant needs | Consider affordability and future tenants' requirements e.g., care needs. | 3 |

| Interest in LZCGT | An interest in using low carbon technologies and materials. | 1 |

| Site characteristics | Specific requirements of the site e.g., off-gas, already part of heat network, only viable option. | 3 |

| Ongoing O&M | Consideration for the lifetime of the technology and associated running costs. | 1 |

| Innovation opportunity | Innovation trial, demonstration project, or presented with an opportunity to learn about LZCGT. | 3 |

| Funding availability | Availability of grants from e.g., Affordable Housing Supply Programme or Low Carbon Infrastructure Transition Programme. | 3 |

| Stakeholder influencers | Having the right stakeholders present, both external and internal, e.g., energy teams and suppliers involved before project commences. | 2 |

| Meeting Regulations | Using low carbon technologies to meet building or planning requirements. | 3 |

| Company strategy | Company strategy to e.g., achieve higher sustainability standards, reduce their long-term maintenance burden, meet anticipated regulation changes, upgrade business model. | 2 |

5.3. Decision making for heating systems

5.3.1. Decision makers

The expertise of internal decision makers and the motivations of external stakeholders were noted to strongly influence the decision-making process in each project. All of the roles identified through the interview process are listed in the table below.

| Category | Role | Position | Involvement | Responsibility |

|---|---|---|---|---|

| Strategy & Management | Board | Internal | Sometimes | To define the strategy and approve the project team's decisions |

| Project Manager | Either | Sometimes | To ensure that the project runs to schedule and to budget and coordinate between design team and contractors, and sometimes to manage procurement during the construction phase | |

| Housing Team | Internal | Always | To procure a housing development that meets the needs of tenants and the goals of the organisation | |

| Quantity Surveyor | External | Sometimes | To provide a cost estimate for the project and cost control during construction | |

| Design | Architect | Either | Always | To architecturally design the development and coordinate Civil and M&E engineering design |

| Civil Engineer | External | Always | To structurally design the buildings and design civil building services | |

| Mechanical & Electrical Engineer | External | Always | To design the development's mechanical and electrical building services, including energy systems | |

| Design & Advice | Suppliers | External | Always | To advise on and design heating systems |

| Advice | Energy/ Sustainability Team | Internal | Sometimes | To ensure that the development meets sustainability goals and to advise on energy systems |

| Mechanical & Electrical Consultant | External | Sometimes | To advise on the feasibility and impacts of energy system options | |

| Maintenance Team | Either | Sometimes | To confirm that the chosen heating systems can be maintained | |

| Delivery | Developer | External | Sometimes | To design and build affordable housing as a Section 75 requirement for a larger development |

| Main contractor | External | Sometimes | To manage procurement for the construction phase, and sometimes to design and build the project |

Among the project teams interviewed, none had the exact same structure, although most Council projects were led by a housing team and were advised on heating systems by internal energy and/or sustainability teams. Some took on external advice from Quantity Surveyors and Mechanical & Electrical (M&E) Consultants to define and compare options. Suppliers' advice was also taken once systems were chosen. RSLs were more likely to require decisions to be approved by a Board and to have an internal Project Manager.

Taking advice from external consultants was generally perceived as very beneficial in terms of decision-making for heating systems. However, a few drawbacks were noted, namely that their reports create a lot of jargon and were not usually accessible to a lay person.

Of the projects participating in this study, each team's structure was very dependent on the type of development process, with the three key categories being:

- Internally-led – Design and procurement managed by RSL/Council team. Sometimes an external project manager is appointed to lead the development.

- Design and Build (D&B) – Contractor appointed to design and build the development.

- Developer-led – Housing developer approaches RSL offering to design and build affordable homes as a Section 75 requirement for larger development.

In the latter two cases, the developer or contractor will be given a budget and brief to follow by the internal housing team, who is allowed to have the final say on the project's heating systems.

5.3.2. Process

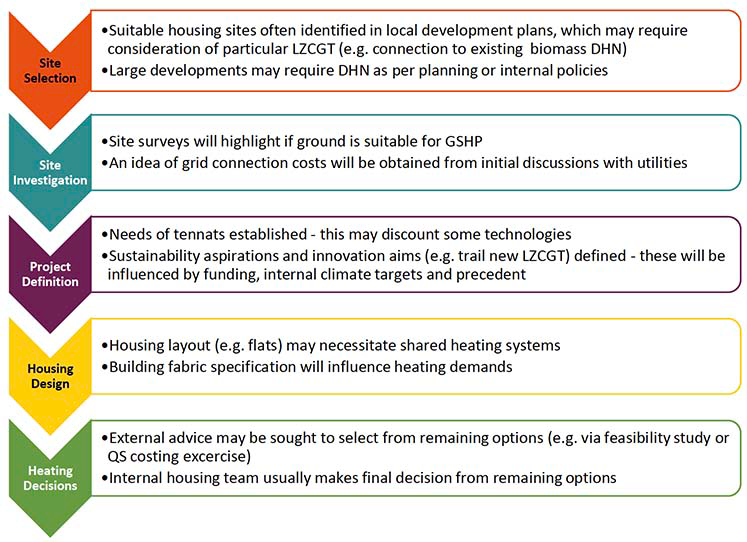

Along the pathway towards developing an affordable housing project, several strategic and design decisions influence the heating system options before these are considered in detail. A generalised decision timeline for an internally led project is provided in Figure 6. The timeline shows the key factors at several stages of development that can open or narrow the options for LZCGTs.

For Design and Build contracts, the Council or RSL will perform the first three stages before appointing a contractor, who must meet the design brief at a negotiated or competitive cost, depending on the tendering process. The project brief will define the sustainability aspirations of the development and may specify a particular LZCGT or range of options for heating systems. For developer-led contracts, an RSL will be approached by a developer, who will have already identified and investigated a site, and will agree to follow the RSL's decision brief. In this case, there is usually the option to choose the same heating system as the main development, but these are more likely to be built to lower sustainability standards than the affordable housing brief necessitates, meaning that gas and other fossil fuel systems are more likely to be specified by developers.

An issue highlighted with the timeline in Figure 6 by one project stakeholder is that the Housing Design stage can 'go too far' before heating systems are considered. If they were considered earlier on in the process, then other aspects of design, such as internal layouts, cupboard space and building fabric specifications, would not need to be revised to accommodate them. The stakeholder who raised this issue did note that it has generally been alleviating over time as more emphasis is placed on the environmental impact of housing developments.

5.3.3. Technology perceptions

In Table 7, perceptions of all heating and hot water systems discussed across the interviews are listed and categorised as reasons for and against their selection. As these are the perceptions of various organisations, some of the points listed may be contradictory. Similarly, the list itself is far from exhaustive as it captures only the points raised during discussions.

| Technology | Reasons for selection | Reasons against selection |

|---|---|---|

| ASHP | Low capex; low opex; tried and tested in terms of design, installation, operation and/or maintenance; external unit accessible for maintenance | Noise concerns for external unit; concern for performance at costal locations; not as operationally efficient as GSHPs |

| ASHP (shared) | Best LZCGT option for flats where DHNs are not feasible | DHN feasible instead |

| GSHP | Few parts for tenants to interact with; low operational costs; low maintenance burden | High capex; ground not suitable; landscape not suitable (too hilly) |

| Heat battery | To trial a new technology; to meet higher sustainability standards | Perceived as unsuitable for larger properties; risk of new technology in isolated (island) location; only one manufacturer; perceived as incompatible with SAP |

| Solar PV | Enhanced SAP scores; reduced energy opex facilitated | High maintenance burden |

| Biomass DHN | To take advantage of existing Biomass DHN; to trial Biomass DHN; because a DHN was required | High capex; fuel availability and sustainability concerns; commercial VAT rates apply to domestic energy if RSL/Council-owned; too many parties required for development |

| Mechanical Ventilation with Heat Recovery | To facilitate higher levels of airtightness required to achieve better building fabric performance | Wary of tenant interaction with ventilation |

| Solar thermal water heating | To provide free water heating to comply with Aspect Silver level 3: Energy for water heating[1] | None identified – incorporated only in one development |

| Mains Gas | Low capex; low opex; tried and tested | High operating emissions; requires PV to pass SAP; non-compliance with incoming regulations; short operational life |

| LPG DHN | Low capex (compared to other DHN options); tried and tested; | High operating emissions; wary of low capex as a loss-leader for opex; wary of long-term supply contracts; requires PV to pass SAP |

| Electric storage heaters | Low capex; Simplicity for operation | High opex; limited suitable tariffs; requires PV to pass SAP |

Within this study, ASHPs were a clear favourite LZCGT for heating. This is because they are widely perceived as able to provide a balance between costs to the Council/RSL (capital and maintenance costs) and operational costs (paid by tenants). Also, unlike gas and electric storage systems, they also pass SAP without requiring solar PV. As such, they are increasingly viewed as a 'go to' option, and, accordingly, several Councils/RSLs have now established a favoured manufacturer and/or model. Interestingly, the three stakeholders that named favourites each named a different manufacturer (Mitsubishi, Vallaint and Daikin).

It was also evident that many organisations, mainly RSLs, still opt for mains gas systems where possible, unless for the purposes of trailing new technologies. However, a small number of RSLs have now completely dropped mains gas systems from consideration, in anticipation of the incoming updates to Scottish building standards. All of the Councils interviewed have declared a Climate Emergency and so they tended to have stricter sustainability policies that either prohibited gas systems from being considered, or mandated higher standards, such as Silver or Gold standard. For example, one council have declared that all new build homes must meet Gold standard, although it is still possible and permissible to achieve this with gas boilers.

5.3.4. Technology costs

'As regulations tighten, it's becoming harder and harder to square the circle between costs & regulations.'

Almost all stakeholders advised that it is difficult to meet building standards 'affordably', and that LZCGT heating systems themselves are an expensive aspect of total unit costs, particularly compared to traditional gas systems. Therefore, capex was one of the main influences on the choice of heating system for several projects, mainly those that incorporated ASHPs as a sole component. However, several projects were motivated by other factors more than technology capex, and some chose to trial new technologies at additional expense in order to 'do something different' (in this case choosing heat batteries), or to deliver the lowest operational cost system to their tenants (in this case choosing GSHPs).

Where multi-technology heating systems were specified, this was done in order to meet higher sustainability standards, including full Silver and Gold. In these cases, the desire to meet these standards outweighed the cost impacts. Similarly, technology costs were noted as the main reason for not pursuing standards higher than Aspects 1 and 2 of Silver level. Stakeholders from one project – which has ASHPs, heat batteries and PV – noted that it was only possible to include multiple technologies through grant funding from the Scottish Government's Low Carbon Infrastructure Transition Programme.

Technology costs varied greatly between projects, as demonstrated in section 6.1. In general, as would be expected, larger projects benefitted from economies of scale, resulting in lower unit costs for heating systems. Several stakeholders of projects in rural and remote locations, noted that capex for heating systems and most other project costs were much higher. One stakeholder provided a rule of thumb that costs for rural locations tend to be 15% higher than in the Central Belt, and 40% higher for affordable housing projects located on Scottish islands.

5.3.5. Building fabric and SAP

Regarding the design process for affordable housing developments, many stakeholders explained that a 'fabric first approach' was adopted, with u-values (the quantitative indicator for heat loss through a building fabric material) specified by the project's architect at an early stage. Scottish building standards specify maximum allowable u-values in new build homes, which the stakeholders perceived to lead to low heat demands.

'Building standards are very high for energy efficiency now.'

The airtightness of a building (essentially a measure of how 'leaky' it is) is another factor affecting heat demand. Several projects were noted to adopt offsite construction methods to enhance airtightness, amongst other benefits such as less time on site and more standardisation. Four stakeholders made very similar statements relating to the escalating costs of building fabric as u-values and airtightness tended towards PassivHaus[2] standards. As such, there are perceived to be diminishing returns for improving fabric efficiency.

'[Building standards are] at a point of diminishing returns on energy efficiency … we want to be as good as possible before the exponential cost curve towards the passivhaus standard kicks in … it's more than 10-15% more expensive to do a passivhaus.'

The building fabric specification (u-vales and airtightness) was noted to be the key decider of whether a project qualified for the Affordable Housing Supply Programme's greener standard, as this is based on achieving Aspect 2 of Silver level, which caps the annual heating demand of a projects' housing units. One stakeholder noted that to meet the greener standard, an additional £6-7,000 per unit was required, with the majority of this cost being attributed to enhanced insulation. Similarly, one of the projects that met Aspect 2 of Gold level incurred an additional cost of £9,109 per unit for the enhanced insultation needed to reduce annual heat demand by a sufficient amount.

Overall, fabric efficiency seen as a standalone consideration, made earlier on by the project's architect, that doesn't greatly influence LZCGT choice. However, it was acknowledged that achieving good fabric efficiency can lower the capex required for heating systems, by lowering peak demands.

Although they are broadly considered independently, often by different members of a project team, fabric and technology choice are interconnected through SAP. One notable example of this came from a stakeholder who noted that when their project's ASHP specification was changed, they had to add ceiling insultation to some properties in order to achieve the same SAP scores and sustainability standards. This also infers that projects are designed to just meet a given standard in order to do so most cost effectively, and that the higher the standard, or the more aspect levels achieved for a given standard, the more an affordable home will cost to build.

'SAP and EPC calculations are well off compared to the actual, by a factor of 3.'

There were several grievances raised with SAP across the interviews. The two most common were that it penalises Scotland (particularly the north of the country) and certain LZCGTs due to the temperature and emissions assumptions it works on. Additionally, SAP is known to produce very inaccurate operational cost estimates, which form the basis of Energy Performance Certificate (EPC) costs. Despite this point being widely agreed, comparing SAP cost estimates is the most common approach to compare different energy efficiency approaches and technologies amongst Councils, RSLs and their consultants.

5.3.6. Network costs

'We didn't consider network costs at the start. There were compelling reasons to take it forward without this step.'

For biomass and LPG DHNs, network costs are easily determined as they are the main component of capex for these systems. For heat pumps and solar PV-based heating systems, electricity network costs were not found to be a significant influence across the projects in this study. In fact, only one had considered costs – the project with 117 homes. During the development of this project, it was found that a new substation would be required to accommodate the start-up currents of the ASHPs. The new substation cost an additional £50,000, which would not have been afforded without the Low Carbon Infrastructure Transition Programme funding that the project received. For this project, the impact of the heating system choice on network costs was more visible since the technology changed from an LPG network to ASHPs at a later stage.

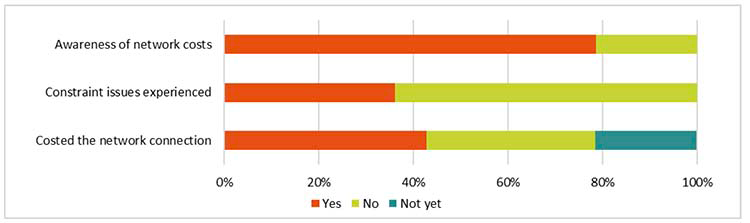

Aside from this example, stakeholders were not concerned about the chosen heating system impacting electricity network costs and generally had limited insight on these costs, due to early-stage investigations being carried out by another stakeholder (either internally or externally) or being looked into at a different phase in the project (e.g. site acquisition). For section 75 developments and design and build contractors, the network works are handled by the developer or contractor, meaning that the RSL is not exposed to these costs. Alternatively, the network costs would have been de-risked at the site acquisition phase by the RSL or contractor.

'We tend to want most of the constraint issues and big costs assessed first.'

'Risks and costs are with the developer … I don't think the connection is a problem or additional cost"

If network upgrades were needed, these were quite often perceived as a norm for new build sites and there were no experiences of surprisingly high network costs. Three RSLs had to build new substations, one of which was on-gas and the other off-gas. Another RSL had a decade of experience with installing ASHPs and noted that paying additional network costs is an issue for large or rural locations, but that, where a substation was required, the impact of electric heating was not guaranteed to be an influence over and above this. Another RSL confirmed that new primary substations are just as likely to be an additional cost to on-gas developments as well, especially on larger sites.

Those more experienced in LZCGTs and dealing with utilities suggested that the Distribution Network Operators are unwilling to investigate how much electricity a site can self-generate to reduce the network upgrade cost. If this changed, one RSL stated that they would be happy to consider batteries or other solutions that could facilitate reduced network capex.

The figure below summarises the interactions of each of the projects represented in this study with electricity network costs.

5.4. Supply chain insights

'There aren't any issues with the supply chain … I think it's just scare mongering.'

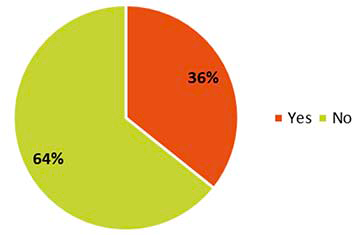

The majority of stakeholders interviewed either did not experience issues with the supply chain or felt that the supply chain issues were not a major problem. The only exception to this was due to location. Those who did experience issues with the supply chain can be directly correlated to location, i.e. the 36% answering 'yes' in Figure 8 were also located in rural and/or remote locations. The key issues experienced were:

- Limited choices depending on what local skills are available. Rural locations are often reliant on transporting in contractors from Scotland's Central Belt, some of whom are believed to be unwilling to do small/very small rural/remote projects. There is a limited pool of available contractors, they tend to be very busy, and may only be certified to install one brand/type of heat pump, for example. This limits the heating design options for the homes.

- Not having readily available maintenance staff in the area. Even if contractors are available for the build, stakeholders are concerned, or have experienced issues with getting the right and readily available maintenance expertise. One stakeholder suggested it would be cheaper to let their heating systems break down rather than procure a standard preventative maintenance regime (i.e. one-year servicing).

- Procurement issues. Specifically, having to use multiple sub-contractors from various locations, providing complicated and unsustainable project management.

- Higher costs. This is thought to be due to limited local competition or having to include contractor travelling costs. This is felt more at smaller sites. As mentioned in section 5.3.4, one stakeholder advised that costs for rural builds are 15% higher than in the Central Belt, and 40% higher for island projects.

This suggests that there is a clear issue with local, readily available and qualified resources in rural areas.

'An ASHP needs servicing once a year … getting contractors to rural areas where there aren't enough skills locally is an issue.'

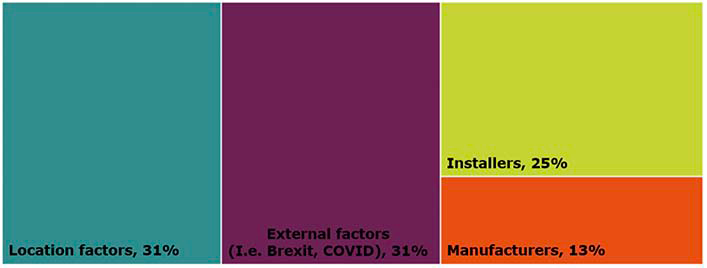

In addition to location, the other supply chain issues (when they were experienced) were due to external factors and installers. Brexit and the COVID-19 pandemic were mentioned as factors that have impacted projects, this included rising costs, availability of materials (steel pipes and radiators) and limitations to travel. Whilst most stakeholders would state that manufacturers and installers are readily available, there were a few issues experienced with installers including perceived over-inflated prices, and the need to have multiple types or specialist contractors on site for installation and commissioning of certain technologies. There were less concerns on manufacturers, with only two stakeholders mentioning issues, including getting the equipment, and due to a worry over potential future issues due to using a start-up manufacturer (e.g. only one heat battery provider).

5.4.1. Industry supply chain insights

Alongside RSL and Council interviews, we also interviewed a small number of industry stakeholders, including manufacturers and suppliers of low carbon technologies, to gain insight into what they think the key challenges to low carbon technologies are and whether supply chain constraints exist. These interviews were undertaken to help confirm or contradict the findings we were gathering from RSL and Council stakeholder interviews.

Key challenges to low carbon technologies

Across all the supply chain interviews, there were a number of common challenges to low carbon technologies that were stated and discussed, including:

- Lower carbon technologies having a higher capital cost compared with default solutions.

- SAP, which is a key issue and at a fundamental level penalises heat pumps over gas boilers.

- Lack of regulations forcing low carbon technologies in new buildings, and uncertainty in future regulations undermine investor confidence.

- Rumours of poorly installed heat pumps are believed to 'put people off'.

- Unlike RSLs, private housing developers do not consider opex, which would be a driving force for using low carbon technologies over the default options.

Critical points in the supply chain

Manufacturers do not see themselves as a critical point in the supply chain and there was consensus across the interviews that they have the capacity today (with high tens of thousands of products produced in the UK) and in the future to meet predicted increasing demand. All of the suppliers we talked to offered multiple products and services to housing developers, and RSLs and have had a lot of experience working with these types of companies, including 'hand-holding' for those who are newer to low carbon technologies.

There were some comments about installers being a key point in the supply chain. There was agreement between manufacturers that there are enough installers, but there appears to be an issue in how much installers are charging. One manufacturer explained that with increasing demand, you would expect prices to fall. However, installers appear to be charging the same or more with increasing demand for their services. It is unclear whether this is due to issues associated with high demand or installers simply 'getting away with charging more'.

5.5. Challenges with LZCGTs

Table 8 provides a summary of the challenge's stakeholders are experiencing with LZCGTs. There is a long list that varies depending on stakeholder, site and technology type, but there is a clear top three:

1. Additional cost

2. Tenant affordability

3. Tenant usability

The additional cost of LZCGTs over default options was the biggest challenge. A common suggestion throughout the interviews was that LZCGTs are more expensive. Section 6 discusses our findings on the cost of LZCGTs compared with the counterfactual for further insight on this. Whether tenants could afford and use them are the other top two challenges for LZCGTs. In terms of affordability, there were concerns from two perspectives. Firstly, to meet ever-increasing sustainability standards and to install LZCGT costs more, and this is inevitably going to be passed on to the tenants in higher rents. Secondly, there were some challenges around whether electric technologies were cheaper to run than gas. Some had experienced complaints from tenants on the cost of the system and plan to investigate tariffs further (i.e. energy suppliers not offering heat pump specific tariffs). There were also perceived and experienced issues with tenants not using LZCGT in the right way despite onboarding, leaflets and instructions being given. It was acknowledged that, fundamentally, the heating systems act in a different way to more familiar heating systems, with lower and enduring heat rather than high-output, boost heat, and tenants were not familiar with this type of heat supply. It seems that even with onboarding from the RSLs and the manufacturers, there are still some issues that need to be addressed.

| Challenge | Description | Score |

|---|---|---|

| Additional costs | Extra capex costs to using LZCGT compared with default options. | |

| Tenant affordability | Running cost concerns e.g. how tenants might/do use them, lack of experience, availability of suitable tariffs. | |

| Tenant usability | Concerns over how user friendly the LZCGT is/will be. | |

| Billing and metering | An issue for communal or district heating systems. | |

| Operation and maintenance | Concerns and issues over how to, and the cost of, O&M for LZCGT. | |

| SAP | Restrictions inherent to SAP calculations and concern over accuracy of, for example, running costs. | |

| Suitability of LZCGT | LZCGT suitability depends on site characteristics and some options are not viable. | |

| Reliant on developer partners | RSLs may not be the decision maker on whether or not to use LZCGT due to, for example, private developer partners. | |

| Limited LZCGT options | Concerns over the limited options available for LZCGT | |

| Uncertainty over new technology | Uncertainty and/or lack of experience or evidence for LZCGT and how it may perform. | |

| Local residents challenge | Challenges from local residents to the development of using specific LZCGT, due to e.g. aesthetics, local pollution. |

The mid-rated concerns include billing and metering, O&M, and SAP. Finding new ways to deal with billing tenants was a challenge in communal and district heating systems projects. One RSL is upgrading their business model to become an Energy Services Company to deal with this (see Figure 15 in Section 7.4.3), others have identified partners to deliver this service. There were many complaints about SAP from a design and running cost perspective. Sometimes SAP calculations made it difficult to install the LZCGT of choice or added on cost. One stakeholder mentioned that they want to use infrared heaters, but these are not currently in SAP, and another RSL had a bit of a shock when they had to install PV in addition to Biomass Boilers to meet requirements. It is experienced and acknowledged across RSLs that the running costs are not accurate in SAP.

'It's a balancing act between grant income and private finance.'

Lower-level challenges are largely due to uncertainty over LZCGTs, but this was for specific technologies, or on less well used LZCGTs, e.g. district heating schemes and heat battery systems. The majority of stakeholders we spoke to had used LZCGTs. There were also a few project-specific issues like the challenges from local residents from one communal biomass boiler system.

5.6. Monitoring

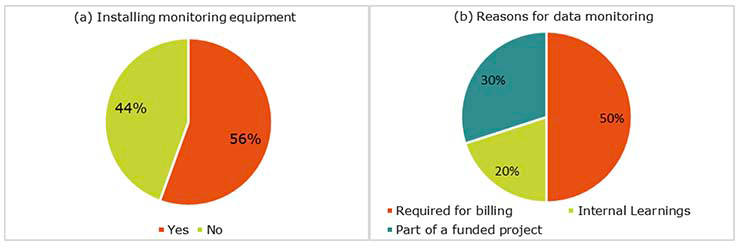

Data monitoring

Nine of the projects in the evaluation include some kind of home energy monitoring program. The range of information collected varies widely and depends on the equipment installed. Among these projects, roughly half have communal systems or heat networks that inherently require heat meters to measure the energy flows into each property for billing purposes. Other projects are looking to monitor energy flows (heat and electricity demands and solar PV generation) as well as a broad range of other factors for internal or external research purposes. To do so, intelligent Internet of Things (IoT) sensors, connected to a LoWaRan network, are the most common approach among these projects[3]. Stakeholders advised that the following measurements would be collected:

- Air quality

- Carbon monoxide concentration

- Building fabric performance

- Internal natural light levels

- Internal humidity

- Internal temperature

- External temperature

- Weather

All stakeholders recognised the benefits of home energy monitoring, and a lack of funds was highlighted as the main reason for not establishing a monitoring program. Among those which do have a monitoring program, several motivations for it were identified, with contractual requirements being the two key drivers:

1. Requirement for billing for communal systems and heat networks

2. Requirement to share information with funders/researchers

3. To confirm that the heating systems work as anticipated and determine if they are useful for future projects

4. To share insights with other external bodies e.g. consultants

5. To troubleshoot tenants' problems e.g. high electricity bills

6. To link to Councils' wider energy programmes e.g. 'smart cities' activities

Aside from contractual obligations, monitoring was recognised as an important aspect of projects that have trialled new LZCGTs, as it allows for the performance of the technologies to be verified. Similarly, it allows for actual bills to be compared to estimates from SAP, which were noted by many to be highly inaccurate predictions. This is particularly important as SAP appears to be relied on more for LZCGTs than for more established heating systems, for which bills are more easily predicted.

'It's part of the feedback loop… we are hoping that everything will be successful but without monitoring it you're never going to know.'

The scale of a project was also noted to influence monitoring programs. For example, one council plans to monitor only one of each unit type, due to the large number of homes in the development. They suggested that they would be able to install further monitoring equipment in homes if tenants highlighted high bills, in order to identify and remedy any issue. Three projects that have a handful of homes with LZCGTs within a larger development plan to monitor these homes as well as the 'standard' home energy systems to compare heating systems within otherwise similar properties. An issue with small samples noted by one RSL was the impact of different household's structure and lifestyles – the interviewee worried that these differences would render the data collected hard to compare.

Surveys and other tenant interactions

All Councils & RSLs interviewed plan to engage with tenants via post-occupancy surveys or have done so already. This appears to be a standard approach across the board, regardless of the heating system installed. A few also plan to use surveys as an analogue method for energy monitoring, through collecting information on energy consumption and electricity tariffs via tenants' bills in order to gain a better understanding of the affordability of heat pumps.

Several intend to take a more involved approach, including educating tenants on how to use their heating systems and, where ASHPs and/or heat batteries are installed, offering advice directly or via third parties on which electricity tariffs will secure cheaper energy bills. There was a general consensus that heat pumps are not inherently cheap to run and that they require the right electricity tariffs in order to be affordable to tenants, and that this advice was therefore necessary to ensure that the homes were affordable in all senses. Similarly, one Council plans to 'coach' tenants to switch to variable electricity tariffs, so that heat pumps and heat battery systems can be programmed to take in electricity from the grid at times when it is cheaper.

Contact

Email: 2024heatstandard@gov.scot