Fishing vessels - economic link: business and regulatory impact assessment

A business and regulatory impact assessment (BRIA) of changes to Scottish economic link conditions contained in Scottish fishing vessels.

2. Purpose and intended effect

Establishing a Scottish landings target for each Scottish licenced and administered fishing vessel is a longstanding ambition of the Scottish Government and was restated as a manifesto pledge in the Programme for Government 2021-22. The Scottish Government is seeking to achieve this commitment by amending the economic link licence condition in Scottish sea fishing licences. The proposed amendments aim to increase the volume and improve the stability of landings of the most valuable fish species into Scottish ports. These benefits should increase and create a more stable supply for Scotland’s fish processing businesses. The policy seeks to improve the distribution of economic benefits arising from Scotland’s natural resources by increasing the value added in Scotland so that local, coastal and rural economies will benefit from increased employment and income from the seafood industry. The policy may help with food security as more raw material (fish) is landed into Scotland.

At present, there are a number of different means by which a Scottish licence holder can comply with economic link arrangements. These are:

I. landing 50% of quota species into UK (so called “Landings Target”);

II. having 50% of their crew resident in the UK;

III. spending 50% of their total expenditure in the UK;

IV. if a licence holder fails to meets any of these options or a combination thereof, they are required to provide quota to its relevant authority – so called “Gifted Quota”.

The key proposed amendments to be introduced from 1 January 2023 include:

- shifting the Landings Target from the UK to Scotland only.;

- removing the option of demonstrating an economic link to Scotland on the basis of crew residence and vessel expenditure;

- a requirement for vessels to meet the landings target aspect of the licence condition by landing 55% of their total landings of 8 key species each year into Scotland;

- continuing to offer the option of quota gifting as an alternative means of meeting the licence condition but using a revised rate; and

- moving the qualification tonnage for economic link provisions from two to ten tonnes.

These amendments are expected to result in an increase in the volume of supply and a reduction in supply chain risks for Scottish sea fish processing and handling businesses, and therefore the potential to attract greater investment and employment in Scotland’s fishing industry. In the longer term it is expected they will contribute to the sustainable growth of the local economies where fishing is an important driver for business activity (e.g. the North East of Scotland and the Islands).

It is anticipated that the amendments will result in more quota being available for distribution and therefore the way that gifted quota received by the Scottish Government is allocated to the Scottish fishing fleet will also change. From January 2024, there will be more stakeholder engagement in the process of deciding how gifted quota will be allocated. We anticipate that this could include allocating beyond the 10 metre and under sector, to whom it is presently allocated.

2.1.1 Current licence condition

At present, Scottish sea fishing licences include a condition that requires vessels over 10 metres in length landing more than 2 tonnes of quota species annually to demonstrate a real economic link to the UK. The current licence condition allows licensees to demonstrate a real economic link to the UK in different ways including:

- Option A – Making 50% by weight of the total landings each year for all stocks subject to quotas into the UK;

- Option B – Having a crew half of which is made up of persons that normally reside in the UK;

- Option C – Spending at least half of the vessel’s operating expenditure (excluding crews’ wages) in the UK; or,

- Option D – by (i) a combination of two or three of the above options (the minimum percentage chosen for any one option may be less than 50% but the percentages chosen individually and in combination must genuinely provide a real economic link); or (ii) criteria other than the above options which genuinely provide a real economic link; in practice this option involves gifting quota back to the Scottish Government.

Generally, the quota that is gifted back to the Scottish Government in compliance with the economic link licence condition is distributed to the non-sector 10 metre and under fleet who make use of it to increase their catches or to fish for longer.

2.1.2 Proposed licence condition

In practice, compliance with the current economic link licence condition has been predominantly through landing above 50% of quota species into the UK, and for those vessels failing this, through the crewing condition or alternatively by gifting quota. However, Ministers have committed to increasing the economic and social returns to Scotland from fishing relative to what the current economic link licence conditions have delivered to date. Therefore, the Scottish Government consulted with stakeholders in 2017 on amending current economic link provisions. The consultation responses have been carefully examined and have informed analysis presented in this Business and Regulatory Impact Assessment (BRIA). It is the Government’s view that the proposal contained in this BRIA is the best way to increase the economic and social return from Scotland’s marine natural resources.

The new proposal streamlines the economic link licence condition and requires licence holders to either:

- Option A – land a minimum of 55% of their total annual landings of 8 key species (by tonnage) into Scotland (the landings target); or,

- Option B –gift quota back to the Scottish Government according to an updated quota gifting formula that presents a maximum that the Scottish Government (or other sea fish licensing authorities) can ask for (quota gifting).

It should be noted that following the consultation there has been a change to the proposed amendments to the economic link licence condition so that the Landings Target element of it will only apply to 8 key species (mackerel, herring, Nephrops, cod, haddock, hake, monkfish and whiting). This change was made in response to views expressed during the consultation that there is a lack of capacity and market for some species in Scotland, and that licence holders could have complied with the originally proposed Landings Target element of the policy by landing high quantities of low value species into Scotland while landing high value species (for which there is significant processing capacity for in Scotland) abroad. The key eight species identified account for around 70% of the tonnage and value landed anywhere by the Scottish Fleet. This change is likely to increase the likelihood of the policy objectives being achieved.

The economic link licence condition only applies to vessels which land more than a particular weight of quota species. Another change we have made to the proposed amendments is that the qualification criteria of two tonnes or more of quota species will increase to ten tonnes or more of the 8 key species. This means that the economic link licence condition will not apply to licence holders landing relatively small amounts of key species and vessels targeting non-quota stocks but landing incidental by-catch of key species (which they are required to land).

Under option B, the quota gifted to the Scottish Government will be allocated to the Scottish fishing fleet. After taking into consideration responses to the consultation, unlike current practice, gifted quota may now be allocated to groups other than the 10 metre and under non-sector vessels. In distributing gifted quota, the Scottish Government will:

- Distribute quota in line with the Fisheries Act 2020 thereby ensuring that gifted quota is distributed in accordance with the provisions of section 25 and in particular, using criteria that:

- Align with the Blue Economy initiative and be consistent with the Blue Economy Outcomes.

This BRIA presents the expected benefits and costs associated with the above proposal relative to the current arrangement. The counterfactual is therefore the situation whereby the economic link licence condition was not changed, in other words that it would continue to exist as set out in the “current licence condition” sub-section above.

2.2 Background

2.2.1 Catching sector

In 2021, provisional statistics indicate that the total tonnage of fish landed by Scottish vessels into the UK and abroad increased by 10% on 2020 figures to 437 thousand tonnes with the value increasing by 11% to £542 million.

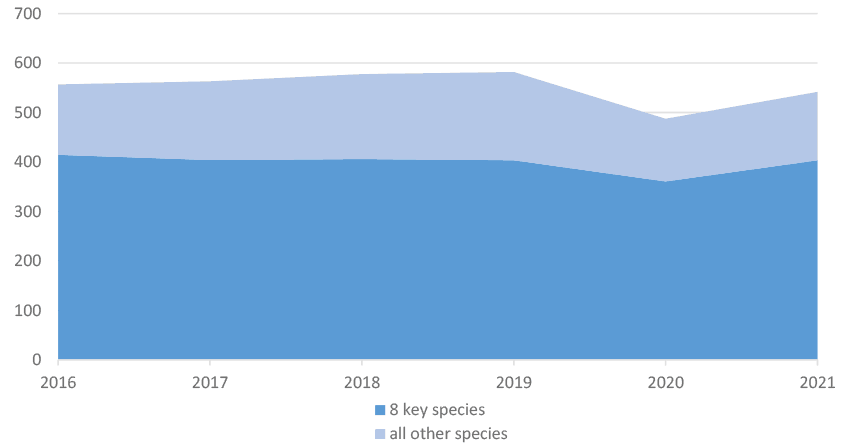

In 2021, provisional statistics indicate that the total tonnage of the 8 key fish species landed by Scottish vessels into the UK and abroad increased by 6% to 311 thousand tonnes (71% of total tonnes landed) with the value increasing by 12% to £403 million (74% of total value landed).

From 2016-2021, these 8 key species accounted for around 70% of total value and total tonnage landed by Scottish vessels anywhere. See Graph 1 for illustration of the value of landings.

Source: Marine Scotland Fisheries Statistics 2020 & provisional figures for 2021

Note: Figures for 2021 are provisional statistics

2.2.2 Landing patterns of the 8 key species

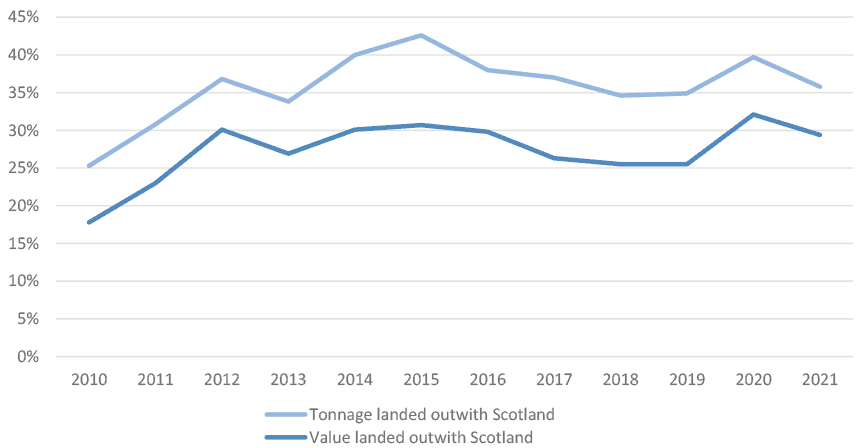

Provisional statistics indicate that landings of the 8 key species outwith Scotland accounted for 36% of all landings by Scottish vessels in terms of tonnage and 26% in terms of value in 2021. Of this, 98% of the tonnage of landings outwith Scotland were pelagic, two% were demersal and Nephrops. Graph 2 below shows that Scottish vessels have increased the proportion of tonnage and value of their catch that is landed abroad over the past twelve years, albeit the majority of the shift was from 2010 to 2012.

Source: Marine Scotland Fisheries Statistics 2020 & provisional figures for 2021

Note: Figures for 2021 are provisional statistics

Provisional statistics indicate that in 2021, the main species landed outwith Scotland was mackerel, 100 thousand tonnes with a value of £101 million, as shown in Table 1. This is 82% of the total tonnage of landings abroad of the 8 key species, and 85% of total landings value abroad of the 8 key species. In addition, this was 54% of the total tonnage and 52% of the total value of mackerel landed by Scottish vessels. In 2021 the average price for mackerel landed into Scotland was £1,116 per tonne and the average price for mackerel landed abroad was £1,011 per tonne, in contrast to previous years when prices achieved in Norway were higher than prices achieved in Scotland.

| Species | Value (£000s) | Tonnage |

|---|---|---|

| Pelagic | 114,108 | 119,398 |

| mackerel | 101,226 | 100,269 |

| herring | 12,883 | 19,129 |

| Demersal | 2,594 | 1,651 |

| cod | 407 | 142 |

| haddock | 154 | 154 |

| hake | 672 | 336 |

| monk | 996 | 661 |

| whiting | 363 | 357 |

| Nephrops | 1,912 | 690 |

| Total landings | 118,613 | 121,739 |

Note: Figures for 2021 are provisional statistics

The majority of landings outwith Scotland were made into Norway and nearly all of these were pelagic species. In 2021, 86% of the value of landings into Norway was for mackerel, amounting to 89 thousand tonnes with a value of £82.8 million. Only 0.7 thousand tonnes of Nephrops were landed outside of Scotland by Scottish vessels, mainly into England, Northern Ireland, and the Republic of Ireland. While 1.7 thousand tonnes of the demersal species within the 8 key species were landed outwith Scotland with a value of £2.6 million, mainly into the Republic of Ireland and Denmark.

The licence holders not meeting the current economic link requirement to land 50% by total annual weight of quota stocks into the UK is generally small in number (See Table 2 below). In 2021, only 20 vessels out of a total of 410 vessels over 10m in length failed to meet the requirement. However, these 20 vessels land considerable quantities of fish with a high economic value abroad – around £96 million in 2021. In 2021, 12 of the 20 vessels met the economic link condition through their UK resident crew and 8 by providing quota gifts in lieu of not meeting the 50% landings target.

| Year | Number of vessels failing to meet a 50% landings threshold into Scotland | Tonnage landed abroad, tonnes | Value landed abroad, £millions |

|---|---|---|---|

| 2013 | 27 | 103,478 | £88m |

| 2014 | 23 | 173,952 | £125m |

| 2015 | 25 | 142,971 | £91m |

| 2016 | 19 | 124,337 | £113m |

| 2017 | 24 | 142,061 | £104m |

| 2018 | 20 | 114,048 | £92m |

| 2019 | 21 | 108,040 | £91m |

| 2020 | 20 | 96,319 | £86m |

| 2021 | 20 | 113,115 | £96m |

Note: Data for 2021 is provisional

2.2.3 Processing sector

In 2021 there were 128 seafood processing sites operating in Scotland, providing 7,800 Full Time Equivalent (FTE) jobs according to the Seafish processing survey. Scottish seafood processing represents approximately 37% of the sites in the UK and 43% of the jobs. Between 2012 and 2021, there was a 14% fall in employment in the Scottish seafood processing industry. In Scotland, seafood processing is concentrated in North Eastern Scotland where there are 48 sites which generate an estimated 43% of Scotland’s seafood processing jobs.

Since 2012, Scotland as a whole has experienced around a 25% decline in the number of seafood processing sites, with the UK overall seeing a 17% decline in the number of sites. Concurrently, there has been a 7% decrease in FTE jobs in the North Eastern Scotland area, compared with a 14% decrease in Scotland and a 10% decrease in the UK overall. The national trend observes the decline principally in companies with 25 or fewer employees. There has also been a shift away from primary processing, which focuses primarily on cutting and washing the fish, towards secondary or mixed processing units, which include smoking and canning the fish.

The Scottish seafood processing industry has seen turnover fall by 15% in real prices between 2012 and 2018, but saw gross value added, the measure of the value of goods and services produced in an area, industry or sector of an economy, (GVA) stay generally stable and even increased in 2018 suggesting the industry is improving efficiency despite the decrease in throughput.

Anecdotally, Scottish sea fish processors tend to trade in pound sterling, while other countries trade in US dollars. This makes Scottish processors especially exposed to pound sterling exchange rate volatility, which, coupled with low margins, can have a particularly large impact.

As 98% of the tonnage of landings outwith Scotland in 2021 were pelagic fish, the change to the economic link licence condition will primarily effect pelagic processors. In 2021, data from Seafish shows that there were 5 Scottish processing sites handling pelagic fish only; and an additional 40 Scottish processing sites handling mixed fish, including pelagic fish. At the 5 processing sites that handle pelagic fish only, employment stands at 524 in 2021; employment has more than halved since 2014.

The key economic characteristics of Scotland’s fish processing sector by type of fish processed can be found in the Appendix A.

2.3 Objectives

The proposal to change the economic link licence condition was reaffirmed in the Programme for Government 2020-2021 to address 1) the significant proportion of tonnage which continues to be landed abroad by Scottish vessels (Graph 2) and, 2) the challenging headwinds faced by the Scottish sea fish processing sector and in particular, the lack of a guaranteed supply.

In introducing a new Scottish economic link licence condition, the objectives of the Scottish Government are to increase the volume of valuable fish stocks landed in Scotland so that it:

- supports the long term, sustainable growth of local economies where fishing is an important driver for business activity (e.g. Peterhead, Fraserburgh, and Shetland) by increasing the volume and regularity of the supply of fish landed and available to process in Scotland;

- attracts greater investment and employment in Scotland’s fishing industry by reducing supply chain risks for Scottish fish processing and handling businesses; and

- brings greater social and economic benefits to Scotland from a Scottish national resource by spreading the benefit arising from fishing quotas more widely through fishing communities

2.4 Rationale for Government intervention

Prior to the consultation on proposed changes to the economic link licence condition in 2017, Scottish Government officials and the then Cabinet Secretary for the Rural Economy engaged with industry to establish if increased landings of pelagic species (which account for the majority of landings abroad) could be achieved without the need for regulatory change. This proved unsuccessful and it was concluded that Government intervention would be required for the following reasons:

2.4.1 Foregone benefits to the local economy by landing abroad.

A fishing vessel will generate economic benefits in its home port, such as through vessel maintenance works and crews’ wages being spent. This can be substantial. However, wherever a fishing vessel lands its catch, i.e. the landing port, it brings with it substantial economic activity. This can be in the form of port operators handling the catch, haulage and processing. The current economic link licensing arrangements have undoubtedly resulted in economic benefits from fish quotas and fishing activities being retained in the UK as a majority of Scottish vessels land their catch into Scotland. However, as set out above, there is the potential to increase those benefits given the significant amount of catch being fished against Scottish quotas which continues to be landed abroad as licence holders can currently opt to comply with the economic link licence condition via the crewing requirement. These landings represent a lost economic opportunity for Scotland’s coastal communities in the form of jobs and earnings, as the benefits of jobs related to landing and processing these fish, along with the supporting businesses, are greater than the benefits gained through the vessel crewing requirement. The prospect of landing and processing these catches within Scotland would allow a larger proportion of the full value chain to be captured resulting in Scotland achieving greater value from this national resource.

Therefore, the Scottish Government is of the view that the economic contribution made by the Scottish fishing industry to local economies where seafood industries are significant could be enhanced by strengthening incentives to land catches into Scotland. Fishing and related industries provide jobs in many coastal areas of Scotland so an increased supply of fish has the potential to stimulate economic growth, attract investment and increase employment. This economic growth could be from increased landings as well as from the availability of additional quota from quota gifting which will be allocated, alongside other criteria, on the basis of securing economic benefits to Scotland’s coastal communities.

2.4.2 To support the growth of Scotland’s processing sector.

Scotland’s fish processing sector cites insufficient volume and irregularity of supply (supply chain risks) among the key constraints to its growth. By tackling these constraints, the Scottish Government’s proposed changes to the economic link licence condition has the potential to result in the growth of Scotland’s fish processing sector. In the long term, this change could more widely distribute the economic benefits from Scotland’s fish resources, especially in coastal communities where fishing is a relatively important driver for economic activity.

2.4.3 National Outcomes

The proposal presented aims to tackle the issues highlighted above, using the rationale and objectives as set out. The proposal is expected to help deliver the following National Outcomes:

- We have a globally competitive, entrepreneurial, inclusive and sustainable economy.

- We live in communities that are inclusive, empowered, resilient and safe.

- We value and enjoy our built and natural environment and protect it and enhance it for future generations.

- We tackle poverty by sharing opportunities, wealth and power more equally.

We have thriving and innovative businesses, with quality jobs and fair work for everyone.