Future of council tax in Scotland: consultation

This consultation seeks views on how Scotland’s council tax system could be made fairer and more up to date. It explores illustrative models such as revaluing properties, adjusting tax bands and introducing protections to help households manage any changes to their bills.

Closed

This consultation closed 30 January 2026.

View this consultation on consult.gov.scot, including responses once published.

4. Transition and Mitigation

4.1 Why Transition Mechanisms Matter

Major changes to council tax can result in noticeable increases in bills for some households, especially in areas where property values have risen significantly since the last valuation.[63] Transitional relief schemes, or "soft landing" measures help give people time to adjust and ease households into the changes.

It recognises that while reform may be equitable overall, a large one-off bill increase can be difficult for some households to absorb. Transitional relief schemes have been used in other parts of the UK to protect households during revaluations. These experiences show that well-designed transition schemes can reduce short-term disruption while still achieving long-term policy goals.[64]

People may be more willing to support long-term improvements if they are reassured that any changes will be introduced gradually.

There is a trade-off between the scale of the support provided and how much it costs. More protection means more households receive help – but it also increases the overall cost of the scheme.

Questions:

8. Do you support the establishment of a transitional relief scheme to limit how much a household’s council tax bill can increase each year following reform?

Yes

No

Don’t know

4.2 Phasing In Changes to Bills

A common approach to transition mechanisms is to limit how much a household's bill can rise each year. This means that people who face the highest increases in their bill under a new system would not need to pay the full increase straight away. The two example schemes below have been modelled by the IFS to show how this might work.[65]

Both options assume that the cap on increases would apply to the gross council tax bill before any discounts (like the single person discount), premiums, exemptions, or Council Tax Reduction (CTR). For those receiving discounts, this means the cap would effectively be lower in cash terms.

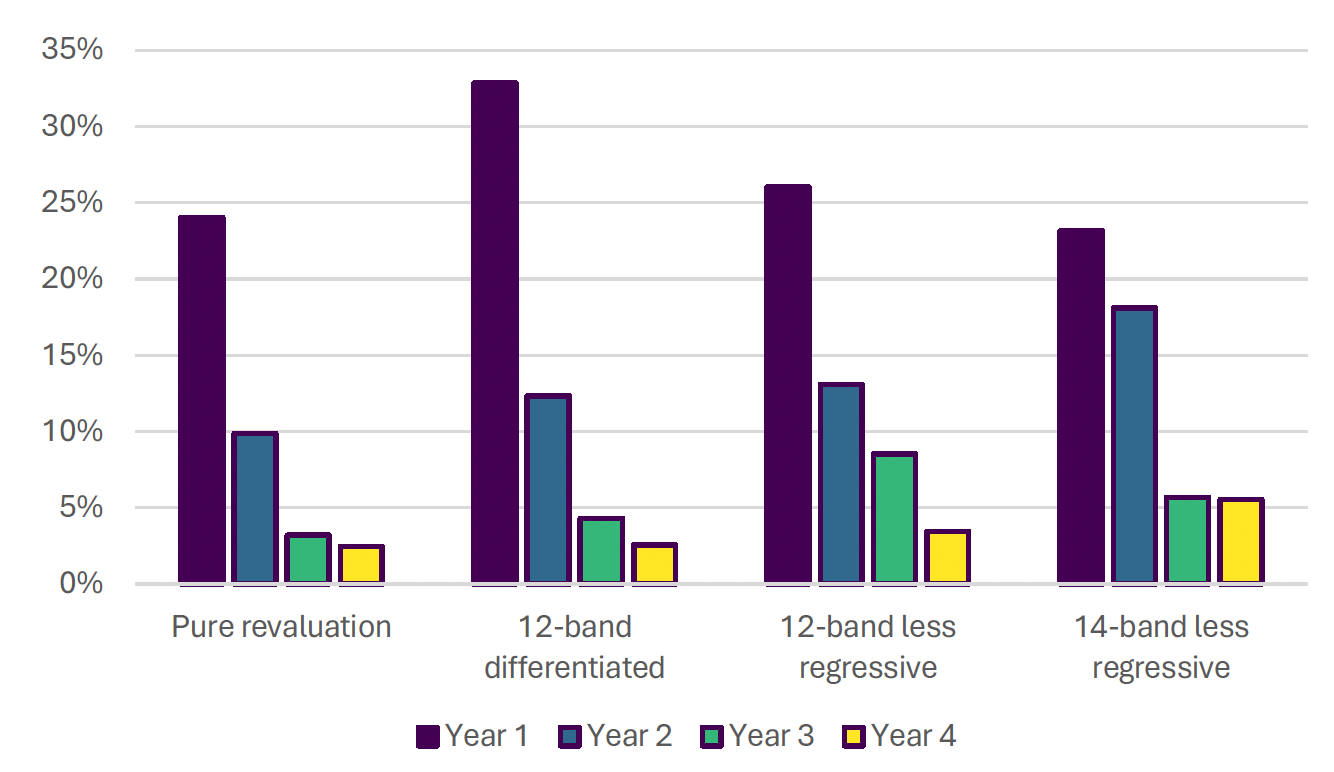

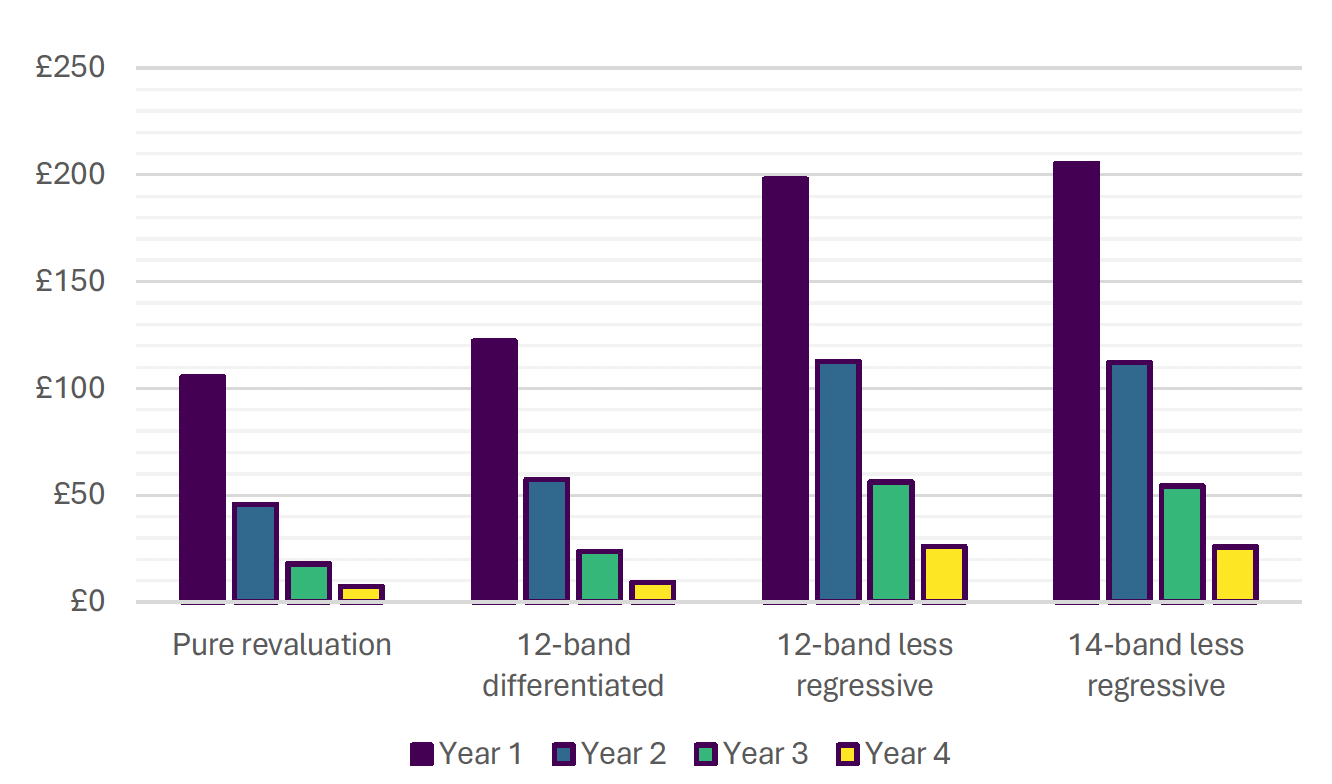

4.2.1 Scheme 1: Cap Increases at 10% or £300 Per Year

This approach would offer the most protection. Under this scheme, council tax gross bill increases due to the reforms would be limited to the lower of 10% or £300 each year, over four years.

This would protect the largest number of households. For example, under a pure revaluation, around 24% of all properties would be estimated to receive some form of transitional relief in the first year. That number could be higher under some of the other reform options. A small number of households would be estimated to continue to benefit from phased increases until the fourth year.[66]

Because more people are protected and for longer, this scheme would also be more expensive. In year one, the estimated costs range from £100 million (for a simple revaluation) to £200 million for reforms that introduce more bands and make the system less regressive. Even by year four, estimated annual costs could still be around £25 million under these more extensive reforms.[67]

Source: Adam et al. (2025), ‘Revaluation and reform of council tax in Scotland: design considerations and potential impacts’, Scottish Government Research Report

Source: Adam et al. (2025), ‘Revaluation and reform of council tax in Scotland: design considerations and potential impacts’, Scottish Government Research Report

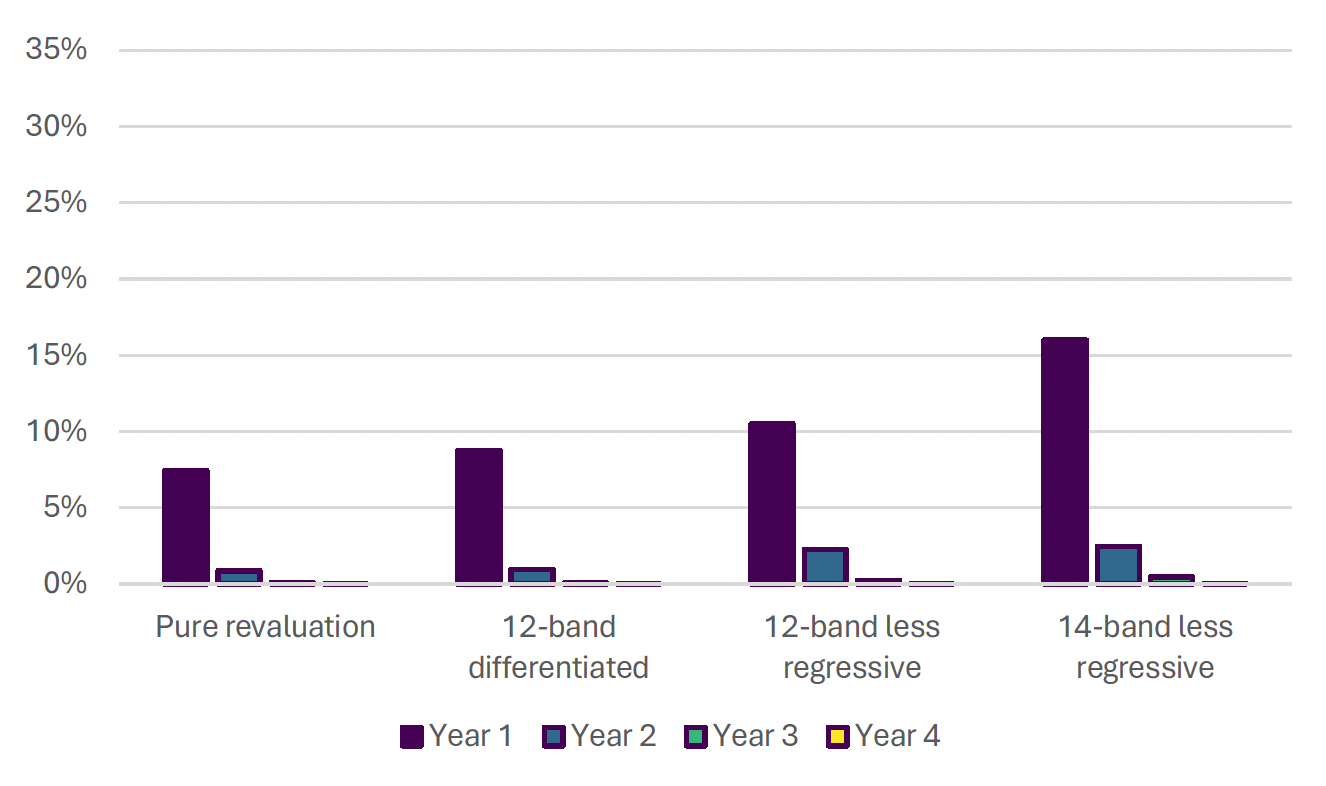

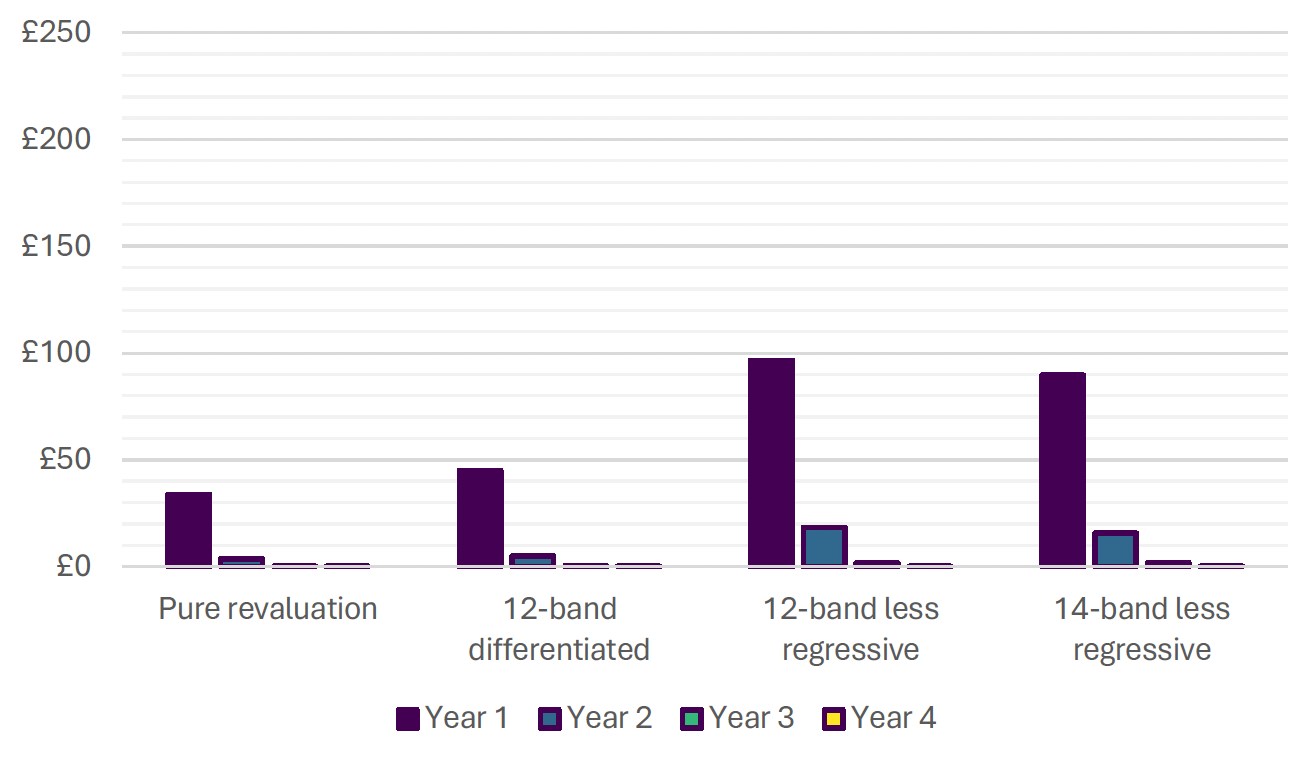

4.2.2 Scheme 2: Cap Increases at 25% or £600 Per Year

This option would offer a faster path to full implementation if a reform goes ahead, with less financial protection for households and lower costs.

Under this scheme, bill increases would be capped at the lower of 25% or £600 per year, over four years. Fewer people would receive transitional relief, with support targeted at those facing the biggest increases.

For example, under a pure revaluation, an estimated 7% of households would be protected in the first year, and the cost would be just over £50 million. By year four, it is estimated that fewer than 0.1% of households would still need support under this scheme.[68]

Source: Adam et al. (2025), ‘Revaluation and reform of council tax in Scotland: design considerations and potential impacts’, Scottish Government Research Report

Source: Adam et al. (2025), ‘Revaluation and reform of council tax in Scotland: design considerations and potential impacts’, Scottish Government Research Report

4.2.3 Who Benefits from Phasing?

Transitional relief would benefit different types of households depending on the option chosen:

- Scheme 1 would support a broader group, including households who face smaller but still significant increases. By virtue of having a wider scope, and capturing more recipients it is likely to include more low and middle value properties than scheme 2.[69]

- Scheme 2 would be more targeted, helping those facing the largest jumps in bills, such as those moving up two or more bands. It would focus support on a smaller group, who are more likely to be those in high-value homes in areas where prices have risen sharply.[70]

Both schemes would likely benefit owner-occupiers more than renters, and households who are not already receiving full support through the Council Tax Reduction scheme[71].

4.2.4 Advantages and Disadvantages of Phasing

Advantages:

- It helps provide a gradual introduction for reform, particularly for those with the larger bill increases.

- It offers temporary financial protection for households.

- A scheme with a lower cap can protect more households

- A scheme with a higher cap is less costly.

Disadvantages:

- It adds complexity in terms of design, administration and communication of the system.[72]

- It requires funding – either from grants, higher bills for others, or higher tax rates.

- A scheme with a lower cap is more costly.

- A scheme with a higher cap will protect fewer households.

The choice of whether to use a transitional relief scheme, and which version to use, depends on the balance between providing support and managing cost. These models are illustrative only, but show the kinds of trade-offs involved.

Questions:

9. Which transitional relief scheme would you prefer?

Scheme 1: Cap increases at 10% or £300 per year

Scheme 2: Cap increases at 25% or £600 per year

Other, please specify [50 words maximum]

Don’t know

4.3 Deferral of Increases

A deferral scheme would allow some households to delay paying the extra council tax they owe as a result of reform. Instead of paying the full increase straight away, they could postpone part or all of it until a later date; for example, when the home is sold or after a fixed number of years.

This could help people who own their homes but have lower incomes. For example, pensioners, disabled people, or families with children may find it difficult to pay a higher bill even though they have housing wealth.

Unlike transitional relief, which reduces the amount paid in early years, deferral only delays payment. The tax is still due in full later – potentially with interest – and so the deferred council tax income and associated costs of deferring, would be expected to be recovered in future years.[73]

4.3.1 How a Deferral Scheme Could Work

The scheme would allow households to treat the extra amount owed due to revaluation or banding changes as a loan. This loan would be recovered later — usually when the property is sold or transferred to someone else.

This kind of approach already exists in other countries, including Ireland and Canada.[74]

To work well, the scheme would need to be carefully designed. Some of the key choices include:

- Who is eligible: The scheme would likely be limited to owner-occupiers with enough equity in their property. Some mortgage holders might not be eligible depending on their mortgage terms.[75]

- How much can be deferred: The scheme might allow deferral of just the increase from reform, or allow full deferral of the total bill for eligible households.

- How long it lasts: Deferred bills could be paid when the home is sold, after a fixed number of years (like five or ten), or on the death of the owner.

- Whether interest is charged: To cover costs and avoid enriching those on the scheme, interest could be added to the deferred amount.

- Who manages it: Councils would likely run the scheme, as they already do for similar arrangements for social care charges.[76]

4.3.2 Supporting Asset-Rich, Income-Poor Households

There are a range of homeowners who could potentially benefit from a deferral scheme, including, for example, older people, long-term homeowners, or families who do not qualify for full Council Tax Reduction. They may live in homes that have risen in value, but their income has stayed the same or fallen.

Details of criteria that have been used for similar schemes in other countries can be found in section 6.2 of the following research report: Revaluation and reform of council tax in Scotland: design considerations and potential impacts.

Deferral would allow ‘income-poor, asset-rich’ households to stay in their homes without extra financial strain. The tax would still be paid eventually, often from the sale of the home.

| Household Criteria | Pure Revaluation | 12-band Differentiated | 12-band Less Regressive | 14-band Less Regressive |

|---|---|---|---|---|

| Owner-occupier and not eligible for full CTRS | 250,000 | 250,000 | 260,000 | 360,000 |

| Additional criteria | No data | No data | No data | No data |

| (1) At least one adult above State Pension Age | 80,000 | 80,000 | 80,000 | 120,000 |

| (2) Satisfies (1) or at least one individual in receipt of health-related benefits | 90,000 | 90,000 | 90,000 | 140,000 |

| (3) Satisfies (1) or (2) or at least one child | 150,000 | 140,000 | 150,000 | 210,000 |

A table showing number of households facing an increase of over £300 in their annual net council tax bill and satisfying various household criteria

Source: Adam et al. (2025), ‘Revaluation and reform of council tax in Scotland: design considerations and potential impacts’, Scottish Government Research Report

Modelling estimates that up to 360,000 households, about 14% of all households in Scotland, could be eligible under a broad scheme. The number would depend on how the scheme is designed:

- It is estimated that around 250,000 households might qualify if eligibility is based on being an owner-occupier, not receiving full CTR, and facing a net bill increase of over £300.

- If eligibility is limited to people over state pension age, it is estimated that the number of eligible households could drop to about 80,000.

- If families with children and those receiving disability benefits are also included, the number of eligible households would be expected to increase.[77]

4.3.3 Repayment Conditions and Triggers

The deferred amount would be repaid later, usually from the sale of the home. Other possible repayment points could include:

- After a fixed number of years (e.g. five or ten).

- When the final resident dies.

- If the homeowner chooses to repay early.

The deferred bill may be subject to interest, to reflect the cost of borrowing. For example, Ireland charges 3% interest[78], and British Columbia charges between 3.45% and 5.45% depending on the household type.[79]

Any interest rate applied to deferred council tax can be set to strike a balance between offering financial security for households and ensuring the long-term sustainability of the scheme for public finances:

For households, a clearly defined and reasonable interest rate provides certainty about the future cost of deferral, making it easier to plan and reducing the risk of unmanageable debt.

Setting the rate too low could create an incentive for households to defer unnecessarily, increasing the cost to the public purse.

Conversely, setting it too high could discourage take-up among those who genuinely need support. The rate, therefore, plays a key role in making the scheme both accessible for households and financially viable for government:

- A lower rate subsidises deferrals, increasing costs to the public purse and potentially encouraging take-up by households who do not genuinely need the support.

- A higher rate helps recover more of the costs to local authorities and discourages households who do not need the support from applying. However, it also risks deterring households who do need support or leaving them with larger debts to repay.

To keep the scheme affordable and low-risk, there could also be a limit on how much can be deferred. For example, British Columbia limits total charges against a home to 75% of its official valuation.[80]

A well-designed deferral scheme could support vulnerable households during the transition to a new system, without reducing the total amount of tax collected over time.

Questions:

10. Do you support the establishment of a council tax deferral scheme for homeowners?

Yes

No

Don’t know

11. In your view, who should be eligible to receive support from a council tax deferral scheme?

[Select as many as you think should apply]

Pensioners (over state pension age)

Disabled people

Households with children

Households experiencing financial hardship

Other, please specify [50 words maximum]

Don’t know

12. Should households who defer payment pay interest on the amount deferred?

Yes

No

Don’t know

4.4 Council Tax Reduction (CTR) Scheme

4.4.1 The Role of CTR in Council Tax Reform

The Council Tax Reduction (CTR) scheme provides means-tested financial support to low-income households to help reduce their council tax bill. For many of these households, CTR already ensures that they pay little or no council tax, meaning they would be protected from any direct impact of reform.[81]

However, some households, particularly those just above the CTR eligibility threshold, could see their bills increase under a reformed system. This makes CTR an important part of any reform package, both as a form of ongoing support and as a way to protect household budgets where affordability might otherwise be a concern.

4.4.2 Existing and Targeted CTR Support

When changes were made to the council tax system in 2017 – which increased the charges in Bands E to H - targeted CTR support was introduced for low-income households in Bands E to H. This allowed eligible households to continue paying lower rates.[82] A similar approach could be applied under reformed systems, particularly where households move into higher bands due to changes in property values.

CTR could be extended to provide targeted support to those in higher-value properties who meet certain income criteria. This would help limit large increases in council tax liability for lower-income households, while allowing structural changes to the tax system to proceed.

| Council tax system | Number of households entitled | Annual cost under full take-up (£ millions) |

|---|---|---|

| Current system | 13,000 | 2.6 |

| Pure revaluation | 17,000 | 3.3 |

| 12-band differentiated | 12,000 | 4.6 |

| 12-band less regressive | 18,000 | 6.4 |

| 14-band less regressive | 19,000 | 4.4 |

A data table showing number of households entitled to, and cost of, Band E–H CTR scheme under full take-up

Source: Adam et al. (2025), ‘Revaluation and reform of council tax in Scotland: design considerations and potential impacts’, Scottish Government Research Report

4.4.3 Expanding the CTR Scheme More Broadly

Reform also creates an opportunity to review the broader design of the CTR scheme itself, particularly for those who are close to the eligibility threshold but not currently supported. One option would be to reduce the taper rate. This is the rate at which support is withdrawn as income rises.

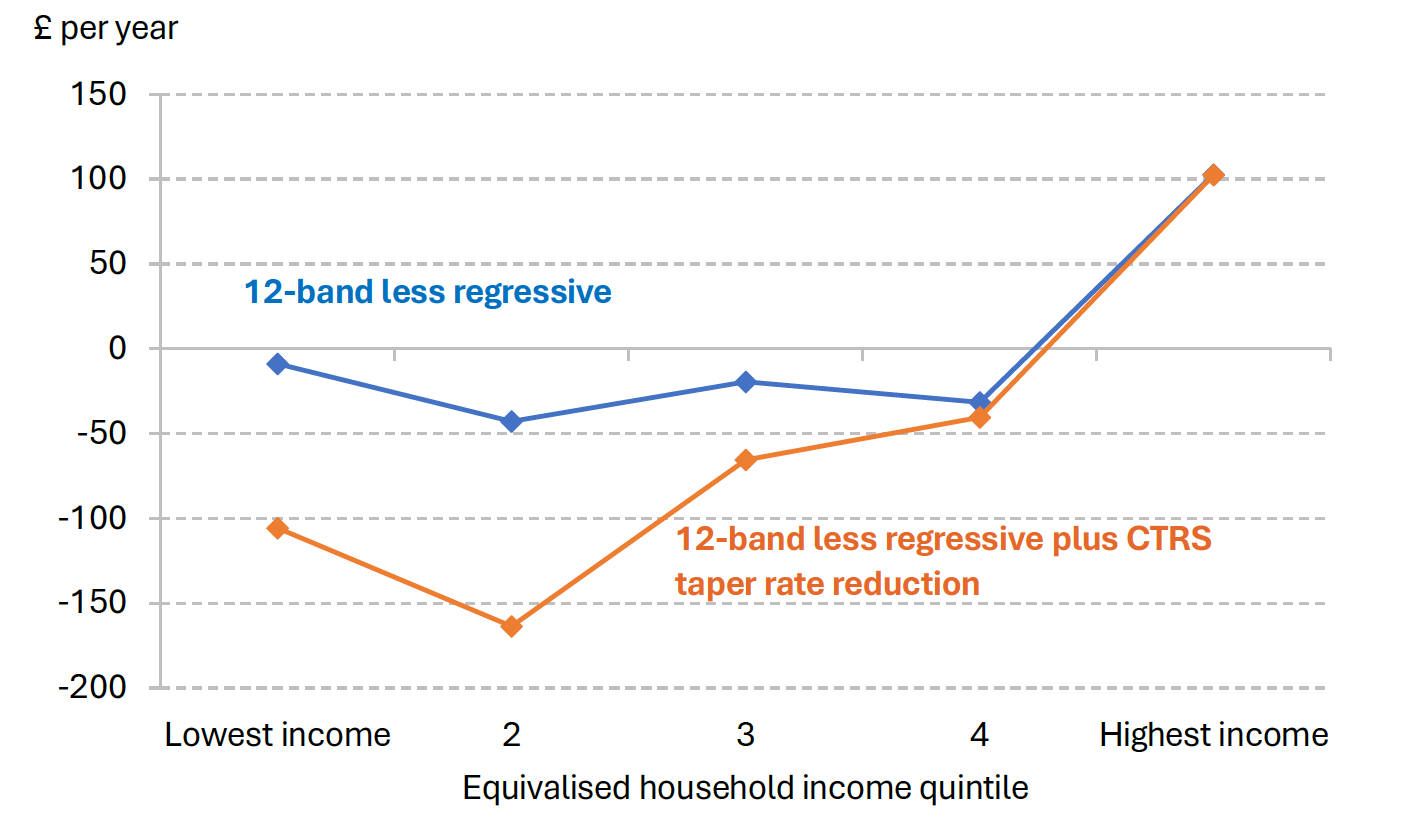

For example, it is estimated that halving the taper rate[83] from 20p to 10p per £1 of additional income would extend support to between 400,000 and 500,000 households, at an estimated cost of between £130 million and £150 million per year. It is estimated that around half of these households would be newly eligible under the lower taper rate, with the rest seeing increased support. According to modelled estimates, the number of households entitled to CTR could rise from around 25% to 35% of all households in Scotland.

Figure 19 below shows the illustrative impact of reducing the CTR ‘taper rate’ on progressivity of the system. With a reduced taper, bills rise with income quintile.

Note: Assumes full take-up of CTRS. Households are allocated to quintiles based on income measured after taxes and benefits but before housing costs are deducted, and are adjusted for household size and composition using the modified OECD equivalence scale.

Source: Adam et al. (2025), ‘Revaluation and reform of council tax in Scotland: design considerations and potential impacts’, Scottish Government Research Report - Authors’ calculations using Understanding Society waves 8-10 and 14 and TAXBEN, the IFS tax and benefit microsimulation model.

4.4.4 Considerations for Reform

Expanding CTR would help ensure that low- and modest-income households are better supported during and after reform. However, there are important design and delivery considerations:

- Take-up rates: Any changes would need to be supported by clear communication, streamlined application processes, and awareness campaigns.

- Administrative complexity: Changes that introduce more variation, such as different rules based on income level, age, or location, could increase costs and make the system harder for both councils and residents to navigate.

- Interaction with other support mechanisms: CTR is one part of a wider support package. Its effectiveness depends on how it works alongside other tools, such as transitional relief and deferral.

The Scottish Government and COSLA welcome views on whether the current CTR scheme should be expanded or adjusted, and which groups of households most need additional support under a reformed system.

Questions:

13. Do you think the Council Tax Reduction scheme should be expanded to support more households following any reform?

Yes

No

Don’t know

14. Which changes to the Council Tax Reduction scheme would you support? [Select as many as you think should apply]

Broaden eligibility criteria for CTRS to include low-income households where the property moves into a higher band due to council tax system changes

Change CTR so support is withdrawn more gradually as rising incomes move individuals out of eligibility

No changes needed

Other, please specify [50 words maximum]

Don’t know

Contact

Email: LocalTax@gov.scot