Council Tax High-Value Property Bands (Mansion Tax): consultation

This consultation seeks views on the proposed rates for two new High-Value Property Council Tax Bands ("Mansion Tax"). Band I for residential properties valued between £1 million and £2 million, and Band J for residential properties valued at more than £2 million.

Open

29 days to respond

Respond online

4. Illustrative Rates and Revenue

4.1 Band I and J Council Tax Rates

Council Tax charges are not set as fixed annual amounts. Instead, each band is assigned a multiplier – a fixed ratio relative to Band D – that is set in legislation. Each local authority then sets its own Band D rate annually, and the charges for all other bands are calculated automatically from that figure using the legislative multipliers.

This means the actual Council Tax bill for a Band I or Band J property will vary between council areas, just as bills for Bands A to H vary today. The multipliers determine the relative charge; the absolute amount depends on where the property is located.

For context, Figure 1 in Section 2.1 sets out the current multipliers for Bands A to H. Band H currently carries a multiplier of 2.45 relative to Band D. This means that in a local authority area, a Band H property pays 2.45 times the amount paid by a Band D property (e.g. where a Band D property currently pays £1,653, a Band H pays 2.45 times that charge and therefore has an annual liability of £4,051).

The tax rates (multipliers) for Band I and Band J will be set through primary legislation and will be higher than the current Band H multiplier, reflecting the higher values of the properties in those bands.

4.2 Illustrative Rates

The rates below are illustrative. They are intended to provide respondents with a concrete basis on which to form and share their views. They do not represent final or proposed rates. Final multipliers for Band I and Band J will be set through primary legislation, informed by the responses to this consultation, engagement with local government, and consideration by the Scottish Parliament.

The illustrative tax rates (multipliers relative to Band D) that are being explored are approximately:

- 2.886 for Band I - equivalent to an annual charge of around £4,770 (based on 2026-27 Band D charges).

- 4.628 for Band J - equivalent to an annual charge of around £7,650 (based on 2026-27 Band D charges).

This means that, compared to the average Band H charge, it is estimated that:

- Band I properties (valued between £1 million and £2 million) would pay around £720 more per year than the Band H.

- Band J properties (valued at over £2 million) would pay around £3,600 more per year than the Band H.

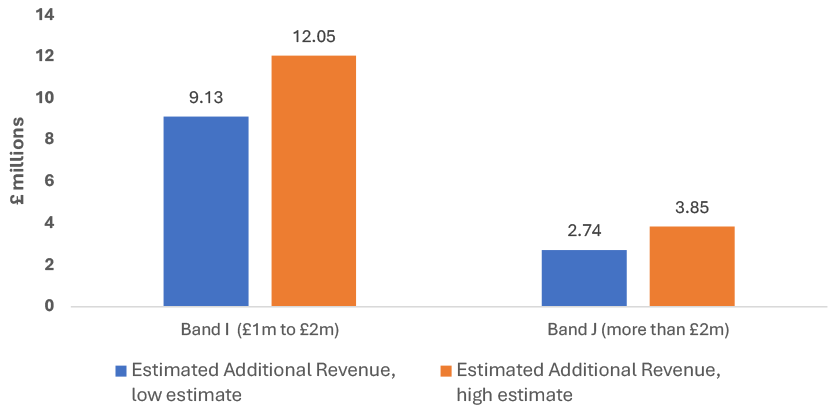

As set out in Figure 2, on the basis of these illustrative rates, the new bands are estimated to raise between £12 million and £16 million per year in total across Scotland. This additional revenue would be retained by Local Government.

Figure 2: Estimates of additional annual revenue from Bands I and J

Source: Illustrative Scottish Government estimates based on Records of Scotland data, CTAXBASE statistics and analysis by the Institute for Fiscal Studies

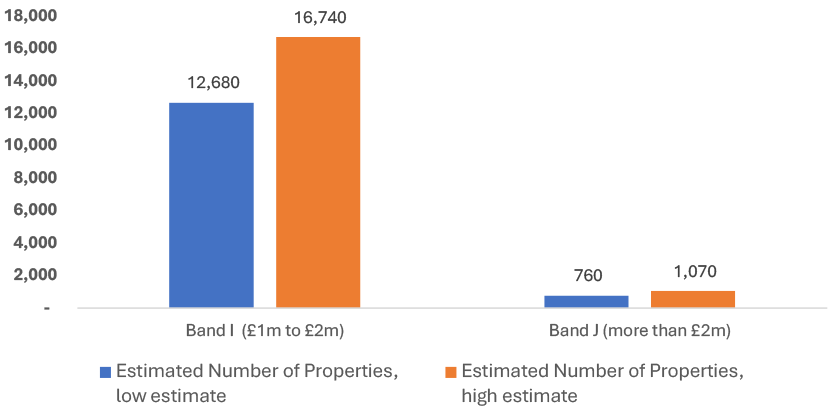

Figure 3: Estimates of number of properties in Bands I and J

Source: Illustrative Scottish Government estimates based on Records of Scotland data, CTAXBASE statistics and analysis by the Institute for Fiscal Studies

4.3 Geography and Distribution

High-value properties are not evenly distributed across Scotland. They are concentrated in particular parts of the country, including in and around Scotland’s cities and in certain rural areas. The proportion of properties likely to fall within Band I or Band J will therefore vary considerably by council area. Further, any property may move into Band I and J from any existing Band (A to H) providing the property is worth more than £1 million as at 1 April 2026.

This variation has implications for the distribution of additional revenue between councils. As noted above, the allocation of that revenue will be agreed with COSLA through established governance processes. Views on this, and on how the geographic concentration of high-value properties may affect households and communities in different parts of Scotland, are welcome as part of responses to this consultation.

Contact

Email: LocalTax@gov.scot