Assessment of electrolysers: report

An assessment into the state of electrolyser manufacturing globally, to support an understanding of the supply chain opportunities in Scotland.

4. Opportunities for Scotland

Based on the assessment of the capabilities required for the manufacture and deployment of electrolysers, it is clear there are potential opportunities for Scotland to capitalise on the expected growth in the global electrolyser market. There are several key areas that can be developed to help make Scotland an attractive place for companies to locate and develop in-house supply chain capabilities. This section gives an overview of these areas and highlights some of the steps that can be taken to support a strong electrolyser supply chain in Scotland.

4.1 Strong demand pipeline

Companies in the electrolyser supply chain will look for a positive pipeline of electrolytic hydrogen projects as they scale up, to ensure stable market conditions and de-risk investment. The Scottish Hydrogen Policy Statement and draft Hydrogen Action Plan provide a clear ambition to install 5GW hydrogen capacity by 2030 and 25GW by 2045, with £100 million in funding committed to developing the hydrogen economy. This government backing of the hydrogen sector helps to signal certainty to investors that the hydrogen market in Scotland is set to grow and stimulates the market. Clear and ambitious hydrogen targets and supporting policy will enable Scotland to maintain its position in a fast-moving global market and differentiate itself from competitors.

Another advantage is the surplus of renewable electricity production in Scotland providing a strong pipeline of demand. The ScotWind offshore leasing round alone will add nearly 25GW of new offshore wind capacity, in addition to an 8-12GW onshore wind target, 1.5GW hydro power and a developing wave and tidal sector. Coordinating hydrogen generation projects with increased renewables capacity is a challenge, therefore having a confirmed pipeline provides a huge opportunity for Scotland to lead the way with renewable-powered hydrogen production.

A policy decision on using hydrogen for heating is expected in 2026, by which point Scotland will have several leading demonstration projects underway to provide an evidence base. This includes providing hydrogen to homes at H100 in Fife and testing hydrogen blending in the gas grid in Aberdeenshire. This experience in demonstration and evidence building means Scotland will have a strong knowledge and skills base in hydrogen production, transportation and use. This can be utilised to quickly scale a large demand base should hydrogen for heating be approved. In addition, Scotland's cities have been early adopters of hydrogen technology, for example hydrogen buses in Aberdeen, and therefore will be better prepared to scale up to provide a demand base at a commercial scale.

The combination of a strong demand pipeline, supportive policy/funding and experience in demonstration projects will make Scotland an attractive location for electrolyser OEMs. The innovative nature of many OEM companies means a supportive market that is de-risked as much as possible will be a key factor in deciding which countries to locate in. In addition, for OEMs that are entering the market, funding and/or support mechanisms deployed at speed is key to enable the companies to scale and gain a market share ahead of international competitors.

This strong demand profile should see Scotland develop significant competency in the servicing and maintenance of electrolysers. Generic system components, such as water and electrical components, could be readily manufactured within Scottish supply chains. This could limit the risk associated with the import of these parts if there was to be a system failure. A local supply chain could reduce the downtime and costs for electrolysers deployed in Scotland. To support the transition of companies that manufacture these components, training will be required for the supply chain.

4.2 Transferable skills and capabilities

As described in Section 3.3, Scotland has a wealth of skills and experience across oil and gas, offshore operations, manufacturing, engineering, chemicals processing and industrial research. All these skill areas can be applied the hydrogen supply chain. Business skills such as collaboration, project management, procurement and safety will also be highly transferable.

According to Skills Development Scotland, there were 76,000 people working in the energy sector in 2021[25]. The majority of people working in the energy sector in Scotland are based in Aberdeen city and Aberdeenshire, which is a leading the energy transition from its oil and gas operations. Additionally, 30% of the UK's Offshore Wind workforce is currently based in Scotland and is set to increase significantly as more offshore windfarms are developed and built.

There is opportunity to tap into Scotland's existing skills base to develop the hydrogen supply chain, which can have additional benefits ensuring a just transition from traditional energy sectors such as oil and gas. It will be important to ensure the transfer of skills is demand-led through a strong pipeline of projects and that strong collaboration is had across sectors to assess needs and gaps.

4.3 Supply chain innovation

As the electrolyser manufacturing industry grows, cost-competitive and efficient supply chains will be key for OEMs. Scotland has a strong track record on innovation within the developing hydrogen sector, and there is opportunity to continue with this for the electrolyser supply chain. Investment in areas such as automation, sustainable materials, recycling and efficiency improvements will be valuable to ensure developers keep up with demand and differentiate themselves from competitors. Due to early pilot projects, Scotland already has skills and knowledge on innovative programmes that could be applied to the electrolyser supply chain. With accelerated support to commercialise the hydrogen industry at pace, Scotland can use its strengths and experience to develop a highly competitive supply chain that is attractive to developers/OEMs.

4.4 Developing key locations

As described in Section 3.3, Scotland has good capabilities in chemicals processing, engineering, manufacturing and control systems (among others). Mapping the locations of Scottish companies with the required capabilities provides understanding of where skills and supply chain requirements can be transitioned for large-scale electrolyser manufacturing. It also enables the development of regional hydrogen hubs, matching supply chains with hydrogen generation projects.

There are several locations in Scotland which has been at the forefront of developing hydrogen systems including island communities, industrial clusters and cities. Some key examples include:

- Fife – The location of H100 Fife, a world first demonstration of using electrolytic hydrogen produced by a 7MW wind turbine in a local gas network

- Aberdeen – The first city in Scotland to introduce hydrogen buses, and is currently planning an Aberdeen Hydrogen Hub. Aberdeen is also the home of the TECA fuel cell, ERM Dolphyn offshore wind demonstrator and has O&G industry capability.

- Orkney – Orkney has been a key hub of hydrogen innovation with the Surf 'n' Turf project producing hydrogen from tidal energy located at the European Marine Energy Centre.

- Western Isles – The Lewis Green Hydrogen Hub is investigating the production of green hydrogen on the Isle of Lewis and refuelling stations have also been tested in Stornoway.

- Cromarty – Alongside the plans to create an energy hub in the Cromarty Firth, there are plans to include significant hydrogen deployment at scale through connection to offshore wind. This could be a key transport and manufacturing hub.

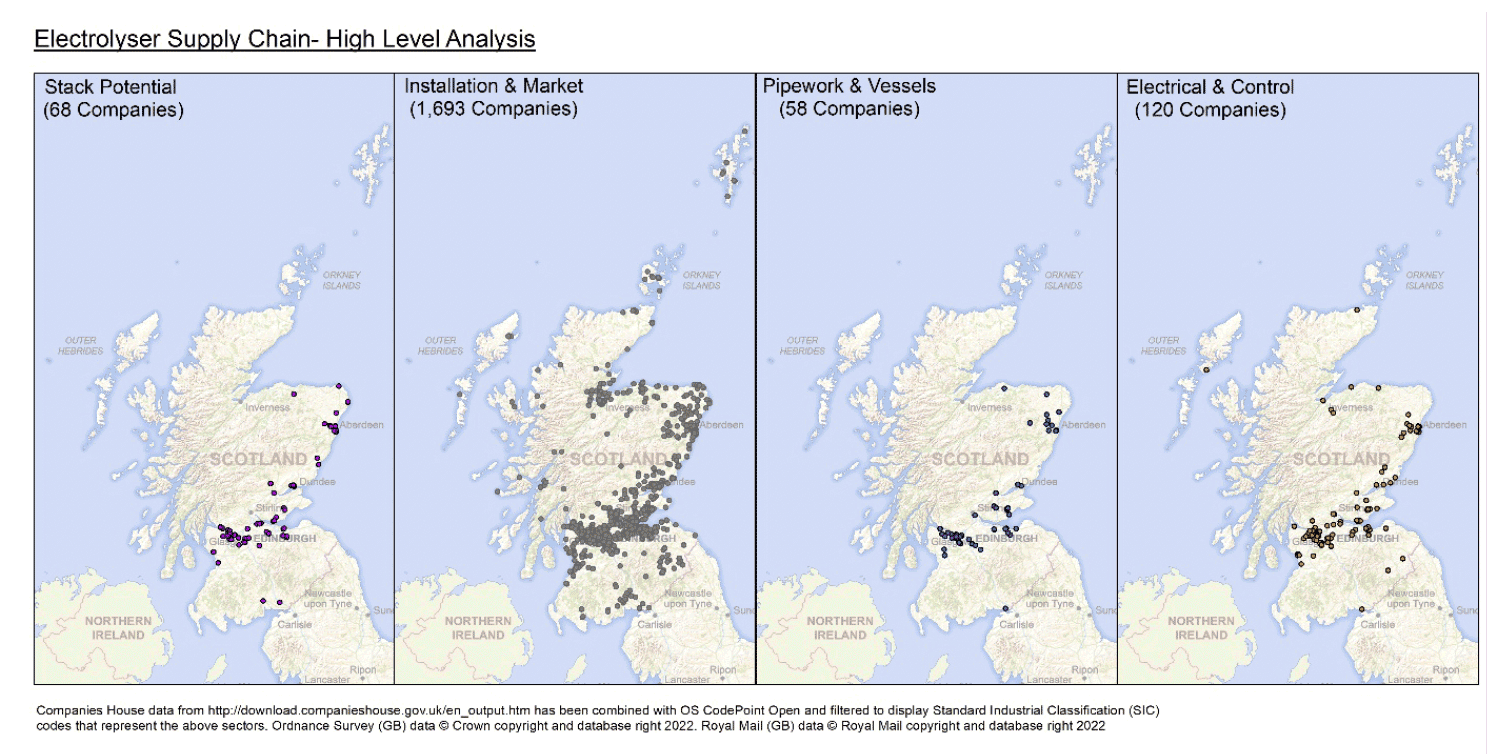

These locations are key to the deployment of hydrogen in Scotland. However, there are areas where there is a significant cluster of companies with the potential to support electrolyser manufacturing. Figure 25 shows the results of a mapping exercise undertaken using the standard industrial classification (SIC) codes. The SIC codes were split into four groups that represent different parts of the supply chain requirements identified in Section 2. The maps only show active companies with more than ten employees who have filed accounts for the most recent year.

The stack potential map includes companies listed against SIC codes for precious metal production, treatment and coating of metals and manufacture of man-made fibres. The two largest clusters of activity are around Glasgow and Aberdeen. However, other centres of activity include Dundee, Edinburgh, Dunfermline and Falkirk.

The installation and market map focuses on companies in the industrial gases sector, electrical and plumbing installation. Due to the large number of companies involved in electrical and plumbing installation at different scales this map is saturated indicating that this would not be a limiting factor for the electrolyser supply chain.

The pipework and vessels map incorporates the tanks and reservoirs, manufacture of valves and manufacture of pumps and compressors SIC codes. Similar to stack potential, there is a strong cluster around Glasgow. However, the cluster around Aberdeen is not as well established and is similar in scale to that around Edinburgh.

The SIC codes for the manufacture of electricity distribution and control apparatus, non-domestic cooling and ventilation equipment and electronic industrial process control equipment are mapped in the electrical and control panel of Figure 25. The clearest cluster is again around Glasgow with smallest clusters around Aberdeen and Edinburgh.

These clusters could represent the beginnings of supply chain hubs that could initially support the deployment of electrolysers around Scotland. These could then grow into manufacturing hubs with electrolyser manufacturing at the centre supported by the more developed local supply chain.

4.5 Export opportunities

There is opportunity for Scotland to capture more economic value from hydrogen activities by becoming a centre for production and export of green hydrogen across Europe. By developing the supply chain early, Scotland will have access to associated skills, products and services that other countries will require to move forward with their hydrogen ambitions. However, if Scotland is slow to deploy, then there is a risk that more of those skills and manufacturing will be developed quicker elsewhere.

There are many advantages to having electrolyser manufacturing local to hydrogen projects to meet Scotland's significant hydrogen potential, as opposed to importing. This includes reduced transportation distance (with associated cost and carbon savings), no customs regulations associated with sourcing abroad, ease of servicing and maintenance, and boosting local skillset and jobs. A local market and favourable policies could also encourage OEMs to locate in Scotland. It is often the case in the energy sector that manufacturing is based where an industry started, for example oil fields in Texas and wind turbines in Denmark and Germany, as manufacturers will often supply local demand and then export once expansion takes place. These advantages could see Scotland become home to large scale electrolyser manufacturing in the near future.

Scotland's geographical location close to mainland Europe will be advantageous in the transport of both hydrogen and supply chain components. Scotland will be able to have easily accessible port connections linking with key infrastructure, such as the planned European Hydrogen Backbone pipeline.

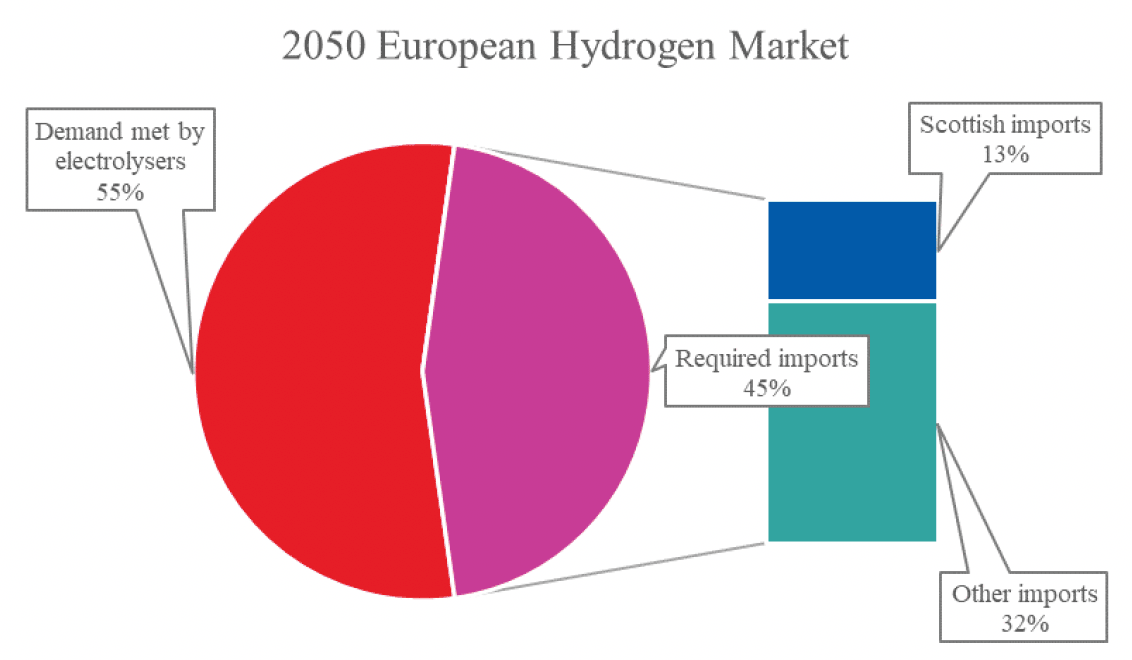

Figure 26 shows that by 2050, there will be an upper estimate of 700 TWh/year demand for hydrogen in northwest Europe (Germany, Belgium, and the Netherlands)[26]. Planned electrolyser projects within the European market amount to a capacity of 381.4 TWh/year by 2050[18], therefore there is currently predicted to be a gap around 318.6 TWh/year of hydrogen which will have to be imported. The Scottish Hydrogen Assessment estimates that 126 TWh of electrolytic hydrogen could be produced in Scotland and 94TWh exported to the European market annually by 2045[5]. This means there is the potential for Scotland to capture a 13% share of the European hydrogen market. Currently, the EU expects 50% of the demand to be met by imports.

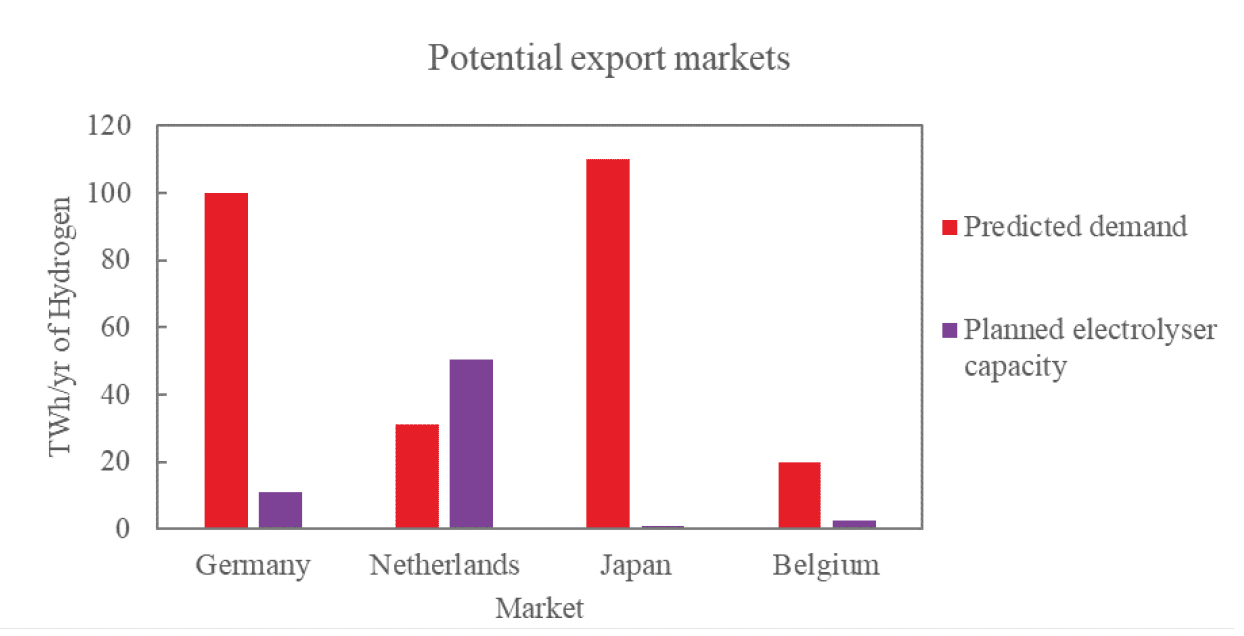

There is also the potential for Scotland to export electrolysers to Europe. A report by Scottish Enterprise identified Germany, Netherlands, Japan and Belgium as key potential export markets[27]. Figure 27 shows the planned electrolyser capacity compared to predicted hydrogen demand in 2030 for each country. Germany, Japan and Belgium have deficits in their current planned electrolyser capacity compared to predicted demand. This means they are promising export markets; there is an opportunity to export hydrogen and/or electrolysers. However, the Netherlands are likely to have surplus electrolyser capacity based on planned electrolyser capacity.

Contact

Email: hydrogeneconomy@gov.scot