Assessment of electrolysers: report

An assessment into the state of electrolyser manufacturing globally, to support an understanding of the supply chain opportunities in Scotland.

3. Existing Supply Chains, Capabilities and Growth

3.1 Global electrolyser supply chain capability

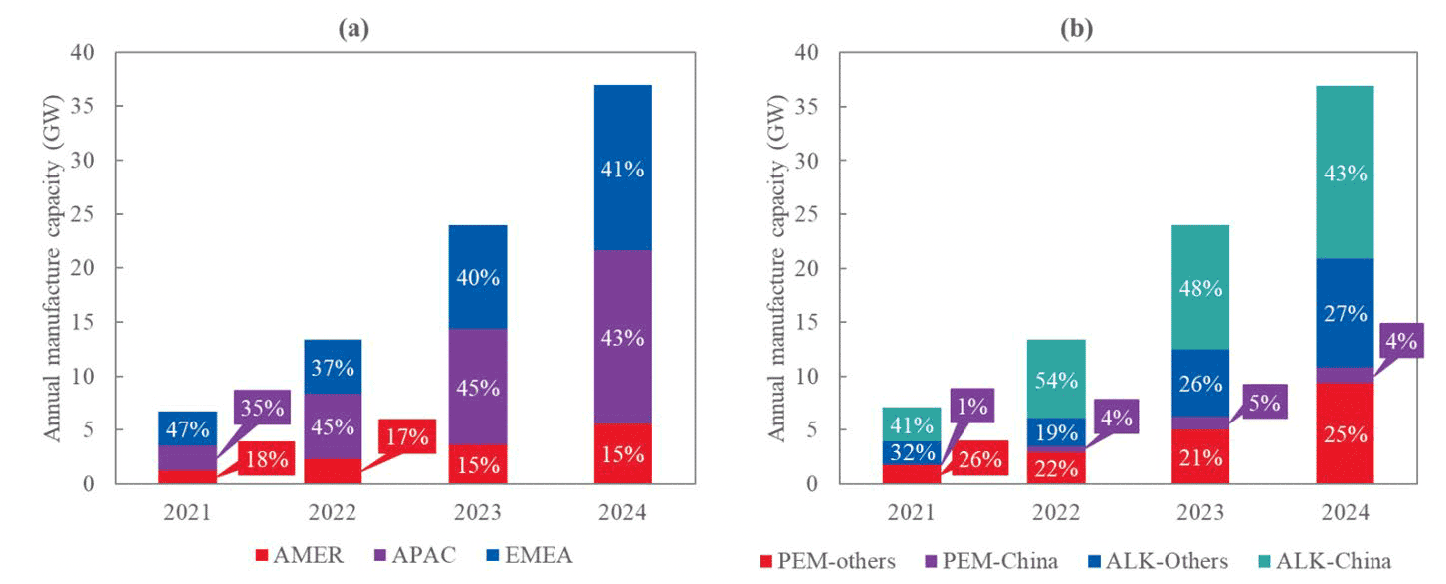

In 2021, global electrolyser manufacturing capacity was 6.7GW. This is expected to increase more than five-fold by the middle of the decade to 37.3GW, highlighting the scale of growth expected to take place in the global hydrogen market[13]. As shown in Figure 17, ALK electrolysers are currently the dominant technology, making up c.75% of global manufacturing capacity, and PEM making up c.25%. SOE's currently account for a very small amount of early-stage manufacturing. Figure 17 also shows that Asia-Pacific (APAC) is the region which has the largest of manufacturing capacity: 58% of ALK and 4% PEM electrolysers were produced in China in 2022 and 45% of manufacturer's headquarters were based in the region.

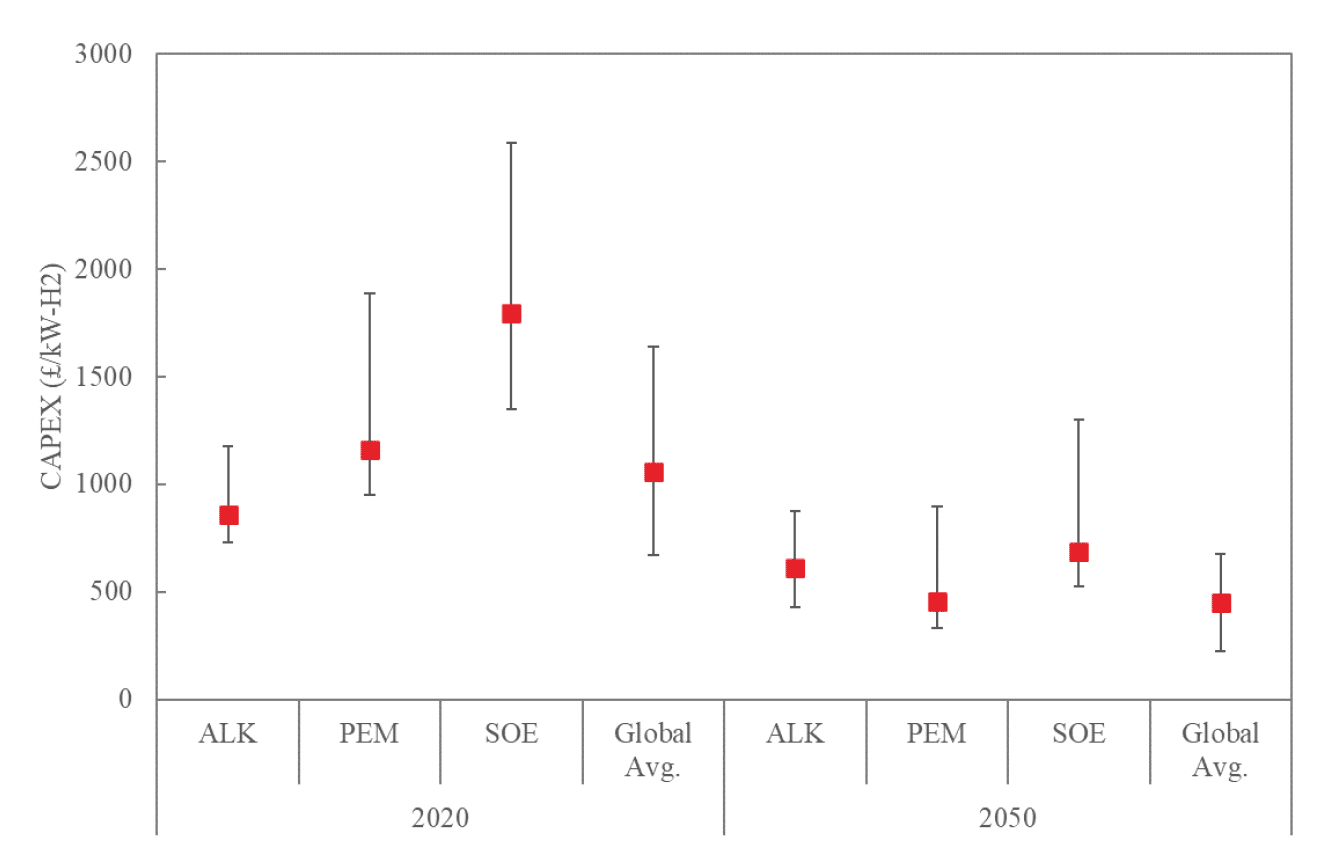

Figure 18 shows the 2020 and 2050 capital cost for each electrolyser technology within the UK, in comparison to the global average. The Department for Business, Energy and Industrial Strategy (BEIS) data was used to assess the cost within the UK, while wider literature was used to determine the global values[14][15]. This suggests that production costs are slightly higher in the UK than the global average. This is likely due to cheaper markets such as China, where the average cost of producing and alkaline electrolyser is 835 £/kW H2 [7], compared to the UK average of 860 £/kW H2 shown in Figure 18. Lowering production costs can be key to attracting manufacturers; for example, Cummins and Ohmium have recently built 500MW/year facilities in Shanghai and Bangalore respectively[13]. Of the three electrolyser chemistries, SOE is consistently the highest cost. Currently ALK offers the lowest figure, however, PEM is projected to become cheaper in the future.

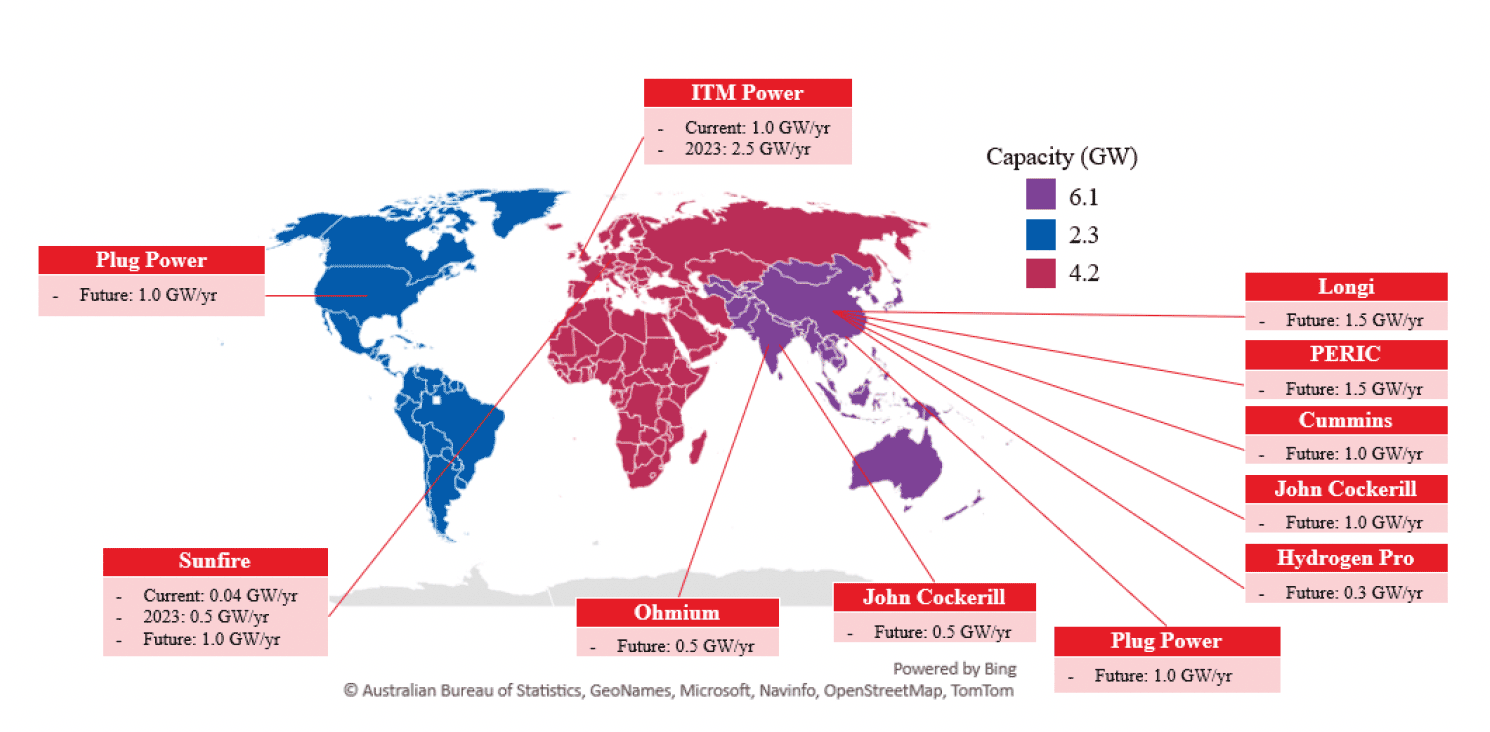

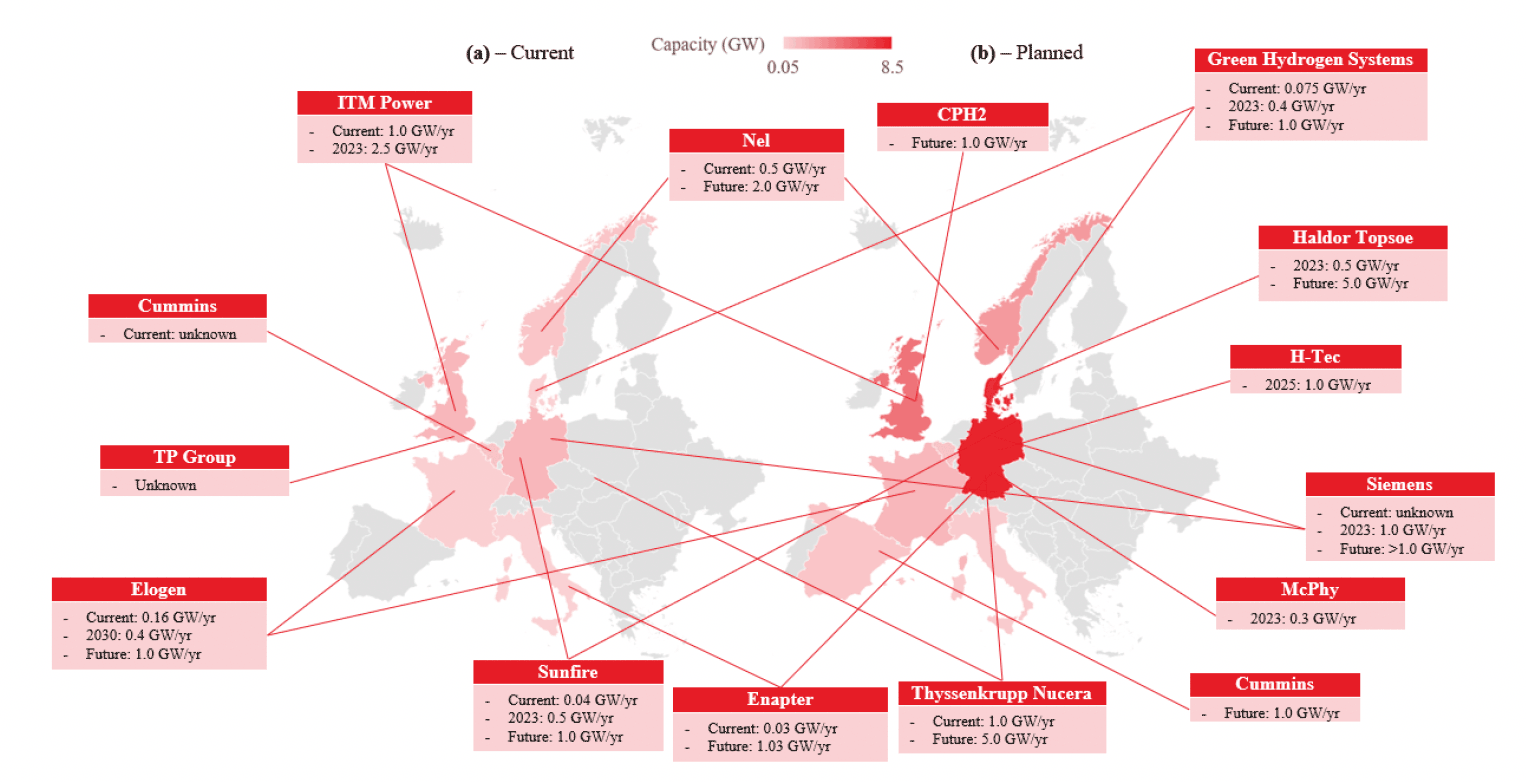

Figure 19 shows the location of key electrolyser manufacturing sites globally, highlighting current and planned capacity.

A large increase in electrolytic hydrogen projects this decade means that supply chains could be a key value chain bottleneck, particularly as countries scale up to meet their net zero and hydrogen targets. The total 2030 electrolyser targets for countries with a hydrogen strategy totals 73.9GW capacity[16], and this would be expected to increase as more countries commit to hydrogen deployment. There are currently thirty-one countries with a hydrogen strategy (fifteen with electrolyser-specific targets) and eighteen countries currently in the process of developing strategies.

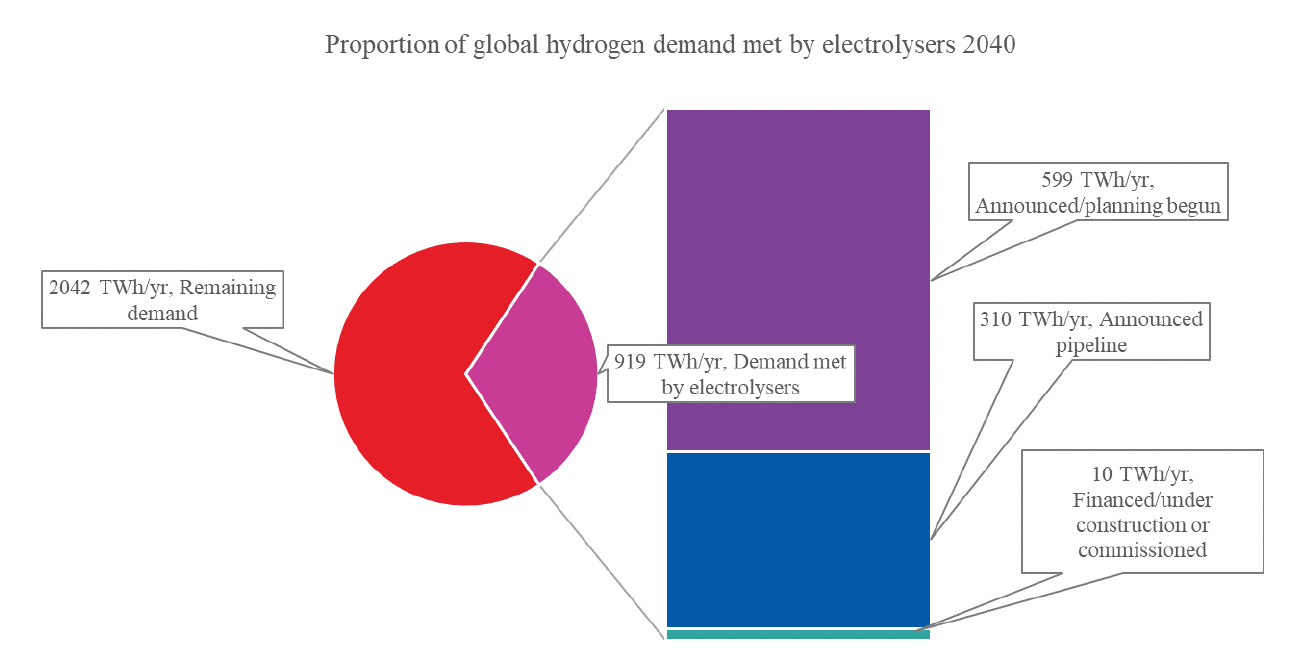

Figure 20 shows the IEA's projected global hydrogen demand by 2040[17] against planned electrolyser projects by developers[18]. This highlights that currently less than half of the expected future hydrogen demand would be met by the planned electrolyser project pipeline (45%), signifying that there will be significant market opportunity for a Scottish electrolyser industry to contribute to meeting future demand.

3.2 European electrolyser supply chain capability

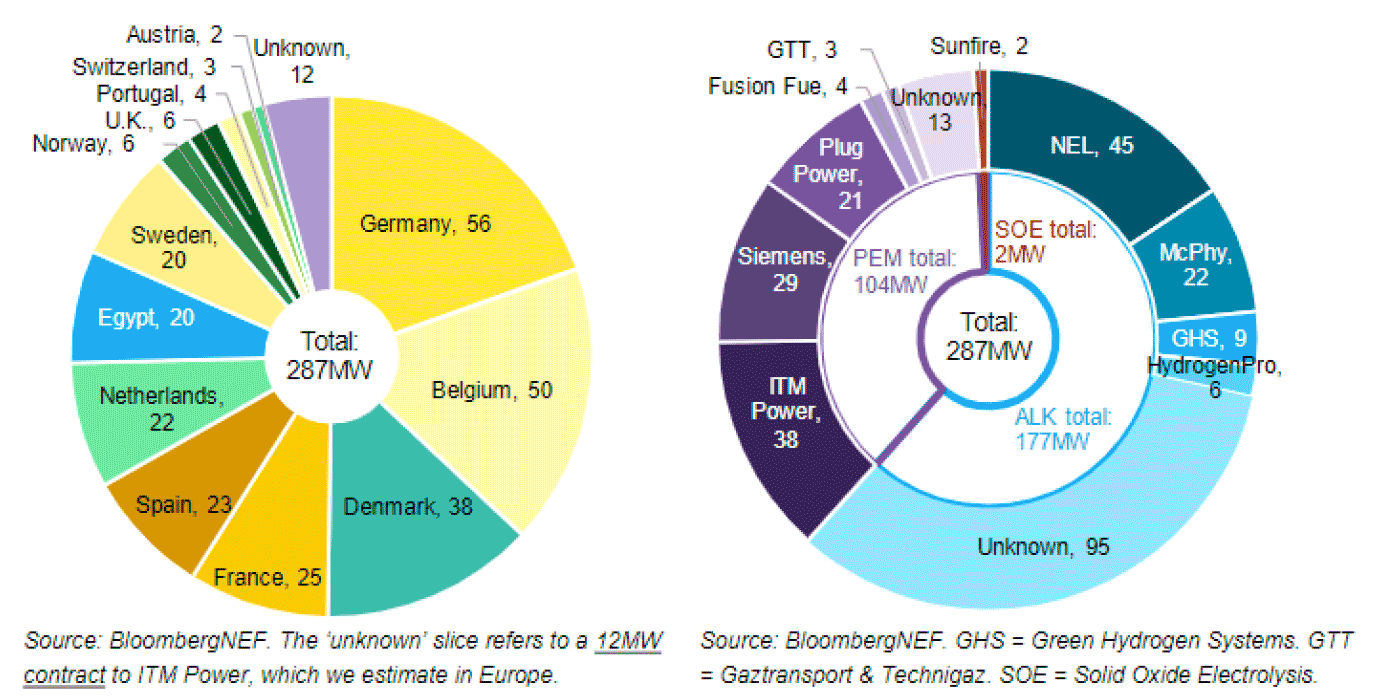

Europe has been a leader in setting hydrogen targets and strategies, however, it has a smaller manufacturing base than China. As shown in Figure 21, the electrolyser manufacturing market in Europe is fairly distributed across countries with largest electrolyser shipments in 2022 expected to be in Germany (56MW), Belgium (50MW) and Denmark (38MW)[13]. For comparison, the UK is expected to ship 6MW of capacity. Electrolyser manufacturers Plug Power, ITM Power, Siemens and NEL represent nearly half of the total capacity of shipped electrolysers expected in 2022.

The current capacity of electrolyser manufacturing in Europe is estimated to be 1.75GW/year and is expected to increase to 17.5GW/year by 2025, driven by the 'Fitfor55' and 'RePowerEU' policies[19]. The European Commission's hydrogen strategy shows a clear desire to scale up production, as it sets out a strategic objective to install at least 40GW of renewable hydrogen electrolysers by 2030 and produce up to 10 million tonnes of renewable hydrogen in the EU. Germany has committed to the largest individual EU country target of 10GW electrolyser capacity (the UK current target is 5GW electrolyser capacity)[16]. However, an integrated supply chain in Europe is emerging and requires upscaling. The European Clean Hydrogen Alliance is facilitating the emergence of integrated European value chains, with twenty electrolyser manufacturers signing a joint declaration at the European Electrolyser summit in May 2022[19]. Figure 22 shows the current and planned manufacturing capabilities of several of the largest electrolyser manufacturers in Europe.

3.3 Scottish electrolyser supply chain capability

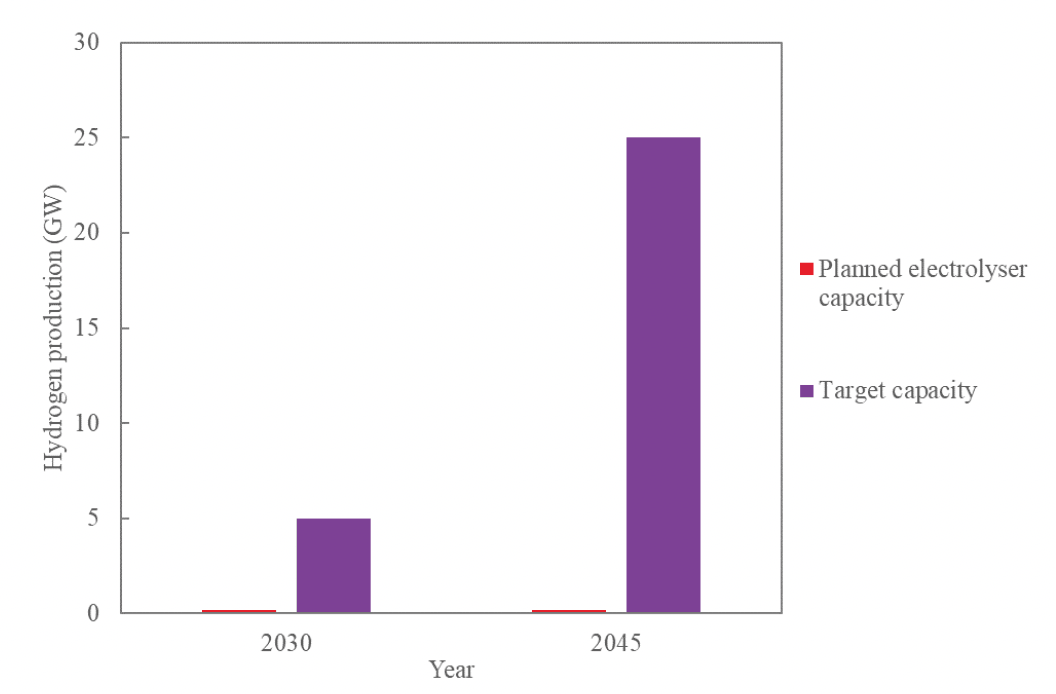

Scotland has a strong heritage of manufacturing and engineering, from ship building on the river Clyde to North Sea oil and gas. To date, Scotland has been at the forefront of hydrogen demonstration and development through several world first demonstration projects, including Levenmouth Community Energy Project (370kW), Surf 'n' Turf (500kW), and Aberdeen H2 Buses (1MW). Larger scale projects currently in development include ERM Dolphyn (2MW) and Whitelee Windfarm (20MW). Scotland's hydrogen targets for 5GW of installed hydrogen capacity by 2030 and 25GW by 2045 are among some of the most ambitious in the world and give a firm signal to industry regarding intent to grow the hydrogen market in Scotland. However, Figure 23 shows the very large gap between announced projects or projects in planning and the ambitious targets.

Scotland's current supply chain capabilities have been assessed against the tiers that were identified when setting out the required capabilities of the supply chain in Section 2.2. These are provided in Table 8.

| Supply chain tier | Current capabilities in Scotland | Opportunities in Scotland | |

|---|---|---|---|

| Raw and processed materials | Metal processing and coating Semiconductor suppliers Chemical processing |

Strong hydrogen policy: 5GW hydrogen by 2030 Engineering (process, electrical, precision and machine) Construction Finance |

Metal mining Complex plastics manufacturing and suppliers |

| Manufacture of components | Manufacturers or suppliers of process and electrical equipment | OEM of electrolysers/fuel cells Novel and innovative manufacturing |

|

| System integration and installation | Control system producers System integrators – specific to hydrogen Pipework and metalwork |

OEM of electrolysers/fuel cells | |

| Operation and maintenance | Renewable energy Demand for hydrogen |

Know-how to operate and maintain facilities | |

| End-of-life | Oil and gas decommissioning industry | Specialist material recovery and recycling services | |

Raw and processed materials

Chemical processing is a crucial part of the first tier: electrolytes, electrocatalysts and other electrolyser specific components rely on it. Scotland's chemical sciences sector is worth £750 million and represents £4.4 billion in exports[20]. This is a clear strength that Scotland offers to the supply chain, and there is opportunity for this sector to become involved in the hydrogen market. For example, Ames Goldsmith Ceimig is a specialist producer of electrocatalysts for the hydrogen market. Additionally, Scotland benefits from a metal processing industry with precision and machine engineering capabilities and an established semiconductor supply chain for a thriving tech sector. However, there is a gap in the extraction and supply of raw materials, as there is little opportunity for commercial mining in Scotland. This means there will be a heavy reliance on raw material imports.

Manufacture of components

Within the second tier, Scotland benefits from strong skills in process and electrical equipment manufacture and supply, through its engineering and oil and gas sectors. Scottish companies, such as Howden (a producer of heat exchangers and compressors), demonstrate the strong capabilities of this tier that already exist. Currently, the lack of a commercial-scale electrolyser OEM is a substantial gap; however, a combination of a strong demand pipeline and supportive policy/funding mechanisms can make Scotland an attractive location for OEMs. In addition, there are opportunities to attract OEMs if the production and supply of key components is located Scotland, alongside hydrogen project opportunities. Moreover, with the supply chain still in its infancy, there is a clear opportunity to support novel and innovative manufacturing techniques that have the potential to improve efficiency and lower costs. Though investment in automation, standardisation and incentives to scale up Scotland could be a leader in the production of electrolysers.

System integration and installation

One of the strengths of tier three is Scotland's many control system producers, which is a key auxiliary service for the electrolysers. Some of these are already expanding into the hydrogen sector from the more traditional oil and gas areas. Examples of this include HCS Control Systems and Hydrasun; they are established producers of control systems and likely have the capabilities to be able to support this supply chain. Moreover, there are several companies, such as Logan Energy and Pure Energy Centre, providing system integration and installation services specific to the hydrogen sector. There are also firms that can provide the necessary pipework, metalwork auxiliary services, process engineering and electrical engineering skills that help to support this tier.

Operation and maintenance

During operation of electrolyser facilities, Scotland benefits from good access to renewable energy; cost and carbon footprint of electricity is a key marker of operational success. However, this tier requires a workforce with the know-how to be able to operate and maintain electrolytic production facilities, which is a potential gap. This can be filled through training of the workforce and offers the opportunity for a just transition.

End-of-life

End-of-life services provides an opportunity for the Scottish market to differentiate itself. This tier is still in its infancy – some companies, such as Johnson Matthey, are beginning to develop closed loop aspects of the chain but this is limited[21]. Development of this tier can improve sustainability and the supply chain's resilience. Modelling of fuel cell markets in China found that a high-quality end-of-life program can help to alleviate high material demand (which is a key vulnerability in the supply chain) reducing risk and potentially costs[22]. Scotland is well positioned to capitalise on this due to the skills developed in the oil and gas and renewables decommissioning sector.

3.4 Hydrogen policy landscape

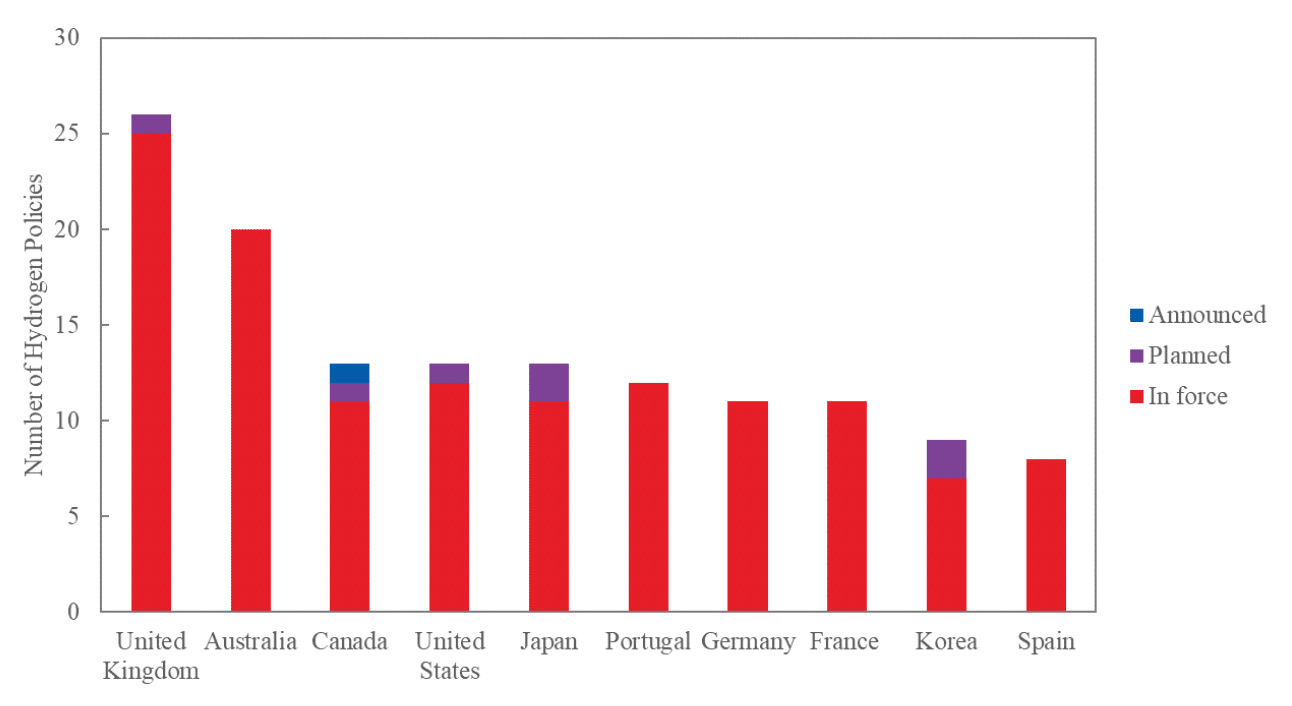

Figure 24 shows the number of hydrogen policies in selected countries according to the IEA[23]. This demonstrates the vast scale of supportive policy available in the UK for the hydrogen sector. As previously discussed, de-risking of hydrogen investment is a crucial requirement of the supply chain as it is scaled up. Through strong hydrogen targets, Government investment, continued development of business models and revenue support, the supply chain can manage risk associated with market prices and demand. This helps to enable private investment, such as the projected £9 billion of investment in production and the 12,000 jobs by 2030 across the supply chain highlighted in the UK Hydrogen Sector Development Action Plan[24].

Both UK and Scottish Government policy sees hydrogen playing a key role in the energy transition. The Scottish Hydrogen Policy Statement aims for 5GW of installed hydrogen capacity by 2030 and 25GW by 2045. The UK-wide hydrogen target has recently been increased from 5GW to 10GW by 2030, with at least half being electrolytic. This provides a positive backdrop to the development of the hydrogen sector and supply chains and is more likely to encourage electrolyser OEMs to locate in Scotland.

Several funding initiatives have been put in place to support the development of the hydrogen economy, including a commitment of £100 million funding from the Scottish Government to support hydrogen projects. The UK Government will invest £100 million of support for hydrogen business models for 250MW of electrolytic production in 2023; further allocations will be made in 2024. The UK Government have developed the Net Zero Hydrogen Fund and Hydrogen Business Model to ensure projects are investible through management of price and volume risks.

Together the Scottish and UK Governments are working to deliver further mechanisms to support the hydrogen sector, such as regulatory frameworks and standards, business models and emissions mandates, all of which are required to ensure a successful hydrogen economy and support a growing supply chain.

Contact

Email: hydrogeneconomy@gov.scot