Visitor Levy Bill: business and regulatory impact assessment

Business and regulatory impact assessment (BRIA) that looks at the likely costs, benefits and risks of the Visitor Levy (Scotland) Bill.

2. Purpose and Intended Effect

2.1 Background to the proposal for a Visitor Levy (Scotland) Bill

2.1.1 In 2018, a number of our local authorities, as well as the Convention of Scottish Local Authorities (COSLA), called on the Scottish Government to create powers to allow them to apply a 'tourist tax' or 'visitor levy', should it be appropriate for local circumstances. This reflected not just the local pressures associated with sustained high numbers of visitors, but also the wider policy context of promoting greater local decision-making together with a recognition of the prevalence of such taxes in other jurisdictions outside the UK.

2.1.2 In response to this call, in 2019 the Scottish Government engaged with a range of partners and stakeholders from the tourism industry, local authorities and the wider business community in Scotland in a National Discussion on the principles of a visitor levy. The National Discussion provided an initial evidence base, illustrating potential opportunities and challenges associated with tourist taxes and drawing out a number of important issues and concerns.

2.1.3 Following the conclusion of the National Discussion and as part of the agreement of the Scottish Budget 2019-20, the Scottish Government committed to consult on the principles of a locally determined 'tourist tax' or visitor levy and introduce legislation to permit local authorities to introduce such a visitor levy if they considered it appropriate. This commitment was part of a package of measures focusing on local tax reforms and local fiscal empowerment. A public consultation was held from September to December 2019, with a consultation analysis report published in March 2020.

2.1.4 Work was then paused during the Covid-19 pandemic, until the Scottish Budget 2022-23 committed the Scottish Government to resuming work on the visitor levy proposal. This culminated in the announcement that a Bill would be part of the 2022-23 Programme for Government.[2]

2.1.5 Based on the findings of the consultation, further engagement with stakeholders and additional research and analysis, the Scottish Government developed formal proposals, and drafted the legislation that if passed would put them into effect. A Bill was therefore developed and introduced to parliament on 24th May 2023.

2.2 Background to the visitor economy in Scotland and taxes on tourism in an international context

2.2.1 The proposal for a visitor levy will mean that the visitor economy in particular parts of Scotland where local authorities choose to introduce the visitor levy will be affected by the provisions of the Bill.

2.2.2 Businesses and other organisations[3] providing commercial accommodation to visitors as well as visitors purchasing accommodation from these businesses in these areas will face some additional costs (these are explored in more detail in section 4). There will be potentially higher accommodation prices for visitors and some new compliance costs for accommodation businesses. Local authorities will benefit from a new source of revenue which will be separately accounted for and required to be invested back into improving the local visitor economy, bringing benefits for visitors and residents.

2.2.3 Background data and statistics covering the visitor economy in Scotland are provided in more detail in Annex D.

2.2.4 The accommodation sector is a very important part of Scotland's economy and society. The accommodation sector is a key element of Scotland's visitor economy, as well as providing a service to support wider business activity in the economy. The scope and diversity of the accommodation sector is wide-ranging, encompassing Hotels, Bed and Breakfast accommodation, Self-Catering accommodation, Caravan and Campsites, as well as Hostels that provide visitor accommodation. It is estimated that the accommodation sector alone in Scotland comprises of 2,925 registered enterprises in 2022 (1.7 per cent of Scotland's total), employing 44,000 people in 2021 (1.7 per cent of Scotland's total employment).[4] As set out in Annex D, the accommodation sector also includes a large number of small enterprises that are not registered for VAT or PAYE and are therefore not included in the statistics above.

2.2.5 Beyond the accommodation sector, the 'Sustainable Tourism Growth[5]' sector as a whole employed 209,000 individuals across Scotland in 2021. This represented around 8 per cent of total employment in Scotland. The sector is also a particularly important source of employment in rural areas of Scotland such as Argyll and Bute, the Highlands, and Stirling.

2.2.6 In large part, it is the spending of visitors in these areas (rather than residents) that supports the accommodation and wider tourism sector across Scotland. Before the Covid-19 pandemic, there were around 17.5 million overnight visitors to Scotland in 2019, spending an estimated £5.9 billion, and around 134 million day visitors, spending £5.8 billion. It should be recognised that the definition of a visitor is broad in this context and will include visitors travelling for non-leisure purposes.

2.2.7 As the visitor levy could be introduced at a local authority level, it is important to recognise the size of the visitor economy varies in significance across different regions of Scotland. Table 1 shows the average number of nights stayed and total spending of visitors using overnight accommodation in different parts of Scotland between 2017 and 2019. It provides an indication of the number of visitors using commercial accommodation that could be required to pay a visitor levy in future. Table 1 shows that 37% of total visitor spend, and a third of visitor nights in commercial accommodation, were in the Edinburgh and Lothians region over the period. The Highlands and Islands also attracted a large proportion of total overnight visitors, accounting for a fifth of both total overnight visitors and of visitor spend. Further analysis of these estimates is provided in Table D10 in Annex D.

| Area | Visits (000s) | Spend (£m) | ||||

|---|---|---|---|---|---|---|

| Domestic | Overseas | Total | Domestic | Overseas | Total | |

| Aberdeen and Grampian | 671 | 225 | 896 | 147 | 103 | 250 |

| Angus and Dundee | 244 | 46* | 290* | 55 | 22* | 78* |

| Argyll, the Isles, Loch Lomond, Stirling & Trossachs | 1,042 | 131 | 1,173 | 266 | 94 | 360 |

| Ayrshire and Arran | 472 | 53 | 525 | 115 | 36 | 151 |

| Dumfries and Galloway | 533 | 22* | 556* | 111 | 11* | 123* |

| Edinburgh and Lothians | 1,952 | 1,926 | 3,878 | 641 | 1,018 | 1,659 |

| Greater Glasgow and Clyde Valley | 1,295 | 675 | 1,970 | 329 | 305 | 634 |

| Highlands and Islands | 1,745 | 602 | 2,347 | 525 | 252 | 777 |

| Kingdom of Fife | 364 | 104 | 468 | 90 | 78 | 168 |

| Perthshire | 573 | 114 | 688 | 140 | 46 | 185 |

| Scottish Borders | 212 | 16* | 228* | 51 | 5* | 56 |

| Not specified | 69* | 40 | 109* | 15* | 37 | 53* |

| Total | 8,696 | 2,956 | 11,652 | 2,486 | 2,008 | 4,494 |

Source: Domestic: VisitBritain, GBTS, average between 2017, 2018 and 2019

Overseas: ONS, IPS, average between 2017, 2018 and 2019

Notes:

1. The coverage of commercial accommodation within the overseas estimates (IPS) includes overnight visits by overseas visitors in: Hotels; Guest Houses; Bed & Breakfasts; Rented House/Flat; Hostel/University/School; Camping/Caravan; Holiday Village and 'Other'. It does not include overnight visitors staying as a free or paying guest with friends or family or in own homes.

2. The domestic estimates (GBTS) include overnight stays by Great British residents in commercial accommodation in: Hotels; Motels; Guest Houses; Bed & Breakfasts; Hostels; Camping and Caravan; Holiday camps; Paying guest and 'Other rented accommodation'. It does not include visitors staying overnight in second homes, owned static caravans or homes of friends / relatives.

3. * estimates are based on a relatively small sample size. This may result in less precise estimates, which should be used with caution.

4. Unshaded estimates are based on a larger sample size. This is likely to result in estimates of higher precision, although they will still be subject to some sampling variability.

2.2.8 It is in part the size of the visitor economies demonstrated by these statistics which has underpinned specific calls by Edinburgh and Highland councils in recent years for powers to introduce a visitor levy to raise additional revenues to manage and sustain this activity in the future, with both local authorities having conducted local consultations on proposals in recent years.[6]

2.2.9 These local authorities and others, as well as the COSLA, have looked to other cities and municipalities in parts of Europe and internationally as examples of how visitor levies have been used to raise additional revenues. Further detail of these taxes and some specific case studies are provided in Annex B of this BRIA.

2.2.10 Taxes on visitors staying overnight in paid-for accommodation are common across Europe and in other locations across the world. The rationale for these taxes varies. Some cities and regions use a levy as a way to increase general revenues to fund the provision of public goods and general services used by residents and visitors. Other cities and regions ring-fence all or a portion of the net revenues arising from these taxes to fund specific projects that support the visitor economy. These include managing any negative impacts of tourism such as specific environmental degradation, increased promotion and marketing of a destination, or the provision of specific benefits to visitors such as free local transport or discounts on attractions.

2.2.11 Taxes raised in other parts of the world have some common features. Whilst the enabling powers for local taxation are often set out in national legislation, in the vast majority of cases local jurisdictions will have autonomy in the decision to implement the tax, the setting of the tax rate, the administration of the tax and the use of revenues within any national parameters that may be set. The basis of charge for these taxes is generally either a small, fixed charge per person per night or an additional percentage charge added to the cost of accommodation.

2.2.12 There are a variety of different exemptions applied to these taxes. Either specific visitors (for example business travellers, people who are temporarily homeless, temporary or seasonal workers or children under a certain age) or specific types of accommodation (such as youth hostels or accommodation sold below a certain price floor) could be exempt for the purposes of the tax or levy. The tax rate may also apply only at specific times of year (with lower rates or no rates charged during the low season) and may be capped at a certain level for visitors staying in an area for a longer period of time.

2.2.13 Whilst it is recognised that accommodation providers and visitors already pay a variety of taxes here and in other contexts internationally such as corporation tax, VAT, taxes on commercial property and employer social insurance contributions, the relative additional burden of visitor levies and similar taxes is generally small.

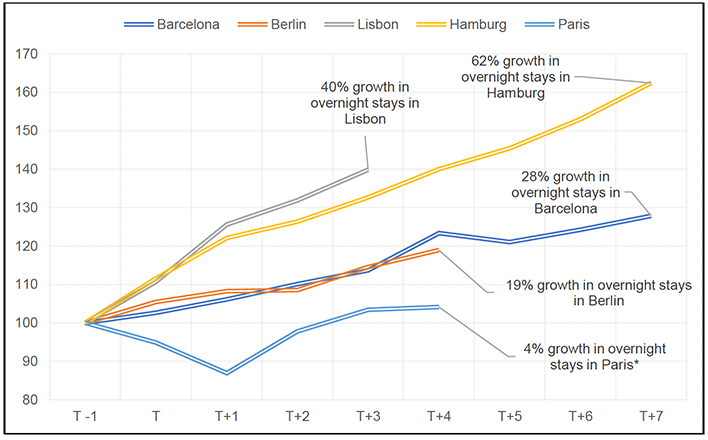

2.2.14 Evidence from cities that have introduced these types of taxes recently show that generally growth in visitor numbers has continued after the introduction of these taxes. Figure 1 shows the relative change in overnight visitors for selected cities in Europe that have either introduced or increased existing taxes on visitors in the past 10 years including Barcelona, Lisbon, Berlin, Hamburg and Paris. In most cases there continued to be strong growth in overnight visitor numbers and no area saw a fall in visitor numbers[7] prior to 2020. Further detail is provided in Annex B.

*'T' is the year a tax on overnight visitors was introduced or increased in each city. T-1' is the year prior to the introduction of the tax. More details are provided in Annex B. The decline in visitor numbers to Paris in 2016 has been linked the impact of terror attacks.

2.2.15 Despite this evidence in Figure 1, it is acknowledged in this BRIA that there is a risk of negative economic impacts arising from the introduction of additional taxes on the visitor economy in local areas. This is discussed in more detail in Annex C, which sets out the elements to consider when assessing the economic impact of the Visitor Levy Bill on the Scottish economy. As part of the requirements set out in the Bill, local authorities must assess the impacts of introducing a visitor levy within in their own areas, before deciding to introduce a levy.

2.2.16 A recent review of tourist taxes internationally produced set of good practice recommendations with respect to the introduction of taxes similar to a visitor levy.[8] The Scottish Government plans to work in consultation with COSLA, the accommodation sector and other relevant stakeholders to develop guidance for local authorities regarding key issues such as the implementation, administration and monitoring of visitor levy policies

2.3 Objectives and rationale for government intervention

2.3.1 The aim of the Bill is to introduce a discretionary power enabling local authorities in Scotland to apply a visitor levy on overnight stays in commercially let accommodation. A successfully implemented Bill will meet the following objectives:

- Strengthen local democracy through increased local decision making and more empowered communities.

- Support the sustainable growth of the tourism sector across Scotland, particularly in cities and regions which have experienced high visitor numbers in recent years.

- Create a new local tax power which is consistent with the Government's overall approach to taxation.

2.3.2 These specific objectives are aligned with the following national outcomes:

- Economic: We have a globally competitive, entrepreneurial, inclusive and sustainable economy.

- Fair Work and Business: We have thriving and innovative businesses, with quality jobs and fair work for everyone.

- Communities: We live in communities that are inclusive, empowered, resilient and safe.

- Environment: We value, enjoy, protect and enhance our environment.

2.3.3 The rationale and objectives underpinning the Bill emerged from on-going engagement with stakeholders on the principle, aims and objectives of taxation on visitors. The Scottish Government engaged with a range of partners and stakeholders from the tourism industry, local authorities and the wider business community in Scotland in a National Discussion on a Transient Visitor Tax (referred to as 'the National Discussion')[9] between November 2018 and January 2019.

2.3.4 As highlighted in the National Discussion there was a shared appreciation among participants of the importance of tourism as a key sector of the economy and accommodation providers as a key part of the overall tourism sector. It was also recognised that future growth in the sector depended on supporting and investing in tourism facilities and services to ensure that Scotland remains an attractive tourism destination.

2.3.5 Local authorities in Scotland (and elsewhere in the UK)[10] do not currently have the power to introduce a visitor levy to raise revenues to sustain tourism activity or local visitor economies. Through the National Discussion, COSLA and local authorities like Edinburgh and Highland expressed support for the principle of a new power that would enable local authorities to introduce a visitor levy, to allow for revenues to be raised to support individual areas' tourism priorities, should local circumstances be supportive.

2.3.6 COSLA's 2022-27 plan[11] set out six priorities for local government over the next 5 years including an objective to 'strengthen local democracy' and to 'secure sustainable funding'. It is recognised by COSLA that the proposals set out in the Visitor Levy Bill are part of meeting these dual objectives of local government, within the context of developing a wider comprehensive fiscal framework between the Scottish Government and Scotland's local authorities.

2.3.7 The National Discussion also highlighted that pressures linked to visitor numbers are not experienced equally across Scotland, and that its introduction across all local authorities may not be appropriate for some areas looking to increase visitor numbers, recognising the potential risk that higher prices of accommodation could discourage visitors to some areas more than others (see Annex C).

2.3.8 In recognition of these issues, the visitor levy that can be introduced under the Visitor Levy Bill is discretionary and local authorities can choose to introduce one or not in their area, depending on their local circumstances. The framework for these local taxes is set out in the Bill which will ensure a degree of consistency in the approach should the tax be adopted by multiple local authorities.

2.3.9 Submissions by some local authorities to the National Discussion also highlighted specific challenges related to tourism activity in their areas and suggested that a visitor levy would potentially offer an appropriate response to these. These included the provision of services to help address tourism pressures, such as additional street cleaning in peak tourist seasons. They also included the provision and maintenance of public goods such as parks, walkways, public toilets, public spaces, and cultural amenities, where the costs of provision were often borne by local residents.

2.3.10 In giving a local authority the power to introduce a visitor levy, the Bill will therefore also be giving local authorities a tool they can use to develop, support and sustain facilities and services which are substantially for, or used by, those visiting a local authority's area for leisure purposes. This may be particularly relevant in the context of pressures on such facilities and services that may arise or be exacerbated by high numbers of visitors, because currently these visitors will generally not directly contribute to the revenues of local authorities. The future of tourism demand and visitor numbers to Scotland (and different areas within Scotland) in the post-pandemic period is inherently unknown, however the discretionary nature of the power will equip local authorities with a new fiscal power to raise revenues to support local visitor economies should particular pressures arise in the future.

Contact

Email: Ben.Haynes@gov.scot