Tax policy and the budget: consultation

This consultation seeks views on our overarching approach to tax policy, through Scotland’s first framework for tax, and how we should use our devolved and local tax powers as part of the Scottish Budget 2022 to 2023.

1 – Introduction

A Vision for Good Tax Policy Making

Taxes form part of the fabric of society. They are a key component of the social contract. How we develop and deliver tax policy is of great and increasing importance to the Scottish Government. We have already taken significant steps to modernise the taxes that have been devolved to the Scottish Parliament, in line with our Scottish Approach to Taxation, and the Framework for Tax further enhances our approach. It embodies our ongoing commitment to, and vision for tax in Scotland; an approach that is underpinned by policy and delivery excellence, good practice, open government and transparency; and where tax policy is positioned to meet the challenges of today and tomorrow.

This is of fundamental importance to the people of Scotland, noting the vision for tax put forward by the Citizens’ Assembly for Scotland:

Scotland should be a country where all taxes are simplified and made more proportionate so that everyone is taxed accordingly; taxation is transparent and understandable; measures are introduced to minimise tax avoidance: and companies are incentivised to adopt green values.

What the Framework does

The Framework broadly sets out the what, how, when and why in relation to our overall approach to tax policy making. One of the core aims is transparency. It is therefore designed to be accessible for the public and stakeholders alike. As far as possible, technical jargon is minimised or explained.

- Chapter 1 provides background, setting out the tax powers devolved to the Scottish Parliament and the fiscal landscape within which they sit.

- Chapter 2 sets out the principles that underpin the Scottish Approach to Taxation.

- Chapter 3 sets out our overarching strategic objectives and our approach to appraisal and decision-making.

- Chapter 4 looks at the policy and Budget cycles and how we plan and deliver tax policy around these.

- Chapter 5 sets out our programme of work for this Parliament 2021-2026, which will be updated around the mid-point in 2023.

Expected Benefits

In creating a Framework for Tax, the Scottish Government is aiming to:

Be open and transparent about how we approach tax policy. Responding to the recommendations of the Citizens’ Assembly, the Framework provides more information, in accessible language, on the purposes for collecting taxes; the principles that underpin our approach; our strategic objectives and our programme of work for this Parliament.

Exemplify best practice and embed continuous improvement by ensuring tax decisions are coherent, rooted in a defined set of principles and objectives and rigorously appraised; and by embedding a policy cycle, including evaluation, and putting proactive engagement at the heart of tax policy making.

Improve sequencing so that policy and Budget cycles align as far as possible, to ensure we take an organised and structured approach to tax policy.

Take a forward thinking approach especially in the wake of COVID-19, identifying medium to longer-term opportunities and threats to inform future work, new ideas and to be prepared should further tax powers be devolved to the Scottish Parliament.

Background

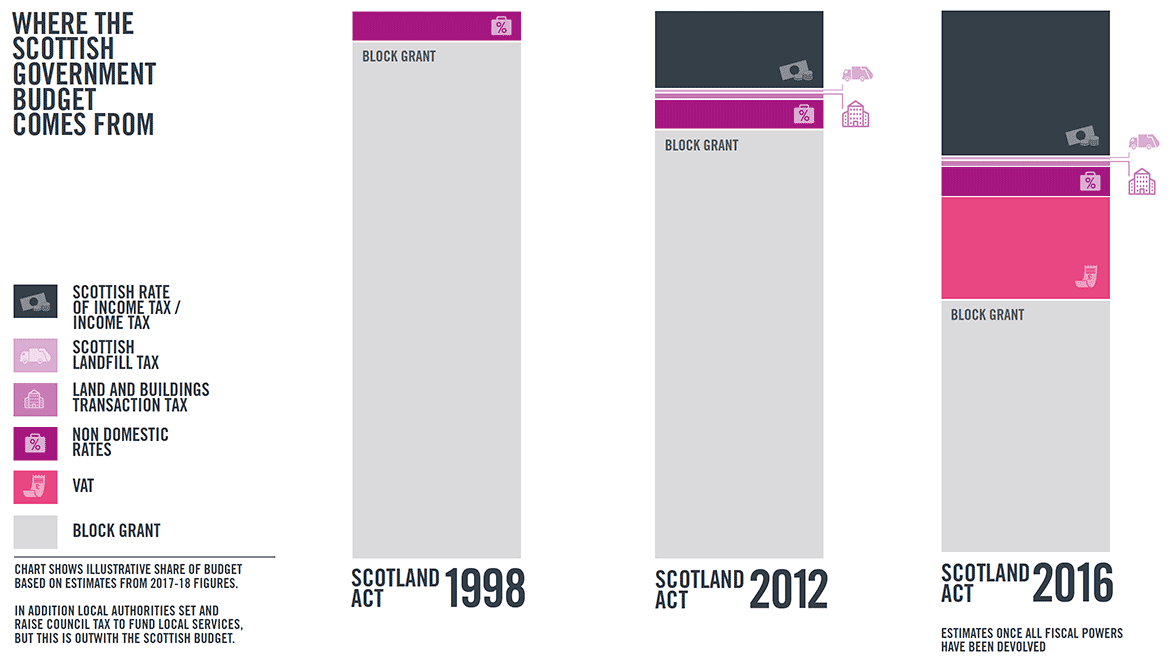

Funding the Scottish Budget

The Scottish Budget is principally comprised of the Block Grant, local tax revenues, net devolved tax revenues and additional funding for devolved social security powers. The overall funding position depends in large part on the operation of the Fiscal Framework.

Figure 1: Funding for the Scottish Budget

Component One: Barnett formula determined Block Grant − Component Two: Deduction to reflect UKG revenues foregone (BGA) + Component Two: Addition to reflect UKG social security expenditure no longer incurred (BGA) + Component Three: Revenues raised from devolved tax in Scotland = Funding for Scottish Budget

- Component One – Barnett formula determined Block Grant – Barnett continues to determine the initial size of the Block Grant and block grant funding remains the largest component of the Scottish Budget.

- Component Two – Block Grant Adjustments (BGAs) – the Block Grant is adjusted to reflect the devolution of tax and social security powers. The size of the adjustment is based upon the performance of the corresponding UK tax revenues and social security expenditure.

- Component Three – Devolved tax revenues – the revenues from devolved local and national taxes, which contribute to Scotland’s funding.

Scotland’s Devolved Taxes

The Scottish Parliament has limited powers when it comes to taxation. Under the current devolution settlement the vast majority of tax powers remain reserved to the UK Government and Parliament. This, together with the operation of the Fiscal Framework, constrains what the Scottish Government can do in relation to tax policy.

The Scottish Parliament currently has devolved responsibilities in relation to five taxes:

- Scottish Income Tax is partially devolved – the Scottish Parliament is able to set the rates and bands for Scottish taxpayers on non-savings and non-dividend income, e.g. earnings from employment, self-employment, pensions or property. The personal allowance, reliefs and the rates and bands for savings and dividend income all remain reserved to the UK Parliament. Scottish Income Tax is administered and collected by HMRC on behalf of the Scottish Government.

- Land and Buildings Transaction Tax, a tax paid in relation to land and property transactions in Scotland, and Scottish Landfill Tax, a tax on the disposal of waste to landfill, are fully devolved national taxes and are managed and collected by Revenue Scotland.

- The Scottish Parliament also has powers over local taxes for local expenditure. Currently, the two main local taxes are Council Tax and Non-Domestic Rates (also known as business rates), which are collected by local authorities. Council Tax is set and collected by local authorities and does not form part of the funding of the Scottish Budget. The Scottish Government guarantees the resources available to local authorities through the combined total of Non-Domestic Rates income (NDRI) and General Revenue Grant (GRG) as an integral part of the Scottish Budget process. Local authorities retain all NDRI raised in their area and GRG allocations are adjusted to ensure each council receives their formula share of the settlement.

In addition:

- The power, provided in Scotland Act 2016, to introduce two further taxes has been devolved to Scotland, but these have not yet been implemented and the relevant reserved taxes therefore continue to apply. These taxes are Air Departure Tax, a tax on all eligible passengers flying from Scottish airports, which will replace Air Passenger Duty when introduced, and a devolved tax on the commercial exploitation of crushed rock, gravel, or sand.

- A portion of VAT revenues generated in Scotland is due to be assigned to the Scottish Budget, referred to as VAT Assignment. This is not a devolved tax power, as VAT policy remains reserved to the UK Government, and its implementation is dependent upon agreement between UK and Scottish Ministers regarding the methodology for assigning VAT receipts. The Scottish and UK governments have agreed to postpone VAT Assignment and revisit the issue during the review of the Fiscal Framework following the 2021 Scottish Parliament elections.

- The Scottish Parliament has the power to create new local taxes (i.e. to fund local authority expenditure). There is also a mechanism allowing the UK Parliament, with the consent of the Scottish Parliament, to devolve powers for new national devolved taxes to be created in Scotland. This is unlikely to be a swift process and depends on the complexity of the new national tax and negotiation over devolution of the requisite powers.

The Fiscal Framework

The funding arrangements agreed mean that Scotland’s budget position improves if tax receipts per head grow more quickly in Scotland than in rUK (and vice versa).

However, there are a number of factors which can affect Scotland’s relative tax performance, including:

- Growth in earnings, pensions, property income and house prices;

- Growth in the number of taxpayers or taxable transactions;

- Differences in the composition of the tax base;

- Policy changes and resulting changes to taxpayers’ behaviours.

The operational constraints of the Fiscal Framework also present additional challenges in the context of tax:

- The Block Grant Adjustment is based on forecasts, and the differences between forecasts and actual receipts do not come to light immediately. Differences in forecast and actual income tax revenues require adjustments three years later. For the fully devolved taxes, an in-year adjustment is made and a final adjustment is made two years later based on the outturn data.

- Borrowing powers are included in the Fiscal Framework to help manage the uncertainty of forecast errors and to fund the required reconciliations in future budgets; however, they remain limited in comparison to the scale of revenues and reasonable forecast error.

Better intergovernmental relations

With the vast majority of tax and macro-economic policy powers remaining reserved to the UK Government, UK policy decisions have a significant impact on devolved tax powers and performance. For example, the Medium Term Financial Strategy, published in January 2021, included calls for further tax powers to be devolved to Scotland to strengthen the Scottish Parliament’s economic levers in response to the pandemic.

More generally, the pivotal interaction between UK and Scottish Government policy is not yet adequately reflected in our governance arrangements. This is symptomatic of wider challenges in relation to intergovernmental relations between the UK Government and the devolved nations. It is therefore crucial that we increase our efforts to agree appropriate governance arrangements and improve trust, information sharing and collaboration at all levels.

The introduction of a formalised Devolved Administrations impact assessment for tax decision-making at a UK level would be a sensible starting point, together with appropriate governance structures that provide systems for policy development, consultation and advance notice and collaboration, allowing new or significant tax changes to be managed appropriately. The Finance Ministers’ Quadrilateral should be strengthened and regularised, meeting more frequently and ensuring that devolved and UK Governments can participate as equal partners in relation to tax policy decisions. This is and will remain a key strategic priority for the Scottish Government.