Social enterprise intermediary review: stakeholder views - research report

Results of research to understand the views of social enterprises and key stakeholders in the social enterprise sector regarding the role and nature of a new single social enterprise intermediary body.

2. Survey analysis: views of social enterprises

2.1. Respondent profile

In total, 151 organisations responded to the survey of social enterprises. A profile of the types of organisations that responded is set out in this section, with comparisons to the 2019 Social Enterprise Census where relevant data is available. According to this analysis, respondents to this survey tended to have larger annual turnovers than average, were more likely than average to be based in urban locations, and were less likely than average to operate only at a local level. This is important to bear in mind when interpreting the results of the survey, as the results reflect the views of this specific sample of social enterprises, rather than the total population of social enterprises.

Legal form of respondent organisations

Forty four percent of respondents were Companies Limited by Guarantee, 19% were Scottish Charitable Incorporated Organisations, and 17% were Community Interest Companies (Limited by Guarantee). Nine percent of respondents were Community Interest Companies (Limited by Shares). The remaining 11% of organisations was made up of a range of different types of legal form, with the most common being Community Benefit Societies (3%) and Trading Subsidiary or Charity/CIC (3%).

The sample is roughly similar to the responses to the 2019 Social Enterprise Census, suggesting that these organisations are relatively representative of the legal forms operating in Scotland.[2] This survey has a similar percentage of Companies Limited by Guarantee (44% compared with 43% in the census), but a higher percentage of SCIOs (19% compared to 11% in the census), and a lower percentage of Community Interest Companies (9% compared with 15%).

Size of respondent organisations

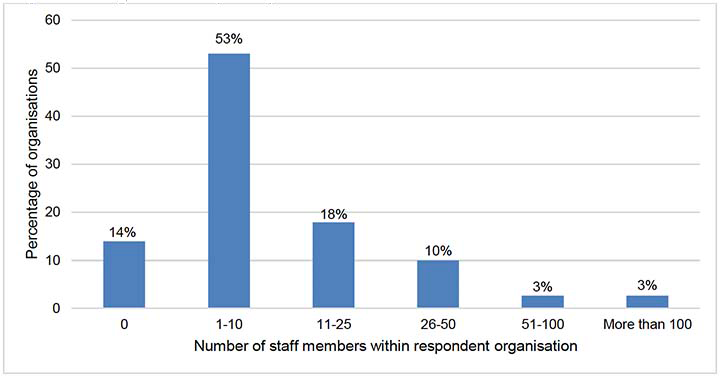

As shown in Figure 1, the majority of respondent organisations employed a relatively low number of staff, with 67% employing 10 people or fewer. This includes 14% of respondents whose organisations employed no staff. Twenty eight percent employed between 11 and 50 staff members, and only 6% of respondents employed more than 50 staff members.

Figure 2 breaks down the survey respondents by the annual turnover of their organisation. Most responses came from organisations with turnovers of more than £100,000 per year (55% of respondents). When compared with the 2019 Social Enterprise Census, where 45% of organisations reported income over £100,000, this suggests that the survey respondents are skewed towards higher-income organisations.[3] The most common turnover bracket was between £100,000 and £999,999 (41% of respondents), while 14% reported an annual turnover of more than £1 million.

Forty-five percent of organisations reported turnovers lower than £100,000. This included:

- 25% of organisations reporting turnover of £25,000 to £99,999

- 7% reporting turnover of £10,000-£24,999

- 13% reporting turnover lower than £10,000.

Where respondents operate

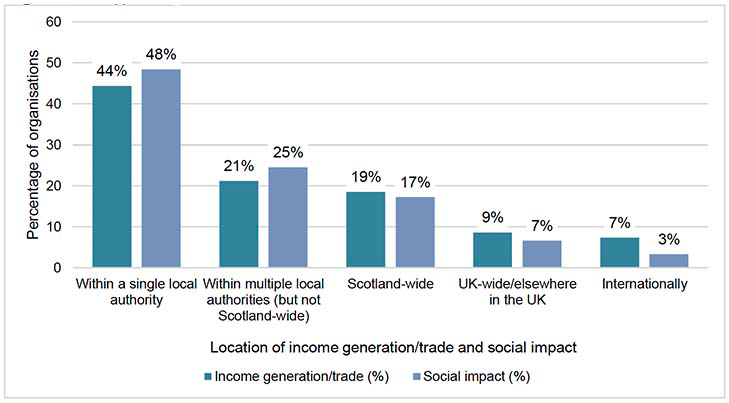

As indicated in Figure 3, respondents tended to be local organisations, with 44% conducting their income generation/trade within a single local authority area, and 48% focusing their social impact on a single local authority area.

Sixteen percent of respondents conducted trading/income generation activities either UK-wide or internationally, and 10% focused their social impact UK-wide or internationally.

Compared with the 2019 Social Enterprise Census, these data suggest that the respondent organisations are slightly skewed towards those operating on a larger geographical scale, rather than locally. The census asked about the "widest geography across which social enterprises operate", and showed that 57% report operating within a single local authority area or within a single neighbourhood/community, a higher percentage than reported doing so for either income generation or social impact in this survey. While a similar percentage to the 2019 census reported working within multiple local authorities (21% in the 2019 census), slightly higher percentages reported operating Scotland-wide (11% in the 2019 census) and across the UK (3% in the census).

Rural/urban location

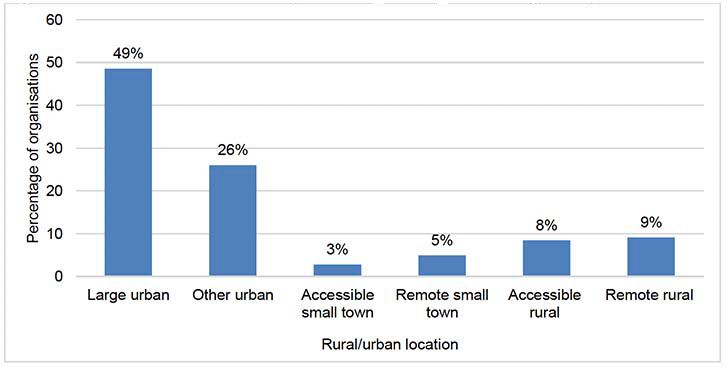

When comparing with the 2019 Social Enterprise Census results, this sample appears to be skewed towards larger urban areas.[4] As shown in Figure 4, the majority of respondents were based in "large" or "other" urban locations (75%), including 49% based in large urban areas (settlements with populations of 125,000 or more).[5] This suggests a higher concentration of urban social enterprises than average; in the 2019 census, only 55% of organisations were based in large or other urban areas.

The remaining respondents were split between those based in remote rural areas/small towns (14%) and those in accessible rural areas/small towns (11%). While a total of 25% of organisations fall into these four categories in this survey, in the 2019 census 45% of respondents did so.

Membership of current social enterprise intermediaries

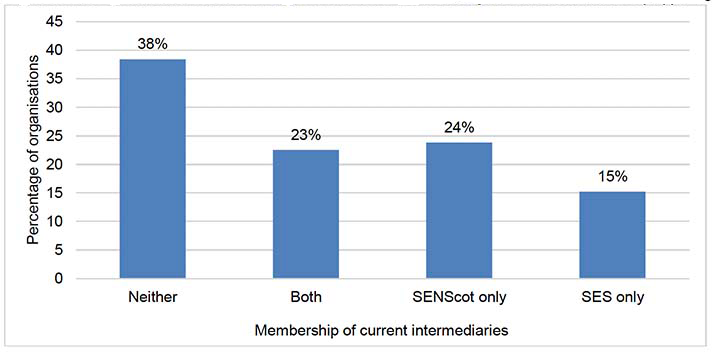

Respondents were asked to specify whether they were currently members of either of the two current social enterprise intermediary bodies, and the results are provided in Figure 5. The majority of respondents (62%) were a member of at least one intermediary body, and 23% were members of both.

In total, 46% of respondents were members of SENScot, while 38% were members of SES. Given that most social enterprises are not members of either intermediary body, this survey has a disproportionately high number of responses from current members.

2.2. Social enterprises' views on the development of the single intermediary

Concerns about the development of a new intermediary

A number of survey respondents expressed scepticism or opposition to the creation of a single intermediary, with organisations questioning whether it is worth the time and cost when similar functions might be better-handled by existing organisations.

Some respondents argued that the creation of a single intermediary would be a negative step. Given the current differences in the focus and emphasis of the two existing intermediaries, some respondents argued that having a single body risks side-lining certain voices and opinions in favour of a single, dominant voice. As has already been highlighted, the main concern here is that certain organisations will not feel represented by the new single intermediary. Others, however, expressed hope that the creation of the new intermediary would be a positive step in bringing together – and mediating – opposing views within the sector.

Finally, some organisations raised concerns about the intended function of the single intermediary. Several respondents did not think that the intermediary body should act as a service provider, and instead wanted to emphasise the importance of the intermediary as a networking and policy-influencing organisation.

Reasons for not joining an intermediary organisation

Organisations that are not currently members of either intermediary were asked the reason for this. As shown previously in Figure 5, 38% of respondents (58 organisations) were not currently members of either social enterprise intermediary body.

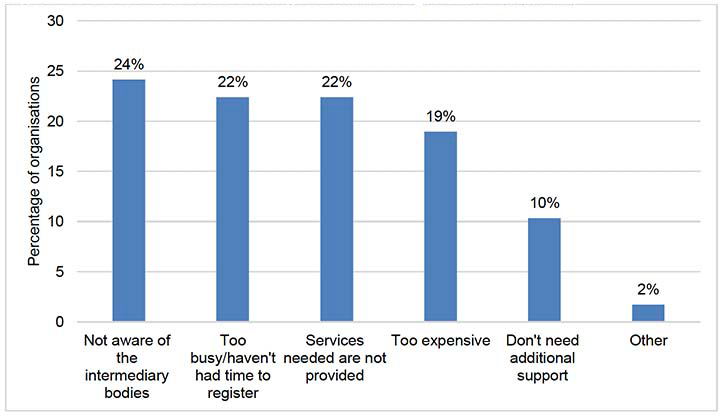

Figure 6 breaks down the most common reasons for not being a member of either body. It shows that the most common reason for this was that the organisation was not aware of the intermediary bodies (24%). This suggests that the new intermediary will need to work to better-publicise itself to social enterprises. This lack of awareness of the intermediary bodies also suggests that the low survey response rate could in part be related to a wider lack of awareness of the intermediaries.

Twenty-two percent of respondents said that they were too busy or had not had time to register. Another 22% felt that the services they needed were not provided by the intermediaries, while 19% found membership too expensive, and 10% said that they did not need any additional support (Figure 6).

Views on fees

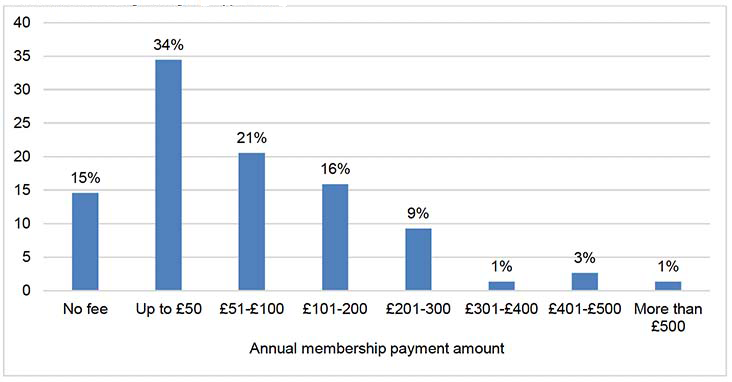

Figure 7 provides information about how much organisations would be willing to pay for annual membership of the new intermediary body. Overall, the vast majority of respondents (85%) said that they would be willing to pay an annual membership fee to join the intermediary body, including 83% of organisations that are not currently members of either intermediary.

The most popular response was that organisations would be willing to pay a fee of up to £50 per year (34%). This was more common among organisations that are not currently members (41%) than among those that are already members (30%). Given that the majority of social enterprises in Scotland are not members of either intermediary, this suggests that keeping the payment below £50 would encourage a greater number of members to sign up to the new intermediary.

Figure 7 also shows that 21% of respondents were willing to pay £51-£100 per year, while 16% were willing to pay £101-200. Relatively few organisations were willing to pay more than £200 per year (14%).

Fees by size of organisation

The amount that organisations would be willing to pay is linked to some extent to the size of the organisation's annual turnover. Smaller organisations (those with a turnover lower than £25,000 per year) were the least likely to be willing to pay a membership fee, with 17% saying they would not. Sixty-three per cent of these organisations said that they would be willing to pay the lowest membership fee suggested (up to £50 per year), while the remaining 20% were willing to pay between £51-100. None were willing to pay more than £100 per year.

Medium-sized organisations (annual turnover between £25,000 and £99,999) were the most likely to be willing to pay a membership fee, with only 11% saying that they would not. The majority of these organisations were willing to pay a relatively low annual fee, with 50% saying they would pay up to £50 per year, and 21% saying they would pay £51-100. 19% were willing to pay over £100 per year.

The largest organisations (annual turnover of £100,000 or more) were generally more willing to pay more for annual membership than smaller organisations. Seventeen percent of these organisations said that they would be willing to pay up to £50 per year, 23% said that they would be willing to pay £51-£100. Forty-five percent were willing to pay more than £100 per year, including 21% that were willing to pay more than £200 per year. Sixteen percent were not willing to pay for membership.

Definition of social enterprise

Where survey respondents were asked to provide open-text comments on the new intermediary, a common theme was the question of what types of organisations the intermediary body should open up its membership to. Of the organisations that commented on this, there was a clear split between those that felt membership should be broad and inclusive of a wide range of legal forms, and those that felt membership should be limited to a smaller range of legal forms.

Those arguing for a broad membership tended to do so on the basis that all businesses working towards social impact and a wellbeing economy have an important role to play, regardless of their legal status. As two separate respondents commented:

"The single intermediary body should work for the widest possible range of social enterprises, and be a broad church to include mission driven businesses, B Corps and all those who are working towards a wellbeing economy."

"Personally, I would question whether the value of social enterprise is found in its organisational form or is it rather in the [social] impact delivered?"

They felt that the Voluntary Code of Practice for Social Enterprise in Scotland, which some organisations currently use to define social enterprises, excludes organisations which make important contributions to the social good in Scotland. It was also argued that organisations which allow part-profits or dividends should be included as this is often the only way for small organisations to attract small investors with relatively low risk. This was seen by some as important in order to reduce the sector's reliance on grant funding.

On the other hand, some organisations argued for continuing to exclude any organisations with profit-making potential from the definition of social enterprise, arguing that widening the definition would "water down" and "undermine" the identity of the social enterprise sector, and risk allowing private businesses with a social mission to identify as social enterprises. As one organisation commented:

"There has been lots of talk of watering down what social enterprise is in Scotland with 'social business' b-corps and other 'social enterprise light' models getting more attention. I'd want to know that the representative body is representing social enterprise and not these other weaker models that potentially undermine what we are about."

Others raised concerns about the possibility of more traditional social enterprises losing out on grant funding and rates relief if their social enterprises were to be seen as on an equal footing with profit-making businesses:

"The national intermediary needs to be clear about who it is there for – current trends to call any business a social enterprise if it says it is there to "do good" raises real issues for funders, local authorities and potentially the public. Arguably, lots of business would be able to assert a claim over the description "social enterprise" on that basis, and seek grants, rate relief and so on. We want to see asset locks and other ways of preventing profit distribution in social enterprises and a national intermediary supporting and promoting those types of organisations".

As all these comments make clear, the question of how the single intermediary will define social enterprises is a concern for some members of the social enterprise community, and there is a very clear divide between those advocating for a "broad church" approach, and those advocating for a more exclusive approach.

One respondent felt that the most important job of the social enterprise intermediary was to play a mediating role in this debate, bringing together people and organisations on both sides of the argument in order to reduce the polarisation of the sector and allow the two groups to learn from each other. As they argued:

"[We need] less polarisation of [the debate between] community good, profit bad! Both can learn from each other and there is room and need for a range of social enterprises".

2.3. Types of support that social enterprises want the single intermediary to provide

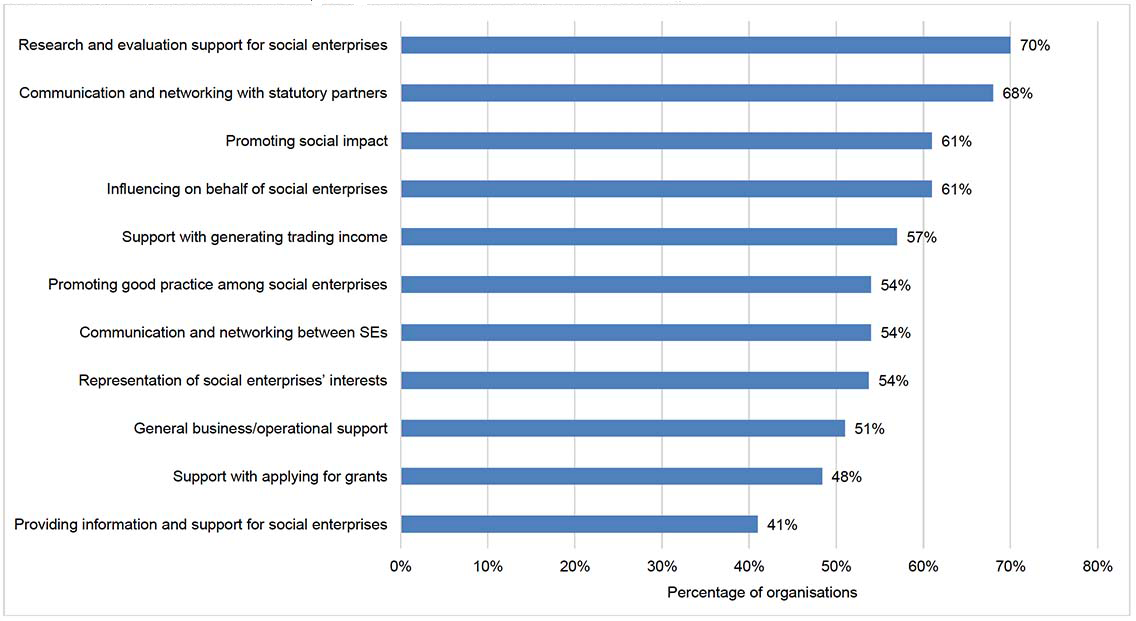

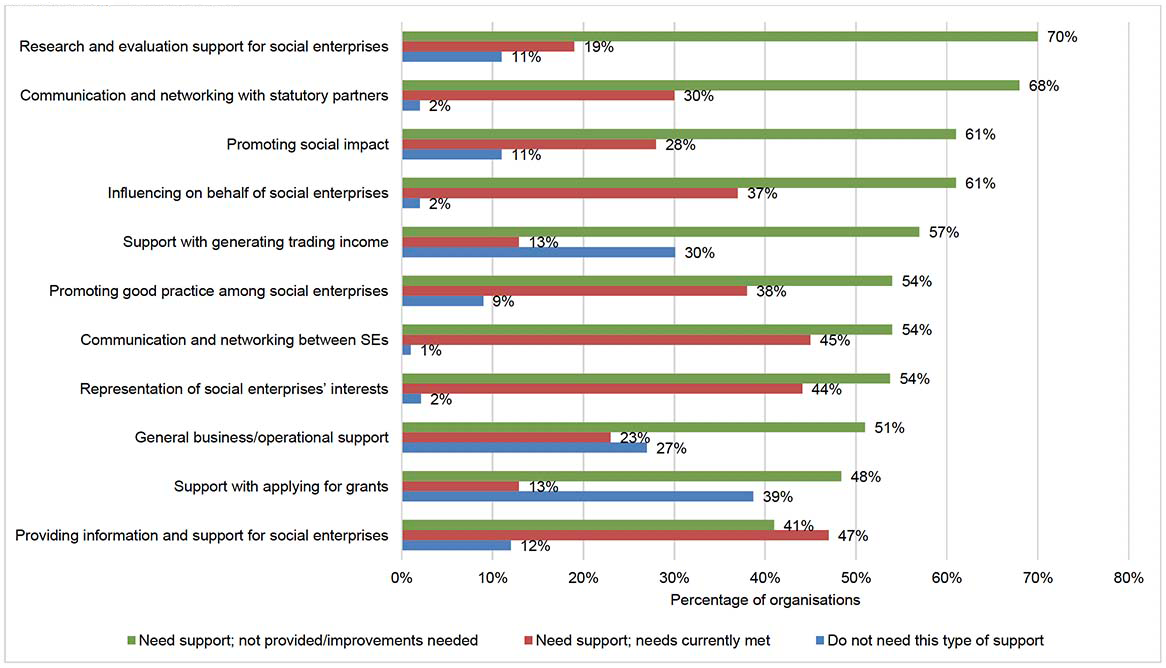

The survey asked social enterprises whether they felt that the new intermediary should provide services for social enterprises in 11 specific areas, as detailed in Figures 8, 9 and 10. Social enterprises that are currently members of at least one intermediary were asked about current provision in relation to their needs.

Figure 8 provides a breakdown of the proportion of organisations indicating that they needed support in each of these 11 areas, and saying that support is either not currently provided or needs to be improved to meet their needs. Figure 10 shows the total proportion of organisations indicating that they need support in each area, including those that said their needs were being met and those that said the current support was not sufficient. Figure 9 shows all the responses.

As Figures 8 to 10 show, the majority of respondents that are currently members of an intermediary reported a need for support in all 11 areas. Ninety-nine percent of respondents said they needed support with communication and networking between social enterprises, while 98% said that they needed support with communication and networking between social enterprises and statutory partners. Influencing on behalf of social enterprises, representation of social enterprises' interests were both very high priorities, with 98% of respondents saying that they needed support in these areas.

A significant proportion of respondents felt that the current provision needed to be improved in each area in order to meet their needs. The areas where the largest proportion of organisations said that there was a need for improvement or that the service was not currently provided were:

- research and evaluation support (70%)

- communication and networking with statutory partners (68%)

- influencing on behalf of social enterprises (61%)

- promoting social impact (61%).

As shown in Figures 9 and 10, organisations suggested that they were least in need of provision of support with applying for grants, support with generating trading income, and general business/organisational support, although the majority still stated that these were needed. Thirty nine percent of organisations said that they did not need support with applying for grants, 30% did not need support with generating trading income, and 27% did not need general business/operational support.

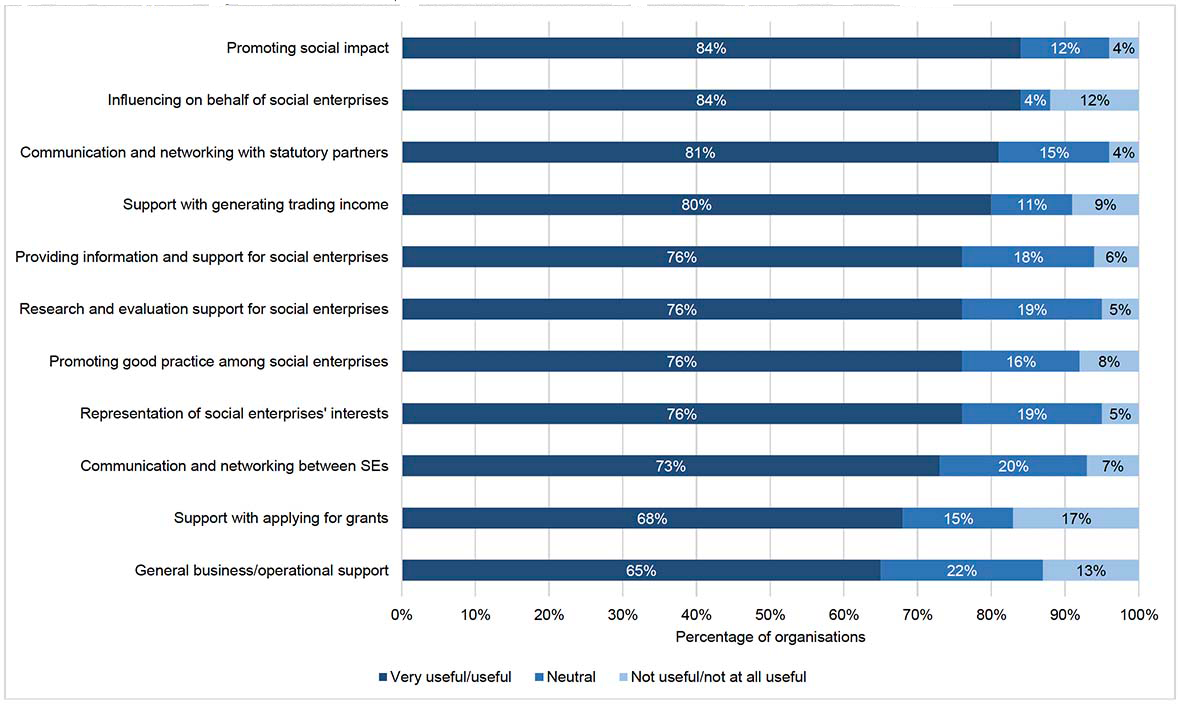

Social enterprises that are not currently members of either intermediary were asked whether it would be useful for the intermediary to provide services in the same 11 areas. The results are provided in Figure 11.

Among organisations that were not currently members of an intermediary, the priorities were slightly different than those of organisations that were currently members. Figures 10 and 11 show that a higher proportion of non-members than members indicated that they would find support with generating trading income useful (80% of non-members said this would be useful, compared with 70% of current members who said that they need this type of support).

Similar to current members, among non-members, applying for grants (68%) and general business/operational support (65%) were the areas where the fewest organisations suggested that they would find support useful.

Non-members showed the most support for:

- influencing on behalf of social enterprises (84%)

- promoting social impact (84%)

- communication and networking with statutory partners (81%)

- generating trading income (80%).

In this section, the survey results for each of these areas are discussed in more detail in turn.

Support for communication and networking between social enterprises

The majority of respondents saw support for communication and networking between social enterprises as being an important role that the intermediary should be playing. Of those organisations which are currently members of an intermediary, 45% answered that their needs in this area are currently met. Thirty-three percent said that they need support in this area and would like to see the support improved to better meet their needs, while 20% said that they need support in this area but it is not currently provided. Only 1% reported that they don't need this type of support.

Of those organisations which are not currently members of an intermediary, 73% said that they would find this type of service "useful" or "very useful". Seven percent said that it would not be useful.

For many respondents, support with communication and networking between social enterprises was the primary role they felt the proposed single intermediary should fulfil. Among the comments, organisations emphasised the importance of encouraging and supporting peer learning, peer support, collaboration with other social enterprises, and forums for sharing ideas and examples of best practice. One respondent also suggested that there is a need for the intermediary to help facilitate this type of networking and collaboration beyond Scotland, supporting Scottish social enterprises to network and collaborate with other social enterprises across the UK and internationally.

Promotion and support for communication and networking between social enterprises and statutory partners (e.g. Scottish Government, local authorities)

Of those organisations which are currently members of an intermediary, 39% answered that they need support in this area and would like to see the support improved to better meet their needs. Thirty percent said that their needs in this area are currently met, while 29% said that they need support in this area but it is not currently provided. Only 2% said that they don't need this type of support.

Of those organisations which are not currently members of an intermediary, 81% answered that they would find this service "very useful" or "useful". Four percent said that they would not find it useful.

Organisations commented that there was a need for better links with a range of statutory bodies beyond the Scottish Government. As one respondent suggested, there is need for:

"…better links into other Scot Gov agencies and organisations such as the NHS, Skills Development Scotland, enterprise agencies and climate agencies"

Several respondents expressed a need for help in interpreting national and local policies, deciphering what various decisions will mean for practitioners on the ground, and disseminating this information clearly throughout the sector as a whole.

Representation of social enterprises' interests

Representation of social enterprises' interests was another of the key areas where respondents most felt that the intermediary should provide support. Of those organisations which are currently members of an intermediary, 44% answered that they need support in this area and would like to see the support improved to better meet their needs, and a further 44% suggested that their needs for this service are currently being met. Ten percent answered that they need support in this area but it is not currently provided. Only 2% of respondents did not want this type of support.

Of those organisations that are not currently members of an intermediary, 78% answered that they would find this service "useful" or "very useful". Only 5% did not feel that it would be useful.

Many respondents commented that there is a need for greater advocacy on behalf of social enterprises which fully involves grassroots members in co-producing support schemes and influencing policy decisions. As one survey respondent commented:

"This initiative [representing social enterprises' interests] would only be effective with a grass-roots focussed support scheme. In all cases we would like to see support to be co-produced with social enterprises operating on the ground and any intermediary being rooted and established within the sphere of social enterprise practitioners."

Respondents also stressed a need for the intermediary to pay greater attention to local knowledge, and to encourage greater collaboration across the sector. Several felt that the current approaches are too centralised and top-down, as one respondent commented:

"I think there is a real benefit to having local knowledge and connections as an intermediary body, so managing the scale of a single intermediary and the level of reach is a fine balancing act. It needs to bring existing groups together rather than centralising services to the point where people don't feel it's for them."

Influencing on behalf of social enterprises

Similar to representation of social enterprises' interests, this was an area where most social enterprises felt that there is a need for support from the intermediary. Of those organisations that are currently members of an intermediary, 48% answered that they need support in this area and would like to see the support improved to better meet their needs, while 37% said that their needs in this area are currently met. Thirteen percent felt that they need support in this area but it is not currently provided. Only 2% reported that they don't need this type of support.

Of those organisations which are not currently members of an intermediary, 84% answered that they would find this service "very useful" or "useful", while 12% would not find it useful.

Social enterprises felt that it is important that the intermediary influences policy on their behalf, and many of the comments suggested a desire for improved support in this area. As highlighted in earlier sections, some felt that there is currently a lack of engagement with the social enterprise sector on policy issues, meaning that social enterprises do not always feel that their views are being taken into account in policy discussions and decisions. As one respondent commented:

"Whilst we accept that there is a good level of support for social enterprises provided in Scotland, we often see little engagement with actual social enterprises to determine what support should be given".

Promoting good practice among social enterprises

Of those organisations which are currently members of an intermediary, 41% answered that they need support in this area and would like to see the support improved to better meet their needs, while 38% answered that their needs in this area are currently met. Thirteen percent said that they need support in this area but it is not currently provided. Nine percent said that they do not need this type of support.

Of those organisations which are not currently members of an intermediary, 76% answered that they would find this service "useful" or "very useful". Eight percent said that it would not be useful.

Many organisations would like the new intermediary to focus on bringing organisations together to share best practice ideas. Others also commented that it would be useful if the intermediary offered signposting and advice relating to specialist services. As one respondent commented:

"It would be beneficial for the single intermediary to support with signposting, good practice, case studies, successful scale up stories, [and] encouraging something like 'trusted traders' for different areas of your social enterprise e.g. HR, Finance, Insurance."

Promoting social impact

Of those organisations which are currently members of an intermediary, 42% answered that they need support in this area and would like to see the support improved to better meet their needs. Twenty eight percent said that their needs in this area are currently met. 19% said that they need support in this area but it is not currently provided; and 11% said that they don't need this type of support.

Of those organisations which are not currently members of an intermediary, 84% answered that they would find this service "useful" or "very useful", while 4% felt that it would not be useful.

In the comments, a number of organisations highlighted a need for greater support with measuring and demonstrating social impact. For example, some organisations felt that it was more challenging for their organisation to demonstrate their social impact than others, and that this could affect their ability to attract funding. As one respondent commented:

"Measuring Social Impact of very high impact on a few people seems to be valued less [while] short term impact on a lot of people seems to be valued more – Understanding how to demonstrate the impact would be great."

Research and evaluation support for social enterprises

Of those organisations which are currently members of an intermediary, 47% answered that they need support in this area and would like to see the support improved to better meet their needs, while 23% reported that they need support in this area but it is not currently provided. Nineteen percent said that their needs in this area are currently being met, and 11% that they don't need this type of support.

Of those organisations which are not currently members of an intermediary, 76% answered that they would find this service "useful" or "very useful" and 5% reported that they would not find it useful.

While there is clearly some desire for this type of support, no organisations elaborated on these needs in the comments. It is therefore unclear exactly what sort of research and evaluation support organisations feel that they would benefit from, and this may be something for the new intermediary to explore further.

Providing information and advice for social enterprises

Of those organisations that are currently members of an intermediary, 47% answered that their needs in this area are currently met, 32% said that they need support in this area and would like to see the support improved to better meet their needs, and 9% said that they need support that is not currently provided. Twelve percent reported that they do not need this type of support.

Of those organisations which are not currently members of an intermediary, 79% answered that they would find this service "useful" or "very useful". Six percent said that they would not find this type of service useful.

Clarity, consistency, and accessibility of information were the main issues expressed by most respondents on this topic. Some organisations felt that information within the sector is currently quite "muddled", with significant overlap in services and conflicting sources of information. As two separate respondents commented:

"Support has to be consistent. Too many times you get advice from one staff member which can be completely different to the advice to the exact same question from another staff member".

"From a local social enterprise perspective, having much greater clarity about support and communication routes would be a significant benefit".

As such, respondents asked for clear and precise information from a single, reliable source, regularly communicated to organisations operating at local level.

General business/operational support for running a social enterprise

Of those organisations that are currently members of an intermediary, 38% answered that they need support in this area and would like to see the support improved to better meet their needs; 23% said that their needs are currently being met. Thirteen percent said that they need support in this area but it is not currently provided. Twenty-seven percent said that they do not need this type of support.

Of those organisations that are not currently members of an intermediary, 65% answered that they would find this service "useful" or "very useful", while 13% would not find it useful.

For the organisations which would like to see this kind of support, comments largely related to wanting support with specialist services such as legal, financial, IT and HR services. In particular, respondents asked for help in signposting to professional service providers that can offer reliable services at affordable rates. As one respondent commented:

"For us it would be specialist support-based services such as HR services, identification of suppliers who provide preferential rates, signposting to training and development opportunities to build capacity, with experts from specialist areas".

Others highlighted a need for training for the day-to-day running of the business as a primary need:

"We would require someone who is dedicated in giving advice on grant funding and the day to day running [of the social enterprise], and planning for the future to ensure sustainability".

Some organisations highlighted that any support offered should be tailored to individual organisations, and should not be provided via single, standardised one-size-fits-all support packages. As one respondent commented:

"We would benefit from more tailor-made support for our social enterprise. A lot of what is provided for everyone doesn't take our unique situation into account, and a lot of help/advice is too general, or is one we have already followed up."

Support with generating trading income

Of those organisations that are currently members of an intermediary, 36% answered that they need support in this area and they would like to see the support improved to better meet their needs. Twenty-two percent said that they need support but it is not currently provided, and 13% that their needs for this service are currently being met. Thirty percent said that they do not need this type of support.

Of those organisations which are not currently members of an intermediary, 80% said that they would find this type of service "useful" or "very useful", while 9% said that they would not find it useful.

Several organisations stated that there is a gap in supporting social enterprises with income generation. Some suggested there should be more hands-on intensive support in product development and trading, while others stressed the need for social enterprises to be given greater support to become viable trading businesses. As one respondent explained:

"[The intermediary should] support the financial sustainability and professionalisation of social business so that it can compete with 'for profit' business in Scotland. I feel energy, resource and focus is often split to ensure social impact remains at the forefront of activity."

As indicated in this comment, however, others see the intermediary's role as primarily to focus on social impact, rather than trade and financial sustainability.

Support with applying for grants

Of those organisations that are currently members of an intermediary, 29% said that they need help in this area and would like to see improvements to the current support, while 19% said that they need support but it is not currently provided. Thirteen percent said that their needs in this area are currently being met and 39% answered that they do not need this type of support.

Of those organisations that are not currently members of an intermediary, 68% said that they would find this type of support "useful" or "very useful". Seventeen percent said that it would be "not useful" or "not at all useful".

Requests for this type of support were most commonly in relation to helping new start-up businesses through the difficult early stages towards becoming viable. In particular, a desire was expressed for greater links to programmes which can fund and support growth within the sector. For example, one respondent commented that there was a need for:

"Help with grant funding applications until the organisation feels able to sustain this themselves. Better links with statutory and direct help for organisations across the first 5 years of set up perhaps on a tiered package offer."

Others suggested a need for greater assistance in applying for grants. Again, this was largely a concern for smaller, more localised and/or newer organisations. Some of these noted that it can be a difficult challenge to navigate the various sources of funding and compete for these against larger, more prominent and better resourced organisations.

Contact

Email: socialresearch@gov.scot