Scottish greenhouse gas emissions annual target report: 2015

This is a report required under the Climate Change (Scotland) Act 2009. It provides detail on the annual climate change emissions reduction targets.

Annex

Accounting For The EU Emissions Trading System ( EU ETS)

Introduction

This annex outlines the calculation of adjusted emissions to take account of trading in the EU Emissions Trading System ( EU ETS).

What is the EU ETS?

The EU ETS is a 'cap and trade' system. A limit (cap) is placed on the overall volume of emissions from participants in the system. Within the cap, organisations receive or buy emissions allowances which they can trade (1 emissions allowance equals 1 tCO 2e). Each year, an organisation must surrender enough allowances to cover its emissions. The cap is reduced over time so that by 2020, the volume of emissions permitted within the system will be 21 per cent lower than in 2005. The reducing cap, alongside the financial considerations of trading emissions allowances, incentivises organisations within the system to find the most cost effective way of reducing their emissions. The EU ETS operates as a number of Phases. Phase III began on 1 January 2013 and will operate until 31 December 2020.

In the greenhouse gas inventory, source emissions can be categorised into traded and non-traded. Traded emissions capture those that come from installations covered by the EU ETS, whereas non-traded emissions are those which do not fall within the scope of the EU ETS. The emissions from some sectors, such as the residential sector, are completely non-traded whereas emissions from other sectors, such as energy supply, business and industrial process emissions are a combination of traded and non-traded. For the years 2012 to 2015, CO 2 emissions from domestic and international aviation are classified as being within the traded sector.

What does this mean for the NSEA?

The figure for source emissions is comprised of emissions from both the non-traded and traded sectors. The figure for the NSEA is comprised of emissions from the non-traded sector and a value for Scotland's share of the notional EU ETS cap. The amount of emissions from the non-traded sector remains the same for both the source emissions and the NSEA.

The EU ETS element of the NSEA is calculated by replacing the number of emissions allowances surrendered from Scottish installations in a given year with Scotland's notional share of the overall EU ETS cap. This involves taking the difference between Scotland's notional share of the overall EU ETS cap and the number of emissions allowances surrendered from Scottish installations in a given year. This difference is then added to net Scottish emissions to get the NSEA.

The NSEA is referred to as "adjusted emissions", as they are adjusted to take into account trading within the EU ETS and the purchase of other credits. As no units were credited to the NSEA in 2015 as a result of the purchase by Ministers of international carbon units, this adjustment takes the form of a 4-step process.

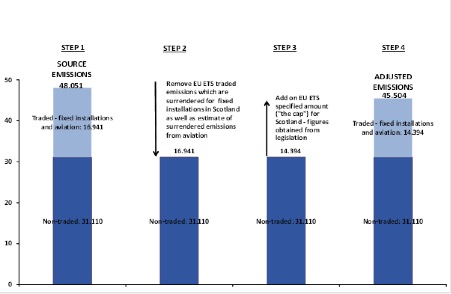

Calculation of adjusted emissions for 2015

STEP 1

Take the Scottish greenhouse gas emissions from Scottish greenhouse gas inventory (for 2015, it is 48.051 MtCO 2e). This figure is comprised of:

- traded emissions units surrendered - sourced from Scottish Environment Protection Agency ( SEPA) for fixed installations (15.132 MtCO 2e)

- an imputed estimate of surrendered CO 2 emissions from domestic aviation (0.507 MtCO 2e) and international aviation (1.303 MtCO 2e) - sourced from the Scottish Greenhouse Gas Inventory for 1990 to 2015

- non-traded emissions from sources such as residential emissions (31.110 MtCO 2e)

STEP 2

Remove an amount relating to surrendered emissions from fixed installations and an estimate of surrendered emissions from domestic and international aviation. This amounts to 15.132 MtCO 2e + 0.507 MtCO 2e + 1.303 MtCO 2e = 16.941 MtCO 2e.

STEP 3

Add on the value of the EU ETS cap which is outlined within The Carbon Accounting Scheme (Scotland) Amendment Regulations 2017 [43] . The cap reflects an estimate of the Scottish share of the European wide EU ETS cap that is used for emissions accounting.

The Scottish EU ETS cap for 2015 is 14.394 MtCO 2e, and is made up of 3 components, as shown in the table below. A methodological paper, Determining a Scottish EU ETS cap for 2015 [44] , documents the calculations that determine how a notional emissions cap has been calculated.

Table 14. Total EU ETS cap for Scotland, 2015 - this is the "specified amount" for fixed installations, domestic aviation and international aviation - as outlined in The Carbon Accounting Scheme (Scotland) Amendment Regulations 2017

| Component |

2015 Allocation tCO 2e |

|---|---|

| Fixed Installation Cap |

13,029,411 |

| Domestic Aviation Cap |

443,255 |

| International Aviation Cap |

921,758 |

| Total 2015 Cap |

14,394,424 |

STEP 4

Adding on the value of the EU ETS cap gives a value of 45.504 MtCO 2e.

In 2015, the adjusted emissions which take account of trading in the EU ETS is 45.504 MtCO 2e. This is 2.547 MtCO 2e lower than the value of estimated source emissions in 2014. Under the Climate Change (Scotland) Act 2009, a downward adjustment to source emissions is referred to as a credit to the Net Scottish Emissions Account. This means that 2,546,649 units have been credited to the Net Scottish Emissions Account in 2015.

Chart 3. Calculation of Adjusted Emissions for Trading in the EU Emissions Trading System ( EU ETS), 2015. Values in MtCO 2e