Scottish economic insights: November 2023

Further analysis and insights on the economic themes presented in the monthly Scottish economic bulletin report.

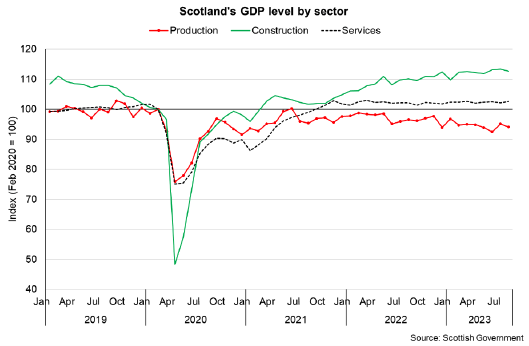

Weakness in Economic Growth

The Scottish economy has proven resilient in 2023 having previously been forecast to fall into recession during the year. This has not happened, however there is an underlying weakness in economic growth with GDP growth remaining broadly flat since the start of 2022 with latest data for August showing growth of 0.1% over the past year.[9]

This reflects a stalling in the recovery from the pandemic as the economic output has remained broadly unchanged at 1.8% above its pre-pandemic level since the start of 2022.

Output growth has varied across sectors over the past year with growth in the services (0.5%) and construction (2.3%) sectors offset by a fall in production output (-2.5%). This pattern is even more pronounced when comparing back to pre-pandemic levels in which construction is 12.7% above its pre-pandemic level and services is 2.7% above, while the production sector is 5.9% below.

The legacy impacts from the pandemic - from the restrictions that had been in place alongside the disruption in global supply chains - were very much key factors in the differences in sector growth leading into 2022.

However since then, the inflation shock, tightening monetary policy (their impact on demand) and the cumulative impacts on economic confidence and risks mean that these factors have had an increasingly significant role over the past year.

In the services sector, this is evident when considering how different parts of the sector have grown over the past year and how their output compares to their pre-pandemic level. Despite the inflationary pressures over the past year, growth has been resilient in some of the more consumer facing services sectors such as Accommodation and Food Services and Arts, Culture and Recreation, while Wholesale and Retail output has contracted.

However, output from Accommodation and Food and Wholesale and Retail remain below their pre-pandemic level of output in February 2020, reflecting the combined impact (alongside other factors) that the succession of shocks from the pandemic and inflation have had on these sectors.

Financial and Insurance activities output contracted over the past year and are only marginally above their pre-pandemic level of output. In contrast, services sectors that have grown more strongly over the past year and have recovered to notably above their pre-pandemic levels include Information and Communication and Professional, Scientific and Technical services.

Looking at the production subsectors provides insight on why the sector has contracted over the past year and remains below its pre-pandemic level of output. Apart from the growth in water supply and waste management sector, the other parts of the production sector have seen falling output over the past year and when compared to pre-pandemic levels.

Manufacturing, which makes up 10% of Scotland's total GDP and 66% of the production output has contracted by 2.7% over the past year and is 1.2% below its pre-pandemic output level, while Mining and Quarrying and Electricity and Gas Supply are more significantly below their pre-pandemic levels (-21.6% and -21.7% respectively). Mining and Quarrying in Scotland is dominated by oil and gas support services, including exploration and drilling, which has seen low levels of activity since 2020. Electricity and Gas is volatile, with recent low output due to a combination of good weather conditions (low renewable generation) and maintenance at other power stations.

Scotland’s Gross National Income

In June 2023, the Scottish Government published provisional estimates up to 2021 of Scotland’s Gross National Income (GNI).

GNI complements GDP as a measure of economic activity. While GDP is a measure of how much income is generated in a country through the production of goods and services, regardless of whether it accrues to residents, GNI is a measure of how much income the residents of a country receive.

As such, the value of GNI is equal to GDP plus the net income from overseas sources such as cross border employee earnings and property income such as interest, dividends and other returns on investment. For Scotland, the estimated value of GNI accounts for net income from both the rest of the UK (RUK) and the rest of the world (ROW).

The Primary Income Account provides the estimates of the flows of primary income into and out of Scotland, based on the ownership of economic assets. Income flows into Scotland’s Primary Account from earned income and returns on investment from Scottish owned overseas assets, while overseas owned assets in Scotland generate outflows from the Primary Account.

In 2021, Scotland’s Primary Income Account showed a net outflow of £10.1 billion, or 5.6% of GDP. As such Scotland’s GNI, including a geographical share of UK extra-regional activity, is estimated at £170.8 billion, or 94.4% of Scotland’s GDP of £181.0 billion.

Looking over the longer term, every year between 1998 and 2021, Scotland’s primary income debits (flows of income from Scotland to investors in RUK and ROW) have been higher than credits (flows of income into Scotland), creating a primary income deficit (or a negative net balance).

As such, Scotland’s GNI has remained below GDP throughout the period from 1998 to 2021, reflecting the primary income deficit over this period. The gap is estimated to have narrowed since its largest estimated value in 2008 in which the primary income deficit was -£17.8 billion. On average, between 1998 – 2007, GNI was 90.6% of GDP, increasing to 92.5% between 2008 – 2021.

The primary income account deficit is driven by a range of factors including relatively high levels of foreign ownership among Scottish industries and a relatively low proportion of UK companies having headquarters in Scotland, particularly in the oil and gas and financial services sectors.

In 2021, the majority of the income flows made a negative contribution to the Primary Income Account and GNI. The largest outflow was returns on direct investment (-3.2% of GDP) followed by portfolio investment from debt securities (-1.4%) and equity securities (-0.7%).

Since 1998 the gap between GDP and GNI has been largely driven by direct investment. Net contributions of other investment flows had also made a large negative contribution to net Primary Income, however this has reduced in more recent years.

For Scotland, the estimated value of GNI accounts for net income from both the rest of the UK (RUK) and the rest of the world (ROW). Since 2008, Scotland has a net primary account deficit (net outflow) with both RUK and the ROW.

Since 2010, the deficit with the ROW has been notably larger than for the UK, apart from in 2020 during the pandemic when there was a sharp fall in the deficit across the board. This has predominantly been driven by a decrease in the net deficit of other investment with RUK coupled with an increase in the net deficit with the ROW on portfolio investments of equity securities.

Outflows to RUK, returns on investment, were higher in the years leading up to the 2007-2008 financial crisis but have been estimated to be lower since, with the results of the latest years including the impacts of the pandemic.

Overall, the GNI measure provides a valuable insight on the domestic economic wealth of Scotland. Although GNI has remained below GDP throughout 1998 to 2021, the gap has slightly narrowed from 2008 onward. In recent years, volatility in direct investment income flows has been dominant, and reflects both the economic disruptions during the pandemic and corporate financial management strategies of companies operating in Scotland.

Looking ahead, the fall in inflationary pressures should present opportunities for growth, however conditions continue to remain challenging for businesses and households as they continue to adjust to higher prices, higher interest rates and are increasingly concerned about weakening demand.

Business investment grew over 2022 as investment recovered from a sharp fall during the pandemic. The pace of growth slowed over the year, however picked up in the second quarter of 2023 growing 4.7% on a rolling four quarter basis. Furthermore, business investment in Q2 2023 had grown 11.3% over the year and is 9.4% above the pre-pandemic level in Q4 2019.

However business surveys indicate that business investment intentions have stagnated during the year. The Scottish Chambers of Commerce Quarterly Economic Indicator reported for Q3 2023, that while on balance, more firms continued to report increases in investment than falls, over half (55%) reported no changes to total investment with this rising to 57% for training investment. Both are five-year highs for the survey.[10]

Households also continue to face financial challenges from inflationary pressures feeding through to higher cost of living. Income, expenditure and savings patterns are continuing to adjust from the pandemic when a combination of Covid restrictions and the furlough scheme resulted in a sharp increase in the household savings ratio. The build-up of savings during that period alongside a pick-up in disposable income growth supported a rebound in expenditure growth in 2021-22.

Over the past year, income growth has continued to rise and was 7.8% in Q2 2023 (on a 4-quarter rolling basis) while individual expenditure growth moderated to 10.1%, having peaked at 19% growth in Q2 2022. The savings ratio has moderated as a result (to 4.9% in Q2 2023) and in recent quarters has fallen to its lowest rates since 2006.

The slowing in individual expenditure growth is reflected in the Scottish Consumer Sentiment Indicator which fell during 2022 and while it has been recovering over 2023, remains notably negative on balance. This has coincided with the slowdown in economic growth and rise in inflationary pressures, with households particularly concerned about the impacts on their personal circumstances including their household's financial security and their confidence to spend money.[11]

The weakness in business investment intentions and consumer sentiment present risks to the outlook for growth. There are variations across forecasts, reflecting the uncertainty in the economic outlook and the extent to which factors such as higher interest rates and weak consumer and business sentiment will impact on growth.

Collectively however, latest GDP growth forecasts illustrate weak growth in the near term. At a UK level, the Bank of England forecast UK economic growth to slow from 0.5% growth in 2023 to flat growth in 2024 (0.0%), while the average of new independent forecasts reported on by HM Treasury forecast 0.5% growth in 2024.[12],[13]

In Scotland, recent forecasts from the Fraser of Allander Institute forecast Scottish economic growth to pick up in 2024, rising from 0.2% to 0.7%, while the EY Scottish ITEM club forecast a more moderate pick-up in GVA growth from 0.2% in 2023 to 0.3% in 2024.[14],[15]

Contact

Email: OCEABusiness@gov.scot